|

시장보고서

상품코드

2073016

통신 네트워크 에너지 효율화 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Telecom Network Energy Efficiency Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

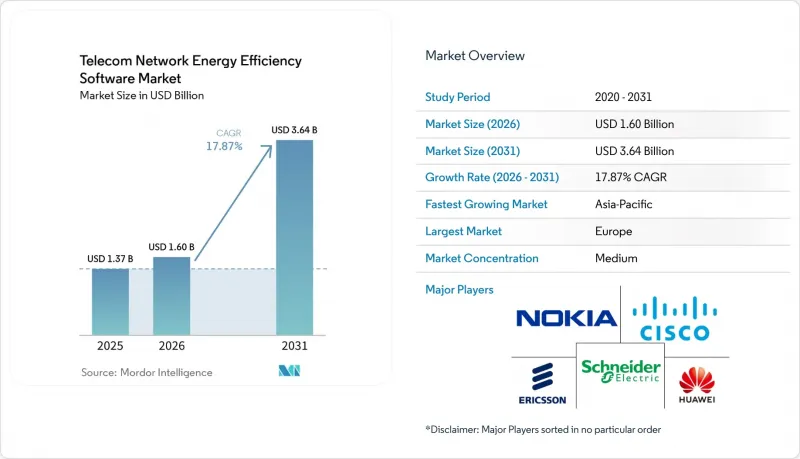

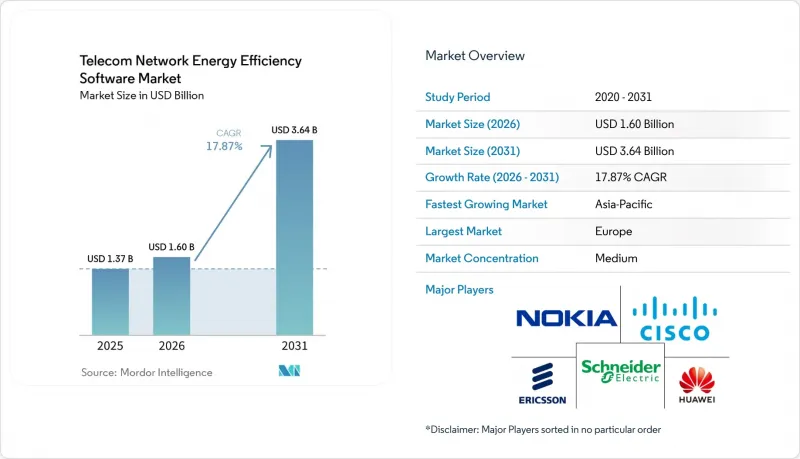

Mordor Intelligence에 의하면, 통신 네트워크 에너지 효율화 소프트웨어 시장 규모는 2025년에 13억 7,000만 달러로 평가되었고 2026년부터 2031년까지 CAGR 17.87%로 확대되어 2031년에는 36억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 솔루션 유형(에너지 모니터링·가시화 소프트웨어, 에너지 분석·보고서 작성 소프트웨어 등), 도입 형태(클라우드/SaaS, On-Premise, 하이브리드), 최종 사용자(모바일 네트워크 사업자, 네트워크 인프라 제공업체 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 통신 네트워크 에너지 효율화 소프트웨어 시장 동향 및 인사이트

증가하는 5G RAN의 에너지 소비량

5G는 기존 네트워크 세대보다 더 큰 에너지 부하를 초래하기 때문에 통신 네트워크의 에너지 효율화 소프트웨어 시장이 확대되고 있습니다. Massive MIMO의 활용 확대와 도시 지역의 네트워크 밀도 증가로 인해 사이트 수준의 전력 수요가 늘어나면서, 가동 중인 네트워크의 운영 비용이 상승하고 있습니다. 2025년 조사에 따르면, 영국의 5G 에너지 수요는 다양한 트래픽 시나리오 하에서 2030년까지 급증할 가능성이 있으며, 특히 도시 지역에서는 소비 밀도가 높아질 것으로 나타났습니다. 이러한 운영 방식에서는 수요 증가만으로는 효율적인 에너지 이용으로 이어지지 않으므로, 고정된 하드웨어 설정의 유효성은 떨어집니다. 따라서 통신 네트워크 에너지 효율화 소프트웨어 시장에서는 다양한 기기 환경에서 절전 모드, 캐리어 셧다운, 사이트 수준의 최적화를 통합적으로 제어할 수 있는 소프트웨어에 대한 수요가 증가하고 있습니다. 통신 사업자가 단일 하드웨어 스택 내부가 아닌, 혼합된 장비 전체에서 비용 절감을 도모할 경우, 벤더 고유의 네트워크 관리 계층을 넘어 운영할 수 있는 벤더가 더 유리한 입장에 있습니다.

AI를 활용한 폐쇄 루프형 전력 절약 기술의 발전

통신 네트워크의 에너지 효율화 소프트웨어 시장도 발전하고 있습니다. AI 기반의 폐쇄 루프형 도구가 시범 단계에 머무르지 않고, 현재 통신 사업자의 실제 운영 환경에 도입되기 시작했기 때문입니다. 에릭슨에 따르면, 이 회사의 "지능형 에너지 효율화" 기능을 통해 2025년 시범 운영 당시, 영국 보다폰의 선정된 거점에서 5G 무선 장치의 일일 전력 소비량을 최대 33%까지 절감할 수 있었습니다고 합니다. 이 결과는 소프트웨어에 의한 판단이 무선 계층에서 측정 가능한 에너지 성과로 직접 이어진다는 점에서 중요합니다. 또한, 최적화 도구는 각 통신사의 네트워크에서 트래픽 패턴과 설정 동작을 학습함에 따라 성능이 향상되기 때문에 시간이 지남에 따라 전환 비용이 증가하게 됩니다. 통신 네트워크 에너지 효율화 소프트웨어 시장에서는 조기에 본격적인 도입을 확보하고, 그 모델을 기반으로 보다 광범위한 서비스 관계를 구축할 수 있는 벤더가 우위를 점할 가능성이 높을 것입니다. 이것이 바로 유력한 기존 기업들이 AI 소프트웨어를 자동화 플랫폼 및 관리형 제공 지원과 결합하고 있는 이유 중 하나입니다.

OSS, RAN 및 전력 시스템 전반에 걸친 통합의 복잡성

통신 네트워크 에너지 효율화 소프트웨어 시장은 여전히 큰 도입 장벽에 직면해 있습니다. 그 이유는 에너지 플랫폼이 종종 서로 다른 데이터 표준을 사용하는 OSS 환경, RAN 시스템 및 사이트 전력 인프라에 연결되어야 하기 때문입니다. 이로 인해 통신 사업자가 에너지 절감 효과의 추정치를 신뢰하거나 제어 조치를 대규모로 자동화할 수 있게 되기까지는 긴 엔지니어링 주기가 필요합니다. 에릭슨과 노키아는 2026년 3월, 자율형 네트워크 용도 공급업체 간의 상호 운용성을 향상시키기 위해 rApp 생태계 및 SMO 마켓플레이스에서의 협력을 확대하면서 이 문제를 인정했습니다. 이러한 움직임은 주요 공급업체들조차 통합 과정에서 발생하는 마찰을 개별 고객의 문제가 아닌 시장 전반에 걸친 제약으로 인식하고 있음을 보여줍니다. 통신 네트워크 에너지 효율화 소프트웨어 시장에서 통합 기간이 길어지면 예산 결정이 지연될 가능성이 있습니다. 이는 통신 사업자가 도입 비용을 라이선스 비용뿐만 아니라 사내 엔지니어링 소요 시간을 통해 산정하기 때문입니다. 이로 인해 전력 소비 절감으로 인한 비즈니스상의 이점이 이미 명확히 드러난 경우에도 도입이 지연되고 있습니다.

부문별 분석

2025년에는 소프트웨어가 매출의 69.45%를 차지하며, 통신 네트워크 에너지 효율화 소프트웨어 시장의 핵심 수익원이 되었습니다. 이는 라이선싱 기반의 모니터링, 분석, 최적화 및 자동화 플랫폼이 통신 사업자의 지출에서 핵심적인 역할을 하고 있음을 반영합니다. 통신 사업자들이 통합 지원, 관리형 최적화 및 지속적인 모델 유지보수에 대한 의존도를 높여감에 따라, 서비스 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 18.25%를 기록하며 성장할 것으로 전망됩니다. 통신 네트워크 에너지 효율화 소프트웨어 시장에서 소프트웨어 부문 시장 규모가 여전히 큰 이유는 통신 사업자가 보다 광범위한 관리형 서비스로 사업을 확장하기 전에 도입 과정의 대부분이 플랫폼 선정 단계에서 시작되기 때문입니다. 노키아는 이미 지속적인 재교육과 AI 기반 유지보수를 중심으로 한 제품 및 서비스를 제공하고 있으며, 이는 소프트웨어 및 서비스가 동일한 예산 범위를 놓고 경쟁하기보다는 점점 더 하나로 통합되어 갑니다는 생각을 뒷받침하고 있습니다.

이러한 변화는 통신 네트워크의 에너지 효율화를 위한 소프트웨어 업계의 경쟁 행태에 있어 중요한 의미를 지닙니다. 왜냐하면 매니지드형 서비스를 통해 초기 도입 단계를 거친 후에도 공급업체와의 관계가 더욱 지속될 가능성이 있기 때문입니다. 이 서비스가 주간 보고, 비용 절감 효과 검증, 운영 워크플로우의 일부가 된다면, 전환 비용은 더 이상 소프트웨어 교체에만 그치지 않게 됩니다. 직원 재교육, 서비스 수준 조정, 모델 재구성 역시 전환 비용에 포함됩니다. 이는 2024년 및 2025년 초반에 본격적인 운영을 시작한 공급업체들 사이에서 지속적인 수익 집중 현상이 나타나고 있음을 뒷받침하는 것입니다. 따라서 통신 네트워크 에너지 효율화 소프트웨어 시장에서 해당 서비스는 초기 플랫폼 판매 이후 고객 가치를 확대함으로써 수익화 격차를 해소하고 있습니다. 그 결과, 소프트웨어가 현재의 수익 기반이 되고, 서비스가 장기적인 고객 유지를 더욱 공고히 하는 구조가 형성되었습니다.

2025년 기준으로, 에너지 모니터링 및 시각화 소프트웨어는 통신 네트워크 에너지 효율화 소프트웨어 시장 점유율의 28.74%를 차지하고 있는 반면, AI 기반 전력 최적화 소프트웨어는 2031년까지 연평균 성장률(CAGR) 18.65%를 나타낼 것으로 예측됩니다. 모니터링 분야가 주도적인 위치를 차지하게 된 것은 통신 사업자가 분석, 최적화 또는 자동화를 신뢰할 수 있게 되기 전에 안정적인 가시성 계층이 필요하기 때문입니다. 이러한 순서에 따라 모니터링 업체에게는 초기 우위가 생깁니다. 왜냐하면, 사이트 데이터를 처음에 수집하고 정리하는 시스템이 이후의 구매 결정을 좌우하는 경우가 많기 때문입니다. 동시에, AI를 통한 최적화는 가동 중인 네트워크의 전력 절약과 소프트웨어의 작동을 보다 직접적으로 연결해 주기 때문에 더 많은 예산이 배정되고 있습니다. 통신 네트워크 에너지 효율화 소프트웨어 시장에서 AI 기반 전력 최적화 분야는 통신 사업자들이 가시화 단계를 넘어 동적 네트워크 제어를 통해 재현 가능한 효율 향상을 추구함에 따라 성장하고 있습니다.

또한, 통신 사업자들이 배출량 및 에너지 거버넌스와 관련하여 감사 가능한 결과를 점점 더 필요로 하고 있기 때문에 에너지 분석 및 보고서 작성 소프트웨어의 중요성도 높아지고 있습니다. 이에 따라 분석의 역할은 사내 운영 도구에서 대외 보고 요건으로 확대되고 있습니다. 에너지 관리 및 자동화 소프트웨어도 병행하여 발전하고 있으며, 특히 통신 사업자가 소프트웨어의 기능을 '권장'에서 "실행"으로 전환하려는 시도가 그 배경에 있습니다. 2026년 5월, 라쿠텐 모바일과 KDDI는 2030년까지 가상 기지국 및 모바일 데이터센터의 전력 소비량을 40% 감축하는 것을 목표로 하는 NEDO 지원 프로그램에 선정되었습니다. 이는 이 분야에서 현재 고조되고 있는 자동화에 대한 열망의 규모를 여실히 보여주고 있습니다. 따라서 통신 네트워크 에너지 효율화 소프트웨어 시장은 통신 사업자들이 단일하고 획일적인 경로를 따르기보다는 성숙도가 각기 다른 단계에서 이 분야에 진입함에 따라, 여러 솔루션 계층을 동시에 지원하고 있습니다. 이러한 계층 구조 덕분에, 특정 솔루션이 다른 솔루션을 완전히 대체할 가능성은 낮아집니다.

지역별 분석

2025년, 유럽은 통신 네트워크 에너지 효율화 소프트웨어 시장 점유율의 34.56%를 차지하며, 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 이 지역의 위상은 더욱 견고한 정책 체계, 통신 사업자들의 더욱 두드러진 지속가능성 프로그램, 그리고 AI 기반 에너지 관리 도구의 조기 상용화에 힘입어 공고해졌습니다. 유럽연합 집행위원회 공동연구센터는 2026년 1월에 ‘통신 네트워크의 지속가능성에 관한 행동 강령’을 공표함으로써, 네트워크 효율화 관련 의사결정 과정에서 규정 준수의 기반을 강화했습니다. 또한 BEREC도 인프라 공유 체계를 통해 지원을 강화함으로써, 이 지역의 보다 효율적인 네트워크 설계 및 운영을 위한 노력을 뒷받침했습니다. 도이체 텔레콤, 테리아, 텔레2는 모두 배출량 감축에서 큰 진전을 보고하고 있으며, 이는 유럽 내 에너지 효율화 소프트웨어 조달이 단기적인 비용 절감 프로그램이 아니라 장기적인 네트워크 및 거버넌스 의사결정과 연계되어 있음을 보여줍니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 18.45%를 나타낼 것으로 예측되며, 통신 네트워크 에너지 효율화 소프트웨어 시장에서 가장 두드러진 성장을 보일 지역 부문이 될 전망입니다. 해당 지역에서는 대규모 네트워크 구축과 다양해지는 통신 사업자의 특성이 맞물려, SaaS 도입과 보다 고도화된 자동화 모두에 대한 수요를 뒷받침하고 있습니다. 2026년 5월, 라쿠텐 모바일과 KDDI는 가상화된 기지국 및 모바일 데이터센터의 전력 소비 감축에 초점을 맞춘 NEDO의 조사 프로그램에 공동으로 선정되었습니다. 이는 소프트웨어 중심의 효율화 프로그램에 대한 공공 및 상업적 지원이 확대되고 있음을 보여줍니다. 또한, 인도네시아와 필리핀에서 노키아가 선보인 SaaS 실제 운영 사례는 동남아시아의 통신 네트워크 에너지 효율화 소프트웨어 시장에 신뢰할 수 있는 실제 운영 실적을 제공합니다.

북미는 전력 가격 상승 압력으로 인해 사이트 및 엣지에서의 전력 사용량을 줄일 수 있는 소프트웨어에 대한 수요가 뒷받침되고 있어, 통신 네트워크 에너지 효율화 소프트웨어 시장에서 여전히 중요한 위치를 차지하고 있습니다. 미국 에너지정보청(EIA)은 소매 전력 가격이 2026년까지 계속 상승할 것으로 전망하고 있으며, 이에 따라 통신 사업자들은 수요 측 제어 및 효율화 소프트웨어에 계속해서 주력하게 될 것입니다. 남미에서는 도시 지역의 5G 프로그램이 네트워크 밀도를 확대함에 따라 보다 엄격한 에너지 관리의 필요성이 대두되면서, 제한적인 기회가 생겨나고 있습니다. 중동 및 아프리카의 상황은 여전히 제각각이며, 네트워크의 자율성을 높이는 것을 목표로 하는 통신 사업자가 있는 반면, 디젤 연료에 의존하는 기지국의 경제성이나 보다 견고한 감시 인프라의 필요성에 직접적으로 밀려나고 있는 사업자도 존재합니다. 따라서 통신 네트워크 에너지 효율화 소프트웨어 시장에서는 지역별로 구매 우선순위가 서로 다르며, 유럽은 규제와 성숙한 도입 측면에서 주도적인 입지를 차지하고 있고, 아시아태평양은 성장률 면에서 선두를 달리고 있으며, 기타 지역은 비용 압박, 인프라 규모, 현지 운영상의 제약 등이 복잡하게 얽힌 가운데 발전하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the telecom network energy efficiency software market size was valued at USD 1.37 billion in 2025 and is forecast to reach USD 3.64 billion by 2031 at a CAGR of 17.87% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Solution Type (Energy Monitoring and Visibility Software, Energy Analytics and Reporting Software, and More), Deployment Mode (Cloud/SaaS, On-Premises, and Hybrid), End User (Mobile Network Operators, Network Infrastructure Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Telecom Network Energy Efficiency Software Market Trends and Insights

Rising 5G RAN Energy Intensity

The telecom network energy efficiency software market is expanding because 5G creates a heavier energy burden than earlier network generations. Higher use of Massive MIMO and denser urban network layers is increasing site-level power needs and raising the cost of operating live networks. A 2025 study showed that 5G energy demand in the United Kingdom could rise sharply by 2030 under different traffic scenarios, with especially high consumption density in urban areas. That operating pattern makes static hardware settings less effective, because demand growth alone does not translate into efficient energy use. The telecom network energy efficiency software market is therefore seeing stronger demand for software that can orchestrate sleep modes, carrier shutdown, and site-level optimization across diverse equipment environments. Vendors that can operate above vendor-specific network management layers are in a stronger position when operators seek savings across mixed estates rather than within a single hardware stack.

AI-Driven Closed-Loop Power Saving Gains

The telecom network energy efficiency software market is also advancing, as AI-based closed-loop tools are now being deployed in live operator environments rather than remaining in pilot phases. Ericsson said its Intelligent Energy Efficiency capabilities reduced daily 5G radio unit power consumption by up to 33% at selected Vodafone UK sites during a 2025 trial. That result matters because it ties software decisions directly to measurable energy outcomes at the radio layer. It also raises switching costs over time, since optimization tools improve as they learn traffic patterns and configuration behavior from each operator's network. The telecom network energy efficiency software market is likely to reward vendors that secure early production deployments and then build a wider service relationship around those models. This is one reason the strongest incumbents are pairing AI software with automation platforms and managed delivery support.

Integration Complexity Across OSS, RAN, And Power Systems

The telecom network energy efficiency software market still faces a significant adoption barrier because energy platforms must connect to OSS environments, RAN systems, and site power infrastructure that often use different data standards. This creates a long engineering cycle before operators can trust savings estimates or automate control actions at scale. Ericsson and Nokia acknowledged this issue in March 2026 when they expanded cooperation across the rApp Ecosystem and SMO Marketplace to improve cross-vendor interoperability for autonomous network applications. That move shows that even leading suppliers see integration friction as a broad market constraint rather than a one-off customer problem. In the telecom network energy efficiency software market, long integration periods can delay budget decisions because operators measure deployment cost through internal engineering time as much as through license fees. This slows rollout even when the business case for lower power consumption is already visible.

Other drivers and restraints analyzed in the detailed report include:

- Cloud SaaS Adoption for Multi-Vendor Network Operations

- ESG Reporting and Net-Zero Compliance Pressure

- Legacy Site Telemetry And Metering Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 69.45% of revenue in 2025, making it the core revenue driver of the telecom network energy efficiency software market. This reflected the central role of licensed monitoring, analytics, optimization, and automation platforms in operator spending. Services are projected to grow at an 18.25% CAGR from 2026 to 2031, as operators rely more on integration support, managed optimization, and ongoing model maintenance. The telecom network energy efficiency software market size for software remained larger because most deployments still begin with a platform decision before operators expand into wider managed engagements. Nokia has already positioned its offering around continuous retraining and AI maintenance, which supports the idea that software and services are increasingly moving together rather than competing for the same budget line.

That shift matters for competitive behavior in the telecom network energy efficiency software industry because managed delivery can make vendor relationships more durable after the first implementation stage. Once a provider becomes part of weekly reporting, savings validation, and operating workflows, the cost of switching is no longer limited to replacing software. Staff retraining, service-level alignment, and model reconfiguration are also included in the exit cost. This supports recurring revenue concentration among suppliers that entered live deployments early in 2024 and 2025. In the telecom network energy efficiency software market, services are therefore closing the monetization gap by extending account value after the initial platform sale. The result is a component mix where software anchors present revenue and services support deeper account retention over time.

Energy Monitoring and Visibility Software held 28.74% of the telecom network energy efficiency software market share in 2025, while AI-Based Power Optimization Software is projected to grow at an 18.65% CAGR through 2031. Monitoring led because operators need a stable observability layer before they can trust analytics, optimization, or automation. That sequence gives monitoring vendors an early advantage, since the first system to collect and organize site data often shapes later purchasing decisions. At the same time, AI optimization is attracting stronger budgets because it links software actions more directly to power savings in live networks. The telecom network energy efficiency software market for AI-based power optimization is growing as operators move beyond visibility and seek repeatable efficiency gains from dynamic network control.

Energy Analytics and Reporting Software is also gaining importance because operators increasingly need auditable outputs for emissions and energy governance. That broadens the role of analytics from an internal operational tool to an external reporting requirement. Energy Management and Automation Software is developing in parallel, especially as operators seek to move software from recommendation to execution. In May 2026, Rakuten Mobile and KDDI were selected for a NEDO-backed program that aims to reduce the power consumption of virtualized base stations and mobile data centers by 40% by 2030, underscoring the scale of automation ambition now building in the sector. The telecom network energy efficiency software market, therefore, supports multiple solution layers simultaneously, because operators enter the stack at different maturity points rather than following a single uniform path. This layered structure reduces the chance that one solution type fully displaces the others.

Complete Report Scope:

- By Component

- Software

- Services

- By Solution Type

- Energy Monitoring and Visibility Software

- Energy Analytics and Reporting Software

- AI-Based Power Optimization Software

- Energy Management and Automation Software

- By Deployment Mode

- Cloud/SaaS

- On-Premises

- Hybrid

- By End User

- Mobile Network Operators

- Tower Companies

- Internet Service Providers

- Network Infrastructure Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 34.56% of the telecom network energy efficiency software market share in 2025, which made it the leading regional contributor. The region's position was supported by a stronger policy framework, more visible operator sustainability programs, and earlier commercialization of AI-based energy tools. The European Commission Joint Research Center published the Code of Conduct for the Sustainability of Telecommunications Networks in January 2026, which strengthened the compliance backdrop for network efficiency decisions. BEREC also added support through its infrastructure-sharing framework, which reinforced the region's push toward more efficient network design and operation. Deutsche Telekom, Telia, and Tele2 all reported major progress on emissions reduction, which shows that energy software procurement in Europe is tied to long-cycle network and governance decisions rather than short-lived cost programs.

Asia-Pacific is projected to grow at an 18.45% CAGR from 2026 to 2031, making it the fastest-growing regional segment in the telecom network energy efficiency software market. The region combines large network rollouts with a widening set of operator profiles, which supports demand for both SaaS adoption and deeper automation. In May 2026, Rakuten Mobile and KDDI were jointly selected for an NEDO research program focused on reducing power consumption in virtualized base stations and mobile data centers, which shows rising public and commercial support for software-led efficiency programs. Nokia's live SaaS deployments in Indonesia and the Philippines also give the telecom network energy efficiency software market credible production references in Southeast Asia.

North America remains an important part of the telecom network energy efficiency software market because electricity price pressure supports demand for software that can reduce site and edge power use. The U.S. Energy Information Administration said retail electricity prices were expected to continue rising through 2026, which keeps operators' focus on demand-side control and efficiency software. South America presents a selective opportunity in which urban 5G programs are expanding network density and increasing the need for more disciplined energy management. The Middle East and Africa remain a mixed region, with some operators pursuing greater network autonomy while others are driven more directly by diesel-heavy site economics and the need for stronger monitoring foundations. This leaves the telecom network energy efficiency software market with different purchase priorities by region, where Europe leads on regulation and mature deployment, Asia-Pacific leads on growth, and other regions advance through a mix of cost pressure, infrastructure scale, and local operational constraints.

- Tupl Inc.

- AirHop Communications, Inc.

- iMBrace Limited

- Recenso Services Ltd.

- TowerSight AI

- Polystar AB

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Cisco Systems, Inc.

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Elisa Industriq

- Vertiv Holdings Co

- Honeywell International Inc.

- Qualcomm Technologies

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising 5G RAN Energy Intensity

- 4.2.2 AI-Driven Closed-Loop Power Saving Gains

- 4.2.3 Cloud SaaS Adoption For Multi-Vendor Network Operations

- 4.2.4 ESG Reporting And Net-Zero Compliance Pressure

- 4.2.5 Autonomous RAN Optimization For Sleep Mode And Carrier Shutdown

- 4.2.6 Energy Price Volatility In Tower And Edge Operations

- 4.3 Market Restraints

- 4.3.1 Legacy Site Telemetry And Metering Gaps

- 4.3.2 Integration Complexity Across OSS, RAN, And Power Systems

- 4.3.3 Cybersecurity And Data Sovereignty Concerns

- 4.3.4 Long Payback Period For Retrofits In Brownfield Networks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Solution Type

- 5.2.1 Energy Monitoring and Visibility Software

- 5.2.2 Energy Analytics and Reporting Software

- 5.2.3 AI-Based Power Optimization Software

- 5.2.4 Energy Management and Automation Software

- 5.3 By Deployment Mode

- 5.3.1 Cloud/SaaS

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Mobile Network Operators

- 5.4.2 Tower Companies

- 5.4.3 Internet Service Providers

- 5.4.4 Network Infrastructure Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tupl Inc.

- 6.4.2 AirHop Communications, Inc.

- 6.4.3 iMBrace Limited

- 6.4.4 Recenso Services Ltd.

- 6.4.5 TowerSight AI

- 6.4.6 Polystar AB

- 6.4.7 Nokia Corporation

- 6.4.8 Telefonaktiebolaget LM Ericsson

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 ZTE Corporation

- 6.4.11 Cisco Systems, Inc.

- 6.4.12 Siemens AG

- 6.4.13 Schneider Electric SE

- 6.4.14 ABB Ltd.

- 6.4.15 Elisa Industriq

- 6.4.16 Vertiv Holdings Co

- 6.4.17 Honeywell International Inc.

- 6.4.18 Qualcomm Technologies

- 6.4.19 Juniper Networks, Inc.

- 6.4.20 Mavenir Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment