|

시장보고서

상품코드

2073072

IT-OT 융합 하드웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)IT-OT Convergence Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

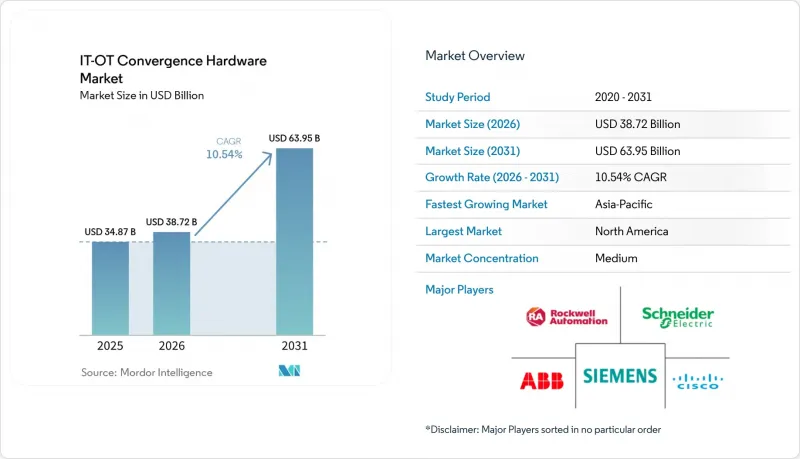

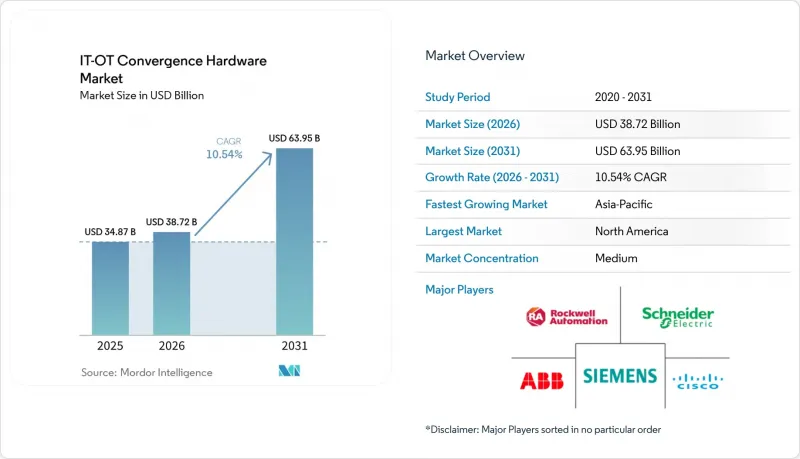

Mordor Intelligence에 의하면, IT-OT 융합 하드웨어 시장 규모는 2025년 348억 7,000만 달러에서 2026년에는 387억 2,000만 달러로 확대되어 2031년까지 639억 5,000만 달러에 이를 것으로 예상되고 있어 2026-2031년까지 CAGR 10.54%로 성장할 전망입니다.

본 보고서는 구성 요소별(산업용 이더넷 스위치 및 라우터, 산업용 게이트웨이 및 엣지 디바이스, 기타), 산업별(제조업, 에너지 및 유틸리티, 석유 및 가스, 기타), 기업 규모별(대기업, 중소기업), 연결 방식별(유선, 무선), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계 IT-OT 융합 하드웨어 시장 동향과 인사이트

엣지 컴퓨팅 게이트웨이의 도입 확대

엣지 게이트웨이는 데이터센터에서 생산 라인으로 연산 처리를 이전함으로써 왕복 지연 시간을 50-100밀리초에서 15밀리초 이하로 단축하여, 폐쇄 루프 제어 시스템의 20밀리초 이하라는 제한을 충족시킵니다. 미국 국립표준기술연구소(NIST)는 주로 가동 중단 시간 단축과 대역폭 비용 절감을 통해 2025년 이산 제조 부문에서 엣지 프로젝트의 투자 대비 효과가 10-20배에 달할 것으로 추정하고 있습니다. 사이버보안 및 인프라 보안국(CISA)이 2025년 12월부터 암호화된 장치 ID의 탑재를 의무화한 데 따라, 각 게이트웨이 공급업체들은 현재 Trusted Platform Module 2.0(TPM 2.0) 칩을 통합하고 있습니다. 듀얼 SIM을 지원하는 5G 무선 모듈과 멀티포트 기가비트 이더넷이 표준 사양으로 자리 잡아가고 있으며, 이를 통해 하나의 링크에 장애가 발생하더라도 결정론적인 트래픽을 유지할 수 있는 하이브리드 백홀 채널이 구현됩니다. 이러한 성능 및 보안 향상으로 인해 기업들은 레거시 스위치보다 엣지 하드웨어를 우선시하는 분산형 인텔리전스 아키텍처로 전환하고 있습니다.

IT 및 OT 네트워크를 아우르는 통합 사이버 보안에 대한 수요

새로운 규제로 인해, 과거 운영 기술(OT)을 보호하던 기존의 ‘ 에어 갭”가 무너져 가고 있습니다. CISA가 2025년 8월에 발표한 지침에 따르면, 모든 OT 자산에 대한 지속적이고 수동적인 감지가 의무화되어 있으며, 실시간 제어 메시지를 방해하지 않으면서 산업용 프로토콜을 검사하는 장치를 사용할 것을 권장하고 있습니다. 유럽연합(EU)의 NIS2 지침에 따라, 사고 보고를 소홀히 할 경우 엄격한 벌금이 부과됨에 따라 18개 주요 부문 전반에서 시스템 업그레이드가 가속화되고 있습니다. 이에 대해 각 하드웨어 벤더들은 IEC 62443-4-2 인증을 획득하여 대응하고 있으며, 포티넷의 견고한 방화벽 시리즈는 그 초기 사례 중 하나입니다. 독일의 개정된 KRITIS 규정에 따라, 2025년에는 유사한 세분화 규정이 유틸리티 및 화학 플랜트로도 확대되었습니다. 이러한 규제들이 복합적으로 작용함에 따라, 보안 기능은 단순한 선택적 부가 기능에서 구매의 핵심 기준으로 그 위상이 높아지고 있습니다.

레거시 시스템과의 비호환성과 막대한 개조 비용

많은 플랜트에서는 이더넷 포트가 없는 1990년대에 설치된 컨트롤러를 여전히 운용하고 있으며, 게이트웨이를 추가할 때는 프로토콜 변환기를 사용하거나 장기간 가동을 중단할 수밖에 없습니다. 2025년 조사에 따르면, 공정 제조업체의 60%가 적어도 하나의 에어갭 네트워크를 유지하고 있으며, 이로 인해 데이터가 분할되어 분석이 복잡해지고 있습니다. IEC 61511에 따른 안전 계장 시스템의 재검증에는 6-12개월이 소요될 수 있으며, 그 결과 통합 프로젝트는 플랜트의 정기 유지보수 기간까지 미뤄지게 됩니다. Stuxnet 공격의 여파가 여전히 남아 있는 탓에, 위험을 회피하려는 경향이 강해지면서 경영진은 레거시 자산을 기업 네트워크에 연결하는 것을 주저하고 있습니다. 이러한 통합상의 장벽으로 인해 인건비가 높아져, 그린필드 방식 도입에 비해 총 비용이 2배가 됩니다.

부문별 분석

엣지 디바이스는 성장의 주목을 받으며 연평균 12.72%의 성장률을 기록했으나, 2025년 IT-OT 융합 하드웨어 시장 규모에서는 산업용 이더넷 스위치와 라우터가 31.35%라는 압도적인 점유율을 차지했습니다. 게이트웨이에는 현재 컨테이너 런타임 환경이 내장되어 있어, 예측 알고리즘을 로컬에서 실행함으로써 클라우드로 데이터를 전송하는 데 드는 비용을 절감할 수 있습니다. 기업들이 제로 트러스트 세분화을 도입함에 따라, IEC 62443-4-2 인증을 획득한 보안 어플라이언스가 차세대 급성장 분야로 부상하고 있습니다. 한편, 스위치 제조업체들은 침입 감지 기능을 탑재함으로써 자사의 사업 기반을 지키고 있지만, 가격 프리미엄을 정당화할 수 있는 분석 기능을 추가하지 못한다면 상품화될 위험이 다가오고 있습니다.

OPC UA Field eXchange는 독자적인 사양의 필드버스로 인한 락인 현상을 위협하고 있기 때문에 차별화의 초점은 사이버 보안, 온보드 AI 가속기, 산업별 인증으로 옮겨가고 있습니다. 델과 휴렛 팩커드 엔터프라이즈(Hewlett Packard Enterprise)는 유전에서의 도입을 확대하기 위해, 컨포멀 코팅 처리를 거치고 광범위한 온도 범위를 지원하는 견고한 엣지 서버를 각각 출시했습니다. 동시에, NVIDIA Jetson을 탑재한 게이트웨이는 머신 비전 워크로드가 랙에서 공장 현장으로 이동하고 있음을 보여주는 실제 사례입니다. 그 결과, 엣지 하드웨어가 데이터 스트림을 실시간으로 해석하고, 결정론적 스위치가 시간적 제약이 엄격한 트래픽에 대해 서브마이크로초 단위의 동기화를 보장하는 다층적인 아키텍처가 형성되어 있으며, 이를 통해 두 카테고리 모두 보다 광범위한 IT-OT 융합 하드웨어 시장에서 필수적인 존재로 자리매김하고 있습니다.

2025년에는 제조업이 41.27%의 점유율로 매출 1위를 유지했으나, 송전망의 현대화에 힘입어 에너지 및 유틸리티 부문은 2031년까지 연평균 성장률(CAGR) 11.93%를 기록하며 개별 산업을 상회하는 성장이 예상됩니다. 전기차 충전, 분산형 태양광 발전의 계통 연계, 실시간 디지털 트윈에는 결정론적 이더넷과 전자기 간섭을 견딜 수 있는 견고한 게이트웨이가 필요합니다. 석유 및 가스 해양 플랫폼에서는 방폭 스위치를 활용해 분출 방지 장치의 디지털화가 진행되고 있는 반면, 화학 플랜트에서는 KRITIS에 따른 보안 개선이 요구되고 있어 차세대 방화벽의 도입이 필수적입니다.

항만 자동화 및 철도 신호 시스템이 주도하는 운송 산업에서는 가동 중단 시간이 인명과 직결되기 때문에 SIL-4 인증을 획득한 장비가 도입되고 있습니다. 의료시설에서는 빌딩 자동화 시스템과 의약품 제조 공정을 통합하여, FDA 21 CFR Part 11의 감사 요건을 충족하는 지속적인 환경 모니터링을 실현하고 있습니다. 광업 분야에서는 자율 운반 시스템이 도입되고 있으며, 고지대에 위치한 광산 현장에서는 영하에서도 안정적으로 작동하는 산업용 PC에 대한 수요가 증가하고 있습니다. 각 산업 분야에서 IT-OT 융합 하드웨어 시장 점유율은 규정 준수 부담이나 지연 허용도에 따라 변동되지만, 디지털 트윈으로의 종합적인 전환에 힘입어 모든 부문에서 하드웨어 도입 규모가 점차 확대되고 있습니다.

지역별 분석

북미는 자동차, 항공우주, 식품 가공 각 클러스터의 견조한 자동화 수요에 힘입어 2025년 매출의 35.19%를 차지했습니다. “인프라 투자 및 고용법”에 따른 연방 정부의 자금 지원이 송전망 현대화 프로젝트를 뒷받침하는 한편, 사이버보안 및 인프라 보안국(CISA)의 지침에 따라 보안 업그레이드가 가속화되고 있습니다. 캐나다의 광업과 멕시코의 마키라도라도 더욱 탄력을 받고 있지만, 인력 부족으로 인해 도입 비용이 상승하고 있습니다. 이러한 정책 지원과 산업 수요의 결합이, 첨단 네트워크 도입에 있어 해당 지역의 주도적 지위를 앞으로도 계속해서 뒷받침할 것으로 보입니다.

연평균 성장률(CAGR) 12.26%로 전망되는 아시아태평양은 중국의 스마트 제조에 대한 세제 혜택과, 대상 하드웨어 지출의 최대 절반을 환급해 주는 인도의 생산 연계형 보조금 등의 혜택을 받고 있습니다. 일본에서는 “Society 5.0” 이니셔티브가 인구 동향상의 역풍에도 불구하고 기업들의 도입을 뒷받침하고 있으며, 한국에서는 적극적인 로봇 기술 도입을 통해 노동력 부족을 보완하고 있습니다. 베트남이나 태국 등 동남아시아의 전자기기 수출 기업들도 1차 공급업체의 요건을 충족하기 위해 결정론적 네트워크 백본에 투자하고 있습니다. 정부의 강력한 지원과 수출 지향적인 제조 생태계가 이 지역의 급속한 성장 궤도를 더욱 공고히 하고 있습니다.

유럽에서는 에너지 가격 변동으로 인해 성장세가 다소 주춤하고 있지만, 안정적인 한 자릿수 중반대의 성장세를 유지하고 있으며, 독일의 개정된 KRITIS 규정이나 프랑스의 ‘Industrie du Futur” 프로그램이 부문화되지 않은 스위치의 업데이트를 촉진하고 있습니다. 중동에서는 석유화학 산업의 디지털화와 스마트 시티 구상에 자금을 투입하고, 정부계 펀드의 자금을 활용하여 기존 아키텍처를 획기적으로 혁신하고 있습니다. 남미에서는 여전히 통화 측면의 제약이 있지만, 브라질의 광업 기업들이 선택적인 현대화를 주도하고 있습니다. 한편, 아프리카에서의 도입은 남아프리카공화국의 심층 금광과 이집트의 신흥 제조업 회랑에 집중되어 있습니다. 지역별 정책 체계와 인프라의 우선순위가, 비록 고르지 못하지만 지속적인 진전을 보이며 도입 양상을 형성해 나가고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the IT-OT convergence hardware market size is expected to increase from USD 34.87 billion in 2025 to USD 38.72 billion in 2026 and reach USD 63.95 billion by 2031, growing at a CAGR of 10.54% over 2026-2031.

This report is Segmented by Component (Industrial Ethernet Switches and Routers, Industrial Gateways and Edge Devices, and More), Industry Vertical (Manufacturing, Energy and Utilities, Oil and Gas, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Connectivity (Wired, and Wireless), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global IT-OT Convergence Hardware Market Trends and Insights

Rising Adoption of Edge Computing Gateways

Edge gateways relocate compute from data centers to production lines, cutting round-trip latency from 50-100 milliseconds to below 15 milliseconds, aligning with the sub-20-millisecond limits of closed-loop control systems. The National Institute of Standards and Technology estimated a 10-20X return on investment for discrete-manufacturing edge projects in 2025, primarily through reduced downtime and lower bandwidth costs. Gateway vendors now integrate Trusted Platform Module 2.0 chips after the Cybersecurity and Infrastructure Security Agency started requiring cryptographic device identity in December 2025. Dual-SIM 5G radios plus multi-port Gigabit Ethernet are becoming baseline specifications, enabling hybrid backhaul paths that sustain deterministic traffic even if one link fails. These performance and security improvements collectively push enterprises toward distributed intelligence architectures that favor edge hardware over legacy switches.

Demand for Unified Cybersecurity Across IT and OT Networks

New regulations are collapsing the traditional air gap that once protected operational technology. CISA's August 2025 guidance compels continuous, passive discovery of every OT asset, rewarding appliances that inspect industrial protocols without disturbing real-time control messages. The European Union's NIS2 Directive introduced stiff fines for failures to report incidents, accelerating upgrades across 18 critical sectors. Hardware vendors responded by earning IEC 62443-4-2 certification; Fortinet's rugged firewall series is one early example. Germany's updated KRITIS regulation extended similar segmentation rules to utilities and chemical plants in 2025. Together, these mandates elevate security capabilities from optional add-ons to core purchase criteria.

Legacy System Incompatibility and High Retrofit Costs

Many plants still operate controllers installed in the 1990s that lack Ethernet ports, forcing the use of protocol converters and long shutdowns when adding gateways. A 2025 survey found that 60% of process manufacturers maintain at least one air-gapped network, fragmenting data and complicating analytics. Safety-instrumented system revalidation under IEC 61511 can stretch 6-12 months, effectively deferring convergence projects until scheduled plant turnarounds. The lingering influence of the Stuxnet attack reinforces a risk-averse mindset, making executives hesitant to connect legacy assets to corporate networks. These integration hurdles add premium labor costs and double the total expense compared with greenfield deployments.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Industrial IoT Platforms in Smart Factories

- Mainstreaming of 5G Private Networks in Manufacturing Plants

- Skills Gap in IT-OT Integration Engineering

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge devices commanded the growth spotlight, expanding at 12.72% a year, whereas industrial Ethernet switches and routers delivered a dominant 31.35% share of the IT-OT convergence hardware market size in 2025. Gateways now bundle container runtime environments, allowing predictive algorithms to run locally and cut cloud egress costs. Security appliances certified to IEC 62443-4-2 are the next high-velocity line as enterprises adopt zero-trust segmentation. Switch vendors, meanwhile, defend their franchises by embedding intrusion-detection functions, although commoditization risk looms if they fail to add analytics that justify price premiums.

OPC UA Field eXchange threatens proprietary fieldbus lock-in, so differentiation is tilting toward cybersecurity, onboard AI accelerators, and vertical certifications. Dell and Hewlett-Packard Enterprise both released rugged edge servers with conformal coating and extended temperature support to penetrate oilfield deployments. At the same time, NVIDIA Jetson-powered gateways illustrate how machine-vision workloads are migrating from racks to the factory floor. The result is a layered architecture in which edge hardware interprets data streams in real time while deterministic switches guarantee sub-microsecond synchronization for time-critical traffic, keeping both categories indispensable to the broader IT-OT convergence hardware market.

Manufacturing retained the revenue lead with 41.27% share in 2025, but grid modernization is pushing energy and utilities to record an 11.93% CAGR through 2031, outpacing discrete industries. Electric-vehicle charging, distributed solar in-feed, and real-time digital twins require deterministic Ethernet and hardened gateways able to withstand electromagnetic interference. Oil and gas offshore platforms are digitizing blowout preventers with explosion-proof switches, while chemical plants face KRITIS-driven security retrofits that dictate next-generation firewalls.

Transportation, driven by port automation and rail signaling, orders SIL-4 certified equipment where downtime risks human life. Healthcare facilities converge building automation with pharmaceutical production for continuous environmental monitoring that satisfies FDA 21 CFR Part 11 audits. Mining operations embrace autonomous haulage, and their high-altitude sites create demand for industrial PCs that operate reliably below freezing. Across each vertical, the IT-OT convergence hardware market share fluctuates by compliance burden and latency tolerance, yet the overarching migration toward digital twins ensures every sector incrementally widens its hardware footprint.

Complete Report Scope:

- By Component

- Industrial Ethernet Switches and Routers

- Industrial Gateways and Edge Devices

- Industrial PCs, Servers, and HMIs

- Network Security Appliances

- Other Components

- By Industry Vertical

- Manufacturing

- Energy and Utilities

- Oil and Gas

- Transportation and Logistics

- Healthcare and Lifesciences

- Mining

- Other Industry Verticals

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Connectivity

- Wired

- Wireless

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America generated 35.19% of 2025 revenue thanks to robust automation demand across automotive, aerospace, and food processing clusters. Federal funding from the Infrastructure Investment and Jobs Act underwrites grid-modernization projects, while Cybersecurity and Infrastructure Security Agency (CISA) guidance accelerates security upgrades. Canadian mining and Mexican maquiladoras add further momentum, though talent shortages inflate deployment costs. This combination of policy support and industrial demand continues to anchor the region's leadership in advanced networking deployments.

Asia-Pacific, projected at a 12.26% CAGR, benefits from China's intelligent-manufacturing tax incentives and India's production-linked subsidies that reimburse up to half of qualifying hardware spend. Japan's Society 5.0 initiative nudges enterprise uptake despite demographic headwinds, and South Korea offsets labor scarcity with aggressive robotics adoption. Southeast Asian electronics exporters in Vietnam and Thailand also invest in deterministic network backbones to comply with Tier-1 supplier requirements. Strong government backing and export-oriented manufacturing ecosystems further reinforce the region's rapid growth trajectory.

Europe maintains steady, mid-single-digit growth held back by energy price volatility, yet Germany's updated KRITIS rules and France's "Industrie du Futur" program stimulate replacements of non-segmented switches. The Middle East funds petrochemical digitization and smart-city initiatives, using sovereign wealth resources to leapfrog legacy architectures. South America remains currency-constrained, with Brazil's mining firms leading selective upgrades, while Africa's adoption is concentrated in South Africa's deep-level gold mines and Egypt's emerging manufacturing corridor. Regional policy frameworks and infrastructure priorities continue to shape uneven but progressing adoption patterns.

- Cisco Systems Inc.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- ABB Ltd.

- Belden Inc.

- Moxa Inc.

- Advantech Co. Ltd.

- HMS Networks AB

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Fortinet Inc.

- Palo Alto Networks Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Phoenix Contact GmbH and Co. KG

- Delta Electronics Inc.

- Hirschmann Automation and Control GmbH

- Check Point Software Technologies Ltd.

- Trend Micro Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Edge Computing Gateways

- 4.2.2 Demand for Unified Cybersecurity across IT and OT Networks

- 4.2.3 Expansion of Industrial IoT Platforms in Smart Factories

- 4.2.4 Mainstreaming of 5G Private Networks in Manufacturing Plants

- 4.2.5 Convergence Requirements for Predictive Maintenance Analytics

- 4.2.6 Government Incentives for Digital Infrastructure Modernization

- 4.3 Market Restraints

- 4.3.1 Legacy System Incompatibility and High Retrofit Costs

- 4.3.2 Skills Gap in IT-OT Integration Engineering

- 4.3.3 Data Ownership and Governance Concerns

- 4.3.4 Macroeconomic Slowdowns Delaying Capex Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Industrial Ethernet Switches and Routers

- 5.1.2 Industrial Gateways and Edge Devices

- 5.1.3 Industrial PCs, Servers, and HMIs

- 5.1.4 Network Security Appliances

- 5.1.5 Other Components

- 5.2 By Industry Vertical

- 5.2.1 Manufacturing

- 5.2.2 Energy and Utilities

- 5.2.3 Oil and Gas

- 5.2.4 Transportation and Logistics

- 5.2.5 Healthcare and Lifesciences

- 5.2.6 Mining

- 5.2.7 Other Industry Verticals

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Connectivity

- 5.4.1 Wired

- 5.4.2 Wireless

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 ABB Ltd.

- 6.4.6 Belden Inc.

- 6.4.7 Moxa Inc.

- 6.4.8 Advantech Co. Ltd.

- 6.4.9 HMS Networks AB

- 6.4.10 Huawei Technologies Co. Ltd.

- 6.4.11 Juniper Networks Inc.

- 6.4.12 Fortinet Inc.

- 6.4.13 Palo Alto Networks Inc.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Hewlett Packard Enterprise Company

- 6.4.16 Phoenix Contact GmbH and Co. KG

- 6.4.17 Delta Electronics Inc.

- 6.4.18 Hirschmann Automation and Control GmbH

- 6.4.19 Check Point Software Technologies Ltd.

- 6.4.20 Trend Micro Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment