|

시장보고서

상품코드

2073196

후두경 블레이드 및 핸들 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Laryngoscope Blades and Handles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

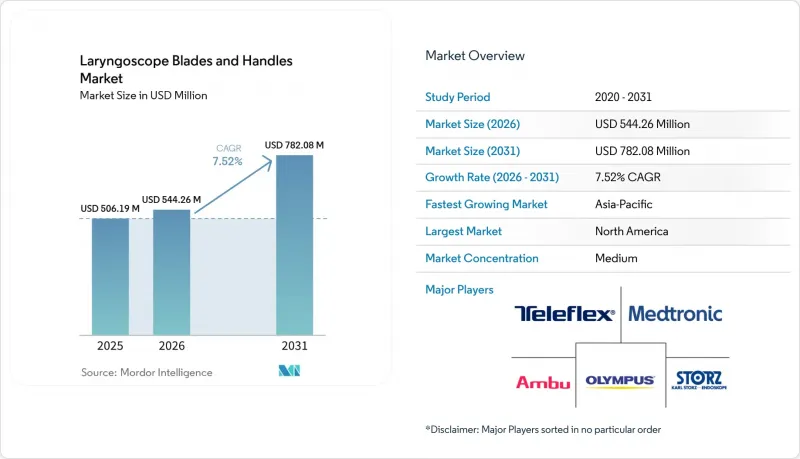

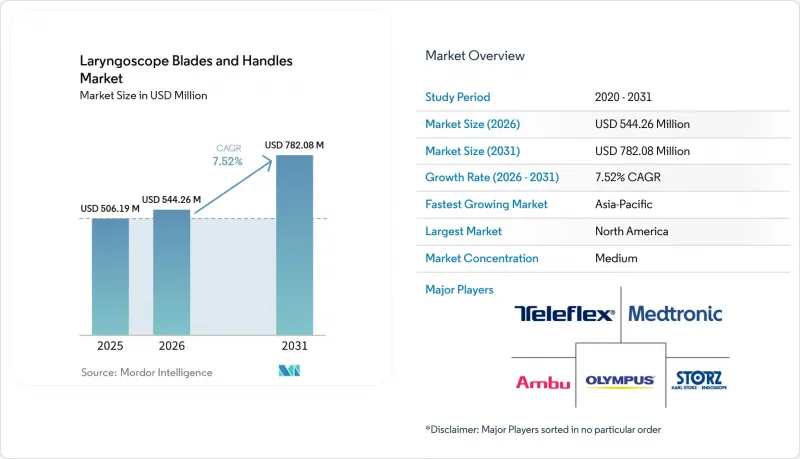

Mordor Intelligence에 의하면, 후두경 블레이드 및 핸들 시장 규모는 2025년 5억 619만 달러에서 2026년에는 5억 4,426만 달러로 확대되어 2031년까지 7억 8,208만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 7.52%로 성장할 전망입니다.

본 보고서는 제품 유형(블레이드(맥킨토시 블레이드 등), 핸들(표준 핸들 등)), 재질(스테인리스 스틸, 플라스틱 및 폴리머 계열, 하이브리드 및 복합재), 용도(성인, 소아, 신생아, 기도 확보가 어려운 사례), 최종 사용자(병원, 전문 클리닉 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 후두경 블레이드 및 핸들 시장 동향과 인사이트

호흡기 질환의 부담 증가에 따른 기도 관리 수요 증가

후두경 블레이드 및 핸들 시장은 선진국과 신흥국 모두의 의료 시스템에서 만성 호흡기 질환의 부담이 증가함에 따라 지속적인 수요에 힘입어 성장하고 있습니다. 세계보건기구(WHO)와 유럽호흡기학회는 2025년 6월, WHO 유럽에서 8,170만 명이 만성 호흡기 질환을 앓고 있으며, 매년 680만 건의 신규 진단 사례가 발생하고, 관련 사망의 80%를 COPD가 차지한다고 보고했습니다. 해당 보고서에서는 진단 누락으로 인한 비용이 연간 200억 달러를 넘는 것으로 추산되고 있으며, 이는 조기 외래 관리가 아닌 급성기 기도 관리가 필요한 상태에서 진료를 받는 환자가 여전히 다수 존재함을 시사하고 있습니다. 동남아시아의 경우, 향후 환자 수 증가를 고려할 때 그 부담은 더욱 심각합니다. WHO가 2025년에 발표한 보고서에 따르면, 만성 호흡기 질환은 전체 사망의 12% 가까이를 차지하고 있으며, 중환자실(ICU) 이용이 여전히 불균등한 의료 체계에서는 응급 및 중환자 치료 시 기관 삽관에 대한 수요가 구조적으로 높은 수준을 유지하게 될 것입니다. 기존 설비의 상당수는 여전히 기존의 재사용 가능한 스테인리스 스틸 시스템에 의존하고 있기 때문에 첫 번째 주요 업그레이드는 고가이며 모니터를 많이 사용하는 솔루션이 아닌, 저비용 비디오 플랫폼을 통해 이루어질 가능성이 높다고 볼 수 있습니다. 2020년부터 2050년까지 전 세계적으로 COPD 환자 수가 23% 증가할 것으로 예측됨에 따라, 이러한 수요 기반은 향후 수년에 걸쳐 확대될 것이며, 후두경 블레이드 및 핸들 시장에는 매우 드문 수준의 장기적인 임상적 전망이 열리게 될 것입니다.

교차 오염 위험을 줄이기 위한 일회용 블레이드로의 전환

후두경 블레이드 및 핸들 시장은 오염에 대한 우려가 더 이상 블레이드 표면에만 국한되지 않게 됨에 따라 일회용 제품으로 전환되고 있습니다. Flexicare사는 2025년에 재사용 가능한 후두경 손잡이의 86%에서 표준 닦아내기 소독 후에도 세균이 검출되었다는 임상 데이터를 보고했습니다. 한편, APSF는 일회용 기기가 재처리 공정에 수반되는 운영상의 복잡성을 해소한다고 지적하고 있습니다. 이 점이 중요한 이유는 병원의 구매 담당자들이 현재 핸들을 블레이드와 동등한 수준의 중요도를 지닌 오염 매개체로 간주하고 있기 때문이며, 이로 인해 과거에는 재사용 가능한 기기가 주류를 이루던 이 분야에 변화가 일어나고 있습니다. 일회용 제품이 블레이드에서 핸들로 전환됨에 따라 수익 구조도 변화하고 있습니다. 이는 프리미엄이 일회성 자본재에서 처치할 때마다 발생하는 지속적인 소모품으로 전환되고 있기 때문입니다. 앰브사가 2026년 6월에 “Recircle” 프로그램을 확대하고 바이오플라스틱으로 제작된 SureSight 블레이드를 추가한 것은 공급업체가 현재 고객에게 둘 중 하나를 선택하도록 강요하는 대신 감염 관리와 지속가능성을 동시에 해결하고자 하고 있음을 보여줍니다. 이러한 복합적인 가치 제안은 기존의 임상적·비용적 기준에 더해, 환경 평가가 낙찰 결과에 영향을 미치기 시작한 유럽의 공공 조달 시장에서 더욱 중요해질 가능성이 있습니다.

첨단 영상·광섬유 시스템 도입 비용의 높음

후두경 블레이드 및 핸들 시장은 첨단 영상 및 광섬유 시스템의 초기 비용을 감당할 수 없는 병원들에서 여전히 뚜렷한 도입 장벽에 직면해 있습니다. 기본적인 재사용 가능한 광섬유 핸들과 독자적인 사양의 영상 기능이 포함된 세트 간의 가격 차이는 여전히 크며, 수술 1회당 15-80달러가 드는 일회용 영상 블레이드의 지속적인 비용은 소모품 예산이 엄격하게 제한된 의료 기관에 있어 추가적인 부담이 되고 있습니다. 비디오 도입에 대한 임상적 근거가 확고하더라도, 이러한 비용 장벽은 중요한 문제가 됩니다. 왜냐하면 많은 조달 팀이 여전히 광범위한 의료 품질 지표가 아닌, 즉각적인 투자 회수라는 관점에서 기도 확보용 기기를 평가하고 있기 때문입니다. 각 공급업체들은 가시화의 이점을 해치지 않으면서, 사례당 비용을 절감하고 진입 장벽을 낮추는 보다 모듈화된 방식으로 이에 대응하고 있습니다. Verathon사의 “ClearFit”디자인은 그러한 대응의 한 예입니다. 이 디자인은 영상 구성 요소를 여러 가지 일회용 커버 옵션에 분산시켜, 신속한 대응이 요구되는 의료 현장에서 보다 유연한 비용 구조를 실현하고 있습니다. 비슷한 가성비를 갖춘 모델이 보급되기 전까지는 남미, 중동 및 아프리카 및 아시아태평양의 비도시권 시장에서 후두경 블레이드 및 핸들 시장의 전환 속도는 계속해서 완만할 것으로 보입니다.

부문별 분석

2025년, 후두경 블레이드는 후두경 블레이드 및 핸들 시장 점유율의 65.31%를 차지하고 있으며, 이 부문의 판매량은 여전히 소모품 쪽에 집중되어 있음을 알 수 있습니다. 이러한 상황은 수술실, 응급실, 중환자실(ICU) 전반에 걸쳐 직접 후두경 검사 워크플로가 전 세계적으로 널리 보급되고 있음을 반영합니다. 맥킨토시형 및 밀러형 디자인은 사용에 익숙하고, 호환성이 넓으며, 일상적인 삽관 시술에 임상적으로 정착되어 있기 때문에 여전히 일상적인 구매의 대부분을 차지하고 있습니다. 블레이드 부문 내에서는 특수 용도용 및 비디오 지원 블레이드가 더욱 빠르게 성장하고 있지만, 이들 제품은 여전히 기존 직접 시인형 제품보다 작은 규모의 도입 기반에서 점차 확대되고 있는 단계에 있습니다. 실용적인 관점에서 볼 때, 기술 업그레이드로 인해 핸들에 대한 가치 배분이 점차 늘어나고 있기는 하지만, 후두경 블레이드 및 핸들 시장의 당면한 수익은 여전히 블레이드 교체에 의존하고 있습니다.

후두경 핸들은 2031년까지 연평균 성장률(CAGR) 9.38%를 나타낼 것으로 예측되며, 후두경 블레이드 및 핸들 시장에서 가장 빠르게 성장하는 제품 하위 부문이 될 것입니다. 이러한 성장은 수동적인 배터리 구동형 설계에서 영상 촬영, 연결성 및 보다 광범위한 의료 현장에서의 사용을 지원하는 능동적인 영상 지원 구성으로의 전환과 밀접한 관련이 있습니다. 2025년 9월에 제정된 ISO 7376-2-2025는 비디오 라린고스코프에 관한 보다 공식적인 기술적 프레임워크를 이 분야에 제공함으로써, 조달 심사 시 사양에 대한 불확실성을 줄이는 데 기여하고 있습니다. 2025년 12월에 출시된 앰브사의 “SureSight Mobile”는 긴급 상황이나 예기치 못한 삽관을 염두에 둔, 화면과 핸들이 일체화된 독립형 모델이며, 반면 “SureSight Connect”는 동일한 제품군 내에서 보다 플랫폼 중심의 접근 방식을 구현하고 있습니다. 이는 체계화된 수술실 환경에서는 모니터 연동형 시스템이 계속해서 강세를 유지하는 반면, 응급 현장, 이송 시, 그리고 공간이 제한된 환경에서는 독립형 핸들이 시장 점유율을 확대할 것이라는 양극화되는 미래상을 시사하고 있습니다.

2025년에는 스테인리스 스틸 재질의 블레이드와 핸들이 수요의 55.24%를 차지하며, 이 소재는 후두경 블레이드 및 핸들 시장에서 중심적인 위치를 유지했습니다. 병원이 여전히 스테인리스를 신뢰하는 이유는 높은 비틀림 강성, 신뢰할 수 있는 치수 안정성, 오토클레이브를 통한 반복적인 멸균에 대한 내성, 그리고 검증된 광섬유 결합 성능을 갖추고 있기 때문입니다. 이러한 특성은 처리 능력이 뛰어난 수술실이나 재사용 빈도가 높은 중환자실 환경에서 여전히 가장 중요하게 여겨지고 있으며, 안정적인 임상 조작감과 내구성이 뛰어난 구조는 임상의에게 필수적입니다. 반면, 플라스틱이나 폴리머로 만든 제품은 일회용 조달과 밀접한 관련이 있으며, 긴 수명보다는 단위당 비용이 저렴하고 폐기하기 쉬운 점이 중시됩니다. 이러한 차이로 인해, 재사용을 전제로 하는 환경에서는 강재가 여전히 표준적인 선택지로 남아 있는 반면, 환자 회전율이나 물류 간소화를 우선시하는 시설에서는 폴리머가 실용적인 선택지로 남아 있습니다.

하이브리드 및 복합재료 시스템은 2031년까지 연평균 성장률(CAGR) 8.52%로 확대될 것으로 예상되며, 이는 후두경 블레이드 및 핸들 시장에서 가장 빠르게 성장하는 재료 부문이 될 것입니다. 그 매력은 경량화, 인체공학적 가능성의 향상, 그리고 구조적 성능을 전혀 희생하지 않으면서도 일회용 형태에 대응할 수 있는 능력의 조합에 있습니다. HEINE사의 “XP"일회용 블레이드 시리즈는 재사용 가능한 스테인리스 스틸 제품의 형태를 비틀림 강성이 높은 폴리머 복합재로 재현함으로써, 공급업체들이 성능 격차를 줄이려 하고 있음을 보여줍니다. Ambu사가 SureSight의 핸들과 블레이드에 2세대 바이오플라스틱 원료로의 전환을 추진하고 있는 것은 또 다른 관점에서 지속가능성을 더하는 것이며, 병원 입찰에서 환경 기준의 중요성이 높아지고 있는 가운데 이는 중요한 의미를 지닙니다. 또한, 중국의 비디오 후두경에 관한 T/CITS 370-2025 그룹 규격 역시 현지에서 성능에 대한 기대치를 형성하는 한 요인이 되고 있습니다. 이는 향후 재료 선정이 세계 및 국내의 규정 준수 기준 모두에 비추어 평가되는 비중이 점점 더 커질 것이기 때문에 중요한 점입니다. 이러한 변화들을 종합해 보면, 복합재료가 강재를 전면적으로 대체하는 것은 아니지만, 향후 제품 포트폴리오에서 핵심적인 위치를 차지해 가고 있음을 시사합니다.

지역별 분석

2025년, 북미는 후두경 블레이드 및 핸들 시장 규모의 39.22%를 차지하며, 계속해서 가장 규모가 큰 지역 기여자로서의 위상을 유지했습니다. 이 지역은 수술 건수가 많고, 성숙한 응급의료 인프라를 갖추고 있으며, 병원과 응급의료 현장에서 안정적인 환자 유입이 이루어지는 이점을 누리고 있습니다. 박스터(Baxter)사가 2026년 3월 31일부로 웰치-알린(Welch Allyn)사의 모든 후두경 블레이드 및 핸들 제품 라인의 판매를 중단하기로 결정함에 따라, 의료기관용 시장에서 단기적인 공백이 발생했으며, 현재 다른 공급업체들이 이를 두고 경쟁을 벌이고 있습니다. 유럽은 여전히 2위 지역이며, 독일, 프랑스, 영국, 이탈리아가 후두경 블레이드 및 핸들 시장의 주요 수요 거점으로 자리 잡고 있습니다. 앰브사는 2026년 4월, SureSight 제품 포트폴리오 전체에 대해 CE 마크를 획득했습니다. 이로 인해 유럽 전역에서의 단계적 확대가 가속화되면서, 기존 재사용 가능 기기 시장 지위에 대한 압박이 커지고 있습니다. 또한, 유럽의 공공 조달에서는 환경 규정 준수가 더욱 중요시되고 있어, 재활용 가능한 소재를 사용하거나 회수 경로를 입증할 수 있는 공급업체가 유리한 입장에 있습니다. 독일에서는 특히 일회용 후두경의 조달이 활발한데, 이는 급성기 의료 현장에서 감염 관리와 운영상의 편의성을 양립시키려는 해당 지역의 태도를 반영하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.15%로 확대될 것으로 예상되며, 후두경 블레이드 및 핸들 시장에서 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 중국에서는 병원의 현대화가 성장을 주도하고 있으며, 각 성의 병원 조달 동향을 살펴보면 기존 비디오 핸들에 호환되는 일회용 블레이드의 구매가 점점 더 증가하고 있습니다. 이러한 경향은 초기 도입 단계에서 블레이드의 반복 수요로 전환되고 있음을 시사하며, 지속적인 수익 확보로 이어지기 때문에 중요합니다. 인도에서는 고위험 의료기기 분야에 새로 진입하는 기업들에게 여전히 승인 획득까지의 과정이 험난한 상황이지만, 주요 공립병원 네트워크와 의과대학 시스템은 수술 건수가 많기 때문에 시장을 상업적으로 매력적인 곳으로 만들고 있습니다. 일본은 고령화 사회로 인해 1인당 삽관 수요가 높은 수준을 유지하고 있으며, 최초 구매뿐만 아니라 더 선명한 영상을 얻을 수 있는 시스템으로의 교체 수요도 뒷받침되고 있어, 다른 성장 양상을 보이고 있습니다.

중동 및 아프리카 및 남미는 합쳐서 기타 지역 수요를 차지하고 있지만, 성장률은 인프라의 질이나 조달 능력에 따라 크게 달라집니다. GCC 국가들에서는 병원의 수용 능력을 확대하고 있으며, 특히 비디오 지원 시스템이 임상적 가치와 브랜드 가치를 강력하게 지닌 민간 의료 네트워크에서 고급 국제 브랜드를 선호하는 경향이 지속되고 있습니다. 남아프리카의 민간 병원 그룹과 브라질의 3차 의료 센터는 각 해당 지역에서 여전히 가장 가치 있는 주요 고객으로 남아 있지만, 다른 많은 고객들은 일회용 또는 저가형 블레이드와 결합된 재사용 가능한 광섬유 핸들에 여전히 의존하고 있습니다. 또한, 이러한 지역에서의 응급의료서비스(EMS) 확대 역시, 본격적인 병원 환경 이외의 장소에서도 신속하게 전개할 수 있는 견고하고 휴대 가능하며 상온 보관이 가능한 핸들형 제품에 대한 수요를 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the laryngoscope blades and handles market size is expected to increase from USD 506.19 million in 2025 to USD 544.26 million in 2026 and reach USD 782.08 million by 2031, growing at a CAGR of 7.52% over 2026-2031.

This report is Segmented by Product Type (Blades [Macintosh Blades and More], Handles [Standard Handles and More]), Material (Stainless Steel, Plastic and Polymer-Based, Hybrid and Composite), Usage (Adult, Pediatric, Neonatal and Difficult Airway), End User (Hospitals, Specialty Clinics, and More), and Geography (North America and More). Market Forecasts are Provided in Terms of Value (USD).

Global Laryngoscope Blades and Handles Market Trends and Insights

Rising Airway Management Demand From Respiratory Disease Burden

The laryngoscope blades and handles market is seeing durable procedure support from the rising burden of chronic respiratory disease across both developed and emerging care systems. WHO and the European Respiratory Society reported in June 2025 that 81.7 million people in the WHO European Region were living with chronic respiratory diseases, with 6.8 million new diagnoses each year and COPD accounting for 80% of related deaths. The same publication also placed the cost of underdiagnosis above USD 20 billion annually, which points to a large pool of patients who may still present late and require acute airway support rather than early outpatient management. In South-East Asia, the burden is even more important for future volume because WHO reported in 2025 that chronic respiratory diseases were responsible for nearly 12% of all deaths, which keeps emergency and critical care intubation demand structurally elevated in systems that still have uneven ICU access. Much of that installed base still relies on conventional reusable stainless-steel systems, so the first major upgrade path is likely to come from lower-cost video platforms rather than premium monitor-heavy solutions. The projected 23% global rise in COPD between 2020 and 2050 extends this demand base for many years and gives the laryngoscope blades and handles market a rare level of long-range clinical visibility.

Shift Toward Single-Use Blades to Reduce Cross-Contamination Risk

The laryngoscope blades and handles market is moving toward single-use procurement because contamination concerns are no longer limited to the blade surface alone. Flexicare reported clinical data in 2025 showing that 86% of reusable laryngoscope handles remained bacterially positive after standard wipe disinfection, while APSF noted that single-use equipment removes the operational complexity tied to reprocessing steps. This matters because hospital buyers are now treating the handle as a contamination vector with equal importance, which changes a category that was once dominated by reusable hardware. The migration of disposability from blades into handles is changing the revenue mix, since the premium is shifting from a one-time capital item toward recurring procedure-linked consumption. Ambu's June 2026 expansion of the Recircle program to include bioplastic SureSight blades shows that suppliers are now trying to solve infection control and sustainability together rather than forcing customers to choose one over the other. That combined value proposition is likely to matter more in European public tenders, where environmental scoring is starting to influence award outcomes alongside traditional clinical and cost criteria.

High Acquisition Cost of Advanced Video and Fiber-Optic Systems

The laryngoscope blades and handles market still faces a clear adoption limit in hospitals that cannot absorb the upfront cost of advanced video and fiber-optic systems. The gap between a basic reusable fiber-optic handle and a proprietary video-enabled setup remains large, and the recurring cost of single-use video blades at USD 15 to USD 80 per procedure adds pressure for facilities that work under strict consumables budgets. This cost barrier matters even when the clinical case for video is strong, because many procurement teams still evaluate airway devices through immediate payback rather than broad care quality metrics. Suppliers are responding with more modular formats that reduce per-case expense and lower entry barriers without removing the benefits of visualization. Verathon's ClearFit design is one example of that response, because it spreads the video component across multiple single-use cover options and supports a more flexible cost profile for fast-turn care settings. Until similar price-performance models become common, the laryngoscope blades and handles market will continue to see slower conversion in South America, the Middle East and Africa, and non-urban Asia-Pacific accounts.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Video-Assisted and Fiber-Optic Systems in Difficult Airway Care

- Expansion of Emergency, Ambulatory, and Pre-Hospital Airway Workflows

- Reprocessing Burden and Sterilization Compliance for Reusable Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laryngoscope blades held 65.31% of the laryngoscope blades and handles market share in 2025, which shows that volume is still centered on the consumable side of the category. This position reflects the global installed base of direct laryngoscopy workflows across operating rooms, emergency departments, and intensive care units. Macintosh and Miller designs continue to account for most routine purchasing because they are familiar, broadly compatible, and clinically embedded in everyday intubation practice. Specialized and video-compatible blades are growing faster inside the blades category, but they are still building from a smaller installed base than conventional direct-view products. In practical terms, the laryngoscope blades and handles market still depends on blade turnover for immediate revenue, even as technology upgrades start shifting more value into handles.

Laryngoscope handles are forecast to grow at a 9.38% CAGR through 2031, which makes them the fastest-growing product sub-segment in the laryngoscope blades and handles market. That growth is tied to the move away from passive battery-operated designs and toward active video-enabled configurations that support imaging, connectivity, and broader care-setting use. ISO 7376-2-2025 gave the category a more formal technical framework for video laryngoscopes in September 2025, which helps reduce specification uncertainty during procurement reviews. Ambu's SureSight Mobile, introduced in December 2025, reflects the standalone path with an integrated screen-and-handle format meant for emergency and unplanned intubation, while SureSight Connect represents a more platform-led approach within the same product family. This points to a split future where monitor-linked systems remain strong in structured operating room environments, while self-contained handles gain share in emergency, transport, and space-constrained settings.

Stainless steel blades and handles commanded 55.24% of demand in 2025, which kept this material base at the center of the laryngoscope blades and handles market. Hospitals continue to rely on steel because it offers high torsional stiffness, dependable dimensional stability, repeated autoclave compatibility, and established fiber-optic coupling performance. Those qualities still matter most in high-throughput operating rooms and reuse-heavy ICU settings, where a stable clinical feel and durable construction remain important to clinicians. Plastic and polymer designs, by contrast, are more closely tied to single-use procurement where lower per-unit cost and easy disposal matter more than long service life. This split means steel remains the default in settings built around reuse, while polymers remain the practical option in facilities that prioritize turnover speed and simpler logistics.

Hybrid and composite material systems are projected to advance at an 8.52% CAGR through 2031, which makes them the fastest-moving material category in the laryngoscope blades and handles market. Their appeal comes from a combination of lower weight, better ergonomic possibilities, and the ability to support single-use formats without fully giving up structural performance. HEINE's XP disposable blade series shows how suppliers are trying to narrow the performance gap by matching the geometry of reusable stainless-steel products in torsionally stiff polymer composite form. Ambu's shift into second-generation bioplastic feedstock across SureSight handles and blades adds a separate sustainability angle, which matters as environmental filters gain weight in hospital tenders. China's T/CITS 370-2025 group standard for video laryngoscopes also helps shape local performance expectations, which is important because material choices will increasingly be judged against both global and domestic compliance benchmarks. Taken together, these changes suggest that composites are not replacing steel across the board, but they are becoming central to the forward product portfolio.

Complete Report Scope:

- By Product Type

- Blades

- Macintosh Blades

- Miller Blades

- Straight Blades

- Specialized and Video-Compatible Blades

- Handles

- Standard Handles

- Reusable Handles

- Disposable Handles

- Video-Enabled Handles

- Blades

- By Material

- Stainless Steel Blades and Handles

- Plastic and Polymer-Based Blades and Handles

- Hybrid and Composite Material Systems

- By Usage

- Adult Use

- Pediatric Use

- Neonatal and Difficult Airway Use

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Emergency Medical Services

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 39.22% share of the laryngoscope blades and handles market size in 2025, which kept it as the largest regional contributor. The region benefits from high surgical volumes, mature critical care infrastructure, and consistent replacement demand across hospital and emergency care settings. Baxter's decision to discontinue all Welch Allyn laryngoscope blade and handle lines, effective March 31, 2026, created a near-term opening in institutional accounts that other suppliers are now contesting. Europe remained the second-largest region, with Germany, France, the UK, and Italy acting as the main volume centers for the laryngoscope blades and handles market. Ambu received CE Mark for its full SureSight portfolio in April 2026, which supports a phased rollout across Europe and increases pressure on legacy reusable-device positions. European public tenders are also giving more weight to environmental compliance, which favors suppliers that can document recyclable materials or take-back pathways. Germany remains especially active in single-use laryngoscope procurement, which reflects the region's willingness to pair infection control with operational convenience in acute care pathways.

Asia-Pacific is forecast to expand at a 9.15% CAGR through 2031, which makes it the fastest-growing regional block in the laryngoscope blades and handles market. China is pushing growth through hospital modernization, and procurement activity across provincial hospitals shows that compatible single-use blades are increasingly being bought against an existing base of video handles. That pattern matters because it signals a move from initial installation into repeat blade demand, which is more supportive of recurring revenue. India still presents a longer registration path for new entrants in higher-risk devices, but major public hospital networks and medical college systems keep the market commercially attractive because of their procedure volume. Japan adds a different growth profile, since its aging population sustains high per-capita intubation need and supports replacement demand for better-visualization systems rather than only first-time purchases.

The Middle East and Africa and South America together account for the remaining regional demand, but growth varies widely by infrastructure quality and procurement capacity. GCC countries are expanding hospital capacity and continue to favor premium international brands, especially in private care networks where video-assisted systems carry strong clinical and brand value. South Africa's private hospital groups and Brazil's tertiary care centers remain the highest-value anchors in their respective sub-regions, while many other accounts still rely on reusable fiber-optic handles paired with disposable or lower-cost blades. EMS expansion across these regions is also supporting demand for rugged, portable, and shelf-stable handle configurations that can be deployed quickly outside a full hospital environment.

- Ambu

- Dahlhausen Medical

- Flexicare Medical

- Hartwell Medical LLC

- HEINE Optotechnik GmbH and Co. KG

- HENKE-SASS WOLF GmbH

- Karl Storz

- Medline Industries

- Medtronic

- Olympus

- Penlon Limited

- PROACT Medical Ltd

- RICHARD WOLF GmbH

- Rudolf Riester

- Smiths Group

- SunMed LLC

- Teleflex

- Verathon

- Vyaire Medical

- Vygon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Airway Management Demand From Respiratory Disease Burden

- 4.2.2 Shift Toward Single-Use Blades to Reduce Cross-Contamination Risk

- 4.2.3 Adoption of Video-Assisted and Fiber-Optic Systems in Difficult Airway Care

- 4.2.4 Expansion of Emergency, Ambulatory, and Pre-Hospital Airway Workflows

- 4.2.5 Under-Operative Preference for Low-Fog, High-Visibility Blade Systems in High-Throughput Settings

- 4.2.6 Rising Demand for Ergonomic Handle Architectures That Reduce Clinician Fatigue

- 4.3 Market Restraints

- 4.3.1 High Acquisition Cost of Advanced Video and Fiber-Optic Systems

- 4.3.2 Reprocessing Burden and Sterilization Compliance for Reusable Systems

- 4.3.3 Training Dependency and User Resistance to Advanced Intubation Platforms

- 4.3.4 Environmental Pressure on Disposable Plastic and Mixed-Material Device Waste

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Blades

- 5.1.1.1 Macintosh Blades

- 5.1.1.2 Miller Blades

- 5.1.1.3 Straight Blades

- 5.1.1.4 Specialized and Video-Compatible Blades

- 5.1.2 Handles

- 5.1.2.1 Standard Handles

- 5.1.2.2 Reusable Handles

- 5.1.2.3 Disposable Handles

- 5.1.2.4 Video-Enabled Handles

- 5.1.1 Blades

- 5.2 By Material

- 5.2.1 Stainless Steel Blades and Handles

- 5.2.2 Plastic and Polymer-Based Blades and Handles

- 5.2.3 Hybrid and Composite Material Systems

- 5.3 By Usage

- 5.3.1 Adult Use

- 5.3.2 Pediatric Use

- 5.3.3 Neonatal and Difficult Airway Use

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Emergency Medical Services

- 5.4.4 Specialty Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Ambu A/S

- 6.3.2 Dahlhausen Medical

- 6.3.3 Flexicare Medical Limited

- 6.3.4 Hartwell Medical LLC

- 6.3.5 HEINE Optotechnik GmbH and Co. KG

- 6.3.6 HENKE-SASS WOLF GmbH

- 6.3.7 KARL STORZ SE and Co. KG

- 6.3.8 Medline Industries, Inc.

- 6.3.9 Medtronic plc

- 6.3.10 Olympus Corporation

- 6.3.11 Penlon Limited

- 6.3.12 PROACT Medical Ltd

- 6.3.13 RICHARD WOLF GmbH

- 6.3.14 Rudolf Riester GmbH

- 6.3.15 Smiths Group plc

- 6.3.16 SunMed LLC

- 6.3.17 Teleflex Incorporated

- 6.3.18 Verathon Inc.

- 6.3.19 Vyaire Medical, Inc.

- 6.3.20 Vygon SA

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment