|

시장보고서

상품코드

2073102

지속가능성 성과 관리 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sustainability Performance Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

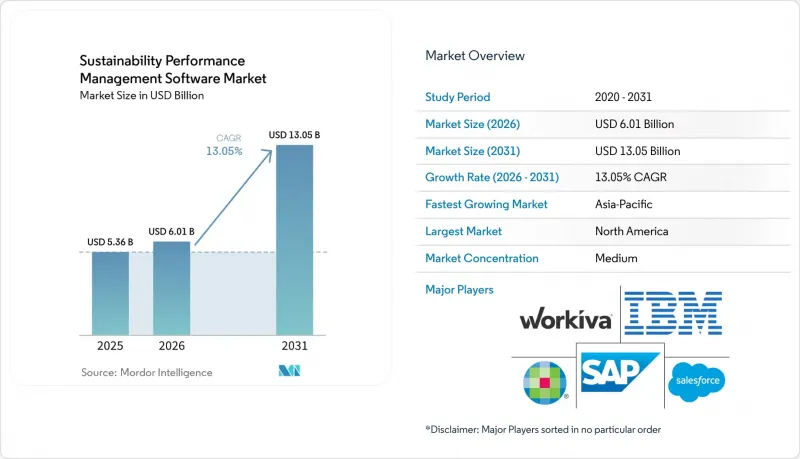

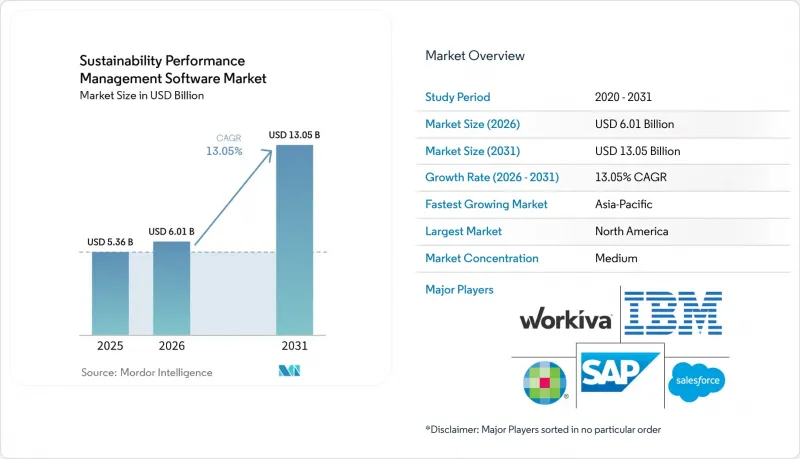

Mordor Intelligence에 의하면, 지속가능성 성과 관리 소프트웨어 시장은 2025년에 53억 6,000만 달러 규모가 되어, 2026년 60억 1,000만 달러에서 2031년까지 130억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 예측 기간 CAGR은 14.04%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 용도(환경 성능 관리, 기타), 기업 규모(대기업 및 중소기업), 최종 이용 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 지속가능성 성과 관리 소프트웨어 시장 동향 및 인사이트

규제에 따른 공시 의무 강화

유럽과 미국의 보고 규정에 따라 기업들은 비체계적인 보고 절차를, 체계적인 기록, 관리된 업무 흐름, 재현 가능한 공시 결과를 지원할 수 있는 시스템으로 대체해야 할 압박을 받고 있습니다. 기업이 업무 지표를 공식 제출 일정 및 내부 검토 절차와 일치시킬 때, 더 이상 제각각인 파일에만 의존할 수 없게 되었기 때문에 지속가능성 성과 관리 소프트웨어 시장은 이러한 변화로부터 직접적인 혜택을 보고 있습니다. 미국에서는 SEC의 기후 변화 공시 규정에 따라 대규모 가속 제출 기업을 대상으로, 2025 회계연도에 시작되어 2026년에 제출되는 결산에 대해 스코프 1 및 스코프 2 배출량을 공시해야 할 의무가 부과되고 있으며, 이는 소프트웨어 조달 및 데이터 정제 프로그램에 있어 명확한 규정 준수 계기가 되고 있습니다. 유럽의 공시 의무 역시 여러 팀에 걸쳐 일관된 태그 지정, 증거 보존, 버전 관리, 보증 지원의 필요성을 높임으로써 유사한 효과를 가져오고 있습니다. 그 결과, 소프트웨어에 대한 지출이 단기적인 시범 프로그램에 그치지 않고 계획적인 운영 예산에 임베디드되게 되었으며, 이로 인해 지속가능성 성과 관리 소프트웨어 시장의 기초적인 수요가 강화되고 있습니다. 또한, 대기업이 자사의 보고 및 보증 업무를 완료하기 위해서는 업스트림 프로세스에서 더 정확한 입력 데이터가 필요하기 때문에 공급업체도 동일한 사이클에 포함되게 됩니다.

AI를 활용한 감사 대응 준비 및 지속적인 통제 모니터링

지속가능성 성과 관리 소프트웨어 시장은 연간 문서 중심의 보고에서 지속적인 모니터링 및 조기 문제 감지로 명확하게 전환되고 있는 추세 덕분에 혜택을 보고 있습니다. 구매자들은 현재 법무팀과 보증팀이 최종 검토를 시작하기 전에 누락된 필드를 파악하고, 원본 레코드를 추적하며, 규제 요건과 비즈니스 데이터를 연계할 수 있는 플랫폼을 원하고 있습니다. SAP는 2026년 5월, 새로운 지속가능성 AI 에이전트를 발표했습니다. 이를 통해 스코프 1, 스코프 2, 스코프 3의 시나리오 모델링에 소요되는 시간을 1영업일에서 20분으로 단축하는 ‘실적 최적화 에이전트”와, 중요도 평가와 보고 요건의 매핑을 자동화하는 “지속가능성 규제 대응 대행사”가 포함됩니다. IBM도 2026년 4월, Excel에서 사용할 수 있는 ‘Envizi Emissions Calculations”를 도입하여 이러한 방향성을 더욱 확대했습니다. 이 도구는 기업이 수작업으로 수행하던 배출량 산정 업무를 확장성이 더 뛰어나고 감사에 대응할 수 있는 보고 프로세스로 전환하는 데 도움이 됩니다. 이러한 제품의 도입이 중요하게 여겨지는 이유는 AI가 더 이상 단순한 속도 향상 도구로서가 아니라, 검토 부담을 줄이고 보고의 일관성을 높일 수 있는 관리 도구로 인식되기 시작했기 때문입니다. 이러한 변화를 통해 벤더는 재무, 감사, 규정 준수 각 부서에서 플랫폼의 관련성을 높이고, 지속가능성 성과 관리 소프트웨어 시장의 가치 제안을 확대할 수 있습니다.

부문화된 기업 데이터 아키텍처가 도입을 저해하고 있습니다.

많은 기업에서는 여전히 ESG 관련 정보를 재무, 조달, 업무, 인사, 법무, 시설 관리 등 각 시스템에 분산하여 보관하고 있어, 정보의 완전성이나 관리 책임의 소재를 파악하기 어려워지고 있습니다. 슈나이더 일렉트릭은 조직이 관할 구역별로 하나의 보고 시스템을 사용하는 경향이 있다고 지적하고 있습니다. 이로 인해 대조 작업이 늘어나게 되어, 수집한 데이터의 활용 가치가 제한될 수밖에 없습니다. 데이터 소스의 일관성이 부족하고, 정의가 통일되지 않았으며, 근거가 되는 증거가 여러 팀에 분산되어 있는 경우 도입에 시간이 오래 걸리기 때문에 바로 이러한 문제가 지속가능성 성과 관리 소프트웨어 시장의 성장을 둔화시키고 있습니다. 2025년 ScienceDirect에 발표된 조사에 따르면, ESG 온톨로지 및 데이터 아키텍처 프로젝트 중 실제 기업 데이터를 활용해 모델을 검증하고 있는 사례는 20% 미만으로 나타났으며, 이는 이상적인 설계 개념과 실제 운영 상황 사이에 괴리가 있음을 여실히 보여주고 있습니다. 벤더 입장에서는 도입 기간이 길어지고, 서비스 수요가 증가하며, 기본적인 데이터 거버넌스가 개선될 때까지 고객이 본격적인 도입을 연기할 가능성이 높아진다는 것을 의미합니다. 또한, 이는 미리 구축된 ERP, 인사, 조달용 커넥터를 갖춘 공급업체에게 경쟁 우위를 제공합니다. 왜냐하면 신속한 통합을 통해 구매 주기의 초기 단계에서 가치를 입증하는 데 필요한 노력이 줄어들기 때문입니다.

부문별 분석

2025년 매출액 중 소프트웨어가 74.13%를 차지하고 있으며, 이는 여전히 가장 큰 지출 항목이 프로젝트 기반 지원 업무가 아니라 핵심 플랫폼에 있음을 보여줍니다. 이러한 구성은 지속가능성 성과 관리 소프트웨어 시장이 성숙기에 접어들었음을 반영하고 있습니다. 왜냐하면 플랫폼이 결산 프로세스, 감사 기록, 공급업체로부터의 입력 데이터, 보고 관리와 통합되면 이를 대체하는 것이 훨씬 더 어려워져 업무에 큰 혼란을 초래하게 되기 때문입니다. 따라서, 갱신 결정은 라이선싱상의 영향에 그치지 않습니다. 이미 도입된 시스템에서 마이그레이션하는 것은 데이터 이전, 프로세스 재설계, 여러 팀에 걸친 재검증 작업이 필요할 수 있기 때문입니다. IBM이 2026년 4월에 Excel용 ‘Envizi Emissions Calculations”를 출시한 것은 주요 벤더들이 아직 엔터프라이즈 시스템에 완전히 통합되지 않은 수동 배출량 계산 워크플로우에 대한 소프트웨어 적용 범위를 여전히 확대해 나가고 있음을 보여줍니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 16.83%로 확대될 것으로 예상되며, 이는 플랫폼 도입이 진전되는 상황에서도 도입, 데이터 설계, 지속적인 지원이 여전히 중요함을 보여줍니다. 기업은 기반이 되는 용도 계층의 가치를 충분히 끌어내기 전에, 중요도 평가, 배출원 매핑, 관리 조치 설계, 보증 준비, 워크플로우 설정에 대한 지원이 필요한 경우가 많습니다. 또한, 사내에 대규모 지속가능성 팀을 갖추지 않은 조직의 경우, 특히 보고 기한이 임박했거나 데이터 소유자가 여러 부서에 걸쳐 있는 경우, 매니지드 서비스의 중요성은 점점 더 커지고 있습니다. 이러한 추세로 인해, 해당 서비스는 지속가능성 성과 관리 소프트웨어 시장과 밀접하게 연계된 상태를 유지하고 있습니다. 이는 고객들이 자문 및 지원 서비스를 독립적인 범주로가 아니라 소프트웨어와 함께 구매하는 경우가 많기 때문입니다. 또한, 이는 파트너 생태계가 잘 갖춰진 벤더일수록 모든 제공 업무를 자체적으로 담당하지 않고도 폭넓은 고객 기반을 지원할 수 있으므로, 더 높은 성장 가능성을 유지할 수 있음을 의미합니다.

2025년 기준으로 지속가능성 성과 관리 소프트웨어 시장의 63.12%를 클라우드 기반 도입이 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 16.53%로 성장할 것으로 전망됩니다. 이는 주요 제공 모델이 기세를 잃기는커녕 여전히 기세를 더해가고 있음을 뒷받침합니다. 이는 보고 규칙, 분류 체계의 변경, 검증 로직, 워크플로우 요구 사항이 빈번하게 변경되고 있기 때문에 많은 고객이 느린 업그레이드 주기에 의존할 수 없다는 현실을 반영하고 있습니다. Workiva의 2026년 5월 지속가능성 관련 보도자료에서는 2025년 12월 EFRAG가 발표한 간소화된 기준안에 연계된 “Simplified ESRS Intelligence”지식 기반이 추가되었습니다. 이는 클라우드 릴리스가 끊임없이 변화하는 보고 요구 사항에 얼마나 신속하게 대응할 수 있는지를 보여줍니다. 지속가능성 성과 관리 소프트웨어 업계에서 제품 출시 속도는 매우 중요합니다. 이는 고객들이 반복적인 로컬 업그레이드나 프로젝트를 필요로 하는 재구성을 거치지 않고도 규칙 변경에 대응할 수 있는 단일 플랫폼을 점점 더 요구하고 있기 때문입니다.

On-Premise 배포는 데이터의 소재지, 사내 호스팅 또는 기밀 기록에 대한 현지 관리를 특히 중시하는 정부 기관, 규제가 엄격한 기관 및 산업 사업자에게 여전히 중요합니다. 또한, 클라우드상에서 통합적인 보고서 작성 및 분석을 수행하고자 하는 한편, 로컬 시스템이나 지역 고유의 데이터 관리와 밀접하게 연계된 상태에서 일부 처리 계층을 유지해야 하는 기업들 사이에서는 하이브리드 모델의 매력도 높아지고 있습니다. ISO 및 SOC 인증과 같은 보안 실적은 표준 조달 심사의 일부로 포함되어 있으며, 호스팅 서비스 선택은 기술적 선호도와 마찬가지로 보증 증거를 바탕으로 결정되고 있습니다. 따라서 지속가능성 성과 관리 소프트웨어 시장은 도입 방식 측면에서 유연성을 유지하고 있지만, 가장 강력한 성장을 주도하고 있는 것은 빈번한 업데이트와 광범위한 워크플로우 조정에 대응할 수 있는 모델입니다. 이러한 균형 덕분에 공급업체는 모든 고객에게 단일 아키텍처를 강요하지 않으면서도, 대규모 세계 기업부터 전문성이 높은 공공 부문 및 규제 대상 구매자에 이르기까지 폭넓게 대응할 수 있게 됩니다.

지역별 분석

2025년, 북미는 지속가능성 성과 관리 소프트웨어 시장 점유율의 34.53%를 차지했으며, 구매자들이 공식 보고 요건을 충족하고 기업용 소프트웨어 도입이 활발해짐에 따라 이 지역은 선도적인 위치를 유지했습니다. 미국 시장은 SEC(미국 증권거래위원회)의 기후 변화 공시 규정의 혜택을 받고 있으며, 캘리포니아주의 SB 253 및 SB 261 법안에 따라 대기업에 대한 배출량 보고 및 기후 관련 재무 보고 의무가 더욱 강화되고 있습니다. 또한, 이 지역은 기존 엔터프라이즈 시스템이 잘 갖춰져 있다는 장점도 있어, 기업이 재무, 조달, 보고 업무 흐름에 지속가능성 요소를 추가할 때의 장벽이 낮아집니다. 캐나다에서는 연방 정부의 규제 대상인 금융기관에 대한 기후 리스크 공시 기대가 추가적인 수요원으로 작용하고 있으며, 이는 금융 주도형 이용 사례에서의 도입을 촉진하고 있습니다. 남미 시장은 여전히 규모가 작지만, 수출업체와 주요 기업들이 고객, 투자자, 해외 컴플라이언스 체인으로부터의 기대가 높아짐에 따라 지속가능성 성과 관리 소프트웨어 시장의 중요성은 계속해서 커지고 있습니다.

2026년에는 유럽이 규정 준수 중심 수요가 가장 견고한 시장이 될 것으로 전망됩니다. 이는 기업이 단일 공시 요건뿐만 아니라 여러 가지 지속가능성 관련 프레임워크를 준수해야 하는 경우가 많기 때문입니다. 따라서 수작업에 의한 중복 작업을 필요로 하지 않고, 보고, 보증, 분류 체계 매핑, 공급업체 모니터링과 같은 업무 간에 동일한 데이터를 재사용할 수 있는 플랫폼의 가치가 높아지고 있습니다. 따라서 지속가능성 성과 관리 소프트웨어 시장은 최종 보고서 자체만큼이나 업무 흐름의 폭이 중요한 유럽 시장에서 유리한 위치를 차지하고 있습니다. EFRAG이 간소화된 기준 초안을 발표한 후, Workiva는 2026년 5월에 지속가능성 플랫폼을 업데이트하여, “Simplified ESRS Intelligence”을 추가한 것은 소프트웨어 공급업체가 보다 신속한 제품 지원을 통해 진화하는 유럽의 보고 요구 사항에 어떻게 대응하고 있는지를 반영한 것입니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역 부문으로, 2031년까지 연평균 성장률(CAGR)이 17.83%를 나타낼 것으로 전망되며, 이 지역 기업들이 보다 체계적인 지속가능성 데이터 시스템을 구축해 나감에 따라 상당한 성장 여지가 있음을 시사하고 있습니다. 아시아태평양의 지속가능성 성과 관리 소프트웨어 시장의 성장은 정보 공개에 대한 기대감 고조, 다국적 기업 고객들공급업체 데이터 수요 증가, 보다 체계적인 ESG 보고 프로세스로의 광범위한 전환에 힘입어 이루어지고 있습니다. 이 지역의 많은 기업들이 처음으로 공식적인 워크플로를 구축하고 있어, 확장 가능한 온보딩, 경량화된 배포 모델, 강력한 공급업체 연동을 제공할 수 있는 벤더에게 시장 기회가 열리고 있습니다. 중동 및 아프리카는 여전히 규모가 작지만, 각국의 전환 의제, 자본 시장의 기대, 상장 기업의 보고 요구가 성숙해짐에 따라 기업의 지속가능성 프로그램은 점차 체계화되고 있습니다. 따라서, 지속가능성 성과 관리 소프트웨어 시장의 다음 단계 지역적 확장은 현재 북미와 유럽이 가장 확고한 수요 거점임에도 불구하고, 시스템 도입 주기가 아직 초기 단계에 있는 지역에서 점점 더 많이 이루어질 것으로 전망됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the sustainability performance management software market was valued at USD 5.36 billion in 2025 and is estimated to grow from USD 6.01 billion in 2026 to reach USD 13.05 billion by 2031, at a CAGR of 14.04% during the forecast period 2026-2031.

This report is Segmented by Component (Software, and Service), Deployment Type (Cloud-Based, On-Premise, and Hybrid), Application (Environmental Performance Management, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Sustainability Performance Management Software Market Trends and Insights

Rising Regulatory Disclosure Mandates

European and U.S. reporting rules are pushing companies to replace loose reporting processes with systems that can support structured records, controlled workflows, and repeatable disclosure output. The sustainability performance management software market benefits directly from this shift, as companies can no longer rely on disconnected files when aligning operational metrics with formal filing calendars and internal review steps. In the United States, the SEC climate disclosure rule requires large accelerated filers to disclose Scope 1 and Scope 2 emissions for fiscal years beginning in 2025 and filed in 2026, which creates a defined compliance trigger for software procurement and data cleanup programs. European disclosure obligations are creating a similar effect by increasing the need for consistent tagging, evidence storage, version control, and assurance support across multiple teams. The result is that software spending is moving into planned operating budgets rather than remaining in short-term pilot programs, which strengthens baseline demand in the sustainability performance management software market. This also brings suppliers into the same cycle, because large enterprises need cleaner upstream inputs before they can complete their own reporting and assurance work.

AI-Enabled Audit Readiness and Continuous Controls Monitoring

The sustainability performance management software market is gaining from a clear move away from annual, document-heavy reporting toward continuous monitoring and earlier issue detection. Buyers now want platforms that can identify missing fields, trace source records, and connect regulatory requirements with business data before legal and assurance teams begin their final review. SAP announced new sustainability AI agents in May 2026, including a Footprint Optimization Agent that reduces time spent on Scope 1, Scope 2, and Scope 3 scenario modeling from one working day to 20 minutes, and a Sustainability Regulatory Readiness Agent that automates mapping between materiality assessments and reporting requirements. IBM also expanded this direction in April 2026 with Envizi Emissions Calculations in Excel, which helps companies move manual emissions work into a more scalable and auditable reporting flow. These product moves matter because AI is no longer being treated only as a speed tool, but as a control layer that can reduce review pressure and improve reporting consistency. That shift helps vendors increase platform relevance across finance, audit, and compliance groups, broadening the value proposition of the sustainability performance management software market.

Fragmented Enterprise Data Architecture Inhibits Deployment

Many companies still store ESG-related information across finance, procurement, operations, HR, legal, and facility systems, making completeness and ownership difficult to manage. Schneider Electric noted that organizations often end up using one reporting system per jurisdiction, which increases reconciliation work and limits the operational value of the data they collect. The same problem slows the sustainability performance management software market because deployments take longer when data sources are inconsistent, definitions are not aligned, and source evidence is spread across many teams. Research published in 2025 on ScienceDirect also found that fewer than 20% of ESG ontology and data architecture projects validate their models against authentic enterprise data, which highlights the gap between clean design concepts and live operating conditions. For vendors, that means longer implementation periods, higher service demands, and a greater chance that customers delay full rollout until basic data governance improves. It also gives providers with pre-built ERP, HR, and procurement connectors an advantage, as faster integration reduces the effort needed to prove value early in the buying cycle.

Other drivers and restraints analyzed in the detailed report include:

- Investor and Lender Preference For Verifiable ESG Data

- Scope 3 Supplier Data Digitization Pressure

- High Integration and Change Management Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 74.13% of revenue in 2025, indicating that the largest spending pool still resides in core platforms rather than project-based support work. That weighting reflects how the sustainability performance management software market has matured, because once a platform is integrated with financial close processes, audit records, supplier inputs, and reporting controls, replacing it becomes far more difficult and disruptive. Renewal decisions, therefore, carry more than licensing implications, since moving away from an installed system can trigger data migration, process redesign, and revalidation work across several teams. IBM's April 2026 launch of Envizi Emissions Calculations in Excel shows how major vendors are still expanding software reach into manual emissions workflows that had not yet been fully absorbed into enterprise systems.

Services are projected to expand at a 16.83% CAGR through 2031, which shows that implementation, data design, and ongoing support remain critical even as platform adoption rises. Companies often need help with materiality work, source mapping, control design, assurance preparation, and workflow configuration before they can fully realize the value of the underlying application layer. Managed services are also becoming increasingly relevant for organizations without large in-house sustainability teams, especially when reporting deadlines are near and data ownership spans several departments. This pattern keeps services closely tied to the sustainability performance management software market, because customers frequently buy advisory and support work alongside the software rather than as a separate category. It also means vendors with stronger partner ecosystems may sustain better expansion potential, since they can support a broader customer base without carrying all delivery work on their own.

Cloud-based deployment accounted for 63.12% of the sustainability performance management software market in 2025 and is projected to grow at a 16.53% CAGR through 2031, confirming that the leading delivery model is still gaining momentum rather than losing it. This reflects the practical reality that reporting rules, taxonomy changes, validation logic, and workflow requirements are changing too often for most customers to rely on slower upgrade cycles. Workiva's May 2026 sustainability release added a Simplified ESRS Intelligence knowledge base tied to draft simplified standards published by EFRAG in December 2025, which illustrates how cloud releases can respond quickly to evolving reporting needs. In the sustainability performance management software industry, the release pace matters because customers increasingly want a single platform that can accommodate rule changes without repeated local upgrades or project-heavy reconfiguration.

On-premise deployment still matters for government users, highly regulated institutions, and industrial operators that place added weight on data residency, internal hosting, or local control over sensitive records. Hybrid models are also gaining appeal where companies want centralized reporting and analytics in the cloud but still need some processing layers to remain closer to local systems or region-specific data controls. Security credentials such as ISO and SOC-style attestations have become part of standard procurement reviews, meaning hosting choice is now judged on assurance evidence as much as on technical preference. The sustainability performance management software market, therefore, remains flexible in deployment terms, but the strongest growth continues to be driven by models that can handle frequent updates and broad workflow coordination. That balance lets vendors address both large global clients and more specialized public-sector or regulated buyers without forcing one architecture on every customer.

Complete Report Scope:

- By Component

- Software

- Service

- By Deployment Type

- Cloud Based

- On Premise

- Hybrid

- By Application

- Environmental Performance Management

- Carbon and Emissions Management

- Resource and Waste Management

- Sustainability Compliance Management

- ESG and Sustainability Reporting

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By End-Use Industry

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Construction and Infrastructure

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 34.53% of the sustainability performance management software market share in 2025, maintaining its leading regional position as buyers respond to formal reporting requirements and strong enterprise software adoption. The U.S. market benefits from the SEC's climate disclosure rule, while California's SB 253 and SB 261 add further pressure on large companies to report on emissions and climate-related financial reporting. This region also has an advantage in installed enterprise systems, which reduces friction when companies add sustainability layers to finance, procurement, and reporting workflows. Canada adds another source of demand through climate risk disclosure expectations for federally regulated financial institutions, which supports adoption in finance-led use cases. South America remains smaller, but the sustainability performance management software market continues to gain relevance there as exporters and larger listed companies face growing expectations from customers, investors, and overseas compliance chains.

Europe represents the deepest compliance-led demand environment in 2026, because companies often need to align several sustainability-related frameworks rather than just one disclosure requirement. That raises the value of platforms that can reuse the same data across reporting, assurance, taxonomy mapping, and supplier oversight tasks without the need for repeated manual work. The sustainability performance management software market is, therefore, well placed in Europe, where workflow breadth can matter as much as the final report itself. Workiva's May 2026 update to its sustainability platform, which added Simplified ESRS Intelligence after EFRAG published draft simplified standards, reflects how software providers are responding to evolving European reporting needs with faster product support.

Asia-Pacific is the fastest-growing regional segment, with a 17.83% CAGR through 2031, suggesting a large expansion runway as companies across the region build more formal sustainability data systems. Growth in the sustainability performance management software market across Asia-Pacific is supported by rising disclosure expectations, growing supplier-data demands from multinational customers, and a broad shift toward more structured ESG reporting processes. Many companies in the region are building formal workflows for the first time, creating space for vendors that can offer scalable onboarding, lighter deployment models, and stronger supplier connectivity. The Middle East and Africa are still smaller, but enterprise sustainability programs are becoming more structured as national transition agendas, capital-market expectations, and listed-company reporting needs mature. The sustainability performance management software market should therefore see its next layer of geographic expansion increasingly come from regions that are still earlier in the system adoption cycle, even though North America and Europe remain the most established demand centers today.

- Workiva Inc.

- Wolters Kluwer N.V.

- SAP SE

- IBM Corporation

- Salesforce, Inc.

- Sphera Solutions, Inc.

- Schneider Electric SE

- Intelex Technologies ULC

- Cority Software Inc.

- UL Solutions Inc.

- Microsoft Corporation

- Diligent Corporation

- ServiceNow, Inc.

- EcoVadis SAS

- OneTrust, LLC

- Benchmark Digital Partners LLC

- Persefoni AI, Inc.

- FigBytes Inc.

- Quentic GmbH

- IsoMetrix Software (Pty) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Regulatory Disclosure Mandates

- 4.2.2 AI Enabled Audit Readiness And Continuous Controls Monitoring

- 4.2.3 Investor And Lender Preference For Verifiable ESG Data

- 4.2.4 Scope 3 Supplier Data Digitization Pressure

- 4.2.5 Finance To Sustainability Data Convergence In ERP And FP and A Workflows

- 4.2.6 Sustainability Data Trust And Assurance Gap Driving Platform Adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented Enterprise Data Architecture Inhibits Deployment

- 4.3.2 High Integration And Change Management Burden

- 4.3.3 Immature Supplier Data Quality Slows Scope 3 Automation

- 4.3.4 Assurance And Liability Concerns For AI Generated ESG Narratives

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Service

- 5.2 By Deployment Type

- 5.2.1 Cloud Based

- 5.2.2 On Premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Environmental Performance Management

- 5.3.2 Carbon and Emissions Management

- 5.3.3 Resource and Waste Management

- 5.3.4 Sustainability Compliance Management

- 5.3.5 ESG and Sustainability Reporting

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small And Medium Enterprises

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Construction and Infrastructure

- 5.5.7 Government and Public Sector

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workiva Inc.

- 6.4.2 Wolters Kluwer N.V.

- 6.4.3 SAP SE

- 6.4.4 IBM Corporation

- 6.4.5 Salesforce, Inc.

- 6.4.6 Sphera Solutions, Inc.

- 6.4.7 Schneider Electric SE

- 6.4.8 Intelex Technologies ULC

- 6.4.9 Cority Software Inc.

- 6.4.10 UL Solutions Inc.

- 6.4.11 Microsoft Corporation

- 6.4.12 Diligent Corporation

- 6.4.13 ServiceNow, Inc.

- 6.4.14 EcoVadis SAS

- 6.4.15 OneTrust, LLC

- 6.4.16 Benchmark Digital Partners LLC

- 6.4.17 Persefoni AI, Inc.

- 6.4.18 FigBytes Inc.

- 6.4.19 Quentic GmbH

- 6.4.20 IsoMetrix Software (Pty) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space And Unmet Need Assessment