|

시장보고서

상품코드

2073279

이민 및 비자 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Immigration and Visa Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

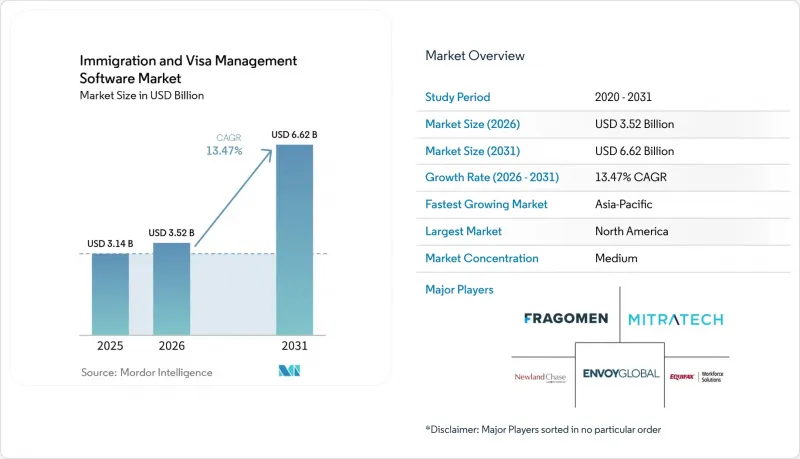

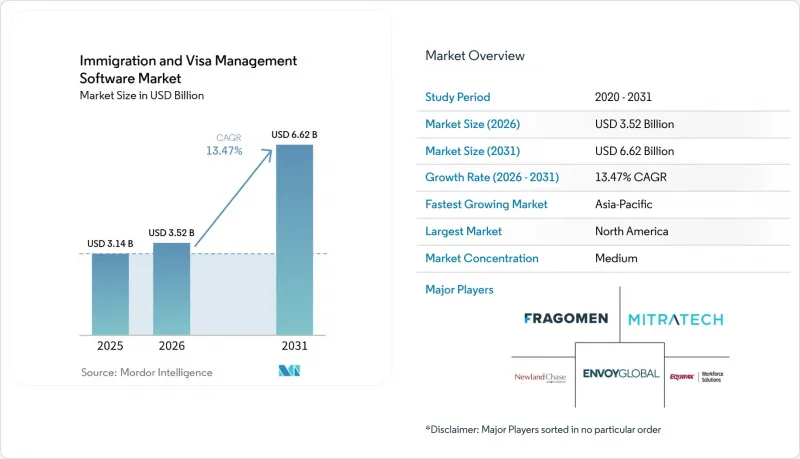

Mordor Intelligence에 의하면, 이민 및 비자 관리 소프트웨어 시장 규모는 2025년 31억 4,000만 달러로 평가되었습니다. 2026년에는 35억 2,000만 달러로 확대되어 2031년까지 66억 2,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 13.47%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(클라우드 및 On-Premise), 용도(비자·입국 관리 프로젝트 관리, 규정 준수 관리 등), 조직 규모(대기업 및 중소기업), 최종 사용자(기업, 법률 사무소, 교육 기관 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 이민 및 비자 관리 소프트웨어 시장 동향 및 인사이트

비자 및 취업 허가 관련 규정 준수에 대한 고용주 수요 증가

법 집행에 대한 압박이 커짐에 따라, 다국적 기업들에게 이민 규정 준수는 정기적인 법적 검토라기보다는 일상적인 운영상의 과제가 되고 있으며, 이러한 변화가 이민 및 비자 관리 소프트웨어 시장을 지속적으로 뒷받침하고 있습니다. 2025년 1월 시행된 H-1B 현대화 규정에 따라 후원사 요건이 변경됨에 따라, 신청 관리의 엄격화, 서류 추적, 그리고 고용주 팀 간의 내부 협업 필요성이 높아졌습니다. 이러한 상황에서는 당국이 증거 제출을 요구하거나 감사를 실시할 때 고용주가 신속하게 제시할 수 있는 완전한 기록이 필요하기 때문에 수작업에 의존하는 프로세스는 위험 요인이 됩니다. 이러한 요건으로 인해, 프로젝트 현황의 가시화, 버전 관리, 기한 알림, 그리고 타당성을 입증할 수 있는 감사 추적을 단일 환경에서 통합한 플랫폼이 유리해지고 있습니다. 그 결과, 고용주들이 규정 위반을 단순한 관리상의 부담이 아니라 사업 중단으로 인식하는 분야에서 이민 및 비자 관리 소프트웨어 시장이 가장 큰 혜택을 보고 있습니다.

국경을 초월한 채용과 분산형 인력의 확대

국경을 초월한 채용이 인재 계획에 점점 더 자리 잡고 있으며, 이에 따라 이민 및 비자 관리 소프트웨어 시장의 사용자 기반이 확대되고 있습니다. 다국적 기업들은 인력을 거점 간에 배치할 때 업무 인계 시점과 규정 준수상의 차이를 최소화하기 위해, 채용, 급여 계산, 인력 이동 및 이민 절차를 연계하려는 움직임을 강화하고 있습니다. 이러한 수요는 거래 동향에서도 드러나고 있으며, 2026년 1월 Payoneer가 Boundless를 인수한 사례가 대표적입니다. 이로 인해 이민 규정 준수가 국경을 초월한 급여 계산, 세무, 복리후생 관리와 더욱 직접적으로 연계되었습니다. Flagomen과 Papaya·World 역시 2026년 5월, 이와 유사한 움직임을 보이며, 이민 관련 지식을 더 광범위한 직원 대상 급여 지급 도구 및 각국에 관한 지식 도구와 연계했습니다. 이러한 움직임은 이민 및 비자 관리 소프트웨어 시장이 더 이상 비자 신청에만 국한되지 않고, 보다 광범위한 세계 고용 운영 모델과 밀접하게 연결되어 있음을 보여줍니다.

기밀성이 높은 이민 데이터의 보안 및 개인정보 보호 위험

기밀성이 높은 이민 기록은 신원 정보, 국적, 법적 지위, 그리고 대부분의 경우 가족에 대한 세부 정보가 단일 시스템에 통합되어 있기 때문에 이민 및 비자 관리 소프트웨어 시장에서 여전히 큰 장벽으로 남아 있습니다. 유럽 데이터 보호 감독관은 2025년, 이민 관리 시스템과 관련된 거버넌스상의 우려를 지적했는데, 이는 데이터 보호의 관점에서 볼 때 이 분야가 얼마나 엄격하게 검토되고 있는지를 보여주는 사례입니다. 영국에서는 내무부의 전자비자(eVisa) 시스템과 관련된 우려 사항이 2025년에 데이터 보호 및 정보 공개 위험에 대한 공식적인 관심을 불러일으켰습니다. 이러한 상황으로 인해, 계약 체결 전에 데이터 저장 위치, 인증, 접근 제어 및 사고 대응의 성숙도에 대해 구매자의 기대가 높아지고 있습니다. 그 결과, 강력한 보안 거버넌스를 입증하지 못하는 소규모 공급업체의 경우, 이민 및 비자 관리 소프트웨어 시장에 진입하기가 점점 더 어려워지고 있습니다.

부문별 분석

2025년, 소프트웨어는 시장의 71.84%를 차지하며 이민 및 비자 관리 소프트웨어 시장의 주요 수익원으로 자리매김했습니다. 이는 고용주가 프로젝트, 서류, 주요 단계, 규정 준수 보고서를 일원화하여 관리할 수 있는 시스템이 필요하기 때문입니다. 이러한 주도적 지위는 변호사가 주도하는 수작업 방식의 관리에서 여러 관할 구역에 걸친 이민 업무를 표준화할 수 있는 기술 주도형 운영 모델로의 보다 광범위한 전환을 반영하고 있습니다. 실제로 소프트웨어는 “시스템 오브 레코드(기록 관리 시스템)"의 역할을 하고 있으며, 이것이 없다면 구매자가 복잡한 프로그램을 효율적으로 관리하기는 어렵습니다. 이러한 기반을 통해 소프트웨어 계층은 분석, 모빌리티, 규정 준수 및 보다 광범위한 인력 워크플로우로의 교차 판매 진입점이 되고 있습니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 14.72%로 확대될 것으로 예측되며, 이는 이민 및 비자 관리 소프트웨어 시장의 도입이 대부분의 경우 도입 지원, 지속적인 규제 대응 지원, 교육 및 운영 관리와 함께 이루어지고 있음을 보여줍니다. 이러한 경향은 고용주가 규제 변경에 직면하여 절차를 신속하게 재구성하기 위해 외부 지원이 필요한 경우에 특히 두드러집니다. 풀스택 벤더가 우위를 점하는 이유는 구매자가 기술, 프로세스 설계, 지속적인 프로그램 지원을 모두 제공할 수 있는 단일 공급업체를 선호하는 경향이 있기 때문입니다. 따라서 이민 및 비자 관리 소프트웨어 업계에서는 소프트웨어에만 의존하는 것이 아니라, 소프트웨어와 탄탄한 관리형 서비스를 패키지로 제공할 수 있는 기업이 높이 평가받고 있습니다.

2025년 기준으로, 이민 및 비자 관리 소프트웨어 시장 규모의 73.42%를 클라우드가 차지했으며, 이러한 우위는 고용주들이 원격 접속, 쉬운 도입, 지속적인 업데이트, 그리고 최신 인사 시스템과의 원활한 통합을 중요하게 여긴다는 점을 반영하고 있습니다. 클라우드 모델이 이 시장에 적합한 이유는 이민 담당 팀, 인사 담당자, 관리자 및 외부 파트너가 서로 다른 장소에서 동일한 사건 기록에 접근해야 하는 경우가 많기 때문입니다. 또한, 기존의 On-Premise형 모델보다 신속하게 규제 변경에 대응할 수 있다는 점도, 각국의 요건이 급격히 변화할 수 있는 시장에서 중요합니다. 그 결과, 이민 및 비자 관리 소프트웨어 시장에서는 도입 장벽이 낮고 모듈식 클라우드 기반 워크플로를 제공할 수 있는 공급업체들이 꾸준히 지지를 얻고 있습니다.

클라우드 시장은 2031년까지 연평균 성장률(CAGR) 14.04%를 나타낼 것으로 예측되며, 이는 예측 기간 동안 규모 및 성장 측면에서 선도적 위치를 유지할 가능성이 높음을 의미합니다. On-Premise형 시스템은 정부 기관이나 일부 금융 기관, 그리고 엄격한 내부 호스팅 규정이 마련된 기타 환경에서 여전히 중요한 역할을 수행하고 있습니다. 그렇긴 하지만, 주요 보안 우려 사항을 해결해 주는 프라이빗 클라우드나 소버린 클라우드와 같은 대안에 대한 구매자들의 수용도가 높아짐에 따라, 그 위상은 점차 약화되고 있습니다. 따라서 이민 및 비자 관리 소프트웨어 시장에서는 중점이 클라우드 제공으로 더욱 이동하고 있는 반면, On-Premise 방식은 주로 특수한 이용 사례에서 그 중요성을 유지하고 있습니다.

지역별 분석

2025년, 북미는 이민 및 비자 관리 소프트웨어 시장 점유율의 45.92%를 차지하며, 이 지역은 계속해서 최대 시장으로 자리매김했습니다. 이는 고용주가 상세한 취업 허가 요건이 수반되는 엄격한 법 집행 환경 속에서 사업을 운영하고 있기 때문입니다. 미국에서는 2025년 1월에 시행된 H-1B 비자 현대화 규정에 따라 고용주의 행정 업무가 더욱 복잡해지면서, 신청 현황, 마감일, 임금 수준 및 자격 요건을 체계적으로 추적할 수 있는 소프트웨어의 가치가 높아졌습니다. 또한 미국에서는 대규모 비자 프로그램을 운영하는 기업뿐만 아니라 모든 고용주에게 I-9 및 E-Verify 의무가 광범위하게 적용되고 있어, 이민 및 비자 관리 소프트웨어 시장에 대한 견고한 수요를 뒷받침하고 있습니다. 캐나다에서는 숙련 노동자 대상 이민 제도를 활용하는 고용주들이 문서 관리 및 신분 상태의 투명성 제고를 통해 혜택을 누릴 수 있게 됨에 따라, 관련 수요가 더욱 확대되고 있습니다. 멕시코는 여전히 소규모 시장이지만, 니어쇼어 방식의 서비스 제공과 국경을 초월한 고용 모델 덕분에 컴플라이언스 소프트웨어의 중요성이 점차 커지고 있습니다.

유럽은 이민 및 비자 관리 소프트웨어 시장에서 규제의 영향을 크게 받는 지역이며, 2026년의 변화 속도에 따라 구매자들은 업무 프로세스를 신속하게 개편해야 하는 상황에 직면해 있습니다. 2026년 4월 10일, EU 전역에서 “입국·출국 시스템(EES)"가 전면적으로 도입되었습니다. 이로 인해 고용주, 운송업체 및 여행 관련 사업자들은 출국 전 절차와 신원 확인 절차를 국경 관리 요건과 더욱 긴밀하게 연계할 필요성이 커졌습니다. 또한, 유럽집행위원회는 2026년 4월 EES와 ETIAS의 구분 및 시행 순서를 확정했으며, 이는 여행 및 규정 준수 업무 전반에 걸친 디지털 전환에 대한 투자를 더욱 촉진할 것입니다. 동시에, 파견 근로자에 대한 규정 준수 대응 역시 여전히 중요한 관련 요구 사항이며, 유럽노동청이 2025년에 실시한 파견 제도 하의 제3국 국민에 관한 조치는 노동력 이동과 입국 관리가 교차하는 지점에서 고용주가 직면하는 업무상의 복잡성을 여실히 드러내고 있습니다. 이러한 요인들로 인해 유럽은 이민 및 비자 관리 소프트웨어 시장에서 시스템 의존도가 가장 높은 지역 중 하나가 되었습니다.

아시아태평양은 연평균 성장률(CAGR) 16.02%로 확대될 것으로 예측되며, 2031년까지의 이민 및 비자 관리 소프트웨어 시장 규모에서 지역별 가장 높은 성장률을 보일 것으로 전망됩니다. 이러한 수요는 인도의 기술 분야 인재 채용, 싱가포르와 호주의 인력 이동, 그리고 보다 체계적인 규정 준수 시스템이 필요해진 일본과 한국의 중견 기업들의 관심 증가에 힘입어 뒷받침되고 있습니다. 또한 호주 및 뉴질랜드에서도 고용주가 후원자가 되는 취업 경로의 경우, 체계적인 기록 관리와 지속적인 프로세스 관리가 요구되기 때문에 도입이 촉진되고 있습니다. 아시아태평양 이외의 지역에서는 남미가 여전히 초기 단계에 있는 반면, 중동에서는 대규모 외국인 노동자와 다수의 취업 허가를 관리하는 고용주들로부터 관심이 쏠리고 있습니다. 아프리카는 전반적으로 아직 소규모 시장이지만, 국경을 넘는 인재 이동과 고용주 주도형 이동 패턴에서 차지하는 역할 덕분에 남아프리카공화국은 이 지역에서 이민 및 비자 관리 소프트웨어 도입이 가장 진전된 지역으로 두각을 나타내고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the immigration and visa management software market size is expected to increase from USD 3.14 billion in 2025 to USD 3.52 billion in 2026 and reach USD 6.62 billion by 2031, growing at a CAGR of 13.47% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, and On-Premises), Application (Visa and Immigration Case Management, Compliance Management, and More), Organization Size (Large Enterprises, and SMEs), End-User (Corporates, Law Firms, Educational Institutions, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Immigration and Visa Management Software Market Trends and Insights

Rising Employer Demand for Automated Visa and Work Authorization Compliance

Heightened enforcement pressure is making immigration compliance a routine operating issue rather than a periodic legal review for multinational employers, and that shift continues to support the immigration and visa management software market. The January 2025 H-1B modernization rule changed sponsorship requirements and increased the need for tighter filing controls, document tracking, and internal coordination across employer teams. In this setting, manual processes create risk because employers need complete records that can be produced quickly when authorities request evidence or conduct audits. That requirement favors platforms that combine case status visibility, version control, deadline alerts, and defensible audit trails in one environment. As a result, the immigration and visa management software market is benefiting most where employers view compliance failure as a business disruption rather than only an administrative burden.

Expansion of Cross-Border Hiring and Distributed Workforces

Cross-border hiring is becoming more embedded in workforce planning, and that is widening the user base for the immigration and visa management software market. Multinational employers are increasingly trying to connect hiring, payroll, mobility, and immigration steps so that talent can be deployed across locations with fewer handoff points and fewer compliance gaps. This demand is also showing up in transaction activity, including Payoneer's January 2026 acquisition of Boundless, which tied immigration compliance more directly to cross-border payroll, taxes, and benefits administration. Fragomen and Papaya Global moved in a similar direction in May 2026 by linking immigration intelligence with broader workforce payment and country knowledge tools. These moves show why the immigration and visa management software market is no longer limited to visa filing alone and is increasingly tied to broader global employment operating models.

Sensitive Immigration Data Security and Privacy Risks

Sensitive immigration records remain a major barrier in the immigration and visa management software market because they combine identity data, nationality, legal status, and often family details in a single system. The European Data Protection Supervisor highlighted governance concerns around migration management systems in 2025, which reinforces how tightly this category is being scrutinized from a data protection perspective. In the United Kingdom, concerns around the Home Office eVisa environment also drew formal attention to data protection and disclosure risks in 2025. These conditions are raising buyer expectations around data residency, certification, access controls, and incident response maturity before contracts are signed. The result is that the immigration and visa management software market is becoming harder to enter for smaller vendors that cannot demonstrate strong security governance.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Cloud-Based and API-Integrated Immigration Platforms

- Need for Audit-Ready Reporting and HRIS Integration

- Legacy Systems and Fragmented Data Ownership Slow Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 71.84% of the market in 2025 and remained the main revenue base of the immigration and visa management software market because employers need a central system for cases, documents, milestones, and compliance reporting. That leadership reflects a broader move away from attorney-led manual administration toward technology-led operating models that can standardize immigration work across multiple jurisdictions. In practice, software functions as the system of record, which makes it difficult for buyers to manage complex programs efficiently without it. This foundation also makes the software layer the entry point for cross-sell into analytics, mobility, compliance, and broader workforce workflows.

Services are projected to expand at a 14.72% CAGR through 2031, which shows that adoption in the immigration and visa management software market is often paired with implementation help, ongoing regulatory support, training, and managed operations. This pattern is especially visible when employers face changing rules and need external support to reconfigure processes quickly. Full-stack vendors benefit because buyers often prefer one provider that can combine technology, process design, and ongoing program support. The immigration and visa management software industry is therefore rewarding companies that can package software with managed service depth rather than relying on software alone.

Cloud accounted for 73.42% of the immigration and visa management software market size in 2025, and this lead reflects the value employers place on remote access, easier deployment, continuous updates, and simpler integration with modern HR systems. The cloud model fits the market well because immigration teams, HR staff, managers, and external partners often need access to the same case record from different locations. It also supports faster regulatory updates than traditional on-premises models, which matters in a market where country requirements can shift quickly. As a result, the immigration and visa management software market is steadily favoring vendors that can deliver modular, cloud-based workflows with lower implementation friction.

Cloud is projected to grow at a 14.04% CAGR through 2031, which means it is likely to retain both scale leadership and growth leadership during the forecast period. On-premises systems still matter in government agencies, some financial institutions, and other environments with strict internal hosting rules. Even so, that position is weakening as buyers become more comfortable with private cloud and sovereign-cloud options that address core security concerns. The immigration and visa management software market is therefore seeing the center of gravity move further toward cloud delivery, while on-premises remains important mainly in specialized use cases.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Application

- Visa and Immigration Case Management

- Compliance Management

- Employee Mobility Management

- Reporting and Analytics

- Other Application Workflows

- By Organization Size

- Large Enterprises

- SMEs

- By End-User

- Corporates

- Law Firms

- Government and Public Sector Agencies

- Educational Institutions

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America accounted for 45.92% of the immigration and visa management software market share in 2025, and the region remained the largest geography because employers operate in a dense enforcement environment with detailed work authorization requirements. In the United States, the January 2025 H-1B modernization rule increased administrative complexity for employers and reinforced the value of software that can track filings, deadlines, wage levels, and eligibility conditions in a structured way. The United States also provides a durable demand floor for the immigration and visa management software market because I-9 and E-Verify obligations apply broadly across employers, not only to firms with large visa programs. Canada adds a related layer of demand because employers working through skilled migration streams benefit from better document management and status visibility. Mexico remains a smaller market, but nearshore service delivery and cross-border employment models are gradually making compliance software more relevant there as well.

Europe is a highly regulation-driven region for the immigration and visa management software market, and the pace of change in 2026 is pushing buyers to refresh workflows quickly. The Entry/Exit System became fully deployed across the EU on April 10, 2026, which increased the need for employers, carriers, and travel-linked operators to align pre-travel and identity processes more closely with border requirements. The European Commission also confirmed the distinction and sequencing between EES and ETIAS in April 2026, which further supports digital readiness investment across travel and compliance operations. At the same time, posted worker compliance remains an important adjacent need, and the European Labour Authority's 2025 work on third-country nationals under posting arrangements highlights the operational complexity employers face when labor mobility intersects with immigration controls. These factors are making Europe one of the most system-intensive areas of the immigration and visa management software market.

Asia-Pacific is projected to expand at a 16.02% CAGR, giving it the fastest regional growth in the immigration and visa management software market size through 2031. Demand is being supported by technology-sector hiring in India, workforce mobility flows in Singapore and Australia, and stronger interest from mid-sized employers in Japan and South Korea that now need more formal compliance systems. Australia and New Zealand also support adoption because employer-sponsored pathways require organized recordkeeping and recurring process control. Outside Asia-Pacific, South America remains earlier stage, while the Middle East is generating interest from employers that manage large expatriate workforces and high permit volumes. Africa is still a smaller market overall, but South Africa stands out as the region's clearest adoption point for the immigration and visa management software market because of its role in cross-border talent flows and employer-sponsored mobility patterns.

- Envoy Global, Inc.

- Fragomen, Del Rey, Bernsen & Loewy, LLP

- Equifax Workforce Solutions

- Newland Chase Limited

- Jobbatical OU

- Localyze GmbH

- Equus Software, LLC

- Topia, Inc.

- xPath Global Pty Ltd

- Centuro Global Limited

- Docketwise

- Cerenade

- Boundless Immigration Inc.

- SimpleCitizen, Inc.

- Almaca, Inc.

- Sapochnick Technologies Inc.

- Imagility LLC

- Mitratech, Inc.

- CIBT Global, Inc.

- LaborLess

- US Immigration AI

- ImmiOne

- ImmiCompliance

- VisaHQ.com, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Employer Demand for Automated Visa and Work Authorization Compliance

- 4.2.2 Expansion of Cross-Border Hiring and Distributed Workforces

- 4.2.3 Shift to Cloud-Based and API-Integrated Immigration Platforms

- 4.2.4 Need for Audit-Ready Reporting and HRIS Integration

- 4.2.5 Convergence of Business Travel, Posted Worker, and Immigration Compliance

- 4.2.6 EES, ETIAS, and Digital Border Readiness Requirements

- 4.3 Market Restraints

- 4.3.1 Sensitive Immigration Data Security and Privacy Risks

- 4.3.2 Legacy Systems and Fragmented Data Ownership Slow Adoption

- 4.3.3 Smart-Border and AI-Driven Government Scrutiny Raising Audit Exposure

- 4.3.4 Portal-Native Filing Changes Increase Maintenance Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Application

- 5.3.1 Visa and Immigration Case Management

- 5.3.2 Compliance Management

- 5.3.3 Employee Mobility Management

- 5.3.4 Reporting and Analytics

- 5.3.5 Other Application Workflows

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 SMEs

- 5.5 By End-User

- 5.5.1 Corporates

- 5.5.2 Law Firms

- 5.5.3 Government and Public Sector Agencies

- 5.5.4 Educational Institutions

- 5.5.5 Other End-Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Envoy Global, Inc.

- 6.4.2 Fragomen, Del Rey, Bernsen & Loewy, LLP

- 6.4.3 Equifax Workforce Solutions

- 6.4.4 Newland Chase Limited

- 6.4.5 Jobbatical OU

- 6.4.6 Localyze GmbH

- 6.4.7 Equus Software, LLC

- 6.4.8 Topia, Inc.

- 6.4.9 xPath Global Pty Ltd

- 6.4.10 Centuro Global Limited

- 6.4.11 Docketwise

- 6.4.12 Cerenade

- 6.4.13 Boundless Immigration Inc.

- 6.4.14 SimpleCitizen, Inc.

- 6.4.15 Almaca, Inc.

- 6.4.16 Sapochnick Technologies Inc.

- 6.4.17 Imagility LLC

- 6.4.18 Mitratech, Inc.

- 6.4.19 CIBT Global, Inc.

- 6.4.20 LaborLess

- 6.4.21 US Immigration AI

- 6.4.22 ImmiOne

- 6.4.23 ImmiCompliance

- 6.4.24 VisaHQ.com, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment