|

시장보고서

상품코드

2073013

소매 및 전자상거래 IT 지속가능성 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Retail and E-Commerce IT Sustainability Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

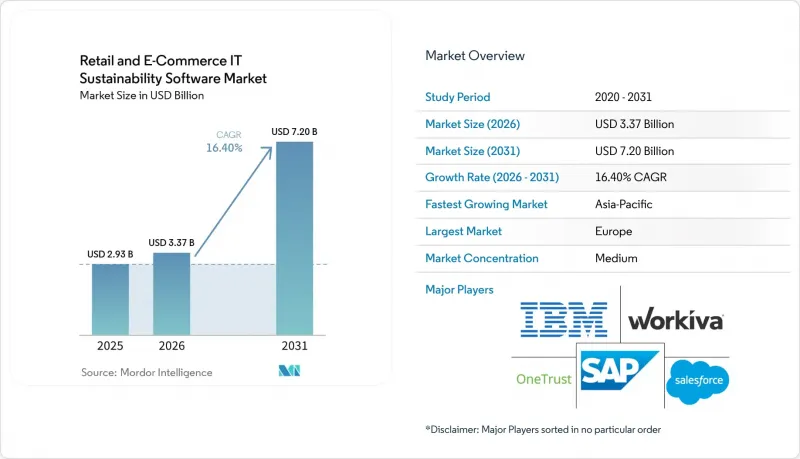

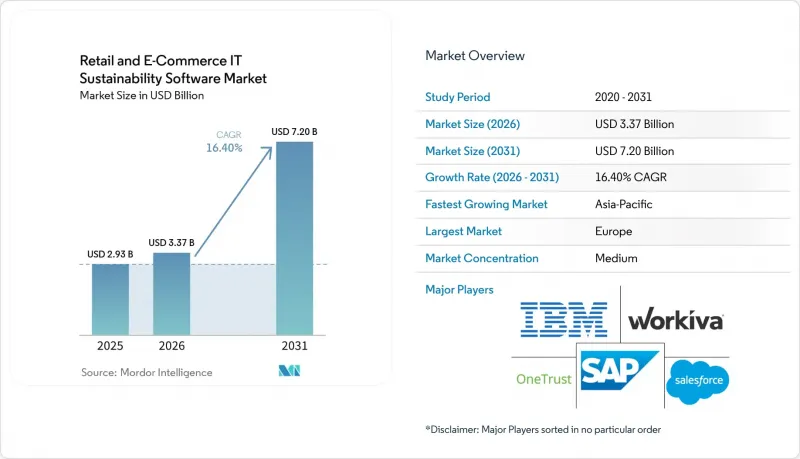

Mordor Intelligence에 의하면, 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장 규모는 2025년 29억 3,000만 달러로 평가되었고, 2026년 33억 7,000만 달러로 추정되고, 2031년까지 72억 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 16.40%를 나타낼 전망입니다.

본 보고서는 제공 형태별(소프트웨어 및 서비스), 도입 형태별(클라우드, 하이브리드 등), 기업 규모별(대기업 및 중소기업), 기능별(탄소 회계 및 배출량 관리 소프트웨어, 지속가능성 보고 및 공시 소프트웨어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장 동향과 인사이트

ESG 공시 및 감사 대응을 위한 규정 준수

규제 상의 공시 요건은 단기간 내에 여러 소매 시장에서 자발적인 보고에서 법적 구속력이 있는 규정 준수로 전환되고 있으며, 이러한 변화가 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 플랫폼 구매를 가속화하고 있습니다. 유럽에서는 2026년 3월에 CSRD 관련 개정안이 시행됨에 따라, 대상 대기업에 대해 ESRS를 준수하는 보고 의무가 유지되었기 때문에 체계적이고 반복 가능한 보고 워크플로우에 기반한 공시 시스템에 대한 수요가 지속되고 있습니다. 다음으로, 소비자 대상의 환경 주장에서 비롯된 압박이 있습니다. '소비자 권한 강화 지침'이 2026년 9월 27일에 발효되며, 그 감독 범위가 연례 보고서에서 소매업체 및 전자상거래 사업자가 사용하는 상품 페이지, 포장, 배송 관련 연락 내용까지 확대되기 때문입니다. 또한, 인도에서는 2026-27 회계연도에 대규모 상장 기업에 대한 BRSR Core의 보증 요건이 확대되었습니다. 이로 인해 소매 그룹 및 해당 발행사와 제휴하는 공급업체의 경우, 감사에 따른 보고 부담이 더욱 가중될 것입니다. 그 결과, 소매 및 전자상거래(EC)용 IT 지속가능성 소프트웨어 시장에서는 여러 프레임워크를 지원하며, 문서화 기록을 보관하고, 동일한 소매업체가 서로 다른 보고 제도를 동시에 충족해야 하는 경우에도 활용 가능한 출력을 생성할 수 있는 플랫폼이 선호되고 있습니다. 단일 프레임워크 구성에 의존하는 벤더는 도입 속도가 둔화될 우려가 있습니다. 이는 소매업체들이 도입 작업을 다시 진행하지 않고도 규제 변경에 대응할 수 있는 시스템을 점점 더 필요로 하고 있기 때문입니다.

소매업체에 스코프 3 및 제품의 환경 발자국에 대한 일관성을 입증하라는 압박

소매 및 전자상거래 IT 지속가능성 소프트웨어 시장은 구매자의 기대가 직접적으로 변화하고 있는 데 힘입어 성장하고 있습니다. 소매업체들은 현재 스코프 3 산정 및 지속가능성 관련 주장을 뒷받침하기 위해 제품 수준 및 공급업체 수준의 증거를 필요로 하고 있기 때문입니다. 많은 소매 밸류체인에서 하류 공급업체에 대한 가시성은 여전히 낮은 편이므로, 상업적 과제는 단순히 데이터를 수집하는 것뿐만 아니라, 업스트림와의 관계를 기밀 사항으로 간주하는 공급업체로부터 신뢰할 수 있는 데이터를 확보하는 데에도 있습니다. Worldly사는 2026년 2월, 자사의 'Product Impact Calculator'를 260개 이상의 소비재 카테고리에 걸쳐 있는 40만 개 제품으로 확대했습니다. 이는 제품 수준의 Scope 3 모델링이 제한적인 시범 단계에서 보다 광범위한 실제 운영 단계로 전환되고 있음을 보여줍니다. 이러한 변화가 중요한 이유는 디지털 제품 여권 의무화가 특정 범주에 영향을 미치기 훨씬 전부터 소매업체들이 1차 공급업체 데이터와 진위 여부를 입증할 수 있는 품목별 기록을 필요로 하고 있기 때문입니다. 따라서 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서는 단순히 광범위한 지출 기반의 추정치에 의존하기보다는 Tier 2 및 Tier 3 공급업체로부터 제공된 정보를 검증하고, 정규화하며, 연계할 수 있는 공급업체가 높이 평가받고 있습니다. 고액 계약은 단순히 대략적인 탄소 발자국을 산출하는 데 그치지 않고, 감사나 고객 검토 시 소매업체가 제품에 대한 주장을 입증하는 데 도움이 되는 도구로 점차 전환되고 있습니다.

ERP, PIM, POS, 공급망 시스템 간의 높은 통합 비용

소매 및 전자상거래 IT 지속가능성 소프트웨어 시장은 여전히 큰 장벽에 직면해 있습니다. 이는 소매업체가 제품, 거래, 공급업체, 재고, 물류를 위해 이미 사용하고 있는 시스템에 지속가능성 플랫폼을 연동하는 데 드는 비용입니다. 많은 옴니채널 소매업체들은 5-7개의 주요 엔터프라이즈 시스템을 운영하고 있으며, 데이터 모델이 일관되지 않을 경우 이러한 환경들을 연동하는 데 드는 비용은 소프트웨어 라이선스 자체의 가치에 육박할 정도로 높아질 수 있습니다. 클라우드 도입이 확대되면서 기반 인프라는 개선되었지만, API 표준화나 벤더 생태계 간 데이터 구조의 일관성을 확보하는 데 필요한 작업이 사라진 것은 아닙니다. SAP의 'Sustainability Control Tower'에 관한 2026년 로드맵 업데이트에서도 내장형 보고 기능과 광범위한 ERP 연결성의 중요성이 강조되고 있으며, 이는 구매자들이 여전히 원천 단계에서의 통합 부담을 줄여주는 시스템을 얼마나 중요하게 여기는지를 반영하고 있습니다. 이러한 부담이 가장 큰 분야는 중견 기업 시장으로, 구식 아키텍처와 소규모 도입 팀으로 인해 도입 주기가 길어지면서 규정 준수 달성 시기가 늦어지고 있습니다. 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서는 각 단계별로 맞춤형 통합이 필요하지 않고, 공급업체들이 인증된 커넥터와 미리 구축된 소매 워크플로를 제공하게 됨에 따라 도입이 가속화될 전망입니다.

부문별 분석

2025년, 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 소프트웨어가 69.45%를 차지했습니다. 이는 탄소 회계, ESG 공시, 공급망 분석, 시나리오 모델링 등 각 분야에서 플랫폼 계층이 여전히 지출의 중심을 차지하고 있음을 뒷받침하는 것입니다. 이러한 집중 현상이 나타난 배경에는 대형 소매업체들이 공급업체에 대한 데이터 요청, 공개 자료 작성, 혹은 지속가능성 계획을 여러 사업 부문으로 확대하기 전에, 우선 거버넌스가 확립된 '시스템 오브 레코드'가 필요했던 적이 있습니다. 또한, 소프트웨어 계층은 소매업체가 장기적인 운영 서비스보다 플랫폼 선정, 내부 데이터 구조 및 보고 관리를 우선시한, 기업 구매의 초기 단계와도 일치합니다. 그런 의미에서 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장은 기반 플랫폼이 예산 배분의 첫 물결을 이끌어낸, 과거 기업 소프트웨어 주기에서 나타났던 패턴을 따랐습니다. 그렇다고는 해도, 소프트웨어가 초기 단계에서 주도권을 잡았다고 해서 서비스가 부차적인 것은 아닙니다. 왜냐하면 구매자 수요에서 다음 단계로 넘어가면, 도입의 질, 감사 지원, 그리고 시스템 전반에 걸친 설정에 점점 더 초점이 맞추어지고 있기 때문입니다.

서비스 시장은 2026-2031년 연평균 성장률(CAGR) 16.92%를 나타낼 것으로 예측되며, 이는 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장이 라이선싱 단계에서 일상적인 운영 단계로 전환되고 있음을 보여줍니다. 스프레드시트 중심의 ESG 워크플로우에서 벗어나려는 소매업체들은 플랫폼을 안심하고 활용할 수 있게 되기 전에, 데이터 마이그레이션, 커넥터 설정, 거버넌스 설계 및 첫 번째 주기의 보고와 관련된 지원이 필요한 경우가 많습니다. 컴플라이언스 체계가 지속적으로 발전함에 따라, 소매업체들은 업무 흐름의 논리, 통제 및 문서화 기준을 정기적으로 업데이트해야 하며, 지속적인 지원에 대한 필요성도 높아지고 있습니다. Workiva가 보유한 다중 프레임워크 지원 보고서의 작성 및 자동화 분야의 강점은 고객이 초기 도입 단계에서 정기적인 보고서 작성 주기로 전환해 나가는 과정에서 소프트웨어와 탄탄한 서비스를 결합한 공급업체가 유리한 입장에 있는 이유를 여실히 보여줍니다. 따라서 소매 및 전자상거래 IT 지속가능성 소프트웨어 업계는 관계 중심적인 시장으로 변화하고 있으며, 관리형 지원 및 자문 서비스가 계약 갱신 및 업셀링 결정 과정에서 더 큰 역할을 수행하게 되었습니다. 플랫폼과 병행하여 확장성이 뛰어난 서비스 팀을 구축하는 벤더는 시간이 지남에 따라 지속적인 규정 준수 관련 지출에서 더 큰 비중을 차지할 가능성이 높습니다.

2025년에는 클라우드 도입이 66.12%의 점유율을 차지할 것으로 예상되며, 이는 SaaS 방식의 제공 형태와 현대의 소매업체 및 전자상거래 기업이 채택하고 있는 분산형 운영 모델 간의 궁합이 매우 뛰어나다는 점을 반영하고 있습니다. 클라우드 시스템은 국가, 사업 부문, 보고 팀을 넘나들며 확장하기 쉬우며, 공시 템플릿, 패키징 규칙 또는 보고 로직이 변경될 때도 신속하게 업데이트할 수 있습니다. 따라서, 장기간에 걸친 현지 인프라 프로젝트를 기다리지 않고 다자간 보고 체계를 구축하고자 하는 소매업체들에게 클라우드는 현실적인 첫 번째 선택지가 되었습니다. 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 클라우드 시장 규모가 계속해서 선두를 달리고 있는 이유는 기업의 구매 담당자들이 여전히 통합 관리, 유지보수 부담 경감, 새로운 기능에 대한 손쉬운 접근을 중요하게 여기기 때문입니다. 반면, 공급업체의 기록, 자사 브랜드 데이터, 또는 관할 구역별 거버넌스 요건으로 인해 보다 엄격한 데이터 관리가 요구되는 경우, 순수한 클라우드만으로는 반드시 충분하다고 할 수 없습니다.

하이브리드 시장 규모는 2026-2031년 연평균 성장률(CAGR) 16.78%로 확대될 것으로 예상되며, 이는 기업 구매자들이 '전부 아니면 전무'라는 아키텍처보다 유연성을 더욱 추구하고 있음을 보여줍니다. 소매업체는 보고서 작성 규모 확대 및 협업을 위해 클라우드를 활용하는 한편, 상업적으로 기밀성이 높은 기록은 거버넌스가 적용된 로컬 환경이나 온프레미스 환경에 보관할 수 있습니다. SAP의 2026년판 '지속가능성 컨트롤 타워' 업데이트에서는 이 모델이 지지를 얻고 있는 이유가 밝혀졌습니다. 이 회사는 좁은 의미의 단일 스택 구성이 아닌, 감사에 대응할 수 있는 보고서 작성, AI를 통한 지원, 그리고 다양한 ERP 환경을 아우르는 폭넓은 지원 범위를 강조했습니다. 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서도 하이브리드 도입이 확대됨에 따라 관련 서비스에 대한 수요가 증가하고 있습니다. 이는 소매업체들이 시스템 간에 미들웨어, 오케스트레이션 및 관리형 데이터 계보가 필요하기 때문입니다. 장기적으로 볼 때, 하이브리드 모델은 보고서 작성 규모 확대와 공급업체 관련 기밀 정보의 엄격한 관리가 모두 필요한 대규모 옴니채널 사업자에게 가장 매력적인 선택지가 될 것입니다. 신뢰성이 높은 하이브리드 옵션을 갖추지 못한 공급업체는 비교적 단순한 이용 사례에서는 여전히 존재 가치를 유지할 수 있겠지만, 더 복잡한 엔터프라이즈 프로그램 프로젝트를 놓칠 위험이 있습니다.

지역별 분석

2025년, 유럽은 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장의 34.56%를 차지했으며, 해당 기간 동안 매출에서 가장 큰 비중을 차지한 지역이 되었습니다. 이 지역의 위상은 소매업 보고, 포장 관련 의무, 그리고 소비자를 대상으로 한 환경 관련 주장에 동시에 영향을 미치는 수많은 지속가능성 규제의 존재에서 기인합니다. 2026년에도 CSRD(기업 지속가능성 보고 지침)와 관련된 변화가 활발히 진행되는 한편, '포장 및 포장 폐기물에 관한 규정' 및 '소비자 권한 강화 지침'으로 인해, 연차 보고서부터 제품 홍보 및 전자상거래상의 표시 사항에 이르기까지 업무상의 부담이 커졌습니다. 또한 영국에서는 오해를 불러일으킬 수 있는 환경 주장에 대한 감시를 지속적으로 강화함으로써 수요를 지속적으로 창출해 왔으며, 유럽 소비자에게 서비스를 제공하는 소매업체의 경우 거버넌스 및 문서화 요건이 높은 수준으로 유지되었습니다. 이러한 상황에서 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장 규모는 대형 다국적 기업뿐만 아니라, 고객 및 공급업체와의 관계를 통해 발생하는 규정 준수 요구에 부응해야 하는 중견 기업들에 의해서도 뒷받침되고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 17.12%를 나타낼 것으로 예측되며, 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 2025년부터 2027년에 걸쳐 일본, 호주, 한국, 싱가포르, 중국, 인도를 포함한 여러 주요 경제권에서 ISSB 기준에 부합하거나 확대된 지속가능성 공시 요건이 거의 동시에 도입됨에 따라 뒷받침되고 있습니다. 또한, 해당 지역이 전 세계 소매 공급망의 주요 생산 거점인 만큼, 소프트웨어 수요는 국내 상장 기업의 규제뿐만 아니라 수출 의존도 및 소매업체가 주도하는 공급업체에 대한 요구에 의해서도 견인되고 있습니다. 이러한 이중적인 압박으로 인해 제조업체, 조달 파트너, 소매 그룹이 동일한 규정 준수 데이터 체인에 통합됨에 따라, 아시아태평양에서는 보다 광범위한 도입 기반이 형성되고 있습니다.

북미는 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 점유율이나 성장률 면에서 지역 1위를 차지하지는 않지만, 상업적으로는 여전히 중요한 위치를 차지하고 있습니다. 2026년, 연방 정부 차원의 불확실성이 커지는 상황 속에서도 캘리포니아주의 기후 정보 공개 체계는 여전히 그 중요성을 유지하며, 해당 주에서 사업을 영위하는 대형 소매업체들의 소프트웨어 수요를 지속시키는 데 기여했습니다. 남미는 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장에서 규모는 작지만 활발한 지역이며, 특히 브라질에서는 기업들이 수출과 관련된 지속가능성에 대한 기대치와 현지 보고 관행을 준수하고 있다는 점이 두드러집니다. 2025년 하반기에 SAP가 'Sustainability Footprint Management'를 브라질 상파울루 AWS 리전으로 확장한 것은 현지 상황에 최적화된 탄소 회계 인프라에 대한 이러한 수요 증가를 반영한 것입니다. 중동에서는 대형 소매 그룹과 각국의 지속가능성 정책이 보다 우수한 ESG 데이터 인프라 구축을 추진하고 있어 이에 대한 관심이 높아지고 있습니다. 한편, 아프리카는 여전히 초기 단계에 있으며, 도입은 수출 지향 기업이나 상장 기업에 집중되어 있습니다. 이 지역 전체에서 소매 및 전자상거래 IT 지속가능성 소프트웨어 시장 규모는 확대되고 있지만, 도입 속도는 여전히 규제 집행의 엄격성과 대형 소매업체들이 공급업체와의 계약에 데이터 요건을 어느 정도 확실하게 반영하고 있는지에 크게 좌우되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the retail and e-commerce IT sustainability software market size is projected to expand from USD 2.93 billion in 2025 and USD 3.37 billion in 2026 to USD 7.20 billion by 2031, registering a CAGR of 16.40% between 2026 and 2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud, Hybrid, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Functionality (Carbon Accounting and Emissions Management Software, Sustainability Reporting and Disclosure Software, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Retail and E-Commerce IT Sustainability Software Market Trends and Insights

Regulatory Compliance for ESG Disclosure and Audit Readiness

Regulatory disclosure requirements have moved from voluntary reporting into binding compliance across several retail markets within a short period, and that shift is accelerating platform purchases in the retail and e-commerce IT sustainability software market. In Europe, CSRD-related amendments entered into force in March 2026 and maintained ESRS-aligned reporting obligations for large in-scope companies, thereby preserving demand for disclosure systems built on structured, repeatable reporting workflows. The next layer of pressure comes from consumer-facing environmental claims, as the Empowering Consumers Directive takes effect on September 27, 2026, and extends scrutiny from annual reports to product pages, packaging, and delivery communications used by retailers and e-commerce operators. India also expanded BRSR Core assurance requirements for large listed companies for the fiscal year 2026-27, which adds another audit-driven reporting burden for retail groups and suppliers tied to those issuers. As a result, the retail and e-commerce IT sustainability software market is favoring platforms that can support multiple frameworks, preserve documentation trails, and produce outputs that remain usable when the same retailer must satisfy different reporting regimes simultaneously. Vendors that rely on single-framework configurations face slower adoption, as retailers increasingly need systems that can absorb regulatory changes without restarting implementation work.

Retailer Pressure to Prove Scope 3 and Product Footprint Integrity

The retail and e-commerce IT sustainability software market is benefiting from a direct shift in buyer expectations, as retailers now need product- and supplier-level evidence to support Scope 3 accounting and sustainability claims. Lower-tier supplier visibility remains weak across many retail value chains, so the commercial problem is not only collecting data but also securing reliable data from suppliers that view their upstream relationships as sensitive. Worldly expanded its Product Impact Calculator to 400,000 products across more than 260 consumer goods categories in February 2026, which shows that product-level Scope 3 modeling is moving beyond narrow pilots and into broader operational use. That change matters because retailers need primary supplier data and defensible item-level records well before Digital Product Passport obligations begin affecting selected categories. The retail and e-commerce IT sustainability software market is, therefore, rewarding vendors that can validate, normalize, and link Tier 2 and Tier 3 supplier inputs rather than relying solely on broad spend-based estimates. Premium contract value is shifting toward tools that help retailers defend product claims during audits and customer reviews, not just calculate a high-level carbon footprint.

High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems

The retail and e-commerce IT sustainability software market still faces a significant barrier: the cost of connecting sustainability platforms to the systems retailers already use for products, transactions, suppliers, inventory, and logistics. Many omnichannel retailers operate across 5 to 7 major enterprise systems, and the cost of linking those environments can approach the value of the software license itself when data models do not align. Stronger cloud adoption has improved baseline infrastructure, but it has not removed the work needed to standardize APIs and reconcile data structures across vendor ecosystems. SAP's 2026 roadmap updates for Sustainability Control Tower also highlighted the importance of embedded reporting and broad ERP connectivity, which reflects how much buyers still value systems that reduce integration effort at the source. This burden is heaviest in the mid-market, where legacy architecture and smaller implementation teams lengthen deployment cycles and delay compliance gains. The retail and e-commerce IT sustainability software market is likely to see faster adoption as vendors offer certified connectors and prebuilt retail workflows, rather than requiring custom integration at each step.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms

- AI-Enabled Sustainability Reporting and Exception Detection

- Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 69.45% of the retail and e-commerce IT sustainability software market in 2025, which confirmed that the platform layer remained the center of spending across carbon accounting, ESG disclosure, supply chain analytics, and scenario modeling. This concentration developed because large retailers first needed a governed system of record before they could scale supplier data requests, disclosure preparation, or sustainability planning across multiple business units. The software layer also aligns with the first phase of enterprise buying, where retailers prioritized platform selection, internal data structure, and reporting controls over longer-term operational services. In that sense, the retail and e-commerce IT sustainability software market followed a pattern seen in earlier enterprise software cycles, where foundational platforms attracted the first wave of budget allocation. Even so, the early software lead does not mean services are secondary, because the next stage of buyer demand is increasingly focused on implementation quality, audit support, and cross-system configuration.

Services are projected to grow at a 16.92% CAGR from 2026 to 2031, indicating that the retail and e-commerce IT sustainability software market is shifting from license acquisition to everyday operational use. Retailers moving away from spreadsheet-led ESG workflows often need support for data migration, connector setup, governance design, and first-cycle reporting before they can rely on the platform with confidence. The need for recurring support is also rising as compliance frameworks continue to evolve, requiring retailers to regularly update workflow logic, controls, and documentation standards. Workiva's strength in multi-framework reporting and automation illustrates why providers that pair software with service depth are positioned well as customers move from initial deployment into repeat reporting cycles. The retail and e-commerce IT sustainability software industry is therefore becoming more relationship-driven, with managed support and advisory execution playing a larger role in renewal and upsell decisions. Vendors that build scalable services teams alongside the platform are likely to capture a greater share of recurring compliance spending over time.

Cloud deployment captured a 66.12% share in 2025, reflecting the strong fit between SaaS delivery and the distributed operating model used by modern retailers and e-commerce groups. Cloud systems are easier to scale across countries, business units, and reporting teams, and they support faster updates when disclosure templates, packaging rules, or reporting logic change. That made cloud a practical first choice for retailers looking to set up multi-country reporting without waiting for lengthy local infrastructure projects. The retail and e-commerce IT sustainability software market size for cloud remained ahead because enterprise buyers still value centralized administration, lower maintenance burden, and easier access to new features. At the same time, pure cloud is not always sufficient when supplier records, private-label data, or jurisdiction-specific governance requirements require tighter data control.

Hybrid deployment is projected to expand at a 16.78% CAGR from 2026 to 2031, which signals that enterprise buyers increasingly want flexibility rather than an all-or-nothing architecture. Retailers can use the cloud for reporting scale and collaboration while keeping commercially sensitive records in governed, local, or on-premises environments. SAP's 2026 Sustainability Control Tower updates showed why this model is gaining traction: the company emphasized audit-ready reporting, AI support, and broader coverage across different ERP environments rather than a narrow, single-stack setup. The retail and e-commerce IT sustainability software market is also seeing adjacent service demand rise as hybrid adoption increases, since retailers need middleware, orchestration, and controlled data lineage across systems. Over time, hybrid will appeal most to large omnichannel operators that need both reporting scale and tighter handling of supplier-sensitive information. Vendors without credible hybrid options may remain relevant in simpler use cases, but they risk losing more complex enterprise programs.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Functionality

- Carbon Accounting and Emissions Management Software

- Sustainability Reporting and Disclosure Software

- Supply Chain ESG and Supplier Sustainability Management

- Sustainability Analytics, Forecasting and Scenario Modeling

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Europe accounted for 34.56% of the retail and e-commerce IT sustainability software market in 2025, making it the leading regional contributor to revenue during the period. The region's position stems from the density of sustainability rules that affect retail reporting, packaging obligations, and consumer-facing environmental claims simultaneously. CSRD-related changes remained active in 2026, while the Packaging and Packaging Waste Regulation and the Empowering Consumers Directive added operational pressure that extends from annual reporting into product communication and e-commerce presentation. The United Kingdom also continued to shape demand by tightening oversight of misleading environmental claims, which kept governance and documentation requirements high for retailers serving European consumers. Within this setting, the retail and e-commerce IT sustainability software market size remains supported not only by large multinationals but also by mid-market operators that must respond to compliance expectations flowing through their customer and supplier relationships.

Asia-Pacific is projected to grow at a 17.12% CAGR from 2026 to 2031, which makes it the fastest-growing region in the retail and e-commerce IT sustainability software market. Growth is being supported by a near-concurrent rollout of ISSB-aligned or expanded sustainability disclosure requirements across several major economies, including Japan, Australia, South Korea, Singapore, China, and India, during the 2025 to 2027 window. The region's role as the main production base for many global retail supply chains also means software demand is driven by export exposure and retailer-led supplier requests, not solely by domestic listed company regulation. That dual pressure gives Asia-Pacific a broader adoption base, as manufacturers, sourcing partners, and retail groups are drawn into the same compliance data chain.

North America remains commercially important, even though the retail and e-commerce IT sustainability software market is not the regional leader in either share or growth rate. California's climate disclosure pathway continued to matter in 2026, even as federal uncertainty increased, helping preserve software demand among large retailers doing business in the state. South America is a smaller but active part of the retail and e-commerce IT sustainability software market, with Brazil standing out as a region where companies align with export-linked sustainability expectations and local reporting practices. SAP's extension of Sustainability Footprint Management into the Brazil Sao Paulo AWS region in late 2025 reflected this growing demand for localized carbon accounting infrastructure. The Middle East is seeing rising interest as large retail groups and national sustainability agendas push for better ESG data infrastructure, while Africa remains earlier stage, with adoption centered on export-oriented and listed entities. Across these geographies, the retail and e-commerce IT sustainability software market is expanding in scope, but adoption speed still depends heavily on the strength of regulatory enforcement and on how firmly large retailers embed data requirements in supplier contracts.

- SAP SE

- Salesforce, Inc.

- IBM Corporation

- Workiva Inc.

- OneTrust, LLC

- Diligent Corporation

- EcoVadis SAS

- Sphera Solutions, Inc.

- Enablon SA

- Intelex Technologies ULC

- Cority Software Inc.

- Persefoni AI, Inc.

- Novisto Inc.

- Greenstone Limited

- Datamaran Limited

- Benchmark Digital Partners LLC

- UL LLC

- Wolters Kluwer N.V.

- Watershed

- Position Green

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Compliance for ESG Disclosure and Audit Readiness

- 4.2.2 Retailer Pressure to Prove Scope 3 and Product Footprint Integrity

- 4.2.3 Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms

- 4.2.4 AI-Enabled Sustainability Reporting and Exception Detection

- 4.2.5 Omnichannel Retail Complexity Increasing Traceability Demand

- 4.2.6 Supplier Scorecarding for Sustainable Procurement and Private Label Risk Control

- 4.3 Market Restraints

- 4.3.1 High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems

- 4.3.2 Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks

- 4.3.3 Shortage of Retail Sustainability Analytics Talent and ESG Control Owners

- 4.3.4 Reporting Standard Volatility Causing Reconfiguration and Compliance Rework

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Functionality

- 5.4.1 Carbon Accounting and Emissions Management Software

- 5.4.2 Sustainability Reporting and Disclosure Software

- 5.4.3 Supply Chain ESG and Supplier Sustainability Management

- 5.4.4 Sustainability Analytics, Forecasting and Scenario Modeling

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Salesforce, Inc.

- 6.4.3 IBM Corporation

- 6.4.4 Workiva Inc.

- 6.4.5 OneTrust, LLC

- 6.4.6 Diligent Corporation

- 6.4.7 EcoVadis SAS

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Enablon SA

- 6.4.10 Intelex Technologies ULC

- 6.4.11 Cority Software Inc.

- 6.4.12 Persefoni AI, Inc.

- 6.4.13 Novisto Inc.

- 6.4.14 Greenstone Limited

- 6.4.15 Datamaran Limited

- 6.4.16 Benchmark Digital Partners LLC

- 6.4.17 UL LLC

- 6.4.18 Wolters Kluwer N.V.

- 6.4.19 Watershed

- 6.4.20 Position Green

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment