|

시장보고서

상품코드

2073117

베어메탈 스위치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bare Metal Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

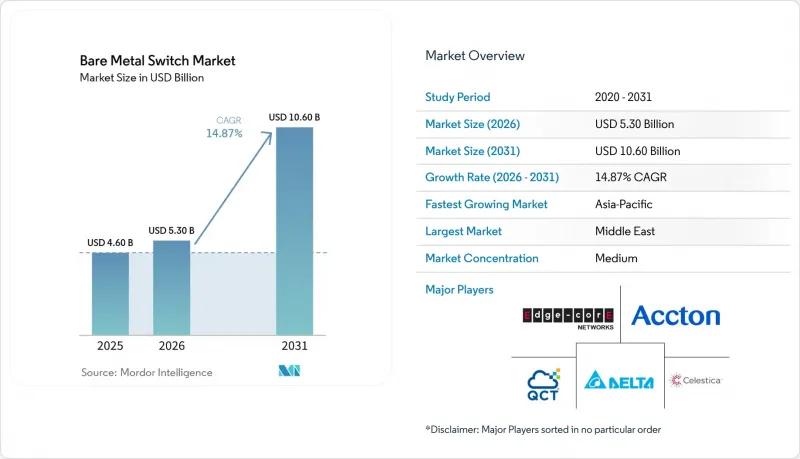

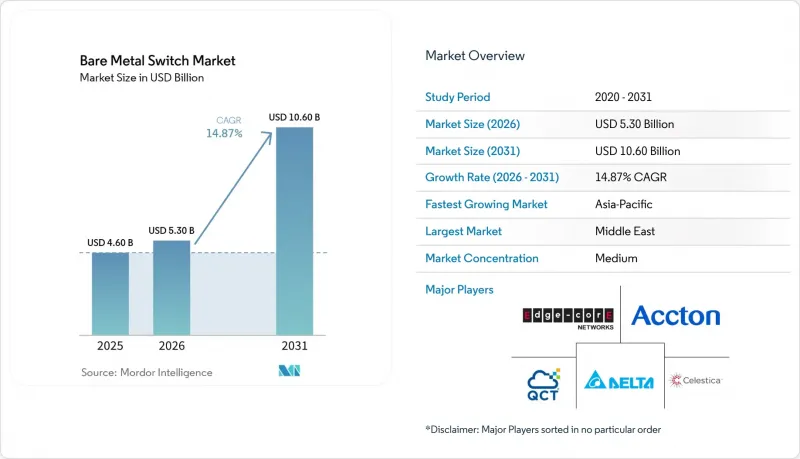

Mordor Intelligence에 의하면, 베어메탈 스위치 시장 규모는 2025년 46억 달러에서 2026년에는 53억 달러로 확대되어 2026년부터 2031년까지 CAGR 14.87%로 성장을 지속하여, 2031년에는 106억 달러에 이를 것으로 예측됩니다.

본 보고서는 스위치 유형(오픈 이더넷 스위치, 브랜드 베어메탈 스위치), 포트 속도(1/10 Gbps, 25/40 Gbps, 100 Gbps 이상), 도입 형태(On-Premise 데이터센터, 클라우드 서비스 제공업체 등), 최종 사용자 산업(클라우드 제공업체, 통신 업계 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 베어메탈 스위치 시장 동향 및 인사이트

하이퍼스케일 데이터센터에서 디스어그리게이트형 네트워크의 도입 확대

하이퍼스케일 사업자들은 스위치를 차별화된 시스템이 아닌 상호 호환 가능한 구성 요소로 간주하며, 디스어그리게이트형 네트워킹을 장기적인 설비 투자(CAPEX) 모델에 통합하고 있습니다. 100만 대 이상의 디바이스에 걸친 오픈 NOS의 대규모 도입으로 인해, Broadcom Tomahawk 및 Marvell Teralynx와 같은 ASIC 플랫폼이 전 세계 여러 지역에서 표준화되고 있습니다. 베어 메탈 패브릭은 모듈식이며 핫스왑이 가능한 구성 요소를 통해 랙당 네트워크 비용을 약 38% 절감하는 동시에 평균 복구 시간(MTTR)을 단축하고 있습니다. 고성능 아키텍처 덕분에 현재 랙당 처리량이 최대 1.6 Tbps에 달하며, 독점 시스템과 동등한 처리량을 실현하고 있습니다. 이러한 성과를 바탕으로 ODM 및 클라우드 제공업체와의 공동 개발이 가속화되고, 혁신 주기가 단축됨에 따라 베어메탈 스위치 시장 전체에서 규모의 경제에 따른 비용 효율성이 더욱 높아지고 있습니다.

독점적 스위치에 대한 비용 최적화

기업과 통신 사업자들은 초기 설비 투자(Capex)에 그치지 않는 총소유비용(TCO) 절감 효과를 정량적으로 평가했습니다. 2025년 업계 조사에 따르면, 자체 관리형 네트워크 OS를 도입하면 5년간의 총 소유 비용(TCO)이 최대 42% 절감되며, 타사 지원을 포함하더라도 그 차이는 약 18%로 줄어듭니다. 대규모 통신 사업자의 도입 사례에 따르면, 오픈 이더넷 스위치로 전환한 후 100 Gbps 포트당 약 1,200달러의 단위 전송 비용이 절감된 것으로 보고되었습니다. 200 Gbps 이상의 부문에서는 가격 차이가 크게 벌어지고 있으며, 독점적인 시스템의 경우 60%에서 80%의 할증 가격이 부과되고 있습니다. 이러한 비용 차이로 인해 400 Gbps 및 800 Gbps 아키텍처로의 전환이 가속화되고 있으며, 이는 2031년까지 베어메탈 스위치 시장의 지속적인 두 자릿수 성장을 뒷받침하고 있습니다.

기업 내 사내 통합 노하우의 부족

하이퍼스케일 환경을 제외하면, 많은 조직이 리눅스 네트워킹에 대한 전문 지식이 부족하여 디스어그리게이트형 스위치의 도입에 제약을 받고 있습니다. 업계 자료에 따르면, 유럽 기업의 약 68%가 기술 격차를 주요 장애물로 꼽고 있습니다. 팀이 SONiC이나 DENT와 같은 플랫폼을 익히는 데는 보통 12-18개월이 소요되므로, ROI 달성이 지연되고 실행 위험이 높아집니다. 남미와 아프리카의 소규모 클라우드 제공업체들은 시스템 통합사업자에 25%에서 40%의 할증료를 지불하는 경우가 많아, 비용 면에서의 경쟁력이 약화되고 있습니다. 금융 서비스 기업들은 공급업체가 지원하는 시스템과 연계된 엄격한 변경 관리 프로세스 때문에 여전히 신중한 태도를 취하고 있습니다. 교육 체계가 확대되기 전까지는 통합 기능이 베어메탈 스위치 시장의 단기적인 보급을 제한할 것으로 보입니다.

부문별 분석

브랜드화된 베어메탈 스위치는 ODM 업체들이 범용 하드웨어에 상용 지원 서비스를 추가함에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 18.53%를 나타낼 것으로 예측되며, 이는 시장 전체의 성장 속도를 상회할 전망입니다. 오픈 이더넷 스위치는 네트워크 운영 체제를 자체적으로 관리하는 하이퍼스케일러들의 주도 하에 2025년에는 시장 점유율의 약 46.36%를 차지했습니다. ODM의 실적은 기업 시장에서 강력한 성장세를 보이고 있으며, 구매자들이 단일 공급업체의 책임 체제에 대해 추가 비용을 지불함에 따라 브랜드 전환 매출이 급증하고 있습니다. 엔터프라이즈급 오픈 NOS 배포판은 비용 면에서의 우위를 유지하면서도, 독점적인 SLA와 동등한 서비스를 제공함으로써 금융 및 의료 등 규제 산업 분야로의 확산을 가능하게 하고 있습니다.

오픈형 솔루션은 엔지니어링의 심도 있는 전문성이 통합 위험을 상쇄하는 클라우드 및 통신 환경에서 계속해서 주류를 이루는 한편, 정부 및 공공 부문에서는 거버넌스 및 규정 준수 요건으로 인해 브랜드 제품에 대한 수요가 증가하고 있습니다. 그 결과, 브랜드 제품 부문의 매출액은 2026년 약 19억 달러에서 2031년까지 44억 달러로 확대되어 시장 총액에서 차지하는 점유율이 높아질 것으로 예측됩니다. 실리콘 최적화와 풀스택 지원을 결합한 ODM은 증가하는 수요를 흡수할 준비가 되어 있는 반면, 순수 제조업체는 이익률 압박에 직면하게 될 것입니다.

200 Gbps를 초과하는 부문은 더 높은 이스트-웨스트 대역폭을 필요로 하는 AI 워크로드에 힘입어 연평균 성장률(CAGR) 25.26%로 확대될 것으로 예측됩니다. 2025년에는 25/40 Gbps 부문이 시장 규모의 약 38.49%를 차지했으나, 각 하이퍼스케일러 기업들은 여러 데이터센터 지역에 걸쳐 400 Gbps 패브릭을 급속히 확장함에 따라 오버구독 비율은 약 1.5 대 1까지 낮아졌습니다. 시판용 실리콘 기술의 발전이 이러한 전환을 가능하게 했으며, 새로운 아키텍처 덕분에 고밀도 800 Gbps 구축이 대규모로 지원되고 있습니다.

광 모듈의 비용 절감과 포트 밀도 향상으로 인해, 2028년까지 100 Gbps가 엔터프라이즈용 톱 오브 랙(Top-of-Rack)의 사실상의 표준이 되고, 1/10 Gbps는 엣지 환경이나 레거시 환경으로 전환될 것으로 예측됩니다. 최대 25.6 Tbps의 처리량을 구현하는 차세대 실리콘의 등장으로, 범용 실리콘 생태계 내의 경쟁이 치열해지고 있습니다. 그 결과, 포트 속도의 구성 비율은 더 높은 대역폭 계층으로 이동하고 있으며, 이는 베어메탈 스위치 시장의 추가적인 성장을 뒷받침하고 있습니다.

지역별 분석

북미는 미국 내 하이퍼스케일러의 지배력과 캐나다 통신 사업자들의 5G 독립형(SA) 네트워크로의 업그레이드에 힘입어 베어메탈 스위치 시장에서 가장 큰 점유율을 차지하고 있습니다. 대규모 네트워크 현대화 프로그램은 지속가능성 목표와 점점 더 부합하고 있으며, 통신 사업자들은 전력 소비와 탄소 발자국을 줄이기 위해 400 Gbps SONiC 기반 패브릭으로의 전환을 추진하고 있습니다. 이러한 동향은 조달 결정이 더 이상 성능이나 비용에만 좌우되는 것이 아니라, 에너지 효율 지표도 고려되게 되었음을 보여줍니다. 이 지역은 성숙한 클라우드 생태계, 강력한 ODM 파트너십, 그리고 더욱 신속한 제품 교체 주기의 혜택을 누리며 선도적 입지를 공고히 하고 있습니다.

아시아태평양은 중국, 인도, 동남아시아 전역에서 활발히 진행되고 있는 데이터센터 확충에 힘입어 2025년 매출의 약 32.97%를 차지했습니다. 정부 주도의 반도체 및 디지털 인프라 프로그램을 통해 오픈 네트워킹 하드웨어의 도입이 가속화되고 있으며, 국내 제조 및 네트워킹 역량에 대한 막대한 투자가 이루어지고 있습니다. 인도와 중국은 주요 조립 및 수요 거점으로서의 위상을 확립해 가고 있는 반면, 동남아시아 국가들에서는 디지털 정부 및 클라우드 인프라 확충이 진행되고 있습니다. 이러한 정책 지원, 생산 능력 확대, 비용 절감 의식의 고조가 맞물리면서, 해당 지역은 베어메탈 스위치 도입에 있어 주요 성장 동력으로서의 역할을 더욱 공고히 하고 있습니다.

중동은 사우디아라비아와 아랍에미리트의 주권 클라우드 구상 및 스마트 시티에 대한 투자에 힘입어, 2031년까지 연평균 성장률(CAGR) 17.12%를 기록하며 성장할 것으로 전망됩니다. 유럽에서는 조달 구조의 세분화로 인해 성장세가 완만하지만, 에너지 효율에 대한 규제적 압력으로 인해 오픈 하드웨어의 단계적 도입이 진행되고 있습니다. 남미와 아프리카는 여전히 초기 단계 시장이며, 예산 제약과 비용 효율이 높은 인프라에 대한 의존이 특징입니다. 이러한 지역에서는 베어메탈 스위치가 고가의 독점 시스템에 대한 현실적인 대안으로 부상하고 있으며, 디지털 인프라에 대한 투자가 확대됨에 따라 단계적인 도입이 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the bare metal switch market size is expected to grow from USD 4.6 billion in 2025 to USD 5.3 billion in 2026 and is forecast to reach USD 10.6 billion by 2031 at 14.87% CAGR over 2026-2031.

This report is Segmented by Switch Type (Open Ethernet Switches, Branded Bare Metal Switches), Port Speed (1/10 Gbps, 25/40 Gbps, 100 Gbps and More), Deployment Mode (On-Premise Data Centers, Cloud Service Providers, and More), End User Industry (Cloud Providers, Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Bare Metal Switch Market Trends and Insights

Growing Adoption of Disaggregated Networking in Hyperscale Data Centers

Hyperscale operators are embedding disaggregated networking into long-term capex models, treating switches as interchangeable building blocks rather than differentiated systems. Large-scale deployments of open NOS across more than 1 million devices have standardized ASIC platforms such as Broadcom Tomahawk and Marvell Teralynx across multiple global regions. Bare metal fabrics have reduced per-rack networking costs by approximately 38% while improving mean-time-to-repair through modular, hot-swappable components. High-performance architectures now achieve up to 1.6 Tbps per-rack throughput, matching the throughput of proprietary systems. These outcomes are accelerating ODM and cloud-provider co-development, shortening innovation cycles and reinforcing scale-driven cost efficiencies across the bare-metal switch market.

Cost Optimization Over Proprietary Switches

Enterprises and telecom operators are quantifying the total cost of ownership savings that extend beyond initial capex. A 2025 industry study indicates up to 42% lower five-year TCO with self-managed network operating systems, narrowing to about 18% when third-party support is included. Large telecom deployments have reported unit transport cost reductions of around USD 1200 per 100 Gbps port after shifting to open Ethernet switches. Pricing gaps widen significantly in the 200+ Gbps segment, where proprietary systems carry 60% to 80% premiums. This cost differential is accelerating migration toward 400 Gbps and 800 Gbps architectures, supporting sustained double-digit growth in the bare-metal switch market through 2031.

Limited In-House Integration Expertise Among Enterprises

Outside hyperscale environments, many organizations lack Linux networking expertise, constraining adoption of disaggregated switches. Industry data shows about 68% of European enterprises cite skills gaps as the primary barrier. Capability ramp up typically takes 12 to 18 months as teams learn platforms such as SONiC and DENT, delaying ROI and increasing execution risk. Smaller cloud providers in South America and Africa often pay 25% to 40% premiums to system integrators, reducing cost advantages. Financial services firms remain cautious due to strict change control processes tied to vendor supported systems. Until training pipelines scale, integration capability will limit near term penetration in the bare metal switch market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Scalability Needs for Cloud-Native 5G Core Networks

- Emergence of Telco Open RAN Fronthaul Transport Requirements

- Vendor Accountability and Single Point of Support Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Branded bare-metal switches are projected to grow at a 18.53% CAGR from 2026 to 2031, outpacing the overall market as ODMs layer commercial support on commodity hardware. Open Ethernet switches held about 46.36% of the market share in 2025, driven by hyperscalers that self-manage their network operating systems. ODM performance indicates strong enterprise traction, with branded switch revenue rising sharply as buyers pay premiums for single vendor accountability. Enterprise-grade open NOS distributions are replicating proprietary SLAs while retaining cost advantages, enabling penetration into regulated sectors such as finance and healthcare.

The open variant will remain dominant in cloud and telecom environments where engineering depth offsets integration risk, while government and public sector demand increasingly favors branded offerings due to governance and compliance needs. As a result, branded segment revenue is expected to expand from about USD 1.9 billion in 2026 to USD 4.4 billion by 2031, increasing its share of total market value. ODMs combining silicon alignment with full stack support are positioned to capture incremental demand, while pure play manufacturers face margin pressure.

The 200+ Gbps segment is expected to expand at a 25.26% CAGR, driven by AI workloads that require higher east-west bandwidth. While the 25/40 Gbps segment accounted for about 38.49% of the market size in 2025, hyperscalers are rapidly scaling 400 Gbps fabrics across multiple data center regions, reducing oversubscription ratios to around 1.5 to 1. Merchant silicon advancements are enabling this transition, with new architectures supporting high-density 800 Gbps deployments at scale.

Declining optics costs and improved port density are expected to make 100 Gbps the default enterprise top-of-rack standard by 2028, shifting 1/10 Gbps to edge and legacy environments. Next-generation silicon offering up to 25.6 Tbps of throughput is intensifying competition in the merchant ecosystem. As a result, the port-speed mix is shifting toward higher-bandwidth tiers, supporting stronger growth in the bare-metal switch market.

Complete Report Scope:

- By Switch Type

- Open Ethernet Switches

- Branded Bare Metal Switches

- By Port Speed

- 1/10 Gbps

- 25/40 Gbps

- 100 Gbps

- 200+ Gbps

- By Deployment Mode

- On-premise Data Centers

- Cloud Service Providers

- Telecom Central Offices

- Edge Computing Sites

- By End User Industry

- Cloud Providers (Hyperscale)

- Telecommunications

- Enterprises

- Government and Public Sector

- Other End User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America accounts for the largest share of the bare-metal switch market, driven by hyperscaler dominance in the United States and 5G standalone upgrades among Canadian telecom operators. Large-scale network modernization programs are increasingly aligned with sustainability targets, with operators transitioning to 400 Gbps SONiC-based fabrics to reduce power consumption and the carbon footprint. These developments indicate that procurement decisions are no longer driven solely by performance and cost, but also by energy efficiency metrics. The region benefits from mature cloud ecosystems, strong ODM partnerships, and faster refresh cycles, reinforcing its leadership position.

Asia Pacific accounted for about 32.97% of 2025 revenue, supported by aggressive data center expansion across China, India, and Southeast Asia. Government-backed semiconductor and digital infrastructure programs are accelerating the adoption of open networking hardware, with significant investments in domestic manufacturing and networking capabilities. India and China are positioning themselves as key assembly and demand hubs, while Southeast Asian economies are expanding digital government and cloud infrastructure. This combination of policy support, capacity expansion, and cost sensitivity is strengthening the region's role as a major growth engine for bare metal switch deployments.

The Middle East is projected to grow at 17.12% CAGR through 2031, driven by sovereign cloud initiatives and smart city investments in Saudi Arabia and the United Arab Emirates. Europe shows moderate growth, driven by fragmented procurement structures, although regulatory pressure on energy efficiency is supporting the gradual adoption of open hardware. South America and Africa remain early-stage markets, characterized by budget constraints and reliance on cost-efficient infrastructure. In these regions, bare-metal switches offer a viable alternative to expensive, proprietary systems, enabling gradual adoption as digital infrastructure investments expand.

- Edgecore Networks Corporation

- Accton Technology Corporation

- Delta Electronics, Inc.

- Quanta Cloud Technology Inc.

- Celestica Inc.

- Super Micro Computer, Inc.

- Interface Masters Technologies, Inc.

- UfiSpace Co., Ltd.

- Inventec Corporation

- Alpha Networks Inc.

- Silicom Ltd.

- Wistron NeWeb Corporation

- Penguin Computing, Inc.

- Lanner Electronics Inc.

- Allied Telesis Holdings K.K.

- FS.COM Inc.

- Netberg LLC

- NoviFlow Inc.

- Ciena Corporation

- Marvell Technology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Disaggregated Networking in Hyperscale Data Centers

- 4.2.2 Rapid Scalability Needs for Cloud-native 5G Core Networks

- 4.2.3 Cost Optimization Over Proprietary Switches

- 4.2.4 Emergence of Telco Open RAN Fronthaul Transport Requirements

- 4.2.5 Sustainability Mandates Driving Energy-efficient Network Fabric Upgrades

- 4.2.6 Government-backed Open Hardware Initiatives in Asia-Pacific

- 4.3 Market Restraints

- 4.3.1 Limited In-house Integration Expertise Among Enterprises

- 4.3.2 Vendor Accountability and Single Point of Support Concerns

- 4.3.3 Interoperability Challenges with Legacy Network Management Systems

- 4.3.4 Supply Chain Volatility for Merchant Silicon Chipsets

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Buyer Power

- 4.8.2 Supplier Power

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Open Ethernet Switches

- 5.1.2 Branded Bare Metal Switches

- 5.2 By Port Speed

- 5.2.1 1/10 Gbps

- 5.2.2 25/40 Gbps

- 5.2.3 100 Gbps

- 5.2.4 200+ Gbps

- 5.3 By Deployment Mode

- 5.3.1 On-premise Data Centers

- 5.3.2 Cloud Service Providers

- 5.3.3 Telecom Central Offices

- 5.3.4 Edge Computing Sites

- 5.4 By End User Industry

- 5.4.1 Cloud Providers (Hyperscale)

- 5.4.2 Telecommunications

- 5.4.3 Enterprises

- 5.4.4 Government and Public Sector

- 5.4.5 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Edgecore Networks Corporation

- 6.4.2 Accton Technology Corporation

- 6.4.3 Delta Electronics, Inc.

- 6.4.4 Quanta Cloud Technology Inc.

- 6.4.5 Celestica Inc.

- 6.4.6 Super Micro Computer, Inc.

- 6.4.7 Interface Masters Technologies, Inc.

- 6.4.8 UfiSpace Co., Ltd.

- 6.4.9 Inventec Corporation

- 6.4.10 Alpha Networks Inc.

- 6.4.11 Silicom Ltd.

- 6.4.12 Wistron NeWeb Corporation

- 6.4.13 Penguin Computing, Inc.

- 6.4.14 Lanner Electronics Inc.

- 6.4.15 Allied Telesis Holdings K.K.

- 6.4.16 FS.COM Inc.

- 6.4.17 Netberg LLC

- 6.4.18 NoviFlow Inc.

- 6.4.19 Ciena Corporation

- 6.4.20 Marvell Technology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment