|

시장보고서

상품코드

2073154

재택 화학요법 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chemotherapy At Home Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

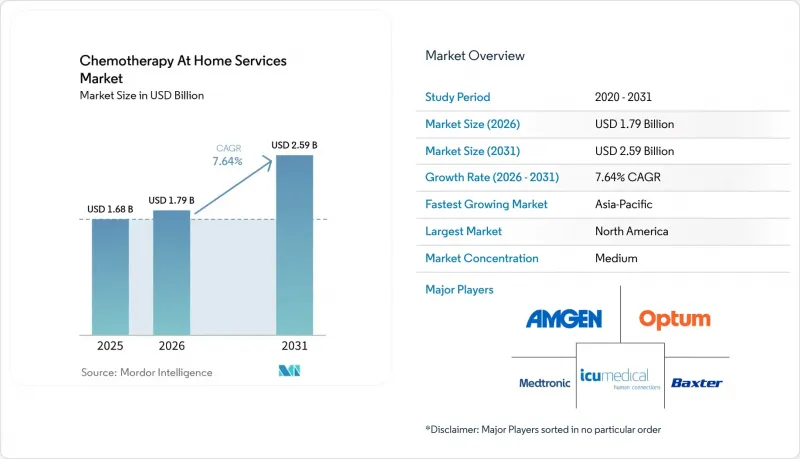

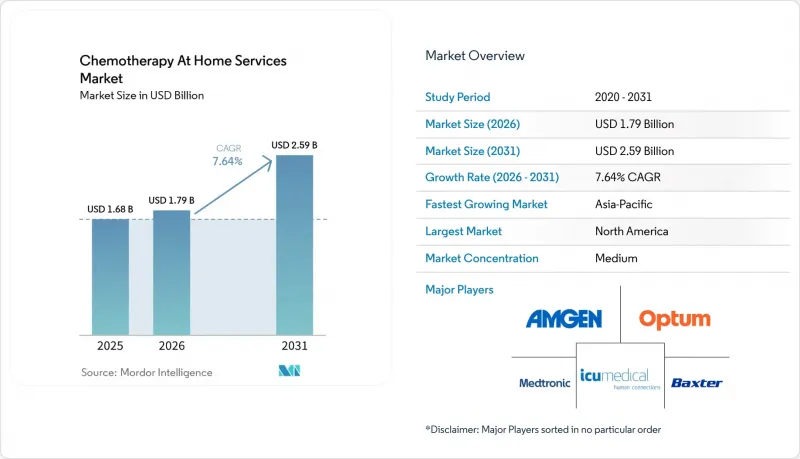

Mordor Intelligence에 의하면, 재택 화학요법 서비스 시장 규모는 2025년 16억 8,000만 달러에서 2026년에는 17억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.64%로 성장을 지속하여, 2031년에는 25억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(항암제, 항암제 주입 펌프), 투여 경로별(경구, 정맥 내), 암 유형별(유방암, 혈액암, 난소암, 대장암, 기타 암 유형), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 재택 화학요법 서비스 시장 동향 및 인사이트

암 발병률 및 치료 건수 증가

세계 암 환자 수는 여전히 높은 수준을 유지하고 있으며, 더욱이 증가 추세를 보이고 있어 재택 화학요법 서비스 시장의 환자 기반이 확대되고 있습니다. 세계보건기구(WHO)의 보고에 따르면, 2022년에는 2,000만 명의 신규 암 환자와 970만 명의 사망자가 확인되었으며, 2050년까지 연간 신규 환자 수는 3,500만 명을 넘어설 것으로 예측됩니다. 많은 의료 시스템에서 병원의 수액 투여 능력이 환자 수 증가를 따라가지 못하고 있기 때문에 이러한 증가는 재택 간호에 있어 중요한 의미를 지닙니다. 이러한 압박은 생존자 수가 늘어남에 따라 더욱 심해지고 있습니다. 2022년 기준으로, 암 진단 후 5년 이내에 생존해 있는 사람은 5,350만 명에 달할 전망입니다. 이러한 환자들 중 상당수는 보조 요법, 유지 요법 또는 반복 주기 치료 계획을 받고 있으며, 이러한 치료는 정기적인 재택 서비스 모델에 적합합니다. 이로 인해 재택 화학요법 서비스 시장에는 단일 연도의 신규 진단 건수에만 의존하지 않는 안정적인 수요 기반이 형성되고 있습니다.

시설 중심의 치료에서 재택 암 치료로의 전환

의료 제공업체, 환자, 보험사가 병원 밖에서의 치료에 점점 더 익숙해짐에 따라, 재택 화학요법 서비스 시장은 확대되고 있습니다. 메이요 클리닉의 “Cancer CARE Beyond Walls”이 프로그램에서는 93건의 재택 정맥 내 화학요법 주사 투여 과정에서 주사 반응이나 카테터 관련 감염이 단 한 건도 보고되지 않았으며, 이는 치료의 질과 제공의 안전성에 대한 신뢰를 뒷받침하는 것입니다. 경제적인 이점도 뚜렷합니다. 유나이티드 헬스 그룹의 추산에 따르면, 암 치료제 투여를 병원 외래에서 자택 또는 진료소로 전환함으로써 민간 보험 가입 환자 1인당 32%-39%의 비용 절감이 가능해집니다. 이 분석에 따르면, 병원에서 정맥 주사 투여 비율이 60%에서 30%로 감소할 경우 연간 120억 달러의 비용 절감이 예상된다고 추산됩니다. 이러한 비용 절감 효과로 인해, 보험사들은 이전보다 더 적극적으로 저비용 의료 제공 환경을 지지하게 되었습니다. 그 결과, 재택 화학요법 서비스 시장은 환자의 편의성뿐만 아니라 의도적인 의료 제공 장소의 전환에 의해서도 형성되고 있습니다.

암 전문 간호사 및 약사의 인력 부족

재택 화학요법 서비스 시장은 암 전문 교육을 받은 간호사나 약사의 채용 및 유지가 여전히 어려워 근본적인 공급 문제에 직면해 있습니다. 『랜싯 종양학 위원회』는 전 세계 암 의료 종사자들의 심각한 인력 부족을 주요 원인으로 지목하고, 치료의 질을 각국 및 의료 현장의 인력 배치 수준과 직접적으로 연관지었습니다. 재택 투여는 화학요법의 독성 평가나 신속한 대응에 있어 일반적인 재택치료 역량만으로는 반드시 충분하지 않기 때문에 더 큰 어려움을 초래합니다. 의료진은 치료로 인한 부작용과 질환의 진행을 구분하여, 방문 진료나 원격 진료 시 적절한 치료 강화 여부를 판단해야 합니다. 따라서 중증도가 낮은 서비스에서 제공되는 일반적인 정맥 주사 지원보다 훨씬 더 심도 있는 교육이 필요합니다. 이러한 인재 기반이 충실해질 때까지는 재택 화학요법 서비스 시장이 본래라면 환자 수요가 허용할 법한 속도보다 더 느린 속도로 계속 확대될 것입니다.

부문별 분석

2025년, 재택 화학요법 서비스 시장의 매출액 중 61.31%를 화학요법제가 차지했으며, 이에 따라 매출 구성은 기기나 물류 비용이 아닌 약제비를 중심으로 이루어진 상태를 유지했습니다. 이러한 상황은 대부분의 환자의 치료 과정이 여전히 치료 자체를 중심으로 구성되어 있으며, 의료기기나 재택 지원이 그 주변에 부수적으로 제공되고 있음을 반영하고 있습니다. 대장암 치료를 위한 플루오로우라실을 주성분으로 하는 치료 등, 수 일에 걸쳐 진행되는 정맥 내 투여 요법은 단일 치료 주기 내에서 약물과 투여 장치가 함께 사용되기 때문에 이러한 구조를 더욱 공고히 하고 있습니다. 펌프 부문은 여전히 가장 빠르게 성장하는 제품 카테고리이며, 2031년까지 연평균 성장률(CAGR)은 8.36%로 전망됩니다. 이러한 성장은 약제의 중요성이 낮아진 데 따른 것이 아니라, 이용 사례가 확대된 데 따른 것입니다. 재택 화학요법 서비스 업계에서는 여전히 약제가 주요 수익원이고 있지만, 이러한 치료의 더 큰 비중을 진료소 밖에서 수행할 수 있도록 하는 데 있어 의료기기의 중요성이 커지고 있습니다.

펌프 도입이 확대되고 있는 배경에는 제품 형태의 다양화가 있으며, 의료 서비스 제공업체는 저비용 엘라스토머 시스템과 보다 정교한 연결성을 갖춘 스마트 플랫폼 중 하나를 선택할 수 있게 되었습니다. 프레제니우스사는 자사의 스마트 수액 플랫폼 "Ivenix"를 2026년의 주요 성장 동력으로 꼽으며, 투자자 설명 자료에서 뛰어난 연결성과 97%의 약물 라이브러리 적합률을 강조했습니다. KORU Medical사도 2026년 1월에 "FreedomEDGE" 수액 시스템에 대한 510(k) 신고를 제출하고, HER2 양성 유방암 환자가 자택에서 펠츠주맙, 트라스투주맙, 히알루로니다제를 피하 투여할 수 있도록 재택 치료의 대상 범위를 확대하려는 움직임을 보였습니다. 메디케어의 급여 대상 범위도 확대되었습니다. 2026년 1월 25일에 발효된 CMS의 LCD 개정안에 따라, 플루오로우라실, 시타라빈, 빈크리스틴을 포함한 지속 투여형 항암제에 사용되는 재택용 주입 펌프에 대한 보험 급여가 확정되었기 때문입니다. 이러한 변화로 인해, 총매출에서 항암제가 차지하는 핵심적인 역할은 변함없이 유지되면서, 재택 항암 치료 서비스 시장은 펌프 도입 대수의 확대 방향으로 나아가고 있습니다.

지역별 분석

2025년, 재택 화학요법 서비스 시장 매출의 45.64%를 북미가 차지하고 있으며, 이러한 우위는 대규모 사업자와 보험사의 지원, 그리고 가치 기반 암 의료 정책이 결합된 결과입니다. Option Care Health사는 190곳 이상의 거점과 5,000명 이상의 임상의, 그리고 미국 전역 50개 주에서 서비스를 제공하고 있다고 밝혔으며, 이는 해당 지역에서 이용 가능한 네트워크가 매우 잘 구축되어 있음을 보여줍니다. 또한, CMS(미국 의료보험서비스센터)는 “암 치료 강화 모델(Enhancing Oncology Model)”을 통해 사업 환경을 강화했습니다. 이에 따라 월별 암 의료 강화 서비스(Enhanced Oncology Services)에 대한 지급액이 증액되어, 환자 중심의 암 의료 업무 흐름이 더욱 뒷받침되게 되었습니다. 북미의 재택 화학요법 서비스 시장 점유율은 승인 절차, 조제, 배송, 규정 준수를 대규모로 관리하는 강력한 운영 역량에 의해서도 뒷받침되고 있습니다.

유럽은 재택 화학요법 서비스 시장에서 여전히 2위 지역 클러스터이지만, 그 성장세는 북미만큼 균일하지는 않습니다. 병원의 종양학 팀, 재택 간병 서비스 제공업체, 공적 보험 제도가 이미 연계된 운영 체계를 통해 협력하고 있는 지역에서 진전이 가장 두드러집니다. 한편, 벨기에에서 진행된 동료 심사 연구에 따르면, 환급 제도가 실제 운영 실태를 반영하도록 설계되지 않은 경우, 재택 암 치료 비용이 일반적인 병원 치료보다 더 비싸질 수 있는 것으로 나타났습니다. 이러한 격차가 확대를 늦추고 있습니다. 왜냐하면, 임상적 실현 가능성만으로는 제공업체의 투자나 프로그램의 일상적인 규모 확대를 보장할 수 없기 때문입니다.

아시아태평양은 재택 화학요법 서비스 시장에서 2031년까지 연평균 성장률(CAGR) 9.59%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 이 지역은 암 환자 수가 많고, 도시 지역과 비도시 지역 간에 병원의 수용 능력에 차이가 있어, 아직 개척되지 않은 시장 기회가 막대합니다. 성장이 가장 두드러지는 곳은 디지털을 통한 연계, 도시 지역의 간호사 확보, 그리고 보험사 측의 수용성이 동시에 개선되고 있는 지역입니다. 한국과 호주에서는 이미 재택 정맥주사 요법 제공업체 네트워크가 구축되어 있지만, 기타 국가들에서는 체계적인 재택 암 치료 개발이 초기 단계에 있습니다. 남미, 중동 및 아프리카는 매출 규모 면에서는 여전히 작지만, 의료 시스템이 주요 병원 이외의 장소에서 치료를 제공하기 위한 보다 유연한 방안을 모색함에 따라, 재택 화학요법 서비스 시장은 이들 지역에서도 그 중요성이 커지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the chemotherapy at home services market size is expected to grow from USD 1.68 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.59 billion by 2031 at 7.64% CAGR over 2026-2031.

This report is Segmented by Product (Chemotherapy Drugs, Chemotherapy Infusion Pumps), Route of Administration (Oral, Intravenous), Cancer Type (Breast Cancer, Blood Cancer, Ovarian Cancer, Colorectal Cancer, Other Cancer Types), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Chemotherapy At Home Services Market Trends and Insights

Rising Cancer Incidence and Treatment Volumes

The chemotherapy at home services market is gaining a larger patient base because global cancer volumes remain high and are still increasing. The World Health Organization reported 20 million new cancer cases and 9.7 million deaths in 2022, and it expects annual new cases to rise above 35 million by 2050. This rise matters for home-based care because hospital infusion capacity does not expand as quickly as case volumes in many health systems. The same pressure is being amplified by the large survivorship pool, with 53.5 million people alive within 5 years of a cancer diagnosis as of 2022. Many of these patients remain on adjuvant, maintenance, or repeat-cycle treatment plans that fit recurring home service models. That gives the chemotherapy at home services market a steady demand base that is not tied only to new diagnoses in a single year.

Preference Shift From Facility-Based Care to Home-Based Oncology Delivery

The chemotherapy at home services market is moving forward as providers, patients, and payers become more comfortable with treatment outside the hospital. Mayo Clinic's Cancer CARE Beyond Walls program reported 93 home intravenous chemotherapy infusions with no infusion reactions and no catheter-related infections, which supports confidence in care quality and delivery safety. The economic case is also strong, as UnitedHealth Group estimated that shifting cancer drug administration from hospital outpatient settings to home or physician office settings can reduce costs by 32%-39% per commercially insured patient. The same analysis estimated USD 12 billion in annual savings if the hospital infusion share drops from 60% to 30%. Those savings are encouraging payers to favor lower-cost settings more actively than before. As a result, the chemotherapy at home services market is being shaped not only by patient convenience, but also by deliberate site-of-care redirection.

Oncology Nurse and Pharmacist Capacity Gaps

The chemotherapy at home services market faces a basic supply problem because oncology-trained nurses and pharmacists remain hard to recruit and retain. The Lancet Oncology Commission identified the global cancer workforce as a critical resource gap and linked care quality directly to staffing levels across countries and care settings. Home administration adds another layer of difficulty because general home health capabilities are not always enough for chemotherapy toxicity assessment and rapid response. Staff must distinguish treatment side effects from disease progression and make correct escalation decisions during visits or remote review. That raises training needs well above standard infusion support in lower-acuity services. Until that workforce base deepens, the chemotherapy at home services market will continue to expand more slowly than patient demand would otherwise allow.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote Monitoring and Tele-Oncology Support Models

- Home Infusion Logistics and Nurse Dispatch Networks Improving Treatment Feasibility

- Reimbursement Variability and Payer Authorization Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemotherapy drugs held 61.31% of revenue in 2025 in the chemotherapy at home services market, which kept the revenue profile centered on drug spending rather than equipment or logistics fees. That position reflects how most patient episodes are still built around the therapy itself, with devices and home support layered around it. Multi-day intravenous regimens such as fluorouracil-based treatment for colorectal cancer reinforce this structure because the drug and the delivery setup are used together in a single care cycle. The pump segment is still the fastest-growing product category, with an 8.36% CAGR projected through 2031. That growth is coming from broader use cases rather than from a decline in drug importance. The chemotherapy at home services industry still depends on drugs as the primary billing driver, but devices are becoming more important for enabling a larger share of those therapies to move out of clinics.

Pump adoption is rising because product formats are widening, and providers can choose between lower-cost elastomeric systems and more connected smart platforms. Fresenius described its Ivenix smart infusion platform as a meaningful growth driver for 2026, and it highlighted advanced connectivity and a 97% drug library compliance rate in its investor communication. KORU Medical also moved to widen home eligibility when it submitted a 510(k) notification in January 2026 for the FreedomEDGE infusion system to administer pertuzumab, trastuzumab, and hyaluronidase subcutaneously at home for HER2-positive breast cancer. Medicare coverage support also improved, as the CMS LCD revision effective January 25, 2026 confirmed home coverage for ambulatory infusion pumps used with continuous antineoplastic drugs including fluorouracil, cytarabine, and vincristine. These changes are pushing the chemotherapy at home services market toward a larger installed pump base without changing the central role of chemotherapy drugs in total revenue.

Complete Report Scope:

- By Product

- Chemotherapy Drugs

- Chemotherapy Infusion Pumps

- By Route of Administration

- Oral

- Intravenous

- By Cancer Type

- Breast Cancer

- Blood Cancer

- Ovarian Cancer

- Colorectal Cancer

- Other Cancer Types

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 45.64% of revenue in 2025 in the chemotherapy at home services market, and that lead rests on a combination of scale operators, payer support, and value-based oncology policy. Option Care Health reported more than 190 locations, more than 5,000 clinicians, and service across all 50 U.S. states, which illustrates the network depth available in the region. CMS also strengthened the operating backdrop through the Enhancing Oncology Model, which increased Monthly Enhanced Oncology Services payments and supported more patient-centered oncology workflows. The chemotherapy at home services market share in North America is also supported by stronger administrative ability to manage authorization, compounding, dispatch, and compliance at scale.

Europe remains the second-largest regional cluster in the chemotherapy at home services market, but growth is less uniform than in North America. Progress is strongest where hospital oncology teams, homecare providers, and public payment systems already work through linked operating pathways. At the same time, a peer-reviewed Belgian study showed that oncology treatment at home can cost more than standard hospital care when reimbursement is not designed to cover operating reality. That gap slows expansion because clinical feasibility alone does not guarantee provider investment or routine program scale.

Asia-Pacific is forecast to grow at a 9.59% CAGR through 2031 in the chemotherapy at home services market, making it the fastest-growing regional block. The region has a large untreated opportunity because cancer volumes are high and hospital capacity remains uneven across urban and non-urban settings. Growth is strongest where digital coordination, urban nurse availability, and payer openness are improving at the same time. South Korea and Australia already have established home infusion provider networks, while other countries are moving through earlier stages of structured oncology-at-home development. South America and the Middle East and Africa remain smaller in revenue terms, but the chemotherapy at home services market is gaining relevance there as health systems search for more flexible ways to deliver treatment outside major hospitals.

- Accredo Health Group, Inc.

- Advocate Health Care

- Amedisys

- Amerita, Inc.

- Amgen

- B. Braun

- Baxter

- Beckton Dickinson

- BioScrip, Inc.

- CareCentrix

- CVS Health

- Fresenius

- HealthCare atHOME

- ICU Medical

- InfiUSystem Holdings Inc.

- Jivika Healthcare

- Lincare Holdings

- LloydsPharmacy Clinical Homecare

- Medibank

- Medtronic

- Optum

- Option Care Health, Inc.

- Penn Medicine

- Portea Medical Private Limited

- Sciensus Pharma Services Limited

- TCP Homecare

- Ubiqare Health Pvt. Ltd.

- View Health Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cancer Incidence and Treatment Volumes

- 4.2.2 Preference Shift From Facility-Based Care to Home-Based Oncology Delivery

- 4.2.3 Expansion of Remote Monitoring and Tele-Oncology Support Models

- 4.2.4 Home Infusion Logistics and Nurse Dispatch Networks Improving Treatment Feasibility

- 4.2.5 Portable Infusion Devices and Drug Stability Protocols Broadening Home Eligibility

- 4.2.6 Value-Based Care Incentives Supporting Site-of-Care Shift

- 4.3 Market Restraints

- 4.3.1 Oncology Nurse and Pharmacist Capacity Gaps

- 4.3.2 Reimbursement Variability and Payer Authorization Friction

- 4.3.3 Hazardous Drug Handling, Cold Chain, and Home Safety Compliance Burden

- 4.3.4 Limited Suitability of High-Risk Regimens for Home Administration

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Chemotherapy Drugs

- 5.1.2 Chemotherapy Infusion Pumps

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Intravenous

- 5.3 By Cancer Type

- 5.3.1 Breast Cancer

- 5.3.2 Blood Cancer

- 5.3.3 Ovarian Cancer

- 5.3.4 Colorectal Cancer

- 5.3.5 Other Cancer Types

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accredo Health Group, Inc.

- 6.3.2 Advocate Health Care

- 6.3.3 Amedisys, Inc.

- 6.3.4 Amerita, Inc.

- 6.3.5 Amgen Inc.

- 6.3.6 B. Braun SE

- 6.3.7 Baxter International Inc.

- 6.3.8 Becton, Dickinson and Company

- 6.3.9 BioScrip, Inc.

- 6.3.10 CareCentrix, Inc.

- 6.3.11 CVS Health Corporation

- 6.3.12 Fresenius Kabi AG

- 6.3.13 HealthCare atHOME

- 6.3.14 ICU Medical, Inc.

- 6.3.15 InfiuSystem Holdings Inc.

- 6.3.16 Jivika Healthcare

- 6.3.17 Lincare Holdings Inc.

- 6.3.18 LloydsPharmacy Clinical Homecare

- 6.3.19 Medibank Private Limited

- 6.3.20 Medtronic plc

- 6.3.21 Optum, Inc.

- 6.3.22 Option Care Health, Inc.

- 6.3.23 Penn Medicine

- 6.3.24 Portea Medical Private Limited

- 6.3.25 Sciensus Pharma Services Limited

- 6.3.26 TCP Homecare

- 6.3.27 Ubiqare Health Pvt. Ltd.

- 6.3.28 View Health Pty Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment