|

시장보고서

상품코드

2073210

중동의 사료용 향료 및 감미료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Middle East Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

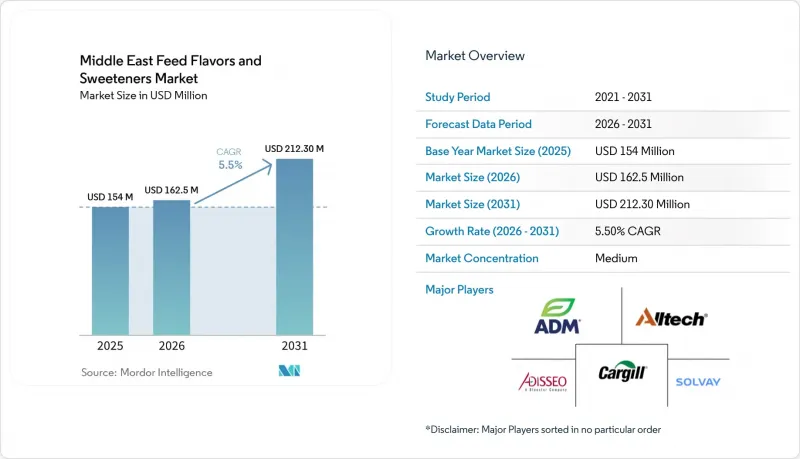

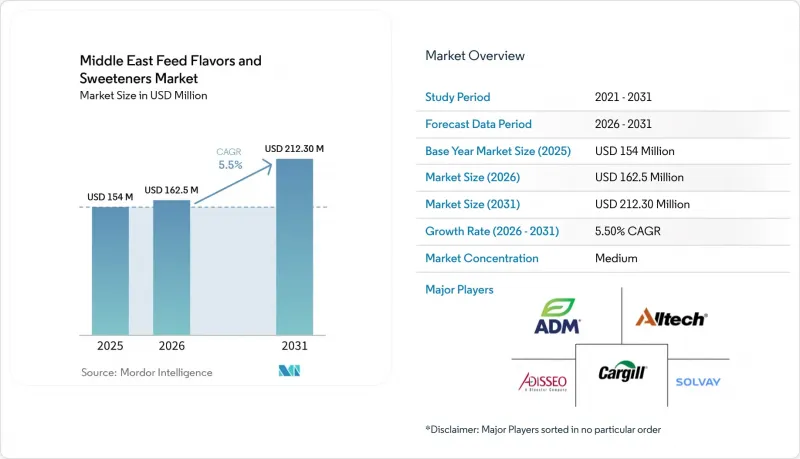

Mordor Intelligence에 의하면, 중동 사료용 향료(Flavor) 및 감미료 시장은 2025년에 1억 5,400만 달러여, 2026년 1억 6,250만 달러에서 2031년까지 2억 1,230만 달러로 성장하여 2026년부터 2031년까지 기간에서 CAGR 5.5%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(향미료 및 감미료), 동물별(반추동물, 돼지, 기타 동물), 국가별(이란, 사우디아라비아, 기타 중동 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

중동 사료용 향료 및 감미료 시장 동향과 인사이트

상업용 사료의 기호성 향상에 대한 수요 증가

해당 지역의 상업용 사료 생산은 기본적인 상품형 배합에서 영양 밀도가 높고 생산 성능을 중시하는 배합으로 전환되고 있으며, 그 결과 배합에 사용되는 관능 첨가물의 사용량이 증가하고 있습니다. 사료 공장에서는 사료 섭취 거부 현상이 사료 전환 효율에 악영향을 미치고, 육류 및 유제품의 생산 비용을 상승시키기 때문에 사료 섭취량을 유지하기 위해 향료와 감미료를 배합하고 있습니다. 사우디아라비아에서는 대규모 가금류 및 낙농 시스템에서 기호성은 이미 사료 배합의 표준적인 구성 요소로 자리 잡고 있으며, 단순한 선택적 첨가물로 간주되지 않습니다. 『Alltech Feed』의 2026년 조사에 따르면, 2025년 전 세계 사료 생산량은 14억 메트릭톤에 달했습니다. 해당 보고서에서는 중동의 사료 생산이 질병의 위협이나 원자재 가격 변동성 등의 과제에 직면해 있다는 점도 지적되고 있으며, 생산자들에게 있어 안정적인 사료 공급이 매우 중요해지고 있습니다. 이러한 첨가제의 가치는 연속 혼합과 정밀한 투여를 통해 저배합률의 특수 원료의 일관성이 향상되는 현대적인 사료 공장에서 더욱 높아지고 있습니다. 그 결과, 중동의 사료용 향료 및 감미료 시장은 사료 수요 증가와 고품질 첨가제 사용을 위한 기술적 여건 개선이라는 두 가지 요인의 혜택을 동시에 누리고 있습니다. 이러한 추세는 재구매 행동을 촉진합니다. 왜냐하면, 섭취 지원 시스템이 표준 사료 사양에 포함되면 사료 제조업체들이 이를 시판용 배합에서 제외하려는 경향이 줄어들기 때문입니다.

가금류 및 반추동물용 사료 생산 확대

사우디아라비아와 이란에서 가축 생산량이 증가함에 따라, 향료와 감미료가 첨가된 사료에 대한 수요가 확대되고 있습니다. 반추동물 분야에서는 사우디아라비아에서 2026년 11월까지 다년생 사료작물의 재배가 단계적으로 폐지될 예정인 만큼, 시판 사료나 토탈 믹스 레이션(TMR)에 대한 의존도가 높아질 것으로 예상되며, 이에 따라 사일리지나 배합 사료 특유의 악취를 가리기 위한 첨가제 수요가 더욱 증가할 것으로 전망됩니다. 이란 역시 막대한 소 사육 두수와 국내 사료 생산 능력을 바탕으로 한 견실한 가금류 산업 덕분에 이러한 추세에 기여하고 있습니다. 2026년, 사우디아라비아가 러시아와 체결한 13건의 축산 협정(총액 48억 사우디아라비아 리얄(13억 달러))은 밸류체인 전반에 걸친 단백질 생산 능력 강화를 위한 지속적인 노력을 다시 한번 보여주고 있습니다. 가금류 및 반추동물 사육 시스템 모두에서 사료 소비량이 증가하는 가운데, 중동의 사료용 향료 및 감미료 시장은 안정적인 섭취량을 전제로 한 시판 배합 사료 시장의 기반 확대에 힘입어 성장하고 있습니다.

수입 특수 원료에 대한 의존

해당 지역에서는 고도의 사료용 향료 및 감미료 시스템에 있어 수입된 특수 원료에 대한 의존도가 매우 높습니다. 천연 향료 베이스, 캡슐화된 기호성 향상제, 활성 감미료 화합물 등의 주요 성분은 국내에서 생산되지 않고, 주로 유럽, 미국, 아시아에서 조달되고 있습니다. 이러한 의존성으로 인해 사료 제조업체들은 운임, 환율 변동, 조달 주기 장기화 등 여러 가지 비용 압박에 직면해 있습니다. 이 문제는 2026년 초, 호르무즈 해협 인근의 군사적 긴장이 고조되면서 주요 해운사들이 페르시아만에서의 운항을 중단하고, 사료 첨가물 납품에 큰 지연이 발생했을 때 특히 두드러지게 나타났습니다. 게다가 규제 당국의 승인 절차가 비상시 대체품의 도입을 방해하고 있습니다. 등록이나 국경을 넘는 승인 절차에 시간이 너무 오래 걸리기 때문에 급박한 공급 부족에 대처하지 못하는 경우가 많기 때문입니다. 그 결과, 중동의 사료용 향료 및 감미료 시장은 수요는 안정적이지만 제품 공급이 예기치 않게 부족해지는 등 구조적인 취약성을 보이고 있습니다. 또한, 이러한 의존 관계는 소규모 구매자의 가격 책정 유연성을 제한하고 있습니다. 소규모 구매자는 대규모 통합형 고객에 비해 재고를 유지하거나 유리한 물류 조건을 확보할 능력이 대개 부족하기 때문입니다.

부문별 분석

2025년 중동 사료용 향료 및 감미료 시장에서 향료는 82.2%를 차지하며, 계속해서 주도적인 위치를 유지하고 있습니다. 이러한 우위는 육계용 스타터 사료와 그로워 사료, 그리고 젖소의 총혼합사료(TMR)에서 풍미 시스템이 널리 사용되고 있기 때문입니다. 이러한 요소들은 원료의 특성 편차를 숨기고, 사료의 기호성을 일정하게 유지하는 데 도움이 됩니다. 또한, 많은 양계 및 낙농 사업에서 향료의 사용은 일반적으로 표준 사료 사양에 포함되어 있습니다. 아디세오가 중동 및 아프리카에서 전개하는 2025년 젖소 영양 파트너십 프로그램은 젖소에서 정밀 영양과 확실한 섭취량의 균형을 맞출 필요성이 커지고 있음을 부각시키고 있으며, 관리형 사료 공급 프로그램에서 향미 시스템의 사용을 더욱 촉진하고 있습니다. 그러나 사료 제조업체들이 첨가율을 낮추면서도 동일한 관능적 효과를 얻을 수 있는 저용량·고효능 시스템을 점점 더 선호하고 있기 때문에 공급업체들은 어려움에 직면해 있습니다.

감미료 시장은 2031년까지 연평균 성장률(CAGR) 4.3%를 나타낼 것으로 예측되며, 현재 시장 규모는 작지만 가장 빠르게 성장하는 하위 카테고리가 될 전망입니다. 이러한 성장은 주로 2026년 7월까지 사료 배합의 준수를 의무화하는 EU 규정 2024/1727에 힘입어, 유럽에서 수입되는 사료 첨가제에서 사카린을 배제한 재배합 추세가 나타난 데 기인합니다. 유럽식품안전청(EFSA)이 2025년에 실시한 NHDC의 안전성 평가는 사카린 대체제의 발전 방향을 더욱 명확히 했습니다. Phytobiotics와 ADM 등의 기업들은 천연 유래 또는 수용체 표적형 감미료 시스템을 활용한 사카린 무첨가 대체품을 시장에 출시하고 있습니다. 이러한 전환은 현지 규제가 아닌 수입 사료의 배합 변경에 따른 영향을 받고 있기 때문에 중동의 사료용 향료 및 감미료 시장 유통업체들은 공급업체의 배합에 광범위한 변경이 이루어지기 전에 대체 감미료 시스템의 적합성을 확인해야 하는 상황에 놓여 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the middle east feed flavors and sweeteners market was USD 154.0 million in 2025 and projected to grow from USD 162.5 million in 2026 to USD 212.3 million by 2031, registering a CAGR of 5.5% during the period from 2026 to 2031.

This report is Segmented by Type (Flavors and Sweeteners), by Animal (Ruminants, Swine, and Other Animals), and by Country (Iran, Saudi Arabia, and the Rest of the Middle East). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East Feed Flavors and Sweeteners Market Trends and Insights

Rising Demand for Palatability Enhancement in Commercial Feed

Commercial feed production in the region is transitioning from basic commodity-style blends to denser, performance-oriented rations, leading to increased use of sensory additives in formulations. Feed mills incorporate flavors and sweeteners to maintain feed intake, as feed refusal negatively impacts conversion efficiency and raises the cost of producing meat and milk. In Saudi Arabia, large poultry and dairy systems already consider palatability as a standard component of feed formulation rather than an optional addition. According to the Alltech Feed survey 2026, global compound feed production reached 1.4 billion metric tons in 2025. The report also highlighted that Middle East feed output faces challenges, including disease pressure and raw material variability, making stable feed intake critical for producers. The value of these additives is further enhanced in modern mills, where continuous mixing and precise dosing improve the consistency of low-inclusion specialty ingredients. Consequently, the Middle East feed flavors and sweeteners market is benefiting from both increased feed demand and improved technical conditions for the use of premium additives. This trend fosters repeat purchasing behavior, as once intake-support systems are integrated into standard feed specifications, mills are less inclined to remove them from commercial formulations.

Growth in Poultry and Ruminant Feed Production

Increasing livestock production in Saudi Arabia and Iran is driving higher demand for compound feed incorporating flavors and sweeteners. On the ruminant side, the planned cessation of perennial forage cultivation in Saudi Arabia by November 2026 is anticipated to increase reliance on commercial feed and total mixed rations, thereby intensifying the need for additives to mask silage and formulation off-notes. Iran also contributes to this trend, with its substantial cattle population and a robust poultry industry supported by domestic feed manufacturing capabilities. In 2026, Saudi Arabia's 13 livestock agreements with Russia, valued at SAR 4.8 billion (USD 1.3 billion), further indicate ongoing efforts to enhance protein production capacity across the value chain. As feed volumes expand in both poultry and ruminant systems, the Middle East feed flavors and sweeteners market benefits from a growing base of commercial formulas reliant on stable intake.

Dependence on Imported Specialty Ingredients

The region heavily relies on imported specialty ingredients for advanced feed flavor and sweetener systems. Key components such as natural flavor bases, encapsulated palatants, and active sweetener compounds are predominantly sourced from Europe, the United States, and Asia, rather than domestic production. This reliance subjects feed mills to multiple cost pressures, including freight charges, currency fluctuations, and extended procurement cycles. The issue became particularly evident in early 2026, when military escalation near the Strait of Hormuz prompted major shipping lines to halt Gulf operations, resulting in significant delays in feed additive deliveries. Additionally, regulatory approval processes hinder emergency substitutions, as registration and cross-border acceptance are often too slow to address immediate shortages. Consequently, the Middle East feed flavors and sweeteners market exhibits structural vulnerability, such as demand remaining steady, but product availability can unexpectedly become constrained. This dependency also limits pricing flexibility for smaller buyers, who typically lack the capacity to maintain inventory or secure favorable logistics terms compared to larger, integrated customers.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Antibiotic-Free Feed Programs

- Expansion of Modern Feed Milling Capacity

- Price Sensitivity Among Small Feed Producers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors account for 82.2% of the Middle East feed flavors and sweeteners market in 2025, maintaining their leading position. This dominance is attributed to the widespread use of flavor systems in broiler starter and grower feeds and in dairy total mixed rations, which help mask variations in raw material characteristics and ensure consistent feed acceptance. Additionally, flavor usage is often integrated into standard feed specifications at many poultry and dairy operations. Adisseo's 2025 dairy nutrition partnership program in the Middle East and Africa highlights the increasing need to balance precision nutrition with reliable intake in dairy cattle, further supporting the use of flavor systems in controlled feeding programs. However, suppliers face challenges as mills increasingly prefer lower-dose, higher-potency systems that achieve similar sensory outcomes at reduced inclusion rates.

Sweeteners are projected to grow at a compound annual growth rate (CAGR) of 4.3% through 2031, positioning them as the fastest-growing subcategory despite their currently smaller market value. This growth is primarily attributed to the saccharin-free reformulation trend in imported European feed additives, driven by Regulation EU 2024/1727, which mandates compliance for compound feed by July 2026. The European Food Safety Authority's (EFSA) 2025 assessment of NHDC safety has further clarified the pathway for saccharin replacements. Companies such as Phytobiotics and ADM have introduced saccharin-free alternatives utilizing natural or receptor-targeted sweetener systems. As this transition is influenced by imported feed reformulation rather than local bans, distributors in the Middle East feed flavors and sweeteners market face pressure to qualify alternative sweetener systems before broader changes are implemented in supplier formulations.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal

- Swine

- Ruminants

- Dairy Cattle

- Beef Cattle

- Others

- Others

- By Country

- Iran

- Saudi Arabia

- Rest of Middle East

List of Companies Covered in this Report:

- Solvay S.A.

- ADM

- Adisseo

- Alltech, Inc.

- Arvesta (Palital Feed Additives B.V.)

- Cargill, Inc.

- Innov Ad NV/SA

- Phytobiotics Futterzusatzstoffe GmbH

- Prinova Group LLC

- AFB International, Inc.

- CJ CheilJedang Corporation

- Orffa International Holding BV

- Amlan International

- Dr. Eckel Animal Nutrition GmbH and Co. KG

- Symrise AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Palatability Enhancement in Commercial Feed

- 4.2.2 Growth in Poultry and Ruminant Feed Production

- 4.2.3 Shift Toward Antibiotic-Free Feed Programs

- 4.2.4 Expansion of Modern Feed Milling Capacity

- 4.2.5 Increasing Use of Natural Feed Inputs

- 4.2.6 Heat Stress Management in Livestock Nutrition

- 4.3 Market Restraints

- 4.3.1 Dependence on Imported Specialty Ingredients

- 4.3.2 Price Sensitivity Among Small Feed Producers

- 4.3.3 Limited Local Formulation and Testing Infrastructure

- 4.3.4 Supply Chain Disruptions and Trade Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Swine

- 5.2.2 Ruminants

- 5.2.2.1 Dairy Cattle

- 5.2.2.2 Beef Cattle

- 5.2.2.3 Others

- 5.2.3 Others

- 5.3 By Country

- 5.3.1 Iran

- 5.3.2 Saudi Arabia

- 5.3.3 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Solvay S.A.

- 6.4.2 ADM

- 6.4.3 Adisseo

- 6.4.4 Alltech, Inc.

- 6.4.5 Arvesta (Palital Feed Additives B.V.)

- 6.4.6 Cargill, Inc.

- 6.4.7 Innov Ad NV/SA

- 6.4.8 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.9 Prinova Group LLC

- 6.4.10 AFB International, Inc.

- 6.4.11 CJ CheilJedang Corporation

- 6.4.12 Orffa International Holding BV

- 6.4.13 Amlan International

- 6.4.14 Dr. Eckel Animal Nutrition GmbH and Co. KG

- 6.4.15 Symrise AG