|

시장보고서

상품코드

2073199

스마트 망막 임플란트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Smart Retinal Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

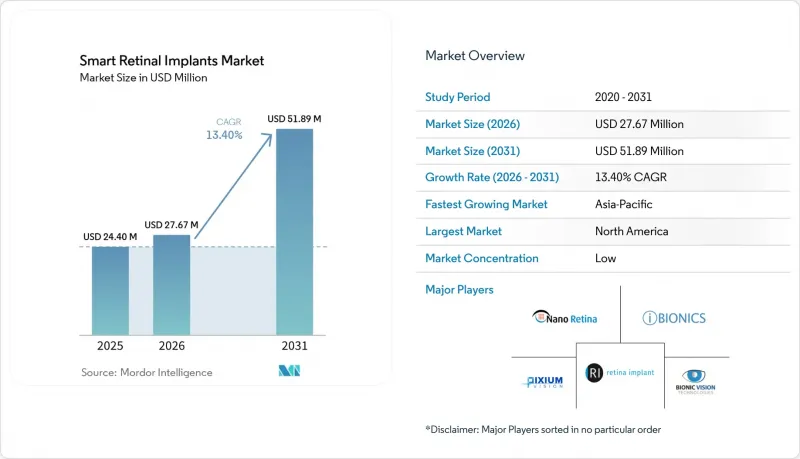

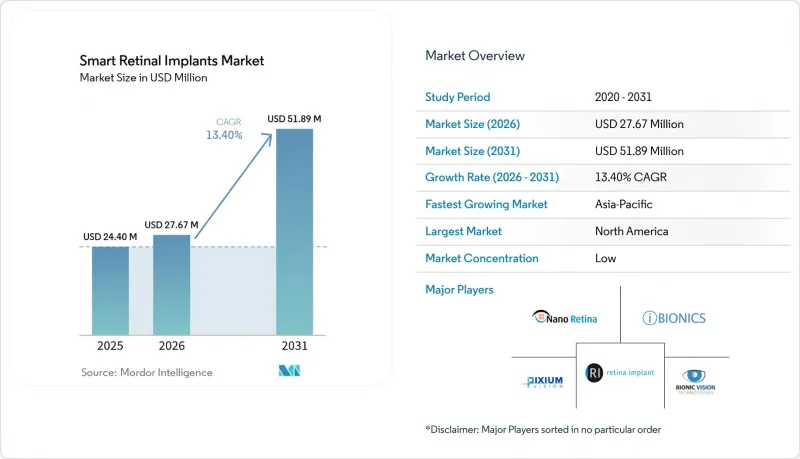

Mordor Intelligence에 의하면, 스마트 망막 임플란트 시장 규모는 2025년 2,440만 달러에서 2026년에는 2,767만 달러로 확대되어 2026년부터 2031년까지 CAGR 13.40%로 성장을 지속하여, 2031년에는 5,189만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(망막 위, 망막 아래 등), 플랫폼(유선 시스템 등), 구성 요소(어레이, 카메라 등), 소재(임플란트 어레이 등), 질환(색소성 망막염 등), 최종 사용자(병원, 클리닉 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 스마트 망막 임플란트 시장 동향 및 인사이트

시력 회복에 대한 임상적 유효성에 대한 근거가 더욱 확고해지고 있습니다.

PRIMAvera 임상시험은 스마트 망막 임플란트 시장의 임상적 기반을 대폭 강화했습니다. 2025년 10월에 발표된 이 임상시험에서 지리적 위축증 환자의 80%가 12개월 후 유의미한 시력 개선을 보인 것으로 입증되었습니다. 이러한 변화로 인해, 기술적 가능성이 아닌 실제 환자의 예후에 기반한 평가가 가능해졌습니다. 또한, 이러한 결과로 인해 유럽에서는 논의가 “실현 가능성”에서 “승인” 및 “시장 출시 준비”로 발전하고 있으며, Science Corporation은 2025년에 CE 마크 인증을 신청했습니다. 또한, 2026년 1월 Cortigent사가 발표한 ‘Orion” 시험의 6년간 실시 가능성 데이터에 따르면, 전극 손실이 4% 미만으로 유지되었으며, 피험자 6명 전원에서 시기능 개선이 확인됨에 따라, 이 시장은 여러 기술적 접근 방식에 있어 그 유효성이 입증되고 있습니다. 이러한 임상적 근거의 다양화로 인해 외과의사, 규제 당국, 투자자들 사이에서 신뢰도가 높아지고 있습니다.

지리적 위축 및 색소성 망막염 환자군의 확대

스마트 망막 임플란트 시장은 특히 지리적 위축이나 색소성 망막염과 같이 지속적인 시력 회복을 위한 선택지가 여전히 제한적인 질환 분야에서 대규모 환자 기반의 혜택을 누리고 있습니다. 지리적 위축은 전 세계적으로 수백만 명에게 영향을 미치고 있으며, 또한 색소성 망막염도 150만에서 200만 명에게 영향을 미치고 있기 때문에 단계적인 상업적 전개라 하더라도 지속적인 수요가 예상됩니다. PRIMA 플랫폼은 망막색소변성증 및 스타가르트병과 관련된 시력 상실을 포함한 광수용체 변성을 앓고 있는 환자를 대상으로 한 새로운 임상시험을 통해 적용 범위를 확대했습니다. 2025년 9월에 시작된 일본의 STS 3상 프로그램은 아시아에서 망막 임플란트 개발에 대한 기관 차원의 지원이 확대되고 있음을 보여주고 있으며, 이는 향후 시장 확대에 있어 매우 중요합니다. 망막색소변성증에 대한 광유전학 연구는 진전되고 있지만, 질환의 진행 단계나 망막 구조에 따른 다양한 임상적 요구가 존재하기 때문에 임플란트에 대한 수요는 앞으로도 지속될 것으로 예측됩니다.

시력 개선에 대한 제한적인 효과와 수술 및 기기의 복잡성

스마트 망막 임플란트 시장은 임상 측면에서 눈부신 진전을 이루고 있지만, 이러한 개선과 일상적인 시각 기능에의 적용 사이에는 여전히 간극이 존재합니다. PRIMAvera 임상시험에서는 시력 개선이 관찰되었으나, 많은 환자들은 여전히 독서, 얼굴 인식, 이동 등의 활동에서 자립적인 생활을 영위하지 못하고 있었습니다. 이 임상시험에서는 38명의 참가자 중 26건의 중대한 이상반응이 보고되었으며, 그중 95%는 2개월 이내에 해소되었으나, 이는 더 광범위한 보급에 있어 해결해야 할 과제를 여실히 드러내고 있습니다. 또한, 이식 수술에는 전문적인 유리체망막외과 또는 뇌신경외과 지식이 필요하지만, 이러한 전문의를 충분히 확보하지 못하고 있어 임상시험에서 일상적인 의료 현장으로의 전환이 지연되고 있습니다.

부문별 분석

2025년, 망막하 임플란트는 스마트 망막 임플란트 시장의 54.66%를 차지하며 선두 자리를 확고히 다졌습니다. 그 장점은 망막 아래에 배치됨으로써 손상되지 않은 양극 세포를 직접 자극할 수 있으며, 많은 표면 부착형 설계에 비해 뛰어난 시각적 충실도를 제공할 수 있다는 점에 있습니다. 이 부문에서는 PRIMA 시스템이 두각을 나타내고 있으며, 2025년 10월 발표된 논문을 통해 망막하 기술의 임상적 신뢰성이 한층 더 높아졌습니다. 그 결과, 시장에서는 망막하 시스템이 지리적 위축 및 관련 퇴행성 질환 환자를 치료하기 위한 가장 유망한 수단으로 간주되고 있습니다.

망막 위 시스템은 이 분야의 초기 임상 역사에서 매우 중요한 역할을 수행했으나, 더 이상 새로운 개발 방향을 주도하는 존재는 아닙니다. 한편, 초맥락막 임플란트는 위험이 낮은 외과적 대안으로 주목받고 있으며, 2025년 실현 가능성 조사에서 보고된 2세대 44채널 장치는 2.7년이 지난 후에도 97%의 전극 기능성을 유지하고 있는 것으로 나타났습니다. 한편, 피질형 시각 보철 장치는 급속히 부상하고 있으며, 2031년까지 연평균 성장률(CAGR) 14.20%를 나타낼 것으로 전망됩니다. 이러한 폭넓은 매력은 시신경 손상이나 진행된 망막 질환 등, 망막 임플란트가 적합하지 않은 환자들에게도 적용할 수 있다는 점에 있습니다.

2025년에는 유선 시스템이 매출의 61.53%를 차지했는데, 이는 초기 임플란트 프로그램과 설계상의 선택이 여전히 큰 영향을 미치고 있음을 보여줍니다. 그러나 이러한 우위는 전략적인 것이라기보다는 역사적 배경에 기인한 것입니다. 스마트 망막 임플란트 시장의 최근 발전 중 상당수는 무선 및 하이브리드 시스템으로 초점을 옮기고 있습니다. 유선 아키텍처는 익숙한 설계 기법과 안정적인 전송을 제공하지만, 케이블 및 외부 하드웨어에 대한 의존성으로 인해 수술이 복잡해지고 환자의 편의성이 저하되며, 장기적으로는 MRI와의 호환성 문제가 발생합니다. 그 결과, 유선 시스템은 단기적으로는 여전히 중요하지만, 미래 설계의 주도권을 쥐고 있는 것은 아닙니다.

무선 시스템은 2031년까지 연평균 성장률(CAGR) 15.15%를 나타낼 것으로 예측되며, 스마트 망막 임플란트 분야에서 가장 빠르게 성장하고 있는 플랫폼으로 자리매김하고 있습니다. PRIMA 시스템은 이러한 추세를 상징하는 것으로, 전력 및 데이터 전송에 근적외선을 활용함으로써 경피 케이블을 필요로 하지 않습니다. 이러한 혁신을 통해 환자의 경험과 수술의 용이성이 모두 크게 향상될 것입니다. 또한, 2026년 기술 연구에서는 무선 기능을 저해하지 않으면서도 화소 크기를 축소할 수 있는 태양광 발전 어레이의 가능성이 강조되고 있으며, 이는 해당 플랫폼의 장기적인 전망을 뒷받침하고 있습니다.

지역별 분석

2025년, 북미는 스마트 망막 임플란트 시장에서 40.65%의 점유율을 차지하며 시장을 주도했습니다. 미국은 망막 및 대뇌피질용 기기 관련 두 프로그램을 추진하는 강력한 전문의 체계와 지원적인 규제 절차를 바탕으로 이러한 성장을 주도했습니다. 사이언스 코퍼레이션은 2025년, 미국 규제 당국을 통해 PRIMA 프로그램을 추진할 예정이며, 한편 코르티젠트사는 2026년 1월, “획기적인 장치”로 지정된 Orion 프로그램에 관한 6년간의 연구 데이터를 발표했습니다. 이 지역에는 임플란트 시술을 수행하는 병원, 의료기기 개발 기업, 안과 연구센터가 밀집해 있어, 이는 임상시험 피험자 모집과 상용화를 위한 준비를 한층 더 뒷받침하고 있습니다.

유럽은 스마트 망막 임플란트 시장에서 여전히 2위의 규모를 자랑하는 거점입니다. 해당 지역은 PRIMAvera 프로그램에서 중요한 역할을 수행하고 있으며, 2025년 10월 논문 발표를 통해 유럽 규제 당국을 위한 증거 자료가 강화되어 CE 마크 심사가 진전을 이루었습니다. 독일, 프랑스, 영국은 망막 외과 분야의 전문성과 학술적 임상시험 참여를 모두 갖추고 있다는 점에서 두드러집니다. 또한, 유럽은 중요한 시장 진출 지역이기도 합니다. 승인이 이루어지면 상환까지의 기간은 길어지겠지만, 체계적인 상용화 경로를 확립할 가능성이 있기 때문입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.44%를 나타낼 것으로 예측되며, 스마트 망막 임플란트 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 이러한 성장을 주도하고 있으며, 고령화가 진행되는 한편, 초맥락막 시스템과 광시야 티플렛 임플란트 기술이 발전하고 있습니다. 오사카 대학은 2025년 9월에 STS의 3상 임상시험을 시작할 예정이며, 한편 도호쿠 대학은 160도의 시야를 목표로 정부 지원을 받아 3D 적층형 인공망막 개발을 추진하고 있습니다. 또한, 이 지역은 호주의 초맥락막 보철 프로그램의 혜택을 받고 있어 혁신의 기반을 확대되고 있습니다. 남미, 중동 및 아프리카는 현재 수익 기여도가 낮은 편이지만, 망막 질환 유병률 증가와 안과 의료 인프라의 개선에 따라 성장이 예상됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the smart retinal implants market size is expected to grow from USD 24.40 million in 2025 to USD 27.67 million in 2026 and is forecast to reach USD 51.89 million by 2031 at 13.40% CAGR over 2026-2031.

This report is Segmented by Product Type (Epiretinal, Subretinal, and More), Platform (Wired Systems, and More), Component (Array, Camera, and More), Material (Implant Array, and More), Disease (Retinitis Pigmentosa, and More), End User (Hospitals, Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Retinal Implants Market Trends and Insights

Rising Clinical Validation for Vision Restoration

The PRIMAvera study has significantly strengthened the clinical foundation of the smart retinal implants market. Published in October 2025, the trial demonstrated that 80% of patients with geographic atrophy achieved meaningful visual acuity improvements after 12 months. This shift enables evaluations based on real patient outcomes rather than engineering potential. Furthermore, these results have advanced discussions from feasibility to approval and market readiness in Europe, where Science Corporation submitted its CE Mark application in 2025. The market is also gaining validation across multiple technical paths, as Cortigent's 6-year Orion feasibility data from January 2026 showed less than 4% electrode loss and improved visual function in all 6 subjects. This diversification of clinical evidence has increased confidence among surgeons, regulators, and investors.

Expanding Addressable Population With Geographic Atrophy and Retinitis Pigmentosa

The smart retinal implants market benefits from a large patient base, particularly in geographic atrophy and retinitis pigmentosa, where durable vision restoration options remain limited. Geographic atrophy affects millions globally, while retinitis pigmentosa impacts an additional 1.5 to 2 million people, ensuring sustained demand even with a gradual commercial rollout. The PRIMA platform has expanded its focus through a new clinical study targeting patients with photoreceptor degeneration, including retinitis pigmentosa and Stargardt-related vision loss. Japan's STS Phase 3 program, launched in September 2025, highlights growing institutional support for retinal implant development in Asia, which is critical for future market expansion. While optogenetics is advancing in retinitis pigmentosa, the diverse clinical needs across disease stages and retinal structures ensure continued demand for implants.

Limited Visual Acuity Gains Versus Surgical and Device Complexity

The smart retinal implants market has achieved significant clinical advancements, but a gap remains between these improvements and their application in daily visual functions. The PRIMAvera study demonstrated progress in visual acuity; however, many patients still could not achieve independence in tasks like reading, face recognition, or navigation. The trial reported 26 serious adverse events among 38 participants, with 95% resolving within two months, highlighting challenges in broader adoption. Additionally, the implantation process requires specialized vitreoretinal or neurosurgical expertise, which is not widely available, slowing the transition from clinical trials to routine care.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of Miniaturized Electronics and Wireless Power Transfer

- Precision-Targeted Retinal Stimulation and AI-Assisted Scene Encoding

- High Procedure Cost and Unclear Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, subretinal implants captured 54.66% of the smart retinal implants market, solidifying their top position. Their advantage lies in their placement beneath the retina, enabling direct stimulation of intact bipolar cells and offering superior visual fidelity compared to many surface-mounted designs. The PRIMA system stands out in this segment, with its October 2025 publication bolstering subretinal technology's clinical credibility. As a result, the market views subretinal systems as the most promising avenue for treating patients with geographic atrophy and related degenerations.

While epiretinal systems played a pivotal role in the field's early clinical history, they no longer steer the course of new developments. Suprachoroidal implants are gaining traction as a less risky surgical alternative, with a second-generation 44-channel device boasting 97% electrode functionality after 2.7 years, as reported in a 2025 feasibility study. Meanwhile, cortical visual prostheses are on a rapid ascent, projected to grow at a 14.20% CAGR through 2031. Their broader appeal stems from their ability to cater to patients unsuitable for retinal implants, including those with optic nerve damage or advanced retinal diseases.

In 2025, wired systems commanded 61.53% of the revenue, a testament to the enduring influence of earlier implant programs and design choices. However, this dominance is more historical than strategic. Most recent advancements in the smart retinal implants market have pivoted towards wireless and hybrid systems. While wired architectures offer familiar engineering pathways and stable transmission, their reliance on cables and external hardware complicates surgery, patient comfort, and MRI compatibility over time. Consequently, while the wired base remains relevant in the near term, it isn't setting the pace for future designs.

Wireless systems are on a trajectory to grow at a 15.15% CAGR through 2031, marking them as the fastest-growing platform in the smart retinal implants arena. The PRIMA system exemplifies this trend, utilizing near-infrared light for power and data transmission, thereby eliminating the need for a transcutaneous cable. This innovation significantly enhances both patient experience and surgical ease. Furthermore, a 2026 technical study highlighted the potential of photovoltaic arrays to downsize pixels without compromising wireless functionality, bolstering the platform's long-term prospects.

Complete Report Scope:

- By Product Type

- Epiretinal Implants

- Subretinal Implants

- Suprachoroidal Implants

- Cortical Visual Prostheses

- By Implant Platform

- Wired Systems

- Wireless Systems

- Hybrid Systems

- By Component

- Implant Array

- External Glasses and Camera System

- Processing Unit

- Power Transmission Module

- Surgical Accessories and Tools

- By Material

- Biocompatible Metals (Platinum, Titanium)

- Polymers (Polyimide, Silicone)

- Ceramics

- Nanomaterials (Graphene, Carbon Nanotubes)

- Hybrid Materials

- By Disease Indication

- Retinitis Pigmentosa

- Geographic Atrophy Due to Age-Related Macular Degeneration

- Other Degenerative Retinal Disorders

- By End User

- Hospitals and Ophthalmic Surgery Centers

- Specialty Eye Clinics

- Academic and Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America dominated the smart retinal implants market, holding a 40.65% share. The United States led this growth due to its strong specialist capacity and supportive regulatory pathways, which advanced both retinal and cortical device programs. Science Corporation progressed its PRIMA program through U.S. regulatory channels in 2025, while Cortigent presented 6-year study data for its Orion program under Breakthrough Device status in January 2026. The region's concentrated network of implanting hospitals, device developers, and ophthalmic research centers further supports clinical enrollment and commercial readiness.

Europe remains the second-largest hub in the smart retinal implants market. The region played a key role in the PRIMAvera program, with an October 2025 publication strengthening the evidence package for European regulators and advancing the CE Mark review. Germany, France, and the UK stand out for their combination of specialist retinal surgery and academic trial participation. Europe is also a critical launch region, as successful approval could establish a structured commercial pathway, despite slower reimbursement timelines.

Asia-Pacific is projected to grow at a 15.44% CAGR through 2031, making it the fastest-growing region in the smart retinal implants market. Japan drives this growth with its aging population and advancements in suprachoroidal systems and wide-field chiplet implants. Osaka University initiated its STS Phase 3 trial in September 2025, while Tohoku University is advancing a government-backed 3D laminated artificial retina targeting a 160-degree visual field. The region also benefits from Australia's suprachoroidal prosthesis program, expanding its innovation base. South America and the Middle East and Africa currently contribute less revenue but are expected to grow as retinal disease prevalence rises and ophthalmic infrastructure improves.

- Bionic Vision Technologies Pty Ltd

- Boston Scientific

- GenSight Biologics SA

- iBionics Inc.

- Intelligent Implants GmbH

- LambdaVision, Inc.

- Nano Retina Ltd.

- Nidek

- Ocumetics Technology Corporation

- Ophthorobotics AG

- Optobionics Corporation

- Pixium Vision SA

- Retina Implant AG

- Science Corporation

- Second Sight Medical Products

- VisionCare Ophthalmic Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Clinical Validation for Vision Restoration

- 4.2.2 Expanding Addressable Population With Geographic Atrophy and Retinitis Pigmentosa

- 4.2.3 Convergence of Miniaturized Electronics and Wireless Power Transfer

- 4.2.4 Post-Implant Rehabilitation and Digital Vision Training Improving Real-World Utility

- 4.2.5 Breakthrough Device and Accelerated Regulatory Pathways Supporting Innovation

- 4.2.6 Precision-Targeted Retinal Stimulation and AI-Assisted Scene Encoding

- 4.3 Market Restraints

- 4.3.1 Limited Visual Acuity Gains Versus Surgical and Device Complexity

- 4.3.2 High Procedure Cost and Unclear Reimbursement Pathways

- 4.3.3 Long-Term Biocompatibility, Packaging, and Hermeticity Risks

- 4.3.4 Small Eligible Patient Pool and Dependence on Specialized Surgical Centers

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Epiretinal Implants

- 5.1.2 Subretinal Implants

- 5.1.3 Suprachoroidal Implants

- 5.1.4 Cortical Visual Prostheses

- 5.2 By Implant Platform

- 5.2.1 Wired Systems

- 5.2.2 Wireless Systems

- 5.2.3 Hybrid Systems

- 5.3 By Component

- 5.3.1 Implant Array

- 5.3.2 External Glasses and Camera System

- 5.3.3 Processing Unit

- 5.3.4 Power Transmission Module

- 5.3.5 Surgical Accessories and Tools

- 5.4 By Material

- 5.4.1 Biocompatible Metals (Platinum, Titanium)

- 5.4.2 Polymers (Polyimide, Silicone)

- 5.4.3 Ceramics

- 5.4.4 Nanomaterials (Graphene, Carbon Nanotubes)

- 5.4.5 Hybrid Materials

- 5.5 By Disease Indication

- 5.5.1 Retinitis Pigmentosa

- 5.5.2 Geographic Atrophy Due to Age-Related Macular Degeneration

- 5.5.3 Other Degenerative Retinal Disorders

- 5.6 By End User

- 5.6.1 Hospitals and Ophthalmic Surgery Centers

- 5.6.2 Specialty Eye Clinics

- 5.6.3 Academic and Research Institutes

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Bionic Vision Technologies Pty Ltd

- 6.3.2 Boston Scientific Corporation

- 6.3.3 GenSight Biologics SA

- 6.3.4 iBionics Inc.

- 6.3.5 Intelligent Implants GmbH

- 6.3.6 LambdaVision, Inc.

- 6.3.7 Nano Retina Ltd.

- 6.3.8 NIDEK CO., LTD.

- 6.3.9 Ocumetics Technology Corporation

- 6.3.10 Ophthorobotics AG

- 6.3.11 Optobionics Corporation

- 6.3.12 Pixium Vision SA

- 6.3.13 Retina Implant AG

- 6.3.14 Science Corporation

- 6.3.15 Second Sight Medical Products, Inc.

- 6.3.16 VisionCare Ophthalmic Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment