|

시장보고서

상품코드

2073089

심장이식 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Heart Transplantation Therapeutic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

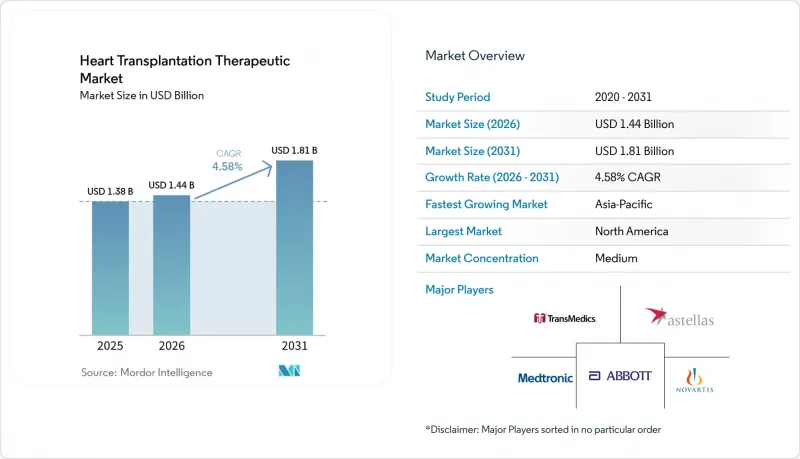

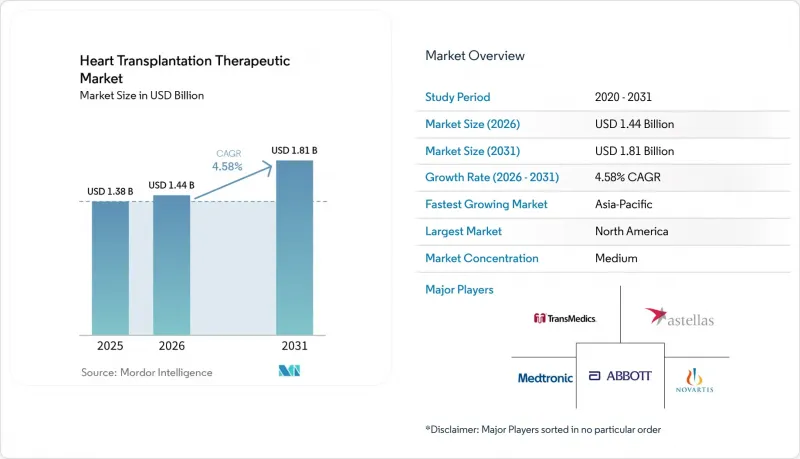

Mordor Intelligence에 의하면, 심장이식 치료 시장 규모는 2025년 13억 8,000만 달러에서 2026년에는 14억 4,000만 달러로 확대되어 2031년까지 18억 1,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 4.58%로 성장할 전망입니다.

본 보고서는 약제 유형(면역억제제, 항감염제 등), 유통 채널(병원, 소매, 온라인 약국), 치료 환경, 환자 연령(성인, 소아), 적응증(확장성 심근병증, 허혈성 심장질환 등) 및 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 심장이식 치료 시장 동향 및 인사이트

말기 심부전으로 인한 부담 증가

심장이식 치료 시장은 진행성 심부전의 유병률 증가에 힘입어 성장하고 있습니다. 2026년 분석에 따르면, 1990년부터 2025년까지 심혈관 질환과 관련된 심부전으로 인한 연령 조정 유병률 및 장애를 안고 지내는 기간이 증가했으며, 특히 20세에서 54세 연령층과 사회인구통계 지수가 중-고 수준인 국가들에서 현저한 증가가 나타났습니다. 전 세계 심부전 환자 수는 6,400만 명으로 여전히 높은 수준을 유지하고 있으며, 잠재적인 이식 후보자층은 광범위하게 존재하지만, 실제로 수술을 받는 사람은 그중 극히 일부에 불과합니다. 미국에서는 2012년부터 2024년까지 심장이식 건수가 101.1% 증가하여, 2024년에는 4,599건에 달했습니다. 또한, 2023년부터 2024년까지 성인 이식 건수가 424건 증가했습니다. 또한 『2025년 세계 심장 보고서』에서는 비만과 관련된 심근병증이 심부전의 원인으로 증가하고 있다는 점도 지적되고 있으며, 이식 후 치료 계획을 환자 개개인의 상황에 맞추어 조정할 필요성이 강조되고 있습니다.

면역억제 유지요법의 활용 확대

타크로리무스를 주성분으로 하는 다제 병용 유지 요법을 기반으로 하는 심장이식 치료 시장은 접근성 개선과 치료법의 정교화로 인해 확대되고 있습니다. 2025년 1월, Biocon Pharma는 중국 국가의약품감독관리국(NMPA)으로부터 0.5mg, 1mg, 5mg 용량의 타크로리무스 캡슐에 대한 승인을 획득하여 제네릭 의약품공급 기반을 확대했습니다. 타크롤리무스의 환자 내 변동성에 관한 연구 결과는 보다 면밀한 모니터링과 보다 안정적인 약물 노출을 보장하는 제제의 개발을 뒷받침하고 있습니다. 2025년 연구에서는 타크로리무스의 변동성이 이식편 예후 불량과 관련이 있는 것으로 나타났으며, 2026년 논문에서는 ABCC2 rs2273697이 이러한 변동성의 결정 요인임이 밝혀졌습니다. 이러한 연구 결과를 바탕으로, 고도의 전문성을 요하는 의료시설에서 체계적인 투여 프로그램이 추진되고 있으며, 표준 치료제의 가격 경쟁과 전문적인 치료 요법의 가치 기반 차별화 간에 균형이 이루어지고 있습니다.

기증 장기 부족

심장이식 치료 시장은 그 성장이 임상적 수요가 아닌 기증자 확보 상황에 좌우되기 때문에 계속해서 제약에 직면하고 있습니다. 2024년에는 전 세계적으로 1만 287건의 심장이식이 이루어졌으나, 표준 냉허혈 시간이 4-6시간인 점을 고려할 때 여전히 큰 공급 격차가 남아 있습니다. 2024년에는 순환 정지 후(DCD) 기증자가 전체 사망 기증자의 28%를 차지하여 전년 대비 17% 증가했으나, DCD 심장이 활용된 국가는 불과 9개국에 그쳤습니다. 이러한 지리적 확산의 한계가 시장 성장을 제약하고 있습니다. 또한, 2024년에 개정된 ISHLT의 후보자 평가 지침에서는 보다 엄격한 위험도 계층화가 강조되고 있으며, 이 체계를 엄격하게 적용하는 기관에서는 이식 대기자 명단의 규모가 줄어들 가능성이 있습니다. 한편, 유나이티드 테라퓨틱스(United Therapeutics)는 2026년 5월, UHeart를 활용한 EXPRESS 이종 이식 임상시험에 대해 FDA의 승인을 획득했는데, 이는 기증자 부족 문제에 대한 장기적인 해결책이 될 것입니다.

부문별 분석

2025년, 면역억제제는 심장이식 치료 시장을 독점하며 매출의 54.60%를 차지했습니다. 이러한 지배적인 위상은 심장이식 수혜자들에게 있어 골드 스탠다드로 여겨지는 칼시뉴린 억제제 기반 치료법에 대한 의존도가 높다는 점을 여실히 보여주고 있습니다. 지출의 대부분은 타크로리무스 제제나 미코페놀산과의 병용 요법에 집중되어 있으며, 두 약제 모두 장기간 사용과 빈번한 용량 조정이 필요합니다. 이러한 추세로 인해, 수술 건수 증가세가 완만하더라도 이 부문이 시장에서 중심적인 위치를 계속 차지할 것으로 확실시되고 있습니다.

항감염제 시장은 2031년까지 연평균 성장률(CAGR)이 6.90%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 단순히 환자 수 증가라기보다는 예방 프로토콜의 강화에 의해 주도되고 있습니다. 조사에 따르면, 기증자가 양성이고 수혜자가 음성인 심장이식 환자의 경우, 발가시클로비르를 3개월간 예방 투여했을 때, 6개월간 투여했을 때와 비교해 CMV 감염 위험이 높아지는 것으로 밝혀졌습니다. 이러한 연구 결과는 특히 이식 후 중요한 첫 1년 동안 항바이러스 치료 기간을 연장할 것을 권장하는 것입니다.

2025년에는 병원 약국이 수익의 61.30%를 차지하고 있어, 심장이식 치료 시장이 3차 의료와 밀접한 관련이 있음을 여실히 보여주고 있습니다. 도입 요법, 조기 타크로리무스 용량 조정, 치료제 모니터링과 같은 주요 과정은 전문 병원의 업무 흐름에 필수적입니다. 이로 인해 병원 약국은 신규 이식 환자에게 있어 주요하고도 규제가 가장 엄격한 조제 거점으로서의 지위를 확립하고 있습니다. 이러한 우위는 수술이 통합된 약국 팀을 보유한 경우가 많은 주요 대학 부속 이식 센터에 집중되어 있다는 점에 의해 더욱 강화되고 있습니다.

온라인 약국 시장은 2031년까지 연평균 성장률(CAGR) 5.95%로 확대될 것으로 예상되며, 이 부문에서 가장 높은 성장률을 보이고 있습니다. 이러한 추세는 편의성보다는 통신판매 처리, 택배 서비스, 그리고 상태가 안정된 환자에 대한 모니터링 수요에 대응하는 등 전문적인 서비스에 의해 주도되고 있습니다. 이식 환자들이 수술 직후 단계를 지나감에 따라, 처방전이 병원에서 장기적으로 안정적인 약품 공급을 보장하는 채널로 뚜렷하게 전환되고 있습니다.

지역별 분석

2025년, 북미는 심장이식 치료 시장 매출의 40.65%를 차지하며 1위를 유지했습니다. 미국은 2024년에 4,636건의 심장이식을 실시하여 세계 1위를 차지했습니다. 메디케어의 환급 및 확립된 전문 약국 네트워크로 인해, 수술 후 환자 1인당 약품비는 고액으로 책정되고 있습니다. 대학병원으로의 환자 집중은 프로토콜의 표준화를 촉진하고, 치료 성과에 대한 대규모 모니터링을 뒷받침하고 있습니다. 밴더빌트 대학병원은 2025년에 성인 및 소아 심장이식 수술 210건을 시행함으로써, 치료 관행을 정립하는 데 있어 높은 처리 능력을 갖춘 센터로서의 역할을 강화한 좋은 사례입니다.

유럽은 심장이식 치료제 시장에서 여전히 2위의 규모를 유지하고 있습니다. 유로트랜스플랜트(Eurotransplant) 회원국들은 2026년 첫 5개월 동안 1,102건의 심장이식 사례를 보고했으며, 이는 2025년 같은 기간의 1,046건보다 증가한 수치입니다. 스페인에서는 2025년에 심장이식 건수가 12% 증가했으며, 주민 100만 명당 50.7명이라는 높은 기증률을 유지했습니다. 독일과 영국은 수술 건수에 크게 기여하고 있는 한편, 엄격한 제조 및 의약품 안전성 감시 기준 덕분에 브랜드 제품과 규제 대상 제제에 대한 수요는 견조한 추세를 보이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.55%라는 가장 높은 성장률을 기록하며 확대될 것으로 전망되며, 가장 역동적인 지역 시장으로 부상하고 있습니다. 중국과 인도가 성장을 주도하고 있으며, 그 배경에는 의료기관의 수용 능력 확대, 제네릭 타크롤리무스 사용 확대, 그리고 이식 및 면역 조절 치료제에 대한 유리한 정책이 있습니다. 2025년 중국에서 바이오콘사의 타크로리무스가 승인 및 출시된 사실은 접근성 확대가 의료기관의 조달 증가를 얼마나 촉진하는지를 보여줍니다. 일본, 한국, 호주는 이식 건수는 적지만, 수술 후 면역억제제 사용을 지원하는 국민건강보험 제도 덕분에 치료비는 높은 수준을 유지하고 있습니다. 중동 및 아프리카 및 남미 지역의 성장세는 여전히 고르지 않은데, 사우디아라비아, 아랍에미리트(UAE), 브라질, 아르헨티나 등의 국가에서는 역량이 향상되고 있는 반면, 기증자 부족, 자금 문제, 전문의 부족과 같은 과제에 직면해 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the heart transplantation therapeutic market size is expected to increase from USD 1.38 billion in 2025 to USD 1.44 billion in 2026 and reach USD 1.81 billion by 2031, growing at a CAGR of 4.58% over 2026-2031.

This report is Segmented by Drug Type (Immunosuppressants, Anti-Infectives, and More), Distribution Channel (Hospital, Retail, Online Pharmacies), Therapy Setting, Patient Age (Adult, Pediatric), Indication (Dilated Cardiomyopathy, Ischemic Heart Disease, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Heart Transplantation Therapeutic Market Trends and Insights

Rising End-Stage Heart Failure Burden

The heart transplantation therapeutic market is driven by the increasing prevalence of advanced heart failure. A 2026 analysis highlighted a rise in age-standardized prevalence and years lived with disability due to cardiovascular disease-related heart failure from 1990 to 2025, with significant increases among individuals aged 20 to 54 and in middle to high Socio Demographic Index countries. Global heart failure prevalence remains high at 64 million individuals, ensuring a broad pool of potential transplant candidates, though only a fraction progresses to surgery. In the U.S., heart transplants increased by 101.1% from 2012 to 2024, reaching 4,599 procedures in 2024, with 424 additional adult transplants between 2023 and 2024. The 2025 World Heart Report also identified obesity-linked cardiomyopathy as a growing contributor to heart failure, emphasizing the need for tailored post-transplant treatment plans.

Expanding Use of Immunosuppressive Maintenance Therapies

The heart transplantation therapeutic market, anchored in tacrolimus-based multi-drug maintenance therapy, is expanding through improved access and treatment refinement. In January 2025, Biocon Pharma received NMPA approval in China for tacrolimus capsules in 0.5 mg, 1 mg, and 5 mg strengths, broadening the generic supply base. Research on tacrolimus intra-patient variability supports closer monitoring and formulations ensuring steadier exposure. A 2025 study linked tacrolimus variability to inferior allograft outcomes, while a 2026 paper identified ABCC2 rs2273697 as a determinant of this variability. These findings promote structured dosing programs at high-complexity centers, balancing price competition in standard agents with value-based differentiation in specialized regimens.

Donor Organ Scarcity

The heart transplantation market continues to face limitations as its growth depends on donor availability rather than clinical demand. In 2024, 10,287 heart transplants were performed globally, yet a significant supply gap remains due to the standard cold ischemia time of 4 to 6 hours. Donation after circulatory death (DCD) donors accounted for 28% of all deceased donors in 2024, a 17% year-over-year increase, but DCD hearts were utilized in only 9 countries. This limited geographic adoption restricts market growth. Additionally, the updated ISHLT candidate evaluation guidance in 2024 emphasizes stricter risk stratification, potentially reducing listings at centers applying the framework rigorously. While United Therapeutics received FDA clearance in May 2026 for the EXPRESS xenotransplantation trial with UHeart, it represents a long-term solution to donor scarcity.

Other drivers and restraints analyzed in the detailed report include:

- Wider Adoption of Ex-Vivo Organ Perfusion and Preservation

- Personalized Immunosuppression Guided by Biomarkers

- Lifelong Immunosuppression Safety Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, immunosuppressants dominated the heart transplantation therapeutic market, accounting for 54.60% of the revenue. This dominance underscores the reliance on calcineurin inhibitor-based regimens, the gold standard for heart transplant recipients. Spending heavily leans towards tacrolimus formulations and mycophenolate combinations, both of which necessitate prolonged use and frequent adjustments. Such dynamics ensure the centrality of this category in the market, even amidst only moderate growth in procedures.

Anti-infectives are set to be the fastest-growing segment, with a projected CAGR of 6.90% through 2031. This growth is driven more by heightened prophylaxis protocols than mere increases in patient volume. Research highlights that heart transplant patients, who are donor positive and recipient negative, face a heightened risk of CMV infection after three months on valganciclovir prophylaxis, compared to six months. Such findings advocate for extended antiviral treatment durations, especially during the crucial first year post-transplant.

In 2025, hospital pharmacies secured 61.30% of the revenue, underscoring the heart transplantation therapeutic market's strong ties to tertiary care. Key processes like induction therapy, early tacrolimus titration, and therapeutic drug monitoring are integral to specialist hospital workflows. This positions hospital pharmacies as the primary and most regulated dispensing point for new transplant recipients. Their dominance is further bolstered by the concentration of procedures at major academic transplant centers, which often feature integrated pharmacy teams.

Online pharmacies are projected to expand at a 5.95% CAGR through 2031, marking the highest growth rate in this segment. This trend is driven less by convenience and more by specialized services like mail order handling, home delivery, and coordination for stable patients' monitoring needs. As recipients progress beyond the immediate post-surgery phase, there's a noticeable shift of prescriptions from hospital settings to channels that ensure consistent long-term refills.

Complete Report Scope:

- By Drug Type

- Immunosuppressants

- Anti-Infectives

- Analgesics

- Other Heart Transplant Therapeutics

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Therapy Setting

- Pre-Transplant Care

- In-Hospital Post-Transplant Care

- Long-Term Outpatient Maintenance Therapy

- By Patient Age Group

- Adult

- Pediatric

- By Indication

- Dilated Cardiomyopathy

- Ischemic Heart Disease

- Hypertrophic Cardiomyopathy

- Restrictive Cardiomyopathy

- Congenital Heart Disease

- Other Indications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 40.65% of the heart transplantation therapeutic market revenue, securing its leading position. The U.S. led globally with 4,636 heart transplants performed in 2024. Medicare reimbursements and established specialty pharmacy networks drive high per-patient drug spending post-surgery. Concentration at academic hospitals enhances protocol standardization and supports large-scale monitoring of treatment outcomes. Vanderbilt exemplified this by performing 210 adult and pediatric heart transplants in 2025, reinforcing the role of high-throughput centers in shaping treatment practices.

Europe remains the second-largest market for heart transplantation therapeutics. Eurotransplant member states reported 1,102 heart transplants in the first five months of 2026, up from 1,046 during the same period in 2025. Spain increased cardiac transplant volumes by 12% in 2025 and maintained a high donation rate of 50.7 donors per million inhabitants. Germany and the U.K. contribute significantly to procedure volumes, while stringent manufacturing and pharmacovigilance standards sustain strong demand for branded and regulated formulations.

Asia Pacific is projected to grow at the fastest CAGR of 6.55% through 2031, emerging as the most dynamic regional market. China and India drive growth, supported by expanding institutional capacities, broader access to generic tacrolimus, and favorable policies for transplant and immune regulation therapeutics. Biocon's tacrolimus approval and rollout in China in 2025 demonstrated how access expansion supports institutional procurement growth. Japan, South Korea, and Australia, though smaller in transplant numbers, maintain high treatment expenditures due to national coverage supporting post-surgery immunosuppressive use. Growth in the Middle East, Africa, and South America remains uneven, with countries like Saudi Arabia, the UAE, Brazil, and Argentina improving capabilities but facing challenges such as donor shortages, funding constraints, and limited specialist availability.

- Abbott Laboratories

- Abbvie

- Astellas Pharma

- Biocon

- Boston Scientific

- Bristol-Myers Squibb

- Dr. Reddy's Laboratories

- Roche

- Glenmark Pharmaceuticals

- Intas Pharmaceutical

- Medtronic

- Mylan

- Novartis

- Organox

- Paragonix Technologies

- Pfizer

- Sanofi

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- TransMedics Group, Inc.

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising End-Stage Heart Failure Burden

- 4.2.2 Expanding Use of Immunosuppressive Maintenance Therapy

- 4.2.3 Wider Adoption of Ex-Vivo Organ Perfusion And Preservation Systems

- 4.2.4 Personalized Immunosuppression Guided by Biomarkers

- 4.2.5 Donor-Heart Logistics Pressure From Time-to-Transplant Constraints

- 4.2.6 Post-Transplant Infection Prevention Protocol Intensification

- 4.3 Market Restraints

- 4.3.1 Shortage of Suitable Donor Hearts

- 4.3.2 Lifelong Immunosuppression Safety Burden

- 4.3.3 High Total Cost of Transplant Care And Follow-Up

- 4.3.4 Limited Center Capacity and Specialist Availability

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power Of Suppliers

- 4.7.2 Bargaining Power Of Buyers

- 4.7.3 Threat Of New Entrants

- 4.7.4 Threat Of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Drug Type

- 5.1.1 Immunosuppressants

- 5.1.2 Anti-Infectives

- 5.1.3 Analgesics

- 5.1.4 Other Heart Transplant Therapeutics

- 5.2 By Distribution Channel

- 5.2.1 Hospital Pharmacies

- 5.2.2 Retail Pharmacies

- 5.2.3 Online Pharmacies

- 5.3 By Therapy Setting

- 5.3.1 Pre-Transplant Care

- 5.3.2 In-Hospital Post-Transplant Care

- 5.3.3 Long-Term Outpatient Maintenance Therapy

- 5.4 By Patient Age Group

- 5.4.1 Adult

- 5.4.2 Pediatric

- 5.5 By Indication

- 5.5.1 Dilated Cardiomyopathy

- 5.5.2 Ischemic Heart Disease

- 5.5.3 Hypertrophic Cardiomyopathy

- 5.5.4 Restrictive Cardiomyopathy

- 5.5.5 Congenital Heart Disease

- 5.5.6 Other Indications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 AbbVie Inc.

- 6.3.3 Astellas Pharma Inc.

- 6.3.4 Biocon Limited

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Bristol Myers Squibb Company

- 6.3.7 Dr. Reddy's Laboratories Limited

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Glenmark Pharmaceuticals Limited

- 6.3.10 Intas Pharmaceuticals Limited

- 6.3.11 Medtronic plc

- 6.3.12 Mylan N.V.

- 6.3.13 Novartis AG

- 6.3.14 OrganOx Limited

- 6.3.15 Paragonix Technologies, Inc.

- 6.3.16 Pfizer Inc.

- 6.3.17 Sanofi S.A.

- 6.3.18 Sun Pharmaceutical Industries Limited

- 6.3.19 Teva Pharmaceutical Industries Limited

- 6.3.20 TransMedics Group, Inc.

- 6.3.21 Viatris Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment