|

시장보고서

상품코드

2073012

책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Responsible AI and Sustainability Governance Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

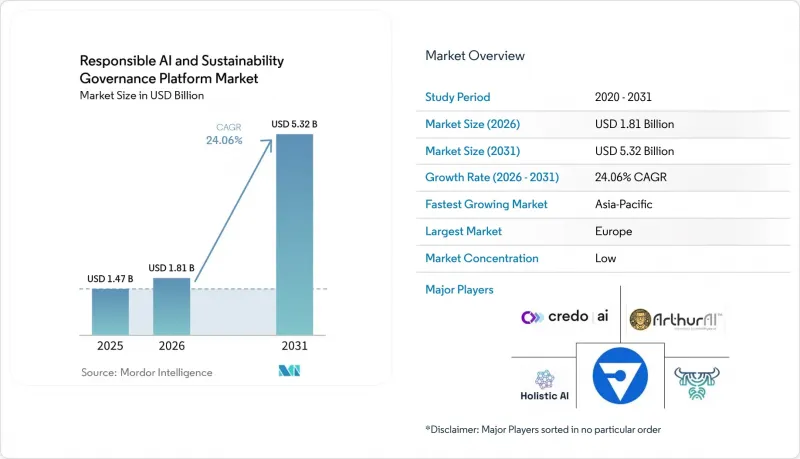

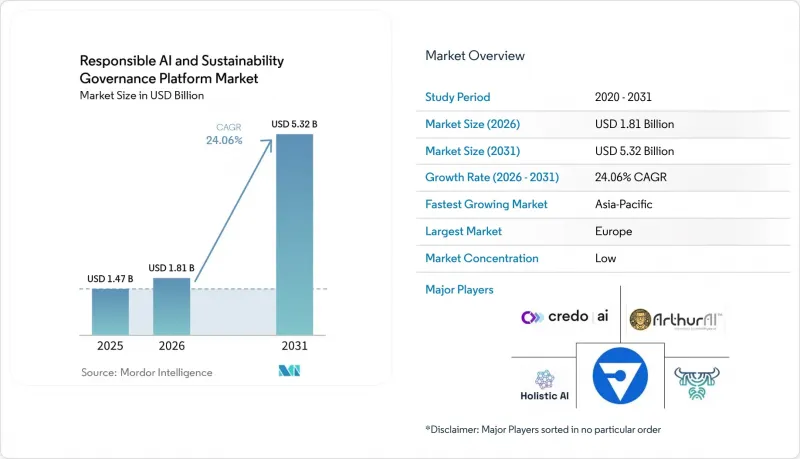

Mordor Intelligence에 의하면, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장 규모는 2025년 14억 7,000만 달러로 평가되었고, 2026년 18억 1,000만 달러로 추정되고, 2031년까지 53억 2,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 24.06%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어 플랫폼 및 서비스), 배포 방식별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업 및 중소기업), 용도별(AI 모델 라이프사이클 거버넌스 등), 최종 이용 산업별(BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장 동향과 인사이트

전 세계 AI 및 지속가능성 공시 요건의 강화

주요 경제권에서 AI 및 지속가능성 보고에 관한 규제 의무가 점차 통일되고 있는 가운데, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장이 급속히 확대되고 있습니다. EU의 옴니버스 I 지침이 2026년 3월 18일에 발효됨에 따라, 유럽에서 중요한 사업을 전개하는 대기업은 더욱 엄격한 공시 범위의 적용을 받게 됨이 확인되었습니다. 이로 인해 거버넌스 관련 지출은 계속해서 기업 규모의 구매자에게 집중될 것입니다. 또한, 미국 증권거래위원회(SEC)는 2026년 5월 29일, 2024년 기후 변화 공시 규정의 철회를 제안했으나, 이는 전 세계 기업의 지배구조 관련 요구를 완화하기는커녕, 유럽과 미국의 정책 격차를 더욱 확대하는 결과를 낳았습니다. 이로 인해, 반응형 AI 및 지속가능성 거버넌스 플랫폼 시장은 여러 관할 구역에 걸쳐 단일 관리 프레임워크가 필요한 다국적 기업에 대한 의존도가 높아지고 있습니다. 또한, AI와 정보 공개에 관한 규정이 각각 다른 일정에 따라 추진되고 있는 가운데, 규정 준수 관련 결정을 미룰 수 없는 기업들의 경우 구매 주기가 단축되는 결과로 이어지고 있습니다.

감사 대응이 가능한 AI 및 ESG 관련 증거 기록에 대한 수요 증가

책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장은 AI 시스템과 지속가능성 공시가 어떻게 작성되고 검토되었는지에 대한 완전한 기록을 남겨야 할 필요성에서도 혜택을 받고 있습니다. OneTrust의 보고서에 따르면, 2025년에는 거버넌스 팀이 AI 위험 관리에 할애하는 시간이 37% 증가할 것으로 예상되며, 이는 수작업에 의한 증거 수집을 유지하기가 점점 더 어려워지고 있는 이유를 여실히 보여주고 있습니다. 기업은 현재 모델의 의사 결정, 정책 승인, 원본 데이터 및 보고 내용의 변경 사항에 대해 처음부터 끝까지 추적 가능함을 입증해야 합니다. NIST의 지침 역시 거버넌스, 측정 및 위험 대응을 체계적으로 문서화할 필요성을 강조하고 있으며, 이를 통해 규제가 엄격한 분야를 넘어선 플랫폼 수요를 뒷받침하고 있습니다. 반응형 AI 및 지속가능성 거버넌스 플랫폼 시장에서는 견고한 감사 로그, 승인 내역 및 증거 보존 기능을 갖춘 공급업체들이 주목받고 있습니다. 이는 AI 감독 절차와 ESG 공시 검토 절차에서 발생할 수 있는 개별적인 문제 발생 위험을 줄여주기 때문입니다.

관할 구역마다 다른 규제 해석

책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장은 기업들이 적용 범위, 법적 구속력, 보고 논리가 서로 다른 다양한 규정을 아우르며 거버넌스 프로그램을 조율하려 노력하고 있기 때문에 여전히 과제에 직면해 있습니다. 유럽에서는 AI 및 지속가능성과 관련된 구속력 있는 요건이 추진되고 있는 반면, 미국에서는 2026년 5월 SEC의 철회 제안에 따라 기후 변화 정보 공개에 대한 연방 정부의 입장이 이전만큼 명확하지 않게 되었습니다. NIST는 여전히 널리 활용되는 AI 위험 관리 프레임워크를 제공하고 있지만, 그 역할은 구속력 있는 규칙집과는 다르기 때문에 다국적 기업들은 특정 지역에서의 형식적인 규정 준수와 다른 지역에서의 위험 기반 관행 사이에서 균형을 맞추어야 하는 상황에 놓여 있습니다. 이러한 상황은 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장의 성장을 둔화시키고 있습니다. 이는 구매자들이 지역별로 최적화된 정책 템플릿, 유연한 문서화 기준, 그리고 시스템 전체를 재구축하지 않고도 변경할 수 있는 보고 로직을 원하기 때문입니다. 또한, 이러한 상황은 여러 법제도에 걸친 규칙 라이브러리 및 워크플로우 설정 업데이트에 드는 지속적인 비용을 감당할 수 있는 대형 벤더에게 유리하게 작용하고 있습니다.

부문별 분석

2025년, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장에서 소프트웨어 플랫폼이 69.85%의 점유율을 차지했습니다. 이는 구매자가 프로젝트 주도형 지원보다 지속적인 관리 시스템을 더 중요하게 여긴다는 것을 보여줍니다. 이 부문은 구독 수익, 내장형 워크플로우, 그리고 거버넌스 규정이 일상 업무에 통합된 후 나타나는 긴 업데이트 주기의 이점을 누리고 있습니다. 기업은 일반적으로 단기적인 지원에만 의존하지 않고, 소프트웨어 내에 정책 라이브러리, 승인 경로, 모델 인벤토리, 증거 저장소를 설정하는 것부터 시작합니다. 거버넌스 로직은 법무, 리스크, 지속가능성, 데이터, 기술 등 여러 팀에 걸쳐 운영되는 경우가 많기 때문에 이러한 접근 방식을 채택할 경우 도입 후 소프트웨어를 교체하기가 어려워집니다. 또한, 대규모 계약의 경우 단일 인터페이스를 통해 지속적인 모니터링, 감사 준비, 부서 간 보고서를 작성할 수 있도록 지원하는 플랫폼이 선호되는 경향이 있습니다.

서비스는 가장 빠르게 성장하고 있는 분야로, 2031년까지의 연평균 성장률(CAGR)은 24.78%에 달할 전망이며, 매출 구성에서 소프트웨어가 주류를 이루고 있음에도 불구하고 도입 작업이 여전히 중요함을 보여줍니다. 업계는 자문, 통합, 워크플로우 설계를 통해 소프트웨어의 사용 편의성을 높이는 모델로 전환되고 있습니다. Credo AI는 2025년 8월에 자문 서비스를 시작했습니다. 이는 거버넌스 원칙을 측정 가능한 운영 관리 조치로 전환하기 위한 실질적인 지원을 원하는 고객 수요가 증가하고 있음을 반영합니다. 서비스의 성장은 소프트웨어가 그 가치를 완전히 발휘하기 전에, 많은 구매자들이 여전히 법무, 규정 준수, 지속가능성, 데이터 팀 간의 내부 책임 조화를 도모하기 위한 지원을 필요로 하고 있다는 사실에서도 기인합니다. 향후 서비스 수요는 초기 도입 작업뿐만 아니라 정책 맞춤 설정, 증거 자료 준비, 관리 조치 테스트 및 변경 관리 분야에서 가장 지속적으로 유지될 것으로 예측됩니다.

2025년, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장에서 클라우드 기반 도입이 66.41%를 차지했습니다. 이는 프로비저닝의 용이성, 신속한 업데이트, 대규모 AI 환경 전반에 걸친 지속적인 모니터링이 뒷받침한 결과입니다. 기업들은 긴 릴리스 주기를 거치지 않고도 다양한 모델에 걸쳐 정책 변경, 승인, 경고를 반영하기를 원하기 때문에 클라우드 제공은 이 시장에 적합합니다. 또한, 사업 부문, 지역, 보고 기능을 아우르는 통합적인 관점이 필요한 공동 거버넌스 팀도 지원합니다. 거버넌스 프로그램이 급속히 확대되고 있거나, 사내 팀이 인프라 관련 부담을 줄이고자 할 때, 구매자들은 종종 클라우드 기반 도구를 선호합니다. 이에 따라 속도, 규모 및 통합 관리가 필요한 조직에게 있어 클라우드는 여전히 가장 일반적인 선택지로 자리 잡고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 25.12%를 나타낼 것으로 예측되며, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장에서 가장 중요한 구조적 변화가 될 것입니다. 이러한 성장을 주도하고 있는 것은 기밀 데이터, 감사 로그 또는 핵심 모델을 온프레미스 환경에 유지하면서 클라우드 기반의 정책 오케스트레이션을 필요로 하는 조직들입니다. 이러한 조합은 주권이나 데이터 소재지 요건이 완전한 클라우드 전환에 현실적인 제약 요인으로 작용하는 은행, 의료, 정부, 중요 인프라 분야에서 특히 중요합니다. ServiceNow가 2026년에 예정하고 있는 'AI Control Tower'의 확장은 벤더가 단일 호스팅 모델을 강요하는 것이 아니라, 다양한 도입 환경을 아우르며 운영 가능한 거버넌스 기능을 구축하고 있음을 보여줍니다. 온프레미스 배포는 규제가 엄격한 워크로드를 대상으로 하는 시장의 일부로 계속 존재하겠지만, 구매자들이 클라우드와 온프레미스 환경 간의 이식성을 점점 더 요구하게 됨에 따라 그 성장 속도는 둔화될 가능성이 높습니다.

지역별 분석

2025년, 유럽은 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장 점유율의 34.56%를 차지했으며, 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 해당 지역이 주도적인 입지를 차지하고 있는 것은 법적 구속력이 있는 지속가능성 보고 의무와 명확한 AI 거버넌스 방향성이 결합되어 있기 때문이며, 이로 인해 구매자들이 플랫폼 도입 결정을 미룰 이유가 줄어들고 있습니다. EU 이사회가 2026년 지속가능성 보고와 관련해 취한 조치는 유럽에서 중요한 사업을 전개하는 대기업을 실질적인 규정 준수 범위 내에 묶어두어, 이를 통해 기업 수요를 지속적으로 뒷받침하고 있습니다. 독일, 프랑스, 영국은 대규모 기업 기반, 보다 엄격한 공시 규범, 그리고 부문 간 거버넌스 프로그램에 대한 자금 지원에 대한 높은 의지를 모두 갖추고 있어, 해당 지역에서의 도입에 있어 여전히 중심적인 역할을 수행하고 있습니다.

북미는 시장 점유율에서 2위를 차지했으며, BFSI(은행 및 금융 및 보험) 및 기술 분야의 주요 기업들이 도입을 주도하고 있습니다. 2026년 5월 미국 증권거래위원회(SEC)가 기후 관련 공시 규정의 철회를 제안함에 따라, 단기적인 연방 차원의 보고 요인 중 하나는 줄어들었지만, 유럽에서 사업을 영위하는 다국적 기업에 대한 지배 구조의 필요성이 사라진 것은 아니었습니다. 이로 인해 국경을 넘어 사업을 전개하는 대기업은 여전히 통일된 거버넌스 체제가 필요한 반면, 일부 중견 국내 기업은 도입 속도를 늦출 수 있게 되는 등 양극화된 시장이 형성되었습니다. 이 지역이 여전히 중요한 이유는 많은 초기 도입 기업들이 AI와 지속가능성을 통합적으로 모니터링할 수 있도록 확장 가능한 데이터, 개인정보 보호 및 모델 거버넌스에 관한 성숙한 역량을 이미 갖추고 있기 때문입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 25.45%로 가장 높은 성장률을 나타낼 것으로 예상되며, 책임있는 AI 및 지속가능성 거버넌스 플랫폼 시장의 주요 성장 지역이 될 전망입니다. 이러한 수요의 상당 부분은 수출 지향 제조업 및 공급망의 투명성과 관련이 있습니다. 해당 지역의 기업들은 고객과의 관계를 통해 유럽 및 미국의 공시 요건의 영향을 받는 경우가 많기 때문입니다. 또한, 기업들이 업무, 고객 참여, 보고 워크플로우에 엔터프라이즈 AI를 더욱 광범위하게 도입함에 따라, 해당 지역에서는 이사회 차원의 AI 거버넌스에 대한 관심도 높아지고 있습니다. 남미는 여전히 신흥 시장이며, 개인정보 보호 규제, 다국적 기업의 자회사, 그리고 대기업의 지속가능성 보고 체계가 강화되고 있는 점이 수요를 뒷받침하고 있습니다. 중동 및 아프리카는 여전히 지역별 부문 중규모가 가장 작은 편이지만, 걸프 국가들의 정부 주도의 디지털화 프로그램 덕분에 공공 서비스, 금융, 대규모 인프라 프로젝트 분야에서 초기 수요가 발생하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the responsible AI and sustainability governance platform market size is projected to expand from USD 1.47 billion in 2025 and USD 1.81 billion in 2026 to USD 5.32 billion by 2031, registering a CAGR of 24.06% between 2026 and 2031.

This report is Segmented by Component (Software Platforms, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (AI Model Lifecycle Governance, and More), End-Use Industry (BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Responsible AI and Sustainability Governance Platform Market Trends and Insights

Tightening Global AI and Sustainability Disclosure Mandates

The responsible AI and sustainability governance platform market is moving faster as regulatory obligations for AI and sustainability reporting are converging across major economies. The EU Omnibus I Directive entered into force on March 18, 2026, and confirmed that large companies with material European exposure remain within a stricter disclosure perimeter, which keeps governance spending focused on enterprise-scale buyers. The SEC proposed rescinding its 2024 climate disclosure rules on May 29, 2026, and that widened the policy gap between Europe and the United States rather than reducing governance needs for global companies. This has made the responsible AI and sustainability governance platform market more dependent on multinational firms that need a single control framework across multiple jurisdictions. It also shortens buying cycles for companies that cannot delay compliance decisions while separate AI and disclosure rules continue to move forward on different timelines.

Rising Demand for Audit-Ready AI and ESG Evidence Trails

The responsible AI and sustainability governance platform market is also benefiting from the need to keep complete records of how AI systems and sustainability disclosures are produced and reviewed. OneTrust reported that governance teams spent 37% more time managing AI risk in 2025, underscoring why manual evidence gathering is becoming harder to sustain. Companies now need proof that model decisions, policy approvals, source data, and reporting changes can be traced from start to finish. NIST guidance also reinforces the need to document governance, measurement, and risk treatment in a structured manner, thereby supporting platform demand beyond highly regulated sectors. In the responsible AI and sustainability governance platform market, vendors with strong audit logs, approval histories, and evidence retention are gaining attention because they reduce the risk of failures in separate AI oversight and ESG disclosure review processes.

Fragmented Regulatory Interpretations Across Jurisdictions

The responsible AI and sustainability governance platform market still faces friction because companies are trying to align governance programs across rules that differ in scope, legal force, and reporting logic. Europe is moving forward with binding AI and sustainability requirements, while the U.S. federal position on climate disclosure has become less direct following the SEC's rescission proposal in May 2026. NIST continues to provide a widely used AI risk management framework, but its role is different from that of a binding rulebook, leaving multinational companies to balance formal compliance in one region with risk-based practices in another. This slows the responsible AI and sustainability governance platform market because buyers want localized policy templates, flexible documentation standards, and reporting logic that can change without a full system rebuild. It also favors larger vendors that can absorb the recurring cost of updating rule libraries and workflow settings across several legal regimes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Generative AI and Agentic AI Requiring Continuous Governance

- Shift Toward Cloud-Native Governance Architecture and Centralized Control

- High Integration Complexity Across AI, ESG, and Enterprise Data Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms captured 69.85% of the responsible AI and sustainability governance platform market in 2025, showing that buyers are prioritizing persistent control systems over project-led support. This segment benefits from subscription revenue, embedded workflows, and long replacement cycles once governance rules are integrated into daily operations. Enterprises typically begin by setting up policy libraries, approval paths, model inventories, and evidence stores within software, rather than relying solely on short-term support. That approach makes software harder to displace after deployment, since governance logic often spans legal, risk, sustainability, data, and technology teams simultaneously. The largest contracts also tend to favor platforms that can support ongoing monitoring, audit preparation, and cross-functional reporting from one interface.

Services are the fastest-growing component, with a 24.78% CAGR through 2031, underscoring that implementation work remains critical even as software dominates the revenue mix. The industry is moving toward a model where advisory, integration, and workflow design accelerate software usability. Credo AI launched advisory services in August 2025, reflecting growing customer demand for hands-on help in translating governance principles into measurable operating controls. Services growth also stems from the fact that many buyers still need support aligning internal ownership across legal, compliance, sustainability, and data teams before software can deliver full value. Over time, service demand is likely to remain strongest in policy customization, evidence readiness, control testing, and change management rather than only in first-time deployment work.

Cloud-based deployment accounted for 66.41% of the responsible AI and sustainability governance platform market in 2025, supported by easier provisioning, faster updates, and continuous monitoring across large AI estates. Cloud delivery fits this market because enterprises want policy changes, approvals, and alerts to move across many models without long release cycles. It also supports shared governance teams that need one view across business units, geographies, and reporting functions. Buyers often prefer cloud-based tools when governance programs are expanding quickly, and internal teams want less infrastructure overhead. This keeps cloud as the default path for organizations that need speed, scale, and centralized administration.

Hybrid deployment is projected to grow at a 25.12% CAGR through 2031, making it the most important structural shift inside the responsible AI and sustainability governance platform market. Growth is coming from organizations that want cloud-based policy orchestration while keeping sensitive data, audit logs, or core models in on-premises environments. That mix is especially relevant in banking, healthcare, government, and critical infrastructure, where sovereignty and residency requirements remain practical limits to full cloud migration. ServiceNow's 2026 expansion of AI Control Tower shows how vendors are building governance functions that can operate across deployment settings, rather than requiring a single hosting model. On-premises deployment will remain part of the market for highly restricted workloads, but its growth is likely to remain slower as buyers increasingly seek portability across cloud and on-premises environments.

Complete Report Scope:

- By Component

- Software Platforms

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Application

- AI Model Lifecycle Governance

- Risk and Compliance Management

- Bias, Fairness, and Explainability Management

- Auditability and Evidence Management

- By End-Use Industry

- IT and Telecom

- BFSI

- Industrial Manufacturing

- Energy and Utilities

- Oil and Gas

- Retail and E-Commerce

- Construction and Infrastructure

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 34.56% of the responsible AI and sustainability governance platform market share in 2025, making it the largest regional contributor. The region leads because it combines binding sustainability reporting obligations with a clear AI governance direction, giving buyers fewer reasons to delay platform decisions. The EU Council's 2026 action on sustainability reporting kept large companies with material European operations within a meaningful compliance perimeter, and that continues to support enterprise demand. Germany, France, and the United Kingdom remain central to regional adoption because they combine large corporate bases, stronger disclosure discipline, and greater readiness to fund cross-functional governance programs.

North America held the second-largest share of the market, with adoption led by large enterprises in BFSI and technology. The SEC's May 2026 proposal to rescind climate-related disclosure rules reduced one near-term federal reporting driver, but it did not remove governance needs for multinational firms with European exposure. This created a split market where large cross-border companies still need unified governance infrastructure, while some domestic mid-market buyers can move more slowly. The region remains important because many early adopters already had mature data, privacy, and model governance capabilities that can be extended into combined AI and sustainability oversight.

Asia-Pacific is projected to register the fastest growth at 25.45% CAGR through 2031, making it the key expansion region for the responsible AI and sustainability governance platform market. Much of that demand is tied to export manufacturing and supply-chain transparency, since firms in the region are often pulled into Western disclosure expectations through customer relationships. The region is also seeing stronger board-level attention to AI oversight as companies deploy more enterprise AI across operations, customer engagement, and reporting workflows. South America remains an emerging market, with demand supported by privacy regulation, multinational subsidiaries, and increasing sustainability reporting discipline among larger corporates. The Middle East and Africa is still the smallest regional segment, but government-led digital programs in the Gulf are creating early demand in public services, finance, and large-scale infrastructure projects.

- Credo AI, Inc.

- ArthurAI, Inc.

- Fiddler Labs, Inc.

- Monitaur, Inc.

- Holistic AI Limited

- DataRobot, Inc.

- Dataiku, Inc.

- Domino Data Lab, Inc.

- H2O.ai, Inc.

- OneTrust, LLC

- Persefoni AI, Inc.

- Plan A GmbH

- Sweep SAS

- Watershed Technology, Inc.

- Novisto Inc.

- Greenly SAS

- Datamaran Limited

- EcoOnline Global Limited

- Novata, Inc.

- Position Green Group AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Global AI and Sustainability Disclosure Mandates

- 4.2.2 Rising Enterprise Demand for Audit-Ready AI and ESG Evidence Trails

- 4.2.3 Expansion of Generative AI and Agentic AI Requiring Continuous Governance

- 4.2.4 Shift Toward Cloud Native Governance Architecture and Centralized Control

- 4.2.5 Convergence of AI Risk, Data Governance, and Sustainability Compliance Workflows

- 4.2.6 Board-Level Demand for Quantifiable Trust, Transparency, and Responsible Innovation

- 4.3 Market Restraints

- 4.3.1 Fragmented Regulatory Interpretations Across Jurisdictions

- 4.3.2 High Integration Complexity Across AI, ESG, and Enterprise Data Stacks

- 4.3.3 Shortage of Specialized AI Governance and Sustainability Compliance Talent

- 4.3.4 Budget Deferral Among Mid-Market Buyers Facing Multi-System Implementation Costs

- 4.4 Impact of Macroeconomic Factors on The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 AI Model Lifecycle Governance

- 5.4.2 Risk and Compliance Management

- 5.4.3 Bias, Fairness, and Explainability Management

- 5.4.4 Auditability and Evidence Management

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Oil and Gas

- 5.5.6 Retail and E-Commerce

- 5.5.7 Construction and Infrastructure

- 5.5.8 Government and Public Sector

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Credo AI, Inc.

- 6.4.2 ArthurAI, Inc.

- 6.4.3 Fiddler Labs, Inc.

- 6.4.4 Monitaur, Inc.

- 6.4.5 Holistic AI Limited

- 6.4.6 DataRobot, Inc.

- 6.4.7 Dataiku, Inc.

- 6.4.8 Domino Data Lab, Inc.

- 6.4.9 H2O.ai, Inc.

- 6.4.10 OneTrust, LLC

- 6.4.11 Persefoni AI, Inc.

- 6.4.12 Plan A GmbH

- 6.4.13 Sweep SAS

- 6.4.14 Watershed Technology, Inc.

- 6.4.15 Novisto Inc.

- 6.4.16 Greenly SAS

- 6.4.17 Datamaran Limited

- 6.4.18 EcoOnline Global Limited

- 6.4.19 Novata, Inc.

- 6.4.20 Position Green Group AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment