|

시장보고서

상품코드

2073164

방사선 의학용 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Radiology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

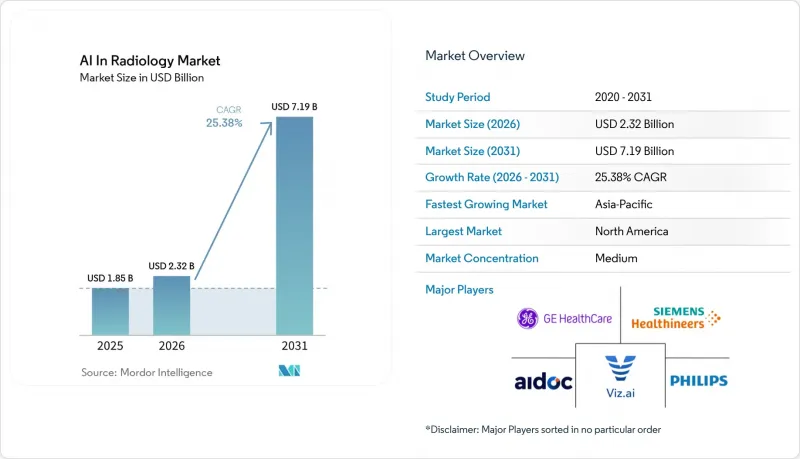

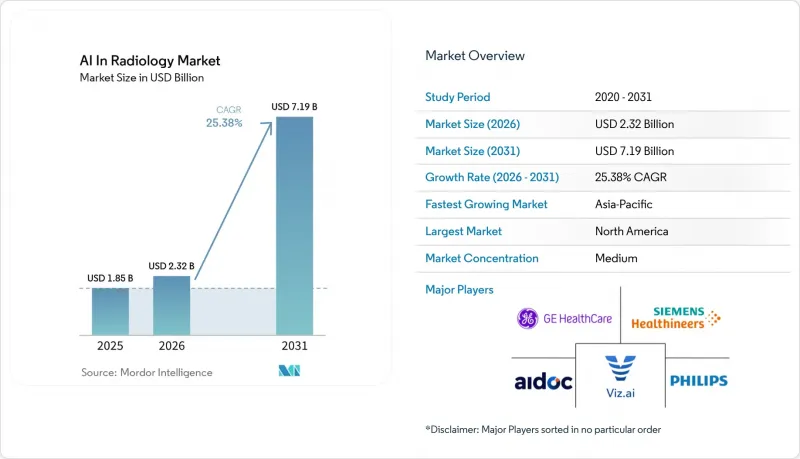

Mordor Intelligence에 의하면, 방사선 의학용 인공지능(AI) 시장 규모는 2025년 18억 5,000만 달러로 평가되었습니다. 2026년에는 23억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 25.38%로 성장을 지속하여, 2031년에는 71억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스, 하드웨어), 기술(딥러닝, 컴퓨터 비전 등), 모달리티(CT, MRI, X선, 초음파, 유방촬영술, PET), 배포 방식(클라우드, On-Premise, 하이브리드), 용도(감지, 분할, 트리아지, 분석, 위험), 최종 사용자(병원 등), 지역(북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 방사선 의학용 인공지능(AI) 시장 동향 및 인사이트

영상 검사 건수 증가와 스캔 처리 지연

많은 의료 시스템에서 영상 검사 건수 증가 속도가 판독 능력의 확대 속도를 앞지르고 있기 때문에 방사선 의학용 인공지능(AI) 시장이 확대되고 있습니다. 영국에서는 진단용 영상 검사 수요가 연평균 5% 이상 증가하고 있는 반면, 인력 공급 증가율은 3% 수준에 그치고 있어, 2023년에는 방사선과 인력 부족률이 33%에 달한 것으로 보고되었습니다. 고령화, 암 경과 관찰, 그리고 첨단 CT의 보급으로 인해 선진국과 신흥국을 막론하고 의료 현장에서 영상 진단 업무 부담은 여전히 높은 수준을 유지하고 있습니다. 따라서 의료 제공업체들은 긴급성이 높은 검사를 우선 처리하고, 보고 지연이 확대되는 것을 방지할 수 있는 도구를 찾고 있으며, 영상 진단 분야의 AI 시장에서는 검사 대기 관리 기능이 구매 결정의 직접적인 요인으로 작용하고 있습니다. 그 결과, 구매자들은 단순한 감지 기능에 그치지 않고, 해당 도구가 영상 진단 워크플로우 전반에 걸쳐 미처리 건수를 줄일 수 있는지 여부를 따져보게 되었습니다. 이러한 수요 추세는 방사선 의학용 인공지능(AI) 시장에서 제한적인 포인트 솔루션 도입이 아닌, 보다 광범위한 플랫폼의 채택을 촉진하고 있습니다.

방사선과 전문의 부족 문제와 번아웃 완화

방사선과 전문의의 인력 부족은 방사선 의학용 인공지능(AI) 시장을 장기적으로 견인하는 요인이 되고 있습니다. 이는 연수 체계의 확대가 의료 수요를 따라가지 못하고 있기 때문입니다. 2014년부터 2023년 사이에 ACR 커리어 센터에 게시된 방사선과 채용 공고 건수는 총 3만 1,825건이었으나, 레지던트 수료 예정자는 1만 180명에 그쳐 미국에서는 누적 21,645명의 인력 부족이 발생했습니다. 2025년 보고서에서는 2032년까지 12만 2,000명의 방사선과 전문의가 부족할 것이라는 예측도 제시되었으며, 이는 해당 공급 문제가 순환적인 것이 아니라 구조적인 것이라는 견해를 뒷받침하고 있습니다. 2025년 『Journal of the American College of Radiology』의 조사에 따르면, 대학병원 방사선과 과장 중 100%가 품질과 효율 향상을 목적으로 AI 도입을 계획하고 있었으며, 95%는 번아웃 완화를 목적으로 도입을 계획하고 있었습니다. 방사선 의학용 인공지능(AI) 시장이 지닌 실질적인 가치는 단순히 업무 자동화에 그치지 않습니다. 우선순위 설정, 체계적인 결과물 산출, 초안 작성 지원을 통해 인지적 부하를 줄이면, 방사선과 의사의 임상적 역할을 변경하지 않으면서도 피로를 완화할 수 있기 때문입니다. 이에 따라 생산성 향상이 필요하면서도 의사의 감독을 유지하고 싶어 하는 병원 네트워크 전반에서 AI 도입에 대한 관심이 계속해서 높아지고 있습니다.

높은 도입 비용과 ROI의 불확실성

도입 비용은 여전히 방사선 의학용 인공지능(AI) 시장에 큰 걸림돌이 되고 있습니다. 특히 소규모 의료 시스템이나 최상위급 의료기관이 아닌 영상 진단 서비스 제공업체의 경우 더욱 그렇습니다. 비용 문제는 소프트웨어 라이선스에 그치지 않고, 구매자는 통합 테스트, 워크플로우 변경, 직원 재교육, 도입 후 지속적인 모니터링과 같은 과제에도 직면하고 있습니다. 2025년 『Journal of the American College of Radiology』의 조사에 따르면, AI 도입을 검토 중인 대학 부속 병원 방사선과 과장들 사이에서 비용이 가장 큰 우려 사항으로 꼽혔습니다. 소규모 의료기관은 불확실한 수익을 상쇄할 여력이 제한적인 경우가 많기 때문에 디지털 영상 진단 인프라가 아직 충분히 갖춰지지 않은 지역에서는 방사선 의학용 인공지능(AI) 시장 성장이 더 완만해질 가능성이 있습니다. 조달 팀이 일관된 비용 대비 효과 모델을 사용하여 유사한 시설 간의 성과를 비교할 수 없는 경우, 이 문제는 더욱 심각해집니다. 따라서, 위험 분담형 가격 책정 및 관리형 서비스 체제가 방사선 의학용 인공지능(AI) 시장에서 주목을 받고 있습니다. 이는 상업적 부담의 일부를 공급업체 측으로 전가하는 구조이기 때문입니다.

부문별 분석

2025년 기준으로 소프트웨어는 방사선 의학용 인공지능(AI) 시장 점유율의 42.31%를 차지한 반면, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 27.38%를 나타낼 것으로 예측됩니다. 현재 매출에서 소프트웨어가 차지하는 우위는 병원 및 영상 진단 네트워크 전반에 걸쳐 감지, 분류, 우선순위 지정 및 보고서 작성 지원을 위해 사용되고 있는 승인된 도구의 도입 실적을 반영한 것입니다. 방사선 의학용 인공지능(AI) 시장에서 소프트웨어는 여전히 구매자가 가장 먼저 평가하는 요소로 남아 있습니다. 이는 소프트웨어가 영상 판독 워크플로우, 사례 배정 및 업무 처리 능력에 직접적인 영향을 미치기 때문입니다. 또한, 이미 구축된 인프라 덕분에 소프트웨어 공급업체는 동일한 의료 시스템 내의 인접한 영상진단 적응증 분야로 사업을 확장할 수 있는 지속적인 기회를 얻고 있습니다. 그 결과, 소프트웨어 계층은 여전히 방사선 의학용 인공지능(AI) 시장 조달 결정의 기반이 되고 있습니다.

서비스 분야의 성장이 가속화되고 있는 이유는 도입이 더 이상 단일 알고리즘이나 제한적인 시범 프로그램에 그치지 않기 때문입니다. 현재 기업 구매 담당자들은 도입 지원, 모델 모니터링, 재학습, 거버넌스 및 변경 관리를 계약의 표준 요소로 요구하고 있습니다. 따라서, 방사선 의학용 인공지능(AI) 시장에서는 병원이 단일 운영 체제 하에서 여러 임상 알고리즘을 운영할 수 있도록 지원하는 매니지드 서비스에 대한 수요가 발생하고 있습니다. 하드웨어는 AI 지원 스캐너로의 업그레이드를 통해 계속해서 성장을 뒷받침하고 있지만, 의료 기관들이 유연한 도입과 장기적인 지원을 우선시함에 따라 수익 구조는 소프트웨어 및 서비스 쪽으로 전환되고 있습니다. 이러한 변화는 방사선 의학용 인공지능(AI) 산업에서 일회성 도구 구매가 아닌, 지속 가능한 플랫폼 경제로의 광범위한 전환을 반영한 것이기도 합니다.

2025년에는 딥러닝이 매출의 55.24%를 차지하며, 방사선 의학 분야 AI 시장의 핵심 기술 기반으로서의 위상을 유지했습니다. 이러한 우위는 CT 및 X선 워크플로우 전반에 걸친 이미지 분류, 이상 감지, 분할, 장기 정량화 분야에서 확립된 활용 사례에서 비롯됩니다. 도입된 이미지 처리 알고리즘의 대부분은 여전히 이러한 작업에 의존하고 있기 때문에 예측 기간 동안 딥러닝은 도입 기반에서 핵심적인 위치를 계속 차지할 것으로 보입니다. 또한, 머신러닝은 직접적인 영상 판독의 범위를 넘어선 예측 모델 및 위험도 계층화 등의 활용 사례를 통해 방사선 의학용 인공지능(AI) 시장을 뒷받침하고 있습니다. 이미지 획득 과정에서 품질 평가를 지원하고 재검사 필요성을 줄이기 위해 컴퓨터 비전 도구의 활용이 점점 더 늘어나고 있습니다.

자연어 처리는 2031년까지 연평균 성장률(CAGR)이 26.52%에 달하며, 방사선 의학용 인공지능(AI) 시장에서 가장 빠르게 성장하고 있는 기술입니다. 이러한 성장은 다음 단계의 초점이 보고서 작성 지원, 체계적인 문서화, 그리고 일상적인 소견의 자동 입력으로 옮겨가고 있음을 보여줍니다. 2026년 『Information Systems Frontiers』에 게재된 논문에서는 개념 강화형 다중 모달 검색-보강 생성(concept-enhanced multimodal retrieval-augmented generation)이 보다 해석하기 쉽고 정확한 방사선 진단 보고서 생성을 위한 현실적인 방안이라고 언급하고 있습니다. 보고서 작성 단계가 중요한 이유는 방사선과 의사가 요구하는 것이 단순한 영상 분류의 정확도 향상뿐만 아니라 속도, 일관성, 그리고 인지 부하의 경감이기 때문입니다. 이는 방사선 의학 분야에서 AI 산업이 영상 판독 지원에서 보고서 작성 워크플로우 전반에 걸친 지원으로 전환될 수 있는 가장 명확한 분야 중 하나입니다.

지역별 분석

2025년, 북미는 방사선 의학 분야 AI 시장 점유율의 43.22%를 차지하며, 해당 시장에서 가장 규모가 큰 지역 거점으로서의 위상을 유지했습니다. 이 지역은 특히 디지털 영상 인프라가 잘 갖춰진 병원 시스템 분야에서 시범 운영을 거쳐 기업 차원의 도입 단계로 나아가며 다른 지역보다 한 발 더 앞서 있습니다. 미국은 방대한 양의 이미지, 활발한 학술 분야에서의 도입, 그리고 OEM 및 소프트웨어 전문 기업에 이르는 탄탄한 공급업체 기반을 모두 갖추고 있어 여전히 주요 견인차 역할을 하고 있습니다. 2026년 3월, GE HealthCare는 Intelerad를 23억 달러에 인수하는 절차를 완료했으며, 이를 통해 미국, 캐나다, 영국, 오세아니아 전역에서 클라우드 우선 기업용 영상 진단 사업의 확장을 가속화했습니다. 캐나다와 멕시코는 여전히 시장에 기여하는 정도는 작지만, 미국의 방사선 의학 분야 AI 시장을 뒷받침하는 것과 동일한 상호운용성 기준 및 공급업체 생태계에 근접해 있다는 장점이 있습니다.

유럽은 방사선 의학용 인공지능(AI) 시장에서 여전히 2위의 규모를 자랑하는 지역 블록이며, 독일, 영국, 프랑스, 이탈리아, 스페인이 주요 수요 기반을 형성하고 있습니다. 특히 독일은 중요한 위치를 차지하고 있으며, 병원의 현대화를 위한 자금 투입으로 인해 영상 진단 AI의 대규모 도입이 가속화되었습니다. 여기에는 2025년 Aidoc이 보고한 28개 병원을 대상으로 한 아스클레피오스(Asklepios) 도입 사례도 포함됩니다. 2025년 1월 기준으로, 최소 219종의 방사선 AI 제품이 EU의 CE 인증을 획득했으며, 이는 이 지역에서 이용 가능한 제품의 폭이 매우 넓음을 보여줍니다. 이에 따라, 각국 및 EU 차원의 요건을 아우르는 규정 준수 요건이 여전히 다층적임에도 불구하고, 유럽의 방사선 AI 시장은 폭넓은 제품 기반을 갖추고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 27.15%에 달하고, 방사선 AI 시장에서 가장 빠르게 성장하고 있는 지역입니다. 중국, 일본, 한국, 인도, 호주가 주요 성장 동력으로 작용하고 있으며, 이들 국가는 의료의 디지털화와 영상 진단 역량의 확대, 그리고 국내 및 수입 AI 제품 증가가 맞물려 성장을 주도하고 있습니다. 중국 국가의약품감독관리국(NMPA)은 2025년에 76건의 혁신적인 의료기기를 승인했으며, 이는 전년 대비 17% 증가한 수치입니다. 이는 첨단 의료 기술용 제품 공급이 더욱 확대되고 있음을 보여줍니다. 2025년 8월, Shanghai United Imaging Healthcare의 “uCT Ultima"는 중국 내에서 최초로 개발된 광자 계수형 스펙트럼 CT로서, NMPA의 승인을 획득했으며, 상하이의 주요 병원에서 임상시험이 시작되었습니다. 일본도 2025년, 일본방사선의학회의 지침 개정을 통해 운영 환경을 정비했습니다. 중동 및 아프리카에서는 각국의 디지털 헬스 프로그램을 통해 성장세가 가속화되고 있는 반면, 남미는 여전히 초기 단계에 머물러 있으며, 브라질과 아르헨티나가 방사선 의학용 인공지능(AI) 시장 개척을 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the AI in radiology market size is expected to grow from USD 1.85 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 7.19 billion by 2031 at 25.38% CAGR over 2026-2031.

This report is Segmented by Component (Software, Services, Hardware), Technology (Deep Learning, Computer Vision, and More), Modality (CT, MRI, X-Ray, Ultrasound, Mammography, PET), Deployment (Cloud, On-Premise, Hybrid), Application (Detection, Segmentation, Triage, Analytics, Risk), End User (Hospitals and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Radiology Market Trends and Insights

Rising Imaging Volumes and Scan Backlogs

The AI in radiology market is expanding because scan volumes continue to rise faster than reading capacity in many health systems. In the United Kingdom, diagnostic imaging demand grows at more than 5% annually, while workforce supply has been expanding at close to 3%, and a 33% radiology staffing shortfall was documented in 2023. Aging populations, oncology surveillance, and wider use of advanced CT are keeping imaging workloads elevated across both developed and emerging care settings. This makes queue control a direct purchasing argument in the AI in radiology market, because providers want tools that can prioritize urgent studies and keep reporting delays from widening. The result is that buyers are looking beyond stand-alone detection and are asking whether a tool can reduce backlogs across the full imaging workflow. That demand pattern supports broader platform adoption in the AI in radiology market instead of narrow point-solution deployment.

Radiologist Shortage and Burnout Relief

The radiologist workforce gap is a long-term driver for the AI in radiology market because the training pipeline is not expanding fast enough to match care demand. Between 2014 and 2023, radiology job listings on the ACR Career Center totaled 31,825 against 10,180 anticipated residency graduates, leaving a cumulative deficit of 21,645 positions in the United States. A 2025 review also noted projections of a 122,000 radiologist shortage by 2032, which reinforces the view that this supply issue is structural rather than cyclical. In a 2025 Journal of the American College of Radiology survey, 100% of academic radiology department chairs planned AI implementation to improve quality and efficiency, and 95% planned it to reduce burnout. The practical value in the AI in radiology market is not only task automation, because cognitive offloading through prioritization, structured outputs, and draft support can lower fatigue without changing the radiologist's clinical role. That keeps adoption interest high across hospital networks that need productivity gains but still want physician oversight.

High Implementation Cost and ROI Uncertainty

Implementation cost is still a real brake on the AI in radiology market, especially for smaller health systems and imaging providers outside top-tier institutions. The cost issue goes beyond software licenses because buyers also face integration testing, workflow changes, staff retraining, and ongoing monitoring after deployment. In the 2025 Journal of the American College of Radiology survey, cost was identified as the leading concern among academic radiology department chairs evaluating AI deployment. Smaller providers often have less room to absorb uncertain returns, so the AI in radiology market can move more slowly where digital imaging infrastructure is still limited. The challenge is stronger when procurement teams cannot compare outcomes across similar facilities with a consistent cost-benefit model. That is why shared-risk pricing and managed service structures are gaining attention in the AI in radiology market, because they shift some of the commercial burden back to vendors.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Faster Triage and Turnaround Times

- Regulatory Support for AI SaMD Approvals

- Data Quality, Label Scarcity, and Annotation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 42.31% of AI in radiology market share in 2025, while services are projected to grow at 27.38% CAGR through 2031. The current revenue lead reflects the installed base of cleared tools used for detection, classification, prioritization, and reporting support across hospital and imaging networks. In the AI in radiology market, software remains the first layer buyers evaluate because it directly affects reading workflow, case routing, and operational throughput. The installed base also gives software vendors a recurring opportunity to expand into adjacent imaging indications within the same health system. As a result, the software layer still anchors procurement decisions in the AI in radiology market.

Services are gaining faster because deployment is no longer limited to a single algorithm or a narrow pilot program. Enterprise buyers now want implementation support, model monitoring, retraining, governance, and change management as standard parts of the contract. The AI in radiology market therefore creates room for managed services that help hospitals run multiple clinical algorithms under one operating structure. Hardware continues to support growth through AI-accelerated scanner upgrades, but the revenue mix is shifting toward software and services as institutions prioritize flexible deployment and long-term support. That shift also reflects the wider move in the AI in radiology industry toward repeatable platform economics instead of one-time tool purchases.

Deep Learning held 55.24% of revenue in 2025, which kept it as the core technology foundation in the AI in radiology market. Its lead comes from established use in image classification, anomaly detection, segmentation, and organ quantification across CT and X-ray workflows. Because most deployed imaging algorithms still depend on these tasks, deep learning is likely to remain central to the installed base over the forecast period. Machine learning also supports the AI in radiology market through predictive models and risk stratification use cases that extend beyond direct image reading. Computer vision tools are increasingly being used during image acquisition to help assess quality and reduce the need for repeat studies.

Natural language processing is the fastest-growing technology in the AI in radiology market at 26.52% CAGR through 2031. That growth shows that the next control point is shifting toward reporting support, structured documentation, and automatic population of routine findings. A 2026 paper in Information Systems Frontiers described concept-enhanced multimodal retrieval-augmented generation as a viable path toward more interpretable and accurate radiology report generation. The reporting layer matters because radiologists need speed, consistency, and lower cognitive load, not only better image classification. This is one of the clearest areas where the AI in radiology industry can move from assisting image review to supporting the full reporting workflow.

Complete Report Scope:

- By Component

- Software

- Services

- Hardware

- By Technology

- Deep Learning

- Machine Learning

- Natural Language Processing

- Computer Vision

- By Modality

- Computed Tomography

- Magnetic Resonance Imaging

- X-ray

- Ultrasound

- Mammography

- Positron Emission Tomography

- Other Modalities

- By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

- By Application

- Detection and Diagnosis

- Image Segmentation and Classification

- Workflow Optimization and Triage

- Predictive and Prognostic Analytics

- Disease Risk Assessment

- Other Applications

- By End User

- Hospitals and Clinics

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 43.22% of AI in radiology market share in 2025, which kept it as the largest regional base for the AI in radiology market. The region has moved further than others from pilot testing into enterprise procurement, especially in hospital systems with strong digital imaging infrastructure. The United States remains the main driver because it combines large imaging volumes, active academic deployment, and a dense vendor base spanning OEMs and software specialists. In March 2026, GE HealthCare completed its USD 2.3 billion acquisition of Intelerad, which expanded its cloud-first enterprise imaging footprint across the United States, Canada, the United Kingdom, and Oceania. Canada and Mexico remain smaller contributors, but they benefit from proximity to the same interoperability standards and vendor ecosystem that support the AI in radiology market in the United States.

Europe remains the second-largest regional block in the AI in radiology market, with Germany, the United Kingdom, France, Italy, and Spain forming the core demand base. Germany has been especially important because hospital modernization funding accelerated imaging AI rollout at scale, including the 28-hospital Asklepios deployment reported by Aidoc in 2025. As of January 2025, at least 219 radiology AI products held EU CE certification, which shows the breadth of available products in the region. This gives the AI in radiology market in Europe a wide product base, even though compliance demands remain layered across national and EU-level requirements.

Asia-Pacific is the fastest-growing region in the AI in radiology market at 27.15% CAGR through 2031. China, Japan, South Korea, India, and Australia are the main growth engines because they combine healthcare digitalization with expanding imaging capacity and a rising number of local and imported AI products. China's National Medical Products Administration approved 76 innovative medical devices in 2025, up 17% year on year, which points to stronger product availability for advanced care technologies. In August 2025, Shanghai United Imaging Healthcare's uCT Ultima, described as the first domestically developed photon-counting spectral CT, received NMPA approval and entered clinical testing at major Shanghai hospitals. Japan also formalized its operating environment in 2025 through revised guidance from the Japan Radiological Society. Middle East and Africa are gaining traction through national digital health programs, while South America remains earlier stage, with Brazil and Argentina as the main openings for the AI in radiology market.

- Aidoc Medical Ltd.

- AIRS Medical, Inc.

- Annalise.ai Pty Ltd.

- Canon

- DeepHealth, Inc.

- Enlitic

- FUJIFILM

- GE HealthCare Technologies Inc.

- Hologic

- iCAD, Inc.

- Koninklijke Philips

- Lunit

- Merative

- Qure.ai Technologies Pvt. Ltd.

- Rad AI, Inc.

- Shanghai United Imaging Healthcare Co., Ltd.

- Siemens Healthineers

- Subtle Medical, Inc.

- Viz.ai, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Imaging Volumes and Scan Backlogs

- 4.2.2 Radiologist Shortage and Burnout Relief

- 4.2.3 Demand for Faster Triage and Turnaround Times

- 4.2.4 Regulatory Support for AI SaMD Approvals

- 4.2.5 Enterprise PACS and EHR Interoperability Push

- 4.2.6 Value-Based Care Pressure on Repeat-Scan Reduction

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost and ROI Uncertainty

- 4.3.2 Data Quality, Label Scarcity, and Annotation Cost

- 4.3.3 Regulatory Fragmentation Across Countries

- 4.3.4 Low Trust in Black-Box Outputs for Edge Cases

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Technology

- 5.2.1 Deep Learning

- 5.2.2 Machine Learning

- 5.2.3 Natural Language Processing

- 5.2.4 Computer Vision

- 5.3 By Modality

- 5.3.1 Computed Tomography

- 5.3.2 Magnetic Resonance Imaging

- 5.3.3 X-ray

- 5.3.4 Ultrasound

- 5.3.5 Mammography

- 5.3.6 Positron Emission Tomography

- 5.3.7 Other Modalities

- 5.4 By Deployment Mode

- 5.4.1 Cloud-Based

- 5.4.2 On-Premise

- 5.4.3 Hybrid

- 5.5 By Application

- 5.5.1 Detection and Diagnosis

- 5.5.2 Image Segmentation and Classification

- 5.5.3 Workflow Optimization and Triage

- 5.5.4 Predictive and Prognostic Analytics

- 5.5.5 Disease Risk Assessment

- 5.5.6 Other Applications

- 5.6 By End User

- 5.6.1 Hospitals and Clinics

- 5.6.2 Diagnostic Imaging Centers

- 5.6.3 Ambulatory Surgical Centers

- 5.6.4 Other End Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Aidoc Medical Ltd.

- 6.3.2 AIRS Medical, Inc.

- 6.3.3 Annalise.ai Pty Ltd.

- 6.3.4 Canon Medical Systems Corporation

- 6.3.5 DeepHealth, Inc.

- 6.3.6 Enlitic, Inc.

- 6.3.7 Fujifilm Holdings Corporation

- 6.3.8 GE HealthCare Technologies Inc.

- 6.3.9 Hologic, Inc.

- 6.3.10 iCAD, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Lunit Inc.

- 6.3.13 Merative

- 6.3.14 Qure.ai Technologies Pvt. Ltd.

- 6.3.15 Rad AI, Inc.

- 6.3.16 Shanghai United Imaging Healthcare Co., Ltd.

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Subtle Medical, Inc.

- 6.3.19 Viz.ai, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment