|

시장보고서

상품코드

2073155

임상시험 기술 및 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Clinical Trial Technology and Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

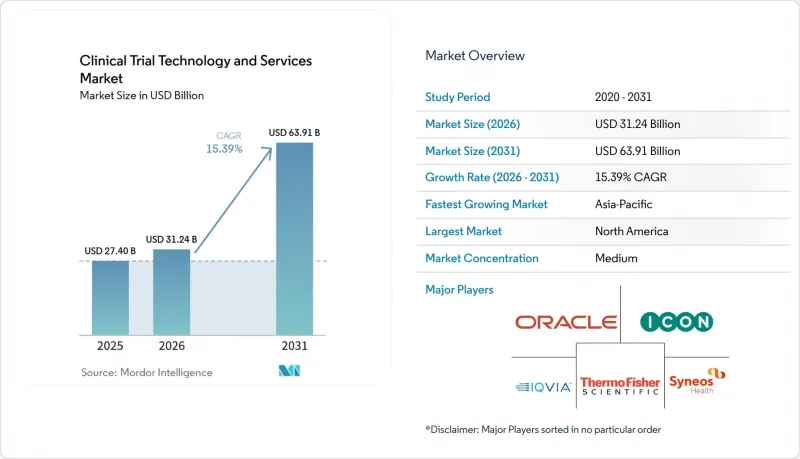

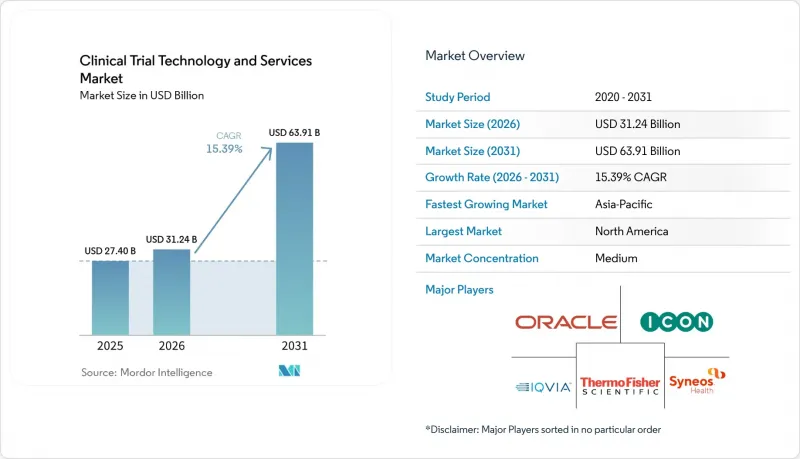

Mordor Intelligence에 의하면, 임상시험 기술 및 서비스 시장 규모는 2025년 274억 달러로 평가되었습니다. 2026년에는 312억 4,000만 달러로 확대되어 2031년까지 639억 1,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 15.39%로 성장할 전망입니다.

본 보고서는 제공 서비스(기술 솔루션, 서비스), 배포 모델(클라우드 기반, On-Premise형, 하이브리드형), 임상시험 단계(1상-4상), 최종 사용자(제약·바이오기술, 의료기기, CRO, 의료 제공업체), 그리고 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임상시험 기술 및 서비스 시장 동향 및 인사이트

임상시험의 복잡화와 프로토콜 부담 증가

프로토콜의 복잡화는 임상시험 실시 비용을 증가시키고 체계적인 디지털 감시의 필요성을 높이기 때문에 임상시험 기술 및 서비스 시장에서 직접적인 지출 요인으로 작용하고 있습니다. 2025년에는 제1상부터 제4상 임상시험의 76%에서 적어도 한 번의 프로토콜 수정이 필요하게 되었으며, 이는 2015년의 57%에서 증가한 수치입니다. 또한, 프로토콜 1건당 평균 수정 횟수는 라이프사이클 전체에 걸쳐 3.3회에 달했습니다. 종양학 분야는 여전히 가장 두드러진 문제 영역으로, 프로토콜의 90%에서 적어도 한 건의 대폭적인 수정이 필요했으며, 그중 45%는 피할 수 있는 수정 사항이었습니다. 2025년 학술지 분석에 따르면, 3상 임상시험 프로토콜 1건당 총 데이터 양이 2020년 이후 연간 10.8%의 속도로 증가하고 있는 것으로 나타났으며, 이는 임상시험 기술 및 서비스 시장에서 후원사들이 더욱 강력한 데이터 수집, 워크플로우 및 분석 도구에 의존하게 된 이유를 설명해 줍니다. 또한, 2024년에는 조사 대상 시설의 38%가 시험의 복잡성을 가장 큰 운영상의 과제로 꼽았으며, 이로 인해 시설에 가해지는 부담도 커지고 있습니다. 이는 임상시험 기술 및 서비스 시장에서 중복 작업과 수작업을 줄여주는 통합 워크플로우에 대한 수요가 증가하고 있음을 뒷받침합니다. 게다가 시험이 복잡해질수록 시험 과정 전반에 걸쳐 기록 건수, 수정 횟수, 감사 대상 항목이 증가하기 때문에 이러한 부담은 데이터 일관성 및 감사에 대한 기대치를 더욱 높이는 결과로 이어지고 있습니다.

분산형 및 하이브리드형 시험 운영의 급속한 확산

임상시험 기술 및 서비스 시장은 분산형 및 하이브리드형 임상시험의 도입으로 인해 혜택을 보고 있습니다. 이는 규제 당국이 이러한 접근 방식을 제한적인 실험이 아닌, 일반적인 시험 계획의 일부로 취급하게 되었기 때문입니다. 분산형 요소를 포함하는 임상시험에 관한 FDA의 최종 지침은 원격 의료를 통한 진료, 환자에 대한 직접적인 제품 배송, 디지털 헬스 기술의 활용 및 원격 감독에 대해 후원사에게 보다 명확한 운영상 기대 사항을 제시하고 있습니다. Trials&Home RADIAL의 개념 증명과 관련된 2025년 동료 심사 논문에 따르면, 온보딩, 검증 및 운영 후 거버넌스를 지원하는 기술 패키지를 활용하면 기존, 하이브리드형 및 완전 분산형 각 설계를 여러 국가에 걸쳐 시행할 수 있음이 밝혀졌습니다. 이것이 바로 임상시험 기술 및 서비스 시장이 단일한 최종 형태로 수렴되지 않는 이유입니다. 왜냐하면 하이브리드 방식은 동일한 프로토콜 내에서 대면 시설 방문과 원격 데이터 수집이 여전히 모두 필요한 임상시험에서 확고히 자리 잡은 모델이기 때문입니다. 이러한 변화에 따라 데이터 추적성의 중요성도 커지고 있습니다. 벤더는 관리 체제를 약화시키지 않으면서 시설 데이터와 원격 데이터를 모두 통합하여 관리할 수 있음을 입증해야 하기 때문입니다. 또한, 임상 팀이 개별 포인트 시스템 대신 연계된 플랫폼을 사용함으로써 하이브리드 운영이 더욱 원활해지기 때문에 시설의 부담을 줄여주는 도구에 대한 수요도 높아지고 있습니다.

EDC, CTMS, eTMF 및 재무 시스템 간의 통합이 지닌 복잡성

통합의 어려움은 여전히 임상시험 기술 및 서비스 시장에서 큰 걸림돌이 되고 있습니다. 이는 주요 스폰서들이 여전히 통합하기 어려운 대규모 레거시 환경을 운영하고 있기 때문입니다. Veeva는 2025년에 바이오의약품 업계 상위 20위권 고객사가 통합형 클라우드 CTMS로 전환함에 따라 100건 이상의 레거시 통합 문제를 해결했다고 보고했습니다. 이번 전환에는 900만 건 이상의 레코드 이전과 4,500명 이상의 사용자에 대한 교육이 필요했습니다. GSK와 관련된 또 다른 Veeva 고객 사례에서는 3년에 걸친 CTMS 현대화 프로그램에 대해 설명하고 있으며, 시스템 가동 전에 진행 중인 1,500건의 임상시험에서 600만 건 이상의 레코드를 마이그레이션하고, 4,500명의 사용자를 시스템에 등록했습니다. 이러한 사례들은 임상시험 기술 및 서비스 시장이 소프트웨어 수요에만 국한되지 않는 이유를 보여줍니다. EDC, CTMS, eTMF, 재무 및 레거시 시스템을 연동하는 데 드는 비용이 라이선스 비용보다 벤더 선정의 결정적 요인이 되는 경우가 많기 때문입니다. 구매자가 대규모 팀이나 규제 대상 워크플로우 전반에 걸친 검증, 교육 및 변경 관리까지 필요로 하는 경우, 이러한 부담은 더욱 커집니다. 또한, 많은 기업이 일괄적인 전환이 아닌 단계적인 현대화를 필요로 하기 때문에 서비스 공급업체나 하이브리드 도입 모델이 유리해집니다.

부문별 분석

2025년, 임상시험 기술 및 서비스 시장에서 기술 솔루션은 63.72%의 점유율을 차지했습니다. 이는 EDC, CTMS, eTMF, 환자 참여 및 전체 분석 환경에서 여전히 핵심 플랫폼에 대한 수요가 지출을 주도하고 있음을 보여줍니다. 모든 유형의 후원사가 여러 지역과 임상시험 단계에 걸쳐 안전한 데이터 수집, 워크플로우 관리 및 임상시험 감독을 필요로 하기 때문에 임상시험 기술 및 서비스 시장은 계속해서 이러한 시스템에 의존하고 있습니다. 기술 솔루션 분야에서는 스폰서들이 플랫폼을 전면적으로 교체하기보다는 기존 시스템 전체에서 작동하는 지능형 계층을 원하고 있기 때문에 AI 통합 도구가 급속히 확산되고 있습니다. 이 부문에서는 임상시험 관리와 데이터 수집이 여전히 핵심적인 위치를 차지하고 있으며, 후기 단계 임상시험에서 프로토콜 데이터의 양이 계속 증가함에 따라 이러한 도구에 대한 부담이 커지고 있습니다. 이와 유사한 경향은 임상시험 기술 및 서비스 업계 전반에서도 나타나고 있으며, 구매자들은 운영 데이터를 통합하고 수작업에 의한 업무 인계를 줄일 수 있는 도구로 전환하고 있습니다.

“서비스"는 2031년까지 연평균 성장률(CAGR)이 16.49%로, 최상위 수준의 부문 중에서 가장 빠르게 성장하고 있으며, 이는 임상시험 기술 및 서비스 시장에서 도입 노력이 소프트웨어 소유만큼 중요해지고 있음을 보여줍니다. 이러한 성장은 플랫폼이 복잡해지는 속도와, 많은 스폰서 팀이 사내에서 통합, 검증, 교육을 관리할 수 있는 능력 사이에 존재하는 구조적인 격차를 반영하고 있습니다. 2025년 8월 IQVIA와 Veeva의 제휴는 데이터 관리, EDC 프로그래밍, AI 지원에 이르는 기술의 상호 운용성과 서비스 제공 역량을 결합한 것으로, 이러한 상업적 논리를 명확히 보여주었습니다. 또한, 특히 종양학이나 원격 진료 시험의 경우, 프로토콜이 복잡해짐에 따라 참가자의 부담이 증가하고 중도 탈락 위험이 높아지기 때문에 피험자 모집 및 유지 서비스도 그 혜택을 보고 있습니다. 따라서 임상시험 기술 및 서비스 시장에서는 디지털 기능과 이를 대규모로 일관성 있게 운영하기 위해 필요한 운영 지원이 모두 중요시됨에 따라, 서비스 수요 증가에 발맞추어 환자 참여 유도 도구도 점차 보급되고 있습니다.

2025년 임상시험 기술 및 서비스 시장 규모에서 클라우드 기반 솔루션의 점유율은 49.77%를 차지했으며, 이는 CRO, 중규모 의뢰사 및 클라우드 네이티브 제공 체계를 기반으로 하는 벤더들 사이에서 널리 활용되고 있음을 반영합니다. 이 모델의 매력은 다기관 임상시험의 규모 확대, 데이터에 대한 신속한 접근, 인프라 부담 경감, 분산형 임상시험 도구와의 손쉬운 연동을 지원한다는 점에서 임상시험 기술 및 서비스 시장에서 여전히 분명합니다. 하이브리드형은 가장 빠르게 성장하고 있는 두 가지 도입 모델 중 하나로, 2031년까지의 연평균 성장률(CAGR)은 18.22%를 나타낼 것으로 예측됩니다. 이는 많은 기업이 단일 단계로 완전한 클라우드 전환을 수행하지 않고 있음을 보여줍니다. 대형 스폰서들은 완전한 교체가 규제 준수 체계 하에서 대규모 재검증 작업을 초래할 가능성이 있기 때문에 검증된 On-Premise형 기록 시스템을 유지하는 경우가 많습니다. 따라서 임상시험 기술 및 서비스 시장은 구식 기록 시스템과 새로운 클라우드 분석 도구, 환자용 도구가 확실하게 연동되어야 하는 혼합 환경을 중심으로 계속해서 발전하고 있습니다.

따라서 임상시험 기술 및 서비스 시장에서 On-Premise 도입의 점유율은 장기적으로 압박을 받고 있는 한편, 여전히 중요한 위치를 차지하고 있습니다. 데이터 저장 위치에 관한 규제나 사내 검증 이력 등으로 인해 신속한 이전보다는 로컬 관리가 더 바람직하다고 여겨지는 상황에서는 On-Premise 도입이 여전히 중요한 역할을 하고 있습니다. Veeva가 2026년 1월에 발표한 eSource 릴리스는 EDC와의 통합 및 EHR에서 EDC로의 데이터 전송을 통해, 현장 수준의 데이터 생성까지 연계된 워크플로우에 포함되고 있음을 보여줍니다. eSource, eConsent, eCOA 도구가 더욱 보급됨에 따라, 도입 결정은 공급업체가 단일 아키텍처만을 권장하는지 여부와 관계없이, 복잡한 전환 과정을 어느 정도 적절하게 지원할 수 있는지에 점점 더 좌우될 것입니다. 따라서 임상시험 기술 및 서비스 시장에서는 규제 대상인 레거시 시스템이나 깊이 뿌리내린 기존 시스템과의 호환성을 유지하면서 클라우드 확장을 관리할 수 있는 벤더가 여전히 우위를 점하고 있습니다.

지역별 분석

2025년, 북미는 임상시험 기술 및 서비스 시장 점유율의 41.64%를 차지하며, 지역별 매출 1위 자리를 계속 유지했습니다. 이 지역은 기업용 EDC, CTMS, eTMF 시스템의 도입 기반이 탄탄할 뿐만 아니라, 후기 단계 임상시험에서 스폰서와 CRO의 활동이 활발하다는 이점을 누리고 있습니다. FDA는 2026년 4월, Paradigm Health의 클라우드 기반 플랫폼을 활용하여 AstraZeneca 및 Amgen과 공동으로 실시간 임상시험 시범 프로젝트를 시작하는 한편, 보다 광범위한 초기 단계 AI 이니셔티브를 병행 추진함으로써 이러한 입지를 더욱 공고히 했습니다. 이 조치는 임상시험 기술 및 서비스 시장 전반에 걸쳐, 보다 견고한 디지털 인프라를 필요로 하는 지속적인 모니터링 모델로의 전환을 시사하는 것으로, 중요한 의미를 지닙니다. 캐나다는 심도 있는 학술 연구와 체계적으로 구축된 임상시험 시설 네트워크를 통해 지원을 강화하고 있는 반면, 멕시코는 북미에서 2상 및 3상 임상시험을 위한 비용 대비 효율이 높은 피험자 모집 거점으로서 여전히 중요한 위치를 차지하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 18.92%를 나타낼 것으로 전망되며, 임상시험 기술 및 서비스 시장에서 그 전략적 중요성이 커지고 있습니다. 이 지역은 스폰서의 관심 증가, 시험 활동의 확대, 그리고 다양한 시험 수행 환경을 아우르며 운영 가능한 확장성 있는 플랫폼에 대한 수요 증가라는 혜택을 누리고 있습니다. 또한, 임상시험 기술 및 서비스 시장에서 아시아태평양은 유연한 도입을 위한 시험장으로서도 주목받고 있습니다. 이는 시험 시설의 성숙도가 북미나 서유럽에 비해 편차가 크기 때문입니다. 이로 인해 도입 장벽이 낮고, 실용적인 교육을 제공하며, 첨단 환경과 일관성이 낮은 환경 모두에서 원활하게 작동하는 시스템을 구축할 수 있는 벤더들에게 비즈니스 기회가 생겨나고 있습니다. 또한, 구매자는 모든 시험 시설이 동일한 속도로 같은 수준의 디지털 전환에 대응할 수 있는 것은 아니기 때문에 클라우드 연결을 통한 조정이 필요한 경우가 많으며, 이러한 지역적 다양성이 하이브리드 도입을 촉진하고 있습니다.

유럽은 임상시험 기술 및 서비스 시장에서 여전히 중요한 수익 지역이며, 독일, 영국, 프랑스가 주요 수요 거점으로 자리 잡고 있습니다. EU 임상시험 규정 및 CTIS는 후원사의 업무 흐름을 재구성하고 있으며, ACT EU의 모니터링 보고서에 따르면, 2022년 1월 CTIS 개시 이후 누적 신청 건수는 2만 8,070건에 달했으며, 2026년 1분기에는 2,465건의 임상시험에 영향을 미치는 3,325건의 대규모 변경 신청이 제출되었습니다. 이러한 부담으로 인해 임상시험 기술 및 서비스 시장 전반에서 신청 관리, eTMF, 그리고 데이터 추적성 도구에 대한 수요가 증가하고 있습니다. 이탈리아, 스페인 및 기타 유럽 국가들에서는 2상 및 3상 임상시험 활동이 현저히 증가하고 있는 반면, 중동 및 아프리카 및 남미는 교육 및 도입 체계에 대한 조기 투자를 주저하지 않는 공급업체들에게 규모는 작지만 전략적으로 중요한 성장의 원천이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the clinical trial technology and services market size is expected to increase from USD 27.40 billion in 2025 to USD 31.24 billion in 2026 and reach USD 63.91 billion by 2031, growing at a CAGR of 15.39% over 2026-2031.

This report is Segmented by Offering (Technology Solutions, Services), Deployment Model (Cloud-Based, On-Premise, Hybrid), Clinical Trial Phase (Phase I-IV), End User (Pharma & Biotech, Medical Device, Cros, Healthcare Providers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Clinical Trial Technology and Services Market Trends and Insights

Rising Clinical Trial Complexity and Protocol Burden

Protocol complexity has become a direct spending trigger in the clinical trial technology and services market because it raises the cost of running studies and increases the need for structured digital oversight. In 2025, 76% of Phase I to Phase IV trials required at least 1 protocol amendment, up from 57% in 2015, and the average protocol accumulated 3.3 amendments across its life cycle. Oncology remained the clearest stress point, where 90% of protocols needed at least 1 substantial amendment, and 45% of substantial amendments were avoidable. A 2025 journal analysis also showed that total data volume per Phase III protocol has been rising by 10.8% a year since 2020, which explains why sponsors are leaning on stronger data collection, workflow, and analytics tools in the clinical trial technology and services market. Site pressure is also increasing because 38% of sites identified trial complexity as their top operating challenge in 2024, which supports demand for unified workflows that cut duplication and manual effort in the clinical trial technology and services market. That same pressure also reinforces stricter data integrity and audit expectations, since more complex studies create more records, more amendments, and more points of inspection across the trial process.

Rapid Adoption of Decentralized and Hybrid Trial Operations

The clinical trial technology and services market is benefiting from decentralized and hybrid trial adoption because regulators now treat these approaches as part of normal trial planning rather than as limited experiments. The FDA final guidance on trials with decentralized elements gives sponsors clearer operating expectations for telehealth visits, direct-to-patient product movement, digital health technology use, and remote oversight. A 2025 peer-reviewed paper on the Trials@Home RADIAL proof of concept also showed that conventional, hybrid, and fully decentralized designs can be run across multiple countries with technology packages that support onboarding, validation, and post-go-live governance. This is why the clinical trial technology and services market is not moving toward a single end state, because hybrid delivery has become a durable model for studies that still need physical site visits and remote data capture in the same protocol. The same shift also raises the importance of data traceability, since vendors must prove they can manage site and remote data streams together without weakening control. It also strengthens demand for site burden reduction tools, because hybrid operations work better when clinical teams use connected platforms instead of separate point systems.

Integration Complexity Across EDC, CTMS, eTMF, and Finance Systems

Integration difficulty remains a major drag on the clinical trial technology and services market because large sponsors still run deep legacy environments that are hard to consolidate. Veeva reported in 2025 that a top 20 biopharma customer removed more than 100 legacy integrations during a unified cloud CTMS move, which required the migration of more than 9 million records and training for more than 4,500 users. A separate Veeva customer story on GSK described a 3-year CTMS modernization program that migrated more than 6 million records from 1,500 active studies and onboarded 4,500 users before go-live. These examples show why the clinical trial technology and services market is not limited by software demand alone, because the cost of connecting EDC, CTMS, eTMF, finance, and legacy systems often shapes vendor choice more than license fees do. The same burden grows when buyers also need validation, training, and change management across large teams and regulated workflows. It also favors service vendors and hybrid deployment models, since many enterprises need staged modernization rather than a single cutover.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of AI-Enabled Feasibility, Monitoring, and Analytics

- Rising Outsourcing by Sponsors Seeking Flexible Trial Execution

- Cybersecurity, Privacy, and Cross-Border Data Governance Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technology solutions held 63.72% of the clinical trial technology and services market share in 2025, showing that core platform demand still leads spending across EDC, CTMS, eTMF, patient engagement, and analytics environments. The clinical trial technology and services market continues to rely on these systems because every sponsor type needs secure data capture, workflow control, and trial oversight across multiple geographies and phases. Within Technology Solutions, AI integration tools are expanding quickly because sponsors want intelligence layers that work across existing systems rather than full platform replacement. Trial management and data collection remain central within this segment, and the pressure on these tools is rising as protocol data volume keeps growing across late stage studies. The same pattern supports the wider clinical trial technology and services industry, where buyers are shifting toward tools that can unify operational data and reduce manual handoffs.

Services is the fastest-growing top-level segment, with a 16.49% CAGR through 2031, which shows that deployment effort is becoming as important as software ownership in the clinical trial technology and services market. This growth reflects a structural gap between the pace of platform complexity and the ability of many sponsor teams to manage integration, validation, and training internally. The August 2025 IQVIA and Veeva partnership made that commercial logic clear because it combined technology interoperability with service delivery capability across data management, EDC programming, and AI support. Recruitment and retention services are also benefiting because more complex protocols increase participant burden and raise dropout risk, especially in oncology and remote enabled studies. Patient engagement tools are therefore rising in parallel with service demand, since the clinical trial technology and services market now values both digital functionality and the operating support needed to make it work consistently at scale.

Cloud-Based deployment accounted for 49.77% share of the clinical trial technology and services market size in 2025, reflecting broad use among CROs, mid-sized sponsors, and vendors built around cloud native delivery. The appeal of this model remains straightforward in the clinical trial technology and services market because it supports multi-site scale, faster data access, lower infrastructure burden, and easier connection to decentralized trial tools. Hybrid is the fastest-growing2 deployment model, with an 18.22% CAGR through 2031, which shows that many enterprises are not making full cloud migrations in a single step. Large sponsors often keep validated on-premises record systems in place because full replacement can trigger major revalidation work under regulated compliance frameworks. That keeps the clinical trial technology and services market centered on mixed environments where older record systems and newer cloud analytics or patient tools need to work together reliably.

On-Premise deployment, therefore, remains relevant even as its share faces longer-term pressure in the clinical trial technology and services market. It still matters in settings where data residency rules or internal validation history make local control more attractive than rapid migration. Veeva's January 2026 eSource launch showed how even site level data origination is being pulled into connected workflows through EDC integration and EHR to EDC transfer. As eSource, eConsent, and eCOA tools spread further, deployment decisions will increasingly depend on how well vendors support complex transitions rather than on whether they promote only 1 architecture. That is why the clinical trial technology and services market still gives an advantage to vendors that can manage cloud growth while preserving compatibility with regulated and deeply embedded legacy estates.

Complete Report Scope:

- By Offering

- Technology Solutions

- Trial Launch Solutions

- Trial Management Solutions

- Data Collection and Analytics Solutions

- Patient Engagement Solutions

- AI Integration Solutions

- Services

- Consulting Services

- Training and Support Services

- Recruitment and Retention Services

- Implementation and Integration Services

- Technology Solutions

- By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

- By Clinical Trial Phase

- Phase I

- Phase II

- Phase III

- Phase IV

- By End User

- Pharmaceutical and Biotechnology Companies

- Medical Device Manufacturers

- Contract Research Organizations

- Healthcare Providers and Research Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.64% of the clinical trial technology and services market share in 2025, which kept it as the leading regional revenue base. The region benefits from a deep installed base of enterprise EDC, CTMS, and eTMF systems, along with dense sponsor and CRO activity across later-stage studies. The FDA strengthened this position in April 2026 when it launched a real-time clinical trial pilot with AstraZeneca and Amgen using Paradigm Health's cloud-based platform and paired that move with a broader early phase AI initiative. This step matters because it signals a shift toward continuous oversight models that require stronger digital infrastructure throughout the clinical trial technology and services market. Canada adds support through academic research depth and coordinated site networks, while Mexico remains relevant as a cost-effective enrollment location for North American Phase II and Phase III work.

Asia-Pacific is the fastest-growing region, with an 18.92% CAGR through 2031, which gives it a rising strategic role in the clinical trial technology and services market. The region is benefiting from broader sponsor interest, expanding trial activity, and a stronger need for scalable platforms that can operate across mixed site conditions. The clinical trial technology and services market also sees Asia-Pacific as a testing ground for flexible deployment because site maturity varies more widely than it does in North America or Western Europe. That creates room for vendors that can deliver low-friction implementations, practical training, and systems that work in both advanced and less uniform operating environments. The same regional mix also supports hybrid deployment, since buyers often need cloud-connected coordination without assuming that every site can absorb the same level of digital change at the same pace.

Europe remains a significant revenue region in the clinical trial technology and services market, with Germany, the United Kingdom, and France forming core demand centers. The EU Clinical Trials Regulation and CTIS are reshaping sponsor workflows, and the ACT EU monitoring report showed that 3,325 substantial modification applications affecting 2,465 trials were submitted in the first quarter of 2026, from a cumulative 28,070 applications since CTIS started in January 2022. This burden is lifting demand for submission management, eTMF, and data traceability tools across the clinical trial technology and services market. Italy, Spain, and other European countries add meaningful Phase II and Phase III activity, while the Middle East and Africa and South America offer smaller but strategically relevant growth pools for vendors willing to invest early in training and implementation capacity.

- Advarra, Inc.

- Clinion

- Cloudbyz

- Fortrea Holdings Inc.

- ICON

- IQVIA

- LabCorp

- Medidata Solutions, Inc.

- Medpace Holdings, Inc.

- Octalsoft

- Oracle

- Oracle Health Sciences

- Parexel International

- RealTime Software Solutions, LLC

- Signant Health

- SimpleTrials

- Syneos Health

- Thermo Fisher Scientific

- Veeva Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Clinical Trial Complexity and Protocol Burden

- 4.2.2 Rapid Adoption of Decentralized and Hybrid Trial Operations

- 4.2.3 Expansion of AI-Enabled Feasibility, Monitoring, and Analytics

- 4.2.4 Rising Outsourcing by Sponsors Seeking Flexible Trial Execution

- 4.2.5 More Stringent Data Integrity, Traceability, and Audit Expectations

- 4.2.6 Site Burden Reduction Through Unified Clinical Operating Platforms

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across EDC, CTMS, eTMF, and Finance Systems

- 4.3.2 High Validation, Training, and Change-Management Costs

- 4.3.3 Cybersecurity, Privacy, and Cross-Border Data Governance Risk

- 4.3.4 Uneven Digital Readiness Across Sites and Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Offering

- 5.1.1 Technology Solutions

- 5.1.1.1 Trial Launch Solutions

- 5.1.1.2 Trial Management Solutions

- 5.1.1.3 Data Collection and Analytics Solutions

- 5.1.1.4 Patient Engagement Solutions

- 5.1.1.5 AI Integration Solutions

- 5.1.2 Services

- 5.1.2.1 Consulting Services

- 5.1.2.2 Training and Support Services

- 5.1.2.3 Recruitment and Retention Services

- 5.1.2.4 Implementation and Integration Services

- 5.1.1 Technology Solutions

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Clinical Trial Phase

- 5.3.1 Phase I

- 5.3.2 Phase II

- 5.3.3 Phase III

- 5.3.4 Phase IV

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Medical Device Manufacturers

- 5.4.3 Contract Research Organizations

- 5.4.4 Healthcare Providers and Research Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Advarra, Inc.

- 6.3.2 Clinion

- 6.3.3 Cloudbyz

- 6.3.4 Fortrea Holdings Inc.

- 6.3.5 ICON plc

- 6.3.6 IQVIA Inc.

- 6.3.7 Labcorp

- 6.3.8 Medidata Solutions, Inc.

- 6.3.9 Medpace Holdings, Inc.

- 6.3.10 Octalsoft

- 6.3.11 Oracle Corporation

- 6.3.12 Oracle Health Sciences

- 6.3.13 Parexel International Corporation

- 6.3.14 RealTime Software Solutions, LLC

- 6.3.15 Signant Health

- 6.3.16 SimpleTrials

- 6.3.17 Syneos Health

- 6.3.18 Thermo Fisher Scientific Inc.

- 6.3.19 Veeva Systems Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment