|

시장보고서

상품코드

2073204

자궁경부암 진단 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cervical Cancer Diagnostic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

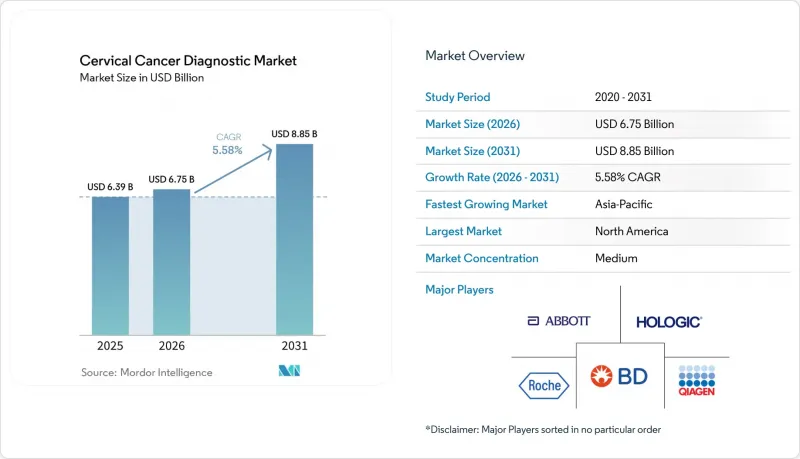

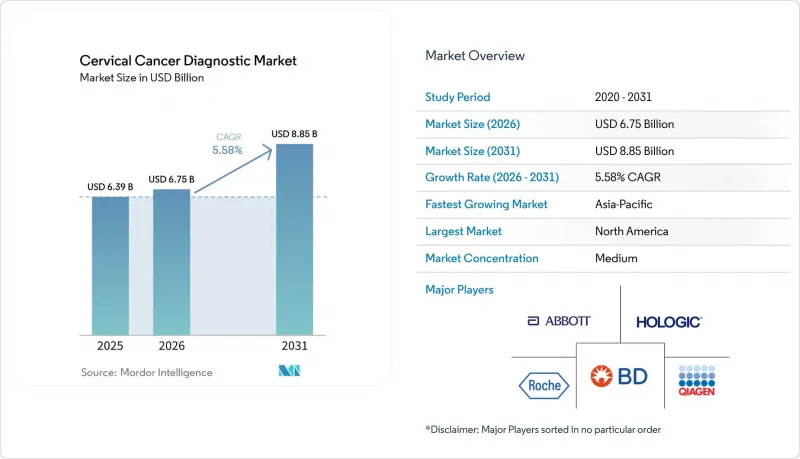

Mordor Intelligence에 의하면, 자궁경부암 진단 시장 규모는 2025년 63억 9,000만 달러, 2026년 67억 5,000만 달러에서 2031년까지 88억 5,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.58%를 나타낼 전망입니다.

본 보고서는 검사 유형(자궁경부 세포진 검사, HPV 검사, 질 확대경 검사, 생검, 기타), 최종 사용자(병원, 전문 클리닉, 진단센터, 암·방사선 치료 센터, 재택 간호), 기술(액체 기반 세포진, 분자진단, 디지털 세포진 및 AI 영상 진단, IHC 및 바이오마커 검사), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예측치는 달러 기준입니다.

전 세계 자궁경부암 진단 시장 동향 및 인사이트

증가하는 자궁경부암의 부담과 여전히 높은 HPV 유병률

자궁경부암 진단 시장은 기술의 포화 상태라기보다는 충족되지 않은 선별 검사 수요에 의해 지탱되고 있습니다. 전 세계 자궁경부암 사례의 99% 이상은 HPV가 원인이며, 모든 의료 시스템에서 선별 검사가 필수적입니다. 자궁경부암으로 인한 사망의 90%라는 놀라운 비율이 저·중소득 국가에서 발생하고 있으며, 이들 국가에서는 선별검사에 대한 접근성이 여전히 제한적이며 지역별로 불균등하게 분포되어 있습니다. 세계보건기구(WHO)는 10억 명 이상의 여성이 한 번도 선별검사를 받은 적이 없습니다고 지적하고 있으며, 이는 체계적인 의료 체계 밖에서 이루어지는 초진 검사에 대한 막대한 수요가 있음을 보여줍니다. 백신 접종 프로그램은 향후 부담을 줄이는 것을 목적으로 하고 있지만, 감염자나 고령 인구에 대한 경과 관찰이 필요하기 때문에 당분간 성인 대상 선별 검사에 대한 수요를 크게 감소시키지는 않을 것입니다. 이러한 상황으로 인해 자궁경부암 진단 시장은 선진국과 신흥 지역 모두에서 충족되지 않은 선별 검사 수요를 충족시켜야 하는 입장에 놓여 있습니다.

HPV 1차 선별검사 및 자가 채취 확대

규제 당국과 의료 기관이 HPV 1차 검사와 자가 채취를 권장하는 가운데, 자궁경부암 진단 시장은 HPV를 중심으로 한 선별 검사 방식으로 전환되고 있습니다. 2026년 2월, 홀로직사는 “Aptima HPV Assay”에 대해 FDA 승인을 획득하고, 그 적용 범위를 파파니콜로 검사, 병용 검사 및 HPV 1차 선별 검사로 확대했습니다. 또한, ASCCP(미국 자궁경부암 검진 전문위원회)는 의료 현장에서 애보트사의 "Alinity", BD사의 “Onclarity”, 로슈사의 “Cobas”의 자가 채취 기능을 승인하여 규정 준수를 강화했습니다. 2026년 4월, ACOG는 30세에서 65세 사이의 평균 위험군 여성에게 3년마다 고위험 HPV 검사를 권장함으로써, 정기 검진 관행에 있어 큰 전환점이 되었습니다. 2027년에 시행될 미국의 정책에 따라, 자가 채취를 통한 검사가 대부분의 건강보험 플랜에서 전액 보장 대상이 되므로, 이러한 추세는 더욱 가속화될 전망입니다. 자가 채취는 그동안 의료기관에서의 검진을 주저하던 여성들을 끌어들이면서 시장을 확대할 것입니다.

자원이 제한된 지역의 선별검사 수진율 저하

자원이 제한된 국가들에서는 검진 보급률이 낮아 자궁경부암 진단 시장의 성장을 크게 저해하고 있습니다. WHO에 따르면, 많은 저·중소득 국가에서 자궁경부암 검진을 받는 여성의 비율은 5% 미만에 그치고 있어, 상당한 개선이 필요하다는 점이 부각되고 있습니다. 공중보건 인프라의 취약성, 일관성 없는 의뢰 경로, 재정적 제약, 도시 외곽 지역의 접근 제한과 같은 기본적인 과제들이 여전히 남아 있습니다. 자금이 확보된다 하더라도, 지속 가능한 전국적인 검진율 달성은 검사 기관 네트워크, 등록 제도, 인재 양성 및 사후 관리 체계의 구축이 필요한 단계적인 과정입니다. 그 결과, 이들 지역 시장 성장은 고르지 않은 양상을 보이며, 도시 지역의 프리미엄 수요를 겨냥하는 기업보다는 단계적인 공공 프로그램이나 실용적인 접근 모델에 적응하는 공급업체가 우위를 점하고 있습니다.

부문별 분석

HPV 검사는 자궁경부암 진단 시장에서 가장 빠르게 성장하고 있는 검사 유형으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.52%를 나타낼 것으로 전망됩니다. 2025년에는 체계적인 선별 검사 시스템 및 병용 검사 워크플로우에서 확고한 역할을 수행하고 있었기 때문에 자궁경부 세포진 검사가 검사 유형 중 가장 큰 비중을 차지했습니다. 2026년 2월, 홀로직사가 “Aptima HPV 검사”이에 대해 FDA 승인을 획득함으로써, 해당 회사의 검사 범위가 모든 주요 선별 검사 방법으로 확대되었으며, HPV를 주축으로 한 1차 선별 검사로의 전환이 더욱 가속화되었습니다. ACOG(미국 산부인과 학회)의 환자 자가 채취형 고위험 HPV 검사 권고, 그리고 2026년 4월 워터스사가 “BD Onclarity HPV 자가 채취 키트”이에 대해 FDA의 승인을 획득한 것은 접근성이 높은 검체 채취 방식으로의 전환을 더욱 촉진했습니다.

HPV 검사의 확대는 단순히 기존 검사법을 대체하는 것만으로 추진되고 있는 것은 아닙니다. 자궁경부암 사례의 약 60%는 검진이 불충분하거나 한 번도 검진을 받은 적이 없는 사람들에게서 발생하고 있으며, 이는 검진 대상자를 확대하기 위한 새로운 접근 모델의 가능성을 부각시키고 있습니다. 2027년에 발효될 HRSA 지침의 개정은 승인된 자가 채취 검사가 미국의 대부분의 보험 플랜에서 본인 부담금 없이 적용되도록 보장함으로써 이러한 전환을 뒷받침할 것입니다. 콜포스코피, 자궁경부 생검 및 자궁경관 소파술은 여전히 중요한 추적 검사 수단이며, 그 시행 건수는 HPV 검사를 통한 선별 검사에서 이상 소견이 확인된 건수와 밀접한 관련이 있습니다. 의료진이 HPV 검사 양성 결과 이후 보다 적절한 위험도 계층화를 모색하는 가운데, 바이오마커에 기반한 선별 도구의 중요성이 커지고 있으며, 대규모로 시행되는 선별 검사와 가치 높은 확정 진단 과정 간의 균형이 이루어지고 있습니다.

지역별 분석

2025년에는 북미가 선진적인 검사실 인프라, 엄격한 지침 준수, 그리고 광범위한 보험 급여 지원을 바탕으로 지역별 시장을 주도했습니다. 2027년에 예정된, 자가 채취를 통한 고위험 HPV 검사에 대한 본인 부담금 전액 면제 보험 적용을 도입하는 미국의 정책 개편은 경제적 및 접근성상의 장벽을 해소함으로써 검사 참여율을 높일 것으로 기대됩니다. 2025년 및 2026년의 주요 승인 사례로는 Teal Wand, Hologic사의 1차 선별 검사용 “Aptima HPV Assay”, BD사의 가정용 “Onclarity HPV 자가 채취 키트”등을 들 수 있으며, 이러한 요소들이 해당 지역의 위상을 더욱 공고히 했습니다. 캐나다에서는 주 정부가 운영하는 통합 선별 검사 시스템을 통해 진전이 나타나고 있는 반면, 멕시코에서는 기존의 자궁경부 세포진 검사를 중심으로 한 공적 의료 모델을 넘어, HPV 검사 경로의 보다 광범위한 도입이 모색되고 있습니다.

유럽에서는 국가마다 정책 시행 시기나 기술 도입 현황에 있어 다양성이 나타납니다. 영국의 1차 HPV 검사 조기 도입은 유사한 전환을 검토하고 있는 다른 국가들에게 벤치마크가 되고 있습니다. 독일, 프랑스, 이탈리아에서는 병용 검사 체계를 모색하는 한편, HPV 우선 프로토콜로의 전환에 따른 비용 대비 효과를 평가했습니다. TrUScreen사가 2026년에 루마니아와 이탈리아로 사업을 확장한 것은 이들 지역이 기존의 검진 방식에서 전환해 나가는 과정에서 남유럽 및 동유럽에 대한 상업적 관심이 높아지고 있음을 보여줍니다.

아시아태평양은 자궁경부암 진단 분야에서 가장 빠르게 성장하고 있는 시장이며, 2031년까지의 연평균 성장률(CAGR)은 7.34%로 예측됩니다. 이러한 성장은 대상 인구의 규모, 근절 목표에 대한 정부의 관심 증대, 그리고 도시 지역에서의 민간 진단 투자 증가에 힘입어 이루어지고 있습니다. 중국에서는 11개 성에서 TrUScreen AI 자궁경부암 검진 장비가 공적 의료보험 급여 대상으로 도입되어, 실용적인 검진 도구의 확장성이 입증되었습니다. 말레이시아가 2026년에 시작할 3년간의 EPICC 자궁경부암 근절 프로그램은 등록 제도 강화, 역량 강화, 그리고 공평한 검진 접근성 확보에 대한 확고한 의지를 반영하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the cervical cancer diagnostic market size is projected to expand from USD 6.39 billion in 2025 and USD 6.75 billion in 2026 to USD 8.85 billion by 2031, registering a CAGR of 5.58% between 2026 to 2031.

This report is Segmented by Test Type (Pap Smear, HPV Testing, Colposcopy, Biopsies, Others), End User (Hospitals, Specialty Clinics, Diagnostic Centers, Cancer/Radiation Centers, Home Care), Technology (Liquid-Based Cytology, Molecular Diagnostics, Digital Cytology and AI Imaging, IHC and Biomarker Testing), & Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in USD Value.

Global Cervical Cancer Diagnostic Market Trends and Insights

Rising Cervical Cancer Burden and Persistent HPV Prevalence

The cervical cancer diagnostic market thrives on unmet screening needs rather than technological saturation. HPV is responsible for over 99% of cervical cancer cases globally, making screening essential across healthcare systems. A staggering 90% of cervical cancer deaths occur in low to middle-income nations, where access to screening remains limited and unevenly distributed. WHO highlights that over 1 billion women have never undergone screening, indicating a vast demand for first-time testing outside organized care. While vaccination programs aim to reduce future burdens, they will not significantly lower the immediate demand for adult screenings due to the need for monitoring infected and aging populations. This positions the cervical cancer diagnostic market to address substantial unmet screening needs in both developed and emerging regions.

Expansion of HPV Primary Screening and Self-Sampling

The cervical cancer diagnostic market is shifting toward HPV-centric screening methods as regulators and clinical entities endorse primary HPV testing and self-collection. In February 2026, Hologic received FDA approval for its Aptima HPV Assay, expanding its application to Pap testing, co-testing, and primary HPV screening. The ASCCP approved self-collection capabilities for Abbott Alinity, BD Onclarity, and Roche Cobas in healthcare settings, strengthening compliance. ACOG endorsed high-risk HPV testing for average-risk women aged 30 to 65 every three years in April 2026, marking a significant shift in routine screening practices. A U.S. policy effective in 2027 will further support this trend, as self-collected tests will be fully covered by most health plans. Self-collection expands the market by attracting women previously deterred from clinic-based screenings.

Low Screening Coverage in Resource-Constrained Settings

In lower-resource countries, limited screening coverage significantly restricts the growth of the cervical cancer diagnostic market. According to the WHO, in many low- and middle-income nations, fewer than 5% of women undergo cervical cancer screening, highlighting the need for substantial improvements. Basic challenges such as weak public health infrastructure, inconsistent referral pathways, financial constraints, and limited access outside urban areas persist. Even with funding, achieving sustainable national coverage is a gradual process requiring the development of laboratory networks, registries, workforce training, and follow-up systems. As a result, the market in these regions grows unevenly, favoring suppliers that adapt to phased public programs and practical access models over those targeting premium urban demand.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Cytology and Digital Colposcopy Workflow Automation

- Government Screening Mandates and Elimination Targets

- Shortage of Trained Cytotechnologists and Colposcopists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HPV testing is the fastest-growing test type in the cervical cancer diagnostic market, with a projected CAGR of 6.52% from 2026 to 2031. Pap smear testing held the largest position among test types in 2025 due to its established role in organized screening systems and co-testing workflows. Hologic's FDA approval for the Aptima HPV Assay in February 2026 strengthened the shift toward HPV-led primary screening by expanding the company's coverage across all major screening approaches. ACOG's endorsement of patient self-collected high-risk HPV testing and Waters' FDA clearance for the BD Onclarity HPV Self-Collection Kit in April 2026 further supported the move toward accessible sample collection methods.

HPV testing growth is not solely driven by replacing older modalities. Approximately 60% of cervical cancer cases arise in under-screened or never-screened individuals, highlighting the potential of new access models to expand the tested population. The HRSA guideline update effective in 2027 will support this shift by ensuring approved self-collected tests are covered without cost-sharing under most U.S. plans. Colposcopy, cervical biopsies, and endocervical curettage remain critical follow-up tools, with their volumes tied to abnormal findings from HPV-led screening. Biomarker-based triage tools are gaining relevance as providers seek better risk stratification after positive HPV results, balancing high-volume screening tests with high-value confirmatory pathways.

Complete Report Scope:

- By Test Type

- Pap Smear Testing

- HPV Testing

- Colposcopy

- Cervical Biopsies and Endocervical Curettage

- Other Diagnostic Tests

- By End User

- Hospitals

- Specialty Clinics

- Diagnostic Centers

- Cancer and Radiation Therapy Centers

- Home Care Settings

- By Technology

- Liquid-Based Cytology

- Molecular Diagnostics

- Digital Cytology and AI-Assisted Imaging

- Immunohistochemistry and Biomarker Testing

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America led the regional market due to its advanced laboratory infrastructure, strict guideline adherence, and extensive reimbursement support. A 2027 U.S. policy update introducing zero-cost-sharing coverage for self-collected high-risk HPV testing is expected to enhance participation by addressing financial and access barriers. Key approvals in 2025 and 2026, including the Teal Wand, Hologic's Aptima HPV Assay for primary screening, and BD's Onclarity HPV Self-Collection Kit for home use, further strengthened the region's position. Canada is advancing through centralized provincial screening systems, while Mexico is exploring broader adoption of HPV pathways beyond traditional Pap-led public care models.

Europe exhibits diversity in policy timing and technology adoption across countries. The United Kingdom's early adoption of primary HPV testing has set a benchmark for other nations considering similar transitions. Germany, France, and Italy are navigating co-testing structures and evaluating the cost-effectiveness of shifting to HPV-first protocols. TrUScreen's 2026 expansion into Romania and Italy highlights growing commercial interest in Southern and Eastern Europe as these regions transition from conventional screening methods.

The Asia-Pacific region is the fastest-growing market for cervical cancer diagnostics, with a projected 7.34% CAGR through 2031. This growth is driven by a large target population, increased government focus on elimination goals, and rising private diagnostic investments in urban areas. China has deployed TrUScreen AI cervical screening devices across 11 provinces under public health insurance reimbursement, showcasing the scalability of practical screening tools. Malaysia's 2026 launch of the 3-year EPICC cervical cancer elimination program reflects a strong commitment to enhancing registries, capacity building, and equitable screening access.

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- BGI Genomics Co., Ltd.

- bioMerieux

- Carl Zeiss

- The Cooper Companies

- Danaher

- DYSIS Medical Ltd.

- Roche

- Femasys Inc.

- Guided Therapeutics, Inc.

- Hologic

- MedGyn Products

- Olympus

- QIAGEN

- Quest Diagnostics

- Seegene

- Siemens Healthineers

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Rising Cervical Cancer Burden and Persistent HPV Prevalence

- 4.1.2 Expansion of HPV Primary Screening and Self-Sampling Adoption

- 4.1.3 AI-Enabled Cytology and Digital Colposcopy Workflow Automation

- 4.1.4 Government Screening Mandates and Elimination Targets

- 4.1.5 Expanded Access Through Decentralized Laboratory Networks

- 4.2 Market Restraints

- 4.2.1 Low Screening Coverage in Resource-Constrained Settings

- 4.2.2 Shortage of Trained Cytotechnologists and Colposcopists

- 4.2.3 Reimbursement Variation and High Upfront Test Costs

- 4.2.4 Specimen Quality and False-Negative Risk in Real-World Screening

- 4.3 Supply/Value Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Test Type

- 5.1.1 Pap Smear Testing

- 5.1.2 HPV Testing

- 5.1.3 Colposcopy

- 5.1.4 Cervical Biopsies and Endocervical Curettage

- 5.1.5 Other Diagnostic Tests

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Specialty Clinics

- 5.2.3 Diagnostic Centers

- 5.2.4 Cancer and Radiation Therapy Centers

- 5.2.5 Home Care Settings

- 5.3 By Technology

- 5.3.1 Liquid-Based Cytology

- 5.3.2 Molecular Diagnostics

- 5.3.3 Digital Cytology and AI-Assisted Imaging

- 5.3.4 Immunohistochemistry and Biomarker Testing

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agilent Technologies, Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 BGI Genomics Co., Ltd.

- 6.3.5 bioMerieux SA

- 6.3.6 Carl Zeiss Meditec AG

- 6.3.7 CooperSurgical, Inc.

- 6.3.8 Danaher Corporation

- 6.3.9 DYSIS Medical Ltd.

- 6.3.10 F. Hoffmann-La Roche Ltd

- 6.3.11 Femasys Inc.

- 6.3.12 Guided Therapeutics, Inc.

- 6.3.13 Hologic, Inc.

- 6.3.14 MedGyn Products, Inc.

- 6.3.15 Olympus Corporation

- 6.3.16 QIAGEN N.V.

- 6.3.17 Quest Diagnostics Incorporated

- 6.3.18 Seegene Inc.

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Thermo Fisher Scientific Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment