|

시장보고서

상품코드

2073153

자가면역성 용혈성 빈혈 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Autoimmune Hemolytic Anemia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

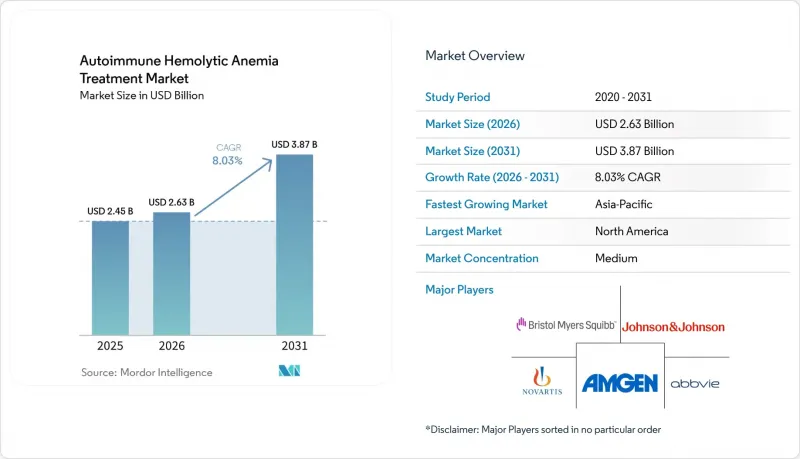

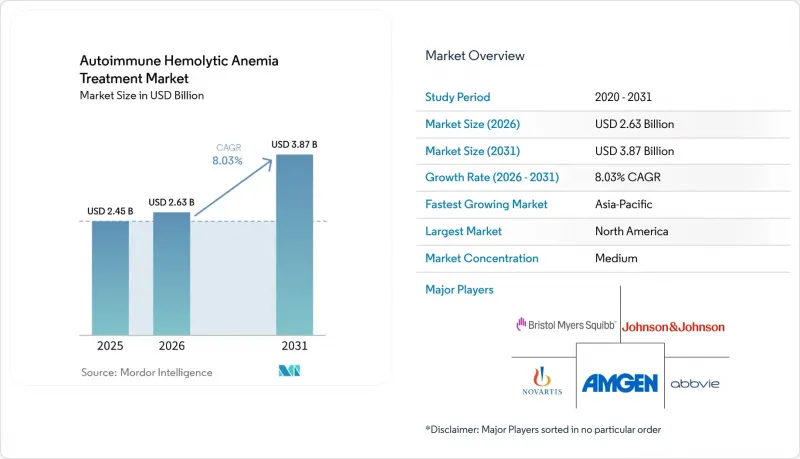

Mordor Intelligence에 의하면, 자가면역성 용혈성 빈혈 치료 시장 규모는 2025년 24억 5,000만 달러, 2026년 26억 3,000만 달러에서 2031년까지 38억 7,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.03%를 나타낼 전망입니다.

본 보고서는 유형별(온식, 냉식, 혼합식, 2차식), 약제 분류별(코르티코스테로이드, IVIG, 단일클론 항체, 보체 억제제, 면역억제제, BTK 억제제, Fcrn 억제제), 투여 경로별(경구 투여 등), 유통 채널별(병원 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 자가면역성 용혈성 빈혈 치료 시장 동향 및 인사이트

난치성 AIHA에서 스테로이드 절약 요법에 대한 필요성 증가

많은 열성 자가면역성 용혈성 빈혈(AIHA) 환자에서 코르티코스테로이드는 여전히 초기 헤모글로빈 수치를 개선시켜 주지만, 용량 감량 후 재발이 빈번하게 발생하기 때문에 자가면역성 용혈성 빈혈 치료 시장은 반복적인 치료 주기에 얽매인 상태가 지속되고 있습니다. 또한, 스테로이드의 장기 투여는 당뇨병, 대사성 합병증, 골다공증의 위험을 높이며, 용혈이 부분적으로 억제된 경우라도 삶의 질을 저하시키고, 피할 수 있는 입원을 증가시키고 있습니다. 리툭시맙은 재발성 또는 난치성 질환에 대한 권장 2차 치료제로 자리매김하게 되었으나, 비장 절제술은 발표된 코호트 연구에서 12%의 수술 후 합병증 발생률이 보고됨에 따라 치료 단계에서 후순위로 밀려나게 되었습니다. 이러한 경향은 자가면역성 용혈성 빈혈 치료 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 표적 치료 옵션이 이용 가능해지면, 기존 약물로 치료 중 재발할 때마다 명확한 치료 전환의 계기가 되기 때문입니다. 2025년 ASH 교육 프로그램에서 개괄된 현재의 치료 순서에서도, 새로운 B세포, 형질세포, SYK 및 FcRn을 표적으로 하는 치료법은 릿룩시맙에 이어 두 번째로 중요한 위치를 차지하고 있으며, 이는 여러 치료 단계에 걸쳐 지속적인 수요가 있음을 뒷받침하고 있습니다.

보체 및 FcRn을 표적으로 하는 치료제 파이프라인 준비 현황이 가속화되고 있습니다.

자가면역성 용혈성 빈혈 치료 시장은 현재 최초의 광범위한 적응증을 갖춘 표적 치료제의 물결을 맞이하고 있으며, FcRn 억제가 이러한 변화의 중심에 자리 잡고 있습니다. FcRn을 표적으로 하는 약물은 순환 IgG를 최대 85%까지 감소시킬 수 있으며, 이를 통해 적혈구 파괴를 유발하는 자가항체에 직접 작용하면서도 IgA, IgM 및 선천성 면역 기능을 유지할 수 있습니다. 니포칼리맙은 온형 자가면역성 용혈성 빈혈 분야에서 개발이 가장 진전된 FcRn 프로그램으로, 2/3상 ENERGY 임상시험에서 지속적인 헤모글로빈 반응을 보인 데 따라 현재 FDA의 우선 심사 대상에 포함되어 있습니다. 냉성 자가면역성 용혈성 빈혈의 경우, 이미 ‘스팀리맙’이라는 승인된 표적 치료제가 존재하며, 등록 데이터에 따르면 치료를 받은 환자의 70% 이상에서 평균 치료 기간이 2년 이상 경과한 후에도 새로운 안전성 문제가 나타나지 않아, 실제 임상 현장에서의 지속적인 유효성이 입증되었습니다. 온성 및 냉성 두 가지 적응증을 모두 갖춘 치료제가 동시에 출시됨에 따라, 자가면역성 용혈성 빈혈 치료 시장에서는 의료진의 신뢰도가 높아지고, 보험 급여 측면에서의 지원도 강화될 것으로 예측됩니다.

혈액내과로의 의뢰가 확정되기까지의 진단 지연

진단 지연은 치료받지 못했거나 오진을 받은 환자들이 혈액내과 진료 경로에 도달하지 못하기 때문에 여전히 자가면역성 용혈성 빈혈 치료 시장의 직접적인 제약 요인으로 작용하고 있습니다. 저·중소득 국가에서는 치료 시작 시점에 헤모글로빈 수치가 3 g/dL에서 6 g/dL에 달하는 소아 사례가 보고되고 있으며, 이는 증상이 나타난 후 전문의의 진료를 받기까지의 기간이 지나치게 길다는 점을 반영하고 있습니다. 한랭성 자가면역성 용혈성 빈혈은 말초 청색증이나 한랭 유발성 순환기 증상이 혈액내과로 의뢰되기 전에 다른 질환과 연관지어지는 경향이 있어, 특히 간과되기 쉬운 질환입니다. 고소득 국가라 하더라도 DAT 음성 질환을 진단하기 위해서는 고도의 교차적합성 검사나 용출법이 필요한 경우가 있는데, 이는 지역 검사실에서는 이러한 검사법을 널리 이용할 수 없는 경우가 많기 때문입니다. 진료 체계, 인지도, 진단 능력이 더 광범위하게 개선되기 전까지는 자가면역성 용혈성 빈혈 치료 시장의 환자 수 확대에는 한계가 있는 상황이 지속될 것입니다.

부문별 분석

2025년, 온형 자가면역성 용혈성 빈혈은 자가면역성 용혈성 빈혈 치료 시장 점유율의 68.13%를 차지하며, 전 세계적으로 가장 흔한 아형이라는 평가와 일치했습니다. 따라서, 미국에서는 이 적응증에 대한 공식 승인이 아직 보류 중임에도 불구하고, 자가면역성 용혈성 빈혈 치료 시장은 여전히 “"웜형" 을 중심으로 사업을 전개하고 있습니다. 이러한 격차로 인해, 웜형 치료제의 현재 시장 가치 대부분은 고가의 브랜드 치료제가 아닌, 적응증 외로 사용되는 코르티코스테로이드나 리툭시맙에 의해 창출되고 있습니다. 이 아형은 가장 광범위한 상업적 기반을 갖추고 있으며, 적응증 확대를 위한 단기적인 로드맵이 가장 명확하기 때문에 후기 임상 개발 프로그램의 주요 표적으로 계속해서 자리 잡고 있습니다.

냉형 자가면역성 용혈성 빈혈 시장은 스팀리맙의 기존 시장 입지와 실세계 데이터(REW)의 개선에 힘입어 2031년까지 연평균 성장률(CAGR) 8.78%를 기록하며 성장할 것으로 전망됩니다. 혼합형 자가면역성 용혈성 빈혈은 전체 증례의 불과 5%에서 8%에 불과하며, SLE(전신성 홍반성 루푸스) 등 복잡한 자가면역 배경과 중복되는 경우가 많기 때문에 여전히 수익 규모는 작은 임베디드니다. 실제로, 혼합형 사례의 25%에서 42%가 SLE와 관련이 있습니다. 이차성 자가면역성 용혈성 빈혈 역시 상업적으로는 여전히 제한적인 시장에 머물러 있습니다. 이는 주요 임상시험에서 이러한 환자들이 종종 제외되기 때문이며, 의사가 치료를 실시하고 있다 하더라도 보험 급여 지원이 약화되는 요인이 되고 있습니다. 장기적으로는 난치성 질환이 새로운 가치 영역을 개척할 가능성이 있습니다. 주벤타스 바이오테크놀러지사의 CAR-T 프로그램이 2025년 4월 중국 국가의약품감독관리국(NMPA)으로부터 임상시험 실시 신청(IND) 승인을 받아 임상시험 단계로 진입했기 때문입니다.

2025년 자가면역성 용혈성 빈혈 치료 시장 규모 중 57.38%를 코르티코스테로이드가 차지했습니다. 이는 지속적인 질환 관리라기보다는 1차 선택 약제로서 확고히 자리 잡은 사용 현황과 제네릭 의약품의 낮은 구입 비용을 반영한 것입니다. 재발 위험이 충분히 알려져 있음에도 불구하고, 여전히 대부분의 환자가 스테로이드 치료를 시작하고 있기 때문에 이러한 기존 상황은 계속되고 있습니다. 단일클론 항체, 특히 렙티맙 및 바이오시밀러를 이용한 치료는 2차 치료로서 여전히 중요하며, 2026년 2월 렙티맙이 자가면역성 용혈성 빈혈 치료로 승인됨에 따라 일본 내에서 새로운 지지를 얻었습니다. 보체 억제제는 스팀리맙을 통해 냉응집증에서 명확한 역할을 수행하고 있지만, 냉응집증 환자 수가 적기 때문에 그 성장은 당연히 정체 상태에 접어들었습니다.

FcRn 억제제는 2031년까지 연평균 성장률(CAGR)이 10.42%로 가장 빠르게 성장하고 있는 약물군이며, 이러한 전망은 온형 자가면역성 용혈성 빈혈에 대한 니포칼리맙의 후기 임상시험 진전과 직접적인 관련이 있습니다. 또한, FcRn 억제는 다른 면역글로불린을 마찬가지로 광범위하게 억제하지 않으면서 병원성 IgG를 감소시키기 때문에 이 약물군에는 강력한 생물학적 근거가 있습니다. BTK 억제제는 또 다른 주요 경쟁 약물군이며, 릴자부르티닙은 원발성 온형 자가면역성 용혈성 빈혈 환자 21명을 대상으로 한 임상시험에서 64%의 전체 헤모글로빈 반응률을 보인 후, 획기적 치료제 지정을 받아 3상 임상시험 단계로 진입했습니다. 면역억제제, IVIG 및 이와 유사한 지지 요법은 계속 사용될 것이지만, 표적 치료제가 승인되어 보험 적용 대상이 된다면, 이러한 치료법들이 자가면역성 용혈성 빈혈 치료 시장의 장기적인 수익 구조를 주도할 가능성은 낮아질 것입니다.

지역별 분석

2025년, 북미는 자가면역성 용혈성 빈혈 치료 시장 점유율의 35.63%를 차지하며 다른 모든 지역을 앞질렀습니다. 미국은 희귀 혈액 질환 전문의가 가장 많이 집중되어 있고, 규제 당국의 심사 절차가 가장 활발하며, 환자 1인당 치료비가 가장 높기 때문에 계속해서 핵심적인 수익 기반이 되고 있습니다. 현재 미국에서 전환점이 되고 있는 것은 온형 자가면역성 용혈성 빈혈(AIHA)에 대한 니포칼리맙의 FDA 우선 심사입니다. 이에 따라 2026년 말 또는 2027년 초에는 이 아형에 대한 최초의 승인된 표적 치료제가 제공될 가능성이 있습니다. 또한, 이 지역에서는 전문 약국 네트워크가 이미 포스타마티닙 등 관련 혈액 질환 치료제를 지원하고 있으며, 엔제이모사가 표적 AIHA 치료에 대해 의료진의 인지도를 이미 확보하고 있기 때문에 상용화를 위한 준비도 더욱 잘 되어 있습니다. 캐나다와 멕시코에서는 희귀질환에 대한 보험 적용 범위가 점차 확대되고 있지만, 환자 1인당 자가면역성 용혈성 빈혈 치료 시장 규모는 여전히 매우 작은 수준에 머물러 있습니다.

유럽은 독일, 영국, 프랑스, 이탈리아, 스페인을 핵심으로 하여, 자가면역성 용혈성 빈혈 치료 시장에서 여전히 두 번째로 큰 주요 지역으로 자리 잡고 있습니다. 이 지역은 엔제이모사의 희귀질환 지정이 유지되고 있는 점과, 자가면역성 용혈성 빈혈에 대한 희귀질환 프로그램의 폭넓은 수용성에서 볼 수 있듯이, 지원적인 희귀질환 제도의 혜택을 받고 있습니다. 영국에서는 NICE가 AIHA 전용 제품을 아직 승인하지 않았기 때문에 여전히 심각한 접근 격차가 존재하며, 이것이 향후 의료 기술 평가 신청에 있어 주요 장애물로 작용하고 있습니다. 또한, HUTCHMED사가 스톡홀름에서 개최된 EHA 2026에서 소브레플레닙의 3상 임상시험 주요 데이터를 발표함에 따라, SYK 억제가 지역 내 논의에서 더욱 주목을 받게 되었으며, 유럽 임상의들 사이에서도 인지도가 높아지고 있습니다.

아시아태평양은 자가면역성 용혈성 빈혈 치료 시장에서 가장 빠르게 성장하고 있는 지역으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 9.06%를 나타낼 것으로 전망됩니다. 일본에서는 2026년 2월, 렙티시맙이 자가면역성 용혈성 빈혈의 치료제로 승인되면서 2차 치료에 대한 접근성이 강화되었습니다. 또한 같은 달, 사노피는 릴자부르티닙에 대해 일본에서 희귀질환 치료제로 지정받았습니다. 중국에서는 HUTCHMED사의 소브레프레닙에 대한 우선 심사 대상 NDA(신약 승인 신청)와 Juventas Biotechnology사의 CAR-T 치료법 임상시험 개시로 인해 그 중요성이 커지고 있습니다. 한편, 중동 및 아프리카 및 남미의 경우 시장 규모는 여전히 작지만, 희귀질환 대책을 위한 정책 지원과 전문 의료 센터에 대한 투자로 인해 시장이 서서히 개방되고 있습니다. 이러한 소규모 지역에서는 진단상의 제약으로 인해 치료 환자 수가 여전히 제한적이기 때문에 성장은 제품 출시와 마찬가지로 의료 시스템의 구축 현황에 크게 좌우될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the autoimmune hemolytic anemia treatment market size is projected to expand from USD 2.45 billion in 2025 and USD 2.63 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 8.03% between 2026 to 2031.

This report is Segmented by Type (Warm, Cold, Mixed, Secondary), Drug Class (Corticosteroids, IVIG, Mabs, Complement Inhibitors, Immunosuppressants, BTK Inhibitors, Fcrn Inhibitors), Route of Administration (Oral, and More), Distribution Channel (Hospital, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Autoimmune Hemolytic Anemia Treatment Market Trends and Insights

Increasing Need for Steroid-Sparing Therapies in Refractory AIHA

Corticosteroids still produce an initial hemoglobin response in many warm autoimmune hemolytic anemia patients, but relapse remains common after tapering, and that keeps the autoimmune hemolytic anemia treatment market tied to repeat treatment cycles. Long steroid exposure also raises the burden of diabetes, metabolic complications, and osteoporosis, which lowers quality of life and adds avoidable hospital use even when hemolysis is partly controlled. Rituximab has moved into the preferred second-line position for relapsed or refractory disease, while splenectomy has shifted later because published cohort evidence showed a 12% surgical complication rate. This pattern matters for the autoimmune hemolytic anemia treatment market because every relapse on a prior agent creates a clear switching event once a targeted option is available. The current treatment sequence outlined in the 2025 ASH Education Program also places newer B-cell, plasma-cell, SYK, and FcRn approaches behind rituximab, which supports continued demand across multiple lines of care.

Rising Pipeline Readiness for Complement and FcRn Targeting Therapies

The autoimmune hemolytic anemia treatment market is now moving closer to its first broad wave of labeled targeted therapies, and FcRn blockade is at the center of that shift. FcRn-targeted agents can reduce circulating IgG by as much as 85%, which directly addresses the autoantibodies that drive red blood cell destruction while preserving IgA, IgM, and innate immune function. Nipocalimab is the most advanced FcRn program in warm autoimmune hemolytic anemia and is under FDA Priority Review after showing durable hemoglobin response in the Phase 2/3 ENERGY study. Cold autoimmune hemolytic anemia already has one approved targeted option through sutimlimab, and registry data in more than 70% of treated patients have supported durable real-world effectiveness without new safety signals after a mean treatment duration of more than 2 years. As labeled warm and cold options come into view at the same time, the autoimmune hemolytic anemia treatment market is likely to see stronger physician confidence and better reimbursement support.

Long Diagnostic Delay Before Confirmed Hematology Referral

Diagnostic delay remains a direct limit on the autoimmune hemolytic anemia treatment market because untreated or misdiagnosed patients do not reach hematology prescribing channels. In low and middle-income countries, pediatric cases have been reported at hemoglobin levels of 3 g/dL to 6 g/dL by the time treatment begins, which reflects long delays between symptom onset and specialist care. Cold autoimmune hemolytic anemia is especially easy to miss because acrocyanosis and cold-triggered circulatory symptoms are often linked to other conditions before hematology referral occurs. Even in higher-income settings, DAT-negative disease can require advanced crossmatch and elution methods that are not widely available in community laboratories. Until referral access, awareness, and diagnostic capability improve more broadly, the autoimmune hemolytic anemia treatment market will continue to face a ceiling on addressable volume.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Orphan-Drug Incentives for Rare Hematology Programs

- Growing Use of Precision Diagnostics to Subtype Warm, Cold, and Mixed AIHA

- Small Treatable Patient Pool in Cold Agglutinin Disease and Secondary AIHA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Warm autoimmune hemolytic anemia held 68.13% of the autoimmune hemolytic anemia treatment market share in 2025, which matched its position as the most common subtype globally. The autoimmune hemolytic anemia treatment market, therefore, remains centered on warm disease, even though formal targeted approval for this setting is still pending in the United States. That gap means much of the current value in warm disease still comes through corticosteroids and rituximab used off label rather than through premium branded treatment lines. The subtype remains the main target for late-stage programs because it offers the broadest commercial base and the clearest near-term path to label expansion.

Cold autoimmune hemolytic anemia is projected to grow at an 8.78% CAGR through 2031, supported by sutimlimab's existing presence and improving real-world evidence. Mixed autoimmune hemolytic anemia remains a smaller revenue pool because it represents only 5% to 8% of cases and often overlaps with complex autoimmune backgrounds such as SLE, where 25% to 42% of mixed cases are associated. Secondary autoimmune hemolytic anemia also remains commercially limited because pivotal studies often exclude these patients, which weakens reimbursement support even when physicians still treat them. Over the longer term, refractory disease may open another layer of value as Juventas Biotechnology's CAR-T program moved into clinical testing after NMPA IND approval in April 2025.

Corticosteroids accounted for 57.38% of the autoimmune hemolytic anemia treatment market size in 2025, which reflects entrenched first-line use and low generic acquisition cost rather than durable disease control. That legacy position continues because most patients still begin treatment with steroids even when relapse risk is well understood. Monoclonal antibodies, especially rituximab and biosimilar-linked use, remain important in second-line care and gained fresh support in Japan after the February 2026 approval of rituximab for autoimmune hemolytic anemia. Complement inhibitors hold a defined role in cold disease through sutimlimab, but their growth is naturally capped by the smaller cold agglutinin disease population.

FcRn inhibitors are the fastest-growing class with a 10.42% CAGR through 2031, and this outlook is tied directly to nipocalimab's late-stage progress in warm autoimmune hemolytic anemia. The class also benefits from a strong biological rationale because FcRn blockade lowers pathogenic IgG without broadly suppressing other immunoglobulins in the same way. BTK inhibitors are the other key challenger class, and rilzabrutinib posted a 64% overall hemoglobin response rate in 21 primary warm autoimmune hemolytic anemia patients before moving into Phase 3 with Breakthrough Therapy designation. Immunosuppressants, IVIG, and similar supportive options will remain in use, but they are less likely to drive the long-term revenue mix of the autoimmune hemolytic anemia industry once targeted classes become labeled and reimbursed.

Complete Report Scope:

- By Type

- Warm Autoimmune Hemolytic Anemia

- Cold Autoimmune Hemolytic Anemia

- Mixed Autoimmune Hemolytic Anemia

- Secondary Autoimmune Hemolytic Anemia

- Other Type Autoimmune Hemolytic Anemia

- By Drug Class

- Corticosteroids

- Intravenous Immunoglobulin

- Monoclonal Antibodies

- Complement Inhibitors

- Immunosuppressive Agents

- BTK Inhibitors

- FcRn Inhibitors

- Other Drug Classes

- By Route of Administration

- Oral

- Intravenous

- Subcutaneous

- Other Routes of Administration

- By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 35.63% of the autoimmune hemolytic anemia treatment market share in 2025, which kept it ahead of every other region. The United States remains the core revenue base because it has the deepest concentration of rare blood disorder specialists, the most active regulatory pipeline, and the highest treatment spending per patient. The current U.S. inflection point is the FDA Priority Review for nipocalimab in warm autoimmune hemolytic anemia, which could deliver the first approved targeted therapy for this subtype in late 2026 or early 2027. Commercial readiness is also stronger in this region because specialty pharmacy networks already support adjacent hematology drugs such as fostamatinib, and because Enjaymo has already established physician familiarity with targeted AIHA treatment. Canada and Mexico are expanding rare disease reimbursement, but the autoimmune hemolytic anemia treatment market remains much smaller there on a per-patient basis.

Europe remains the second major region for the autoimmune hemolytic anemia treatment market, anchored by Germany, the United Kingdom, France, Italy, and Spain. The region benefits from a supportive orphan framework, as seen in Enjaymo's maintained orphan status and the broader openness to orphan programs in autoimmune hemolytic anemia. The United Kingdom still has a key access gap because NICE has not approved an AIHA-specific product, which makes future health technology submissions a major gating step. European clinician awareness is also rising as HUTCHMED presented pivotal sovleplenib Phase 3 data at EHA 2026 in Stockholm, which brought SYK inhibition further into the regional discussion.

Asia-Pacific is the fastest-growing geography in the autoimmune hemolytic anemia treatment market, with a 9.06% CAGR projected for 2026-2031. Japan strengthened second-line access in February 2026 when rituximab was approved for autoimmune hemolytic anemia, and Sanofi also received orphan designation there for rilzabrutinib in the same month. China is gaining importance through HUTCHMED's priority-reviewed sovleplenib NDA and Juventas Biotechnology's CAR-T clinical entry, while the Middle East, Africa, and South America remain smaller but are gradually opening through rare disease policy support and specialist center investment. Diagnostic limits still suppress treated volume in those smaller regions, so growth will depend as much on health system readiness as on product launches.

- Abbvie

- Alexion AstraZeneca

- Alpine Immune Sciences, Inc.

- Amgen

- Apellis Pharmaceuticals, Inc.

- argenx SE

- Bristol-Myers Squibb

- Roche

- Genentech

- GlaxoSmithKline

- Incyte

- Johnson & Johnson

- Novartis

- Omeros Corporation

- Rigel Pharmaceuticals, Inc.

- Sanofi

- Teva Pharmaceutical Industries

- TG Therapeutics

- UCB

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need for Steroid-Sparing Therapies in Refractory AIHA

- 4.2.2 Rising Pipeline Readiness for Complement and FcRn Targeting Therapies

- 4.2.3 Expanding Orphan-Drug Incentives for Rare Hematology Programs

- 4.2.4 Growing Use of Precision Diagnostics to Subtype Warm, Cold, and Mixed AIHA

- 4.2.5 Higher Treatment Switching After Steroid Toxicity and Relapse

- 4.2.6 Increasing Specialist Referral Networks for Rare Blood Disorders

- 4.3 Market Restraints

- 4.3.1 Long Diagnostic Delay Before Confirmed Hematology Referral

- 4.3.2 Small Treatable Patient Pool in Cold Agglutinin Disease and Secondary AIHA

- 4.3.3 Weak Standardization of Clinical Endpoints in Warm AIHA Trials

- 4.3.4 High Dependence on Steroids, Transfusion, and Splenectomy in Routine Care

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Warm Autoimmune Hemolytic Anemia

- 5.1.2 Cold Autoimmune Hemolytic Anemia

- 5.1.3 Mixed Autoimmune Hemolytic Anemia

- 5.1.4 Secondary Autoimmune Hemolytic Anemia

- 5.1.5 Other Type Autoimmune Hemolytic Anemia

- 5.2 By Drug Class

- 5.2.1 Corticosteroids

- 5.2.2 Intravenous Immunoglobulin

- 5.2.3 Monoclonal Antibodies

- 5.2.4 Complement Inhibitors

- 5.2.5 Immunosuppressive Agents

- 5.2.6 BTK Inhibitors

- 5.2.7 FcRn Inhibitors

- 5.2.8 Other Drug Classes

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

- 5.3.3 Subcutaneous

- 5.3.4 Other Routes of Administration

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacy

- 5.4.2 Retail Pharmacy

- 5.4.3 Online Pharmacy

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Alexion AstraZeneca

- 6.3.3 Alpine Immune Sciences, Inc.

- 6.3.4 Amgen Inc.

- 6.3.5 Apellis Pharmaceuticals, Inc.

- 6.3.6 argenx SE

- 6.3.7 Bristol-Myers Squibb Company

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Genentech, Inc.

- 6.3.10 GSK plc

- 6.3.11 Incyte Corporation

- 6.3.12 Johnson and Johnson Services, Inc.

- 6.3.13 Novartis AG

- 6.3.14 Omeros Corporation

- 6.3.15 Rigel Pharmaceuticals, Inc.

- 6.3.16 Sanofi

- 6.3.17 Teva Pharmaceutical Industries Ltd.

- 6.3.18 TG Therapeutics, Inc.

- 6.3.19 UCB S.A.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment