|

시장보고서

상품코드

2073281

급여 선지급(EWA) 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Earned Wage Access (EWA) Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

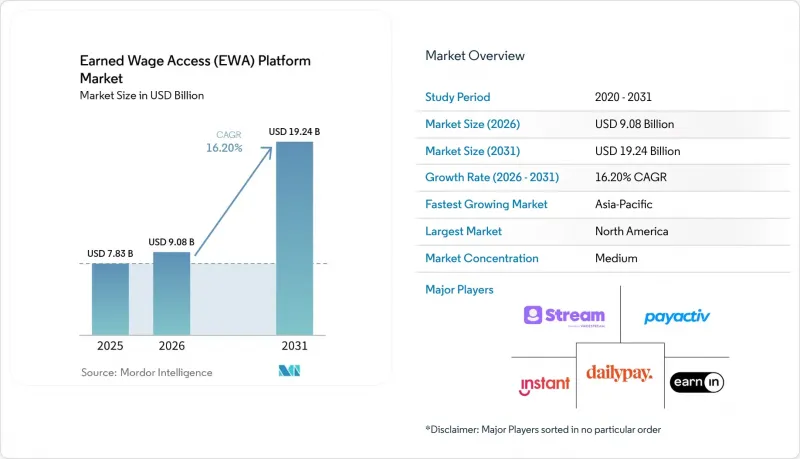

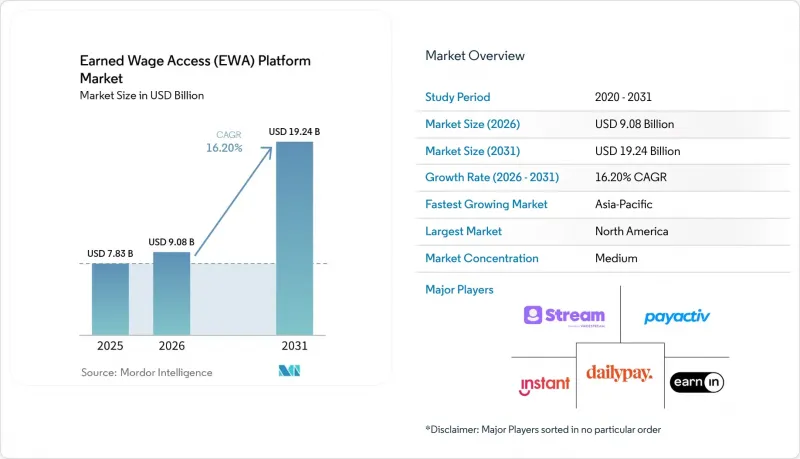

Mordor Intelligence에 의하면, 급여 선지급 플랫폼 시장 규모는 2025년에 78억 3,000만 달러로 평가되었습니다. 2026년에 90억 8,000만 달러에 달하고, 2031년까지 192억 4,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 16.2%로 성장할 전망입니다.

본 보고서는 제공 모델(고용주 통합형 급여 선지급 서비스(EWA), 소비자 직접형 급여 선지급 서비스(EWA) 등), 도입 모델(클라우드 기반, On-Premise형), 조직 규모(대기업 및 중소기업(SME)), 최종 사용자 산업(소매 및 전자상거래, 기타), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 급여 선지급(EWA) 플랫폼 시장 동향 및 인사이트

금융 웰니스 복리후생으로서의 “급여 선지급 서비스(EWA)"의 도입이 급증

의료 현장의 최전선에서 일하는 직원 중 절반 이상이 금전적 스트레스와 업무 성과 사이에 연관성이 있다고 응답한 조사 결과를 바탕으로, 고용주들은 온디맨드 급여를 단순한 부가적인 혜택에서 벗어나 재정적 웰니스 전략의 핵심 요소로 재정의했습니다. 간호사의 자발적 이직률이 감소함에 따라, 이직 1건을 방지할 때마다 5자리 수의 비용 절감 효과가 발생했고, 급여 선지급 서비스의 평가 기준이 인사 예산에서 CFO 수준의 비용 절감 지표로 전환되었습니다. 시급제 근로자의 압도적 다수가 주급 지급 또는 즉시 지급을 선택한다고 응답했음에도 불구하고, 고용주들의 도입은 여전히 더딘 상황이며, 이는 성장 여지가 크다는 것을 보여줍니다. SOC 2 및 GDPR(EU 개인정보보호규정)과 같은 감사 기준이 기본 요건으로 자리 잡은 가운데, 업계 최고 수준의 벤더들은 투명성이 높은 요금 체계와 변조가 불가능한 감사 추적을 통해 차별화를 꾀하고 있습니다. 이러한 요인들이 복합적으로 작용하여 민간 및 공공 부문의 고용주 모두에게서 수요를 공고히 하고 있습니다.

선진국 시장에서의 실시간 결제 인프라 확대

실시간 결제 시스템(미국의 FedNow, 유럽의 RTP, 호주의 New Payments Platform)은 2025년에 규모가 급격히 확대되었으며, 거래 한도가 상향 조정되고 금융기관의 참여도 늘어났습니다. 당일 결제를 통해 기존에 제공업체가 부담하던 사전 자금 조달로 인한 자금 정체 현상이 완화되거나 해소됨에 따라, 수수료 없는 급여 선지급이 경제적으로 지속 가능해졌습니다. 거래 한도 상향 조정으로 인해 중규모 급여 일괄 처리도 대상에 포함되게 되었으며, 고용주는 급여 선지급과 일반 급여 지급 모두에 단일 결제 경로를 이용할 수 있게 되었습니다. 그 결과, 공급업체는 선불 카드에 의존하지 않고도 근로자에게 즉시 지급을 약속할 수 있게 되었으며, 사용자 경험 조사에서 지적되었던 가장 큰 과제 중 하나가 해결되었습니다. 그 결과, 단위당 경제성이 구조적으로 개선되어 더 광범위한 지역으로의 확대가 가능해졌습니다.

대출과 비대출 분류와 관련된 규제상의 모호성

미국의 연방 지침에 따르면, 수수료 없이 고용주의 시스템에 통합된 ‘급여 선지급 서비스"는 대출 관련 법규의 적용 대상에서 제외되어 있지만, 각 주와 많은 해외 관할 구역에서는 여전히 송금업자나 소액 대출업자로서의 면허 취득을 의무화할 재량권을 보유하고 있습니다. 캘리포니아주의 정보 공개 의무와 코네티컷주의 등록 요건은 규정 준수 비용을 증가시켜, 신생 공급업체에게 특히 큰 부담이 되고 있습니다. 아시아태평양에서는 인도가 제공업체를 비은행계 금융회사로 취급함으로써 명확성을 제공하는 반면, 인도네시아 등에서는 여전히 수수료 상한선 및 라이선스 분류에 대한 논의가 계속되고 있습니다. 그 결과 발생하는 규제 불일치로 인해, 플랫폼은 단편적인 라이선스 취득을 강요받거나, 통일된 규정을 요구하며 로비 활동을 펼칠 수밖에 없게 되어, 여러 주로의 진출이 지연되고 법적 비용이 증가하고 있습니다. 성장을 위해서는 광범위한 지리적 확장이 필수적이기 때문에 이러한 지속적인 불확실성은 단기적인 사업 확장에 여전히 큰 걸림돌이 되고 있습니다.

부문별 분석

2025년, 고용주와 연계된 시스템은 급여 선지급(EWA) 플랫폼 시장에서 54.77%라는 가장 높은 점유율을 차지했습니다. 이는 대출 관련 규정 준수를 회피할 수 있는 수수료 없는 복리후생 제도를 우선시하는 대기업의 경향을 반영한 것입니다. 두 기능을 결합한 하이브리드형 플랫폼은 연평균 성장률(CAGR) 18.34%로 성장하고 있으며, 가장 성장세가 두드러지는 부문입니다. 그러나 긱 워커나, 기업 차원의 지원 프로그램이 없는 기업의 직원들에게는 소비자용 직접 앱이 여전히 필수적입니다. 이러한 솔루션은 예산 관리 대시보드, 저축 촉진 기능, 조기 이체 기능을 하나의 워크플로우로 통합하여, 종합적인 자금 관리를 원하는 근로자들의 요구를 충족시키고 있습니다. 최근 화이트 라벨 API의 등장으로, 급여 계산 업체들은 이러한 서비스를 기존 제품군에 통합할 수 있게 되었으며, 도입 기간을 몇 주로 단축할 수 있게 되었습니다. 이러한 융합은 단일 목적의 서비스가 쇠퇴하고 통합형 웰니스 스위트가 주류를 이루게 될 미래를 시사하며, 고용주, 급여 계산, 소비자와의 접점이 가장 넓은 플랫폼에 이익을 가져다주는 네트워크 효과를 더욱 강화할 것입니다.

하이브리드 모델은 고용주의 급여 데이터를 수집하는 동시에 자금을 근로자에게 직접 지급함으로써 규제 위험을 완화하고, 관할 구역별로 유연한 규정 준수 설정을 가능하게 합니다. 주요 제공업체의 보고서에 따르면, 하이브리드 모델 사용자들은 3개월 이내에 예산 관리나 목표 기반 저축과 같은 부가 서비스 중 최소 2가지를 이용하고 있으며, 이를 통해 고객 유지율과 교차 판매 수익이 향상되고 있습니다. 기업들이 규정 준수 요건과 근로자들의 선호도를 모두 충족할 수 있는 맞춤형 옵션을 모색함에 따라, 하이브리드 플랫폼에 할당되는 급여 선지급 시장 규모는 2031년까지 2배 이상으로 증가할 전망입니다.

2025년에는 On-Premise 도입이 매출의 66.67%를 차지했으나, 중견 기업들이 보다 신속한 가동 개시와 설비 투자 절감을 요구하는 가운데, 클라우드 도입은 연평균 성장률(CAGR) 18.71%를 나타낼 것으로 전망됩니다. Workday의 전략적 투자를 통해 DailyPay가 Workday의 클라우드 HCM 제품군에 직접 통합되어, 미들웨어로 인한 지연이 해소되었습니다. 클라우드 플랫폼은 매주 기능 업데이트를 실시하여 다중 리전에서의 이중화를 제공하는 한편, On-Premise 도입에 소요되는 시간의 극히 일부만으로 실시간 결제 시스템과 연동됩니다. 주요 HR 소프트웨어 공급업체들의 전략적 투자를 통해 클라우드 기반 급여 선지급 기능이 핵심 인력 관리 제품군에 직접 통합되면서, 이러한 아키텍처가 신규 도입 시 기본 설정으로 자리 잡아가고 있습니다.

엄격한 데이터 주권 규제가 적용되는 업계에서는 On-Premise 환경이 계속 사용되겠지만, 최상위 기업을 제외한 거의 모든 신규 계약에서 현재는 클라우드 도입이 명시되어 있습니다. 급여 선지급 플랫폼 시장에서는 벤더가 맞춤형 패치를 제공하는 대신, 테넌트 간에 보안 업그레이드를 통일할 수 있기 때문에 구체적인 효율성이 실현되고 있습니다. 또한, API 우선 클라우드 시스템을 통해 개발자 생태계의 개방이 용이해지면서, 급여 선지급 자산 거래나 자동 저축과 같은 부가 기능이 잇달아 등장하고 있어, 핵심 제안 가치를 한층 더 높이고 있습니다.

지역별 분석

북미는 2025년에 매출 점유율의 36.54%를 차지했습니다. 이는 성숙한 급여 계산 소프트웨어 생태계, 자금력이 탄탄한 공급업체, 그리고 7,400만 건의 거래를 처리한 FedNow 레일의 가동 시작에 힘입은 결과입니다. 연방 규제가 명확해짐에 따라 기업의 망설임이 더욱 해소되었고, 포춘 500대 기업에 선정된 고용주들 사이에서 도입이 가속화되었습니다. 캐나다와 멕시코에서는 고용주의 보증이 필요 없는 소비자 직접 판매 모델을 도입한 긱 경제 플랫폼에 힘입어 관심이 높아지고 있습니다.

아시아태평양은 성장의 원동력이 되고 있으며, 2031년까지 연평균 성장률(CAGR) 17.92%를 나타낼 것으로 전망됩니다. 인도에서는 프로바이더를 비은행계 금융회사로 분류함에 따라 부채를 통한 자금 조달의 길이 열렸고, 긱 근로자 수는 770만 명을 넘어섰습니다. 지역 기업들은 이러한 규제 측면의 호재를 활용하여 호주의 ‘New Payments Platform"와 싱가포르의 “FAST"시스템과 같은 실시간 결제 인프라를 활용하여 아시아 전역으로 사업 영역을 확대되고 있습니다. 중국, 일본, 한국에서는 전자상거래와 제조업을 중심으로 중간 수준의 도입이 진행되고 있습니다.

유럽에서는 SEPA 인스턴트 참여가 의무화되고, 회원국 간 즉시 결제가 표준화됨에 따라 꾸준한 성장세를 이어가고 있습니다. GDPR(EU 개인정보보호규정) 준수로 인해 초기 보안 비용이 증가하고 조달 주기가 길어지고 있지만, 일단 통합이 완료되면 기업 측에서는 차지백 감소와 직원 만족도 향상이 보고되고 있습니다. 남미에서는 아르헨티나의 지갑 기반 급여 지급에 관한 규제 논의가 플랫폼 간 제휴를 촉진하며 탄탄한 성장세를 보이고 있습니다. 한편, 브라질과 콜롬비아에서는 급여 선지급 이용 확대를 도모하기 위한 오픈 파이낸스 지침 마련이 시작되었습니다. 중동에서는 대규모 외국인 노동자층이 도입을 뒷받침하고 있으며, 8자리 규모의 합작 사업이 그 대표적인 사례입니다. 한편, 아프리카에서는 즉시 결제 인프라가 미비하고 소비자의 금융 이해도에도 편차가 있어, 아직 발전 단계에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the earned wage access (EWA) platform market size is expected to be USD 7.83 billion in 2025, USD 9.08 billion in 2026, and reach USD 19.24 billion by 2031, growing at a CAGR of 16.2% from 2026 to 2031.

This report is Segmented by Delivery Model (Employer-Integrated Earned Wage Access [EWA], Direct-To-Consumer Earned Wage Access [EWA], and More), Deployment Mode (Cloud-Based, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises [SMEs]), End-User Industry (Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Earned Wage Access (EWA) Platform Market Trends and Insights

Surging Adoption of Earned Wage Access as a Financial-Wellness Benefit

Employers have repositioned on-demand pay from a fringe perk to a central component of financial-wellness strategies, driven by survey evidence showing more than half of frontline healthcare staff link money stress to job performance. Lower voluntary turnover among nurses translated into five-figure savings per departure prevented, shifting evaluation of earned wage access from HR budgets to CFO-level cost-avoidance metrics. Hourly workers overwhelmingly state a preference for weekly or instant pay, yet employer adoption still lags, signaling significant headroom for growth. As audit standards such as SOC 2 and GDPR become baseline requirements, best-in-class vendors differentiate through transparent fee structures and immutable audit trails. Taken together, these factors anchor demand across both commercial and public-sector employers.

Expansion of Real-Time Payments Infrastructure in Developed Markets

Instant-settlement systems, FedNow in the United States, RTP in Europe, and the New Payments Platform in Australia, scaled dramatically during 2025, lifting transaction ceilings and widening financial-institution participation. Same-day clearing lowers or eliminates the pre-funding float previously carried by providers, making zero-fee wage advances economically sustainable. Higher transaction limits now cover mid-sized payroll batches, enabling employers to use a single rail for both advances and regular salary. In turn, vendors can promise workers immediate disbursement without relying on prepaid cards, addressing one of the largest pain points cited in user-experience surveys. The result is a structural improvement in unit economics that supports broader geographic rollouts.

Regulatory Ambiguity Around Lending Versus Non-Lending Classification

Federal guidance in the United States excludes fee-free, employer-integrated earned wage access from lending statutes, yet each state, and many foreign jurisdictions, retains discretion to impose money-transmitter or small-loan licensing. California's disclosure mandates and Connecticut's registration thresholds raise compliance costs that weigh heaviest on emerging vendors. In Asia-Pacific, India offers clarity by treating providers as non-banking financial companies, whereas Indonesia and others still debate fee caps and license categories. The resulting patchwork forces platforms into either piecemeal licensing or lobbying for harmonized rules, slowing multi-state rollouts and inflating legal overhead. Because growth requires wide geographic reach, persistent ambiguity remains a significant drag on near-term expansion.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Gig-Economy Workforce Across Asia-Pacific

- Intensifying Competition for Hourly Talent in Retail and Hospitality

- Data-Security and Privacy Concerns Among Large Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Employer-integrated systems commanded the largest slice of the Earned Wage Access (EWA) Platform market with 54.77% in 2025, a reflection of large organizations prioritizing zero-fee benefits that sidestep lending compliance. The blend of both hybrid platforms is the fastest-growing segment, expanding at an 18.34% CAGR. Direct-to-consumer apps, however, remain essential for gig workers and employees at firms without sponsored programs. These solutions weave budgeting dashboards, savings nudges, and early-deposit features into one workflow, addressing worker demand for holistic money management. Recent white-label API launches let payroll vendors bolt such services onto existing suites, shortening deployment to weeks. This convergence points to a future where single-purpose advances fade, and bundled wellness suites dominate, reinforcing network effects that reward platforms with the broadest employer, payroll, and consumer touchpoints.

Hybrid models also temper regulatory risk because they collect employer payroll data yet settle funds directly to workers, allowing dynamic compliance configurations by jurisdiction. Major providers report that hybrid users engage with at least two ancillary services, budgeting or goal-based savings, within three months, improving stickiness and cross-sell revenue. The earned wage access market size allocated to hybrid platforms is on track to more than double by 2031 as enterprises seek configurable options that satisfy both compliance and worker preference.

On-premise installs represented 66.67% of revenue in 2025, yet cloud deployments advance at an 18.71% CAGR, as mid-market firms look for faster go-lives and lower capital expenditure. Workday's strategic investment embedded DailyPay directly into its cloud HCM suite, eliminating middleware latency. Cloud platforms push weekly feature updates, provide multi-region redundancy, and integrate with real-time payment rails in a fraction of the time required for on-prem installs. Strategic investments from leading HR software vendors baked cloud earned wage access directly into core human-capital suites, cementing these architectures as default for greenfield implementations.

While on-premise will persist in industries subject to stringent data-sovereignty rules, practically every new contract below the top-tier enterprise category now specifies cloud deployment. The earned wage access platform market experiences tangible efficiency gains because vendors can unify security upgrades across tenants, rather than delivering custom patches. Moreover, API-first cloud systems make it straightforward to open developer ecosystems, spawning add-ons such as earned-asset trading or automated savings that amplify the core proposition.

Complete Report Scope:

- By Delivery Model

- Employer-Integrated Earned Wage Access (EWA)

- Direct-to-Consumer Earned Wage Access (EWA)

- Hybrid Models

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- Retail and E-Commerce

- Healthcare

- Manufacturing

- Hospitality and Food Service

- Transportation and Logistics

- Banking, Financial Services and Insurance (BFSI)

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.54% revenue share in 2025, underpinned by a mature payroll-software ecosystem, well-capitalized providers, and the operational debut of the FedNow rail that processed 74 million transactions. Federal regulatory clarity further thawed enterprise hesitancy, accelerating adoption among Fortune 500 employers. Canada and Mexico show rising interest, driven by gig-economy platforms embedding direct-to-consumer models that bypass employer sponsorship.

Asia-Pacific is the growth engine, advancing at a 17.92% CAGR through 2031. India's classification of providers as non-banking financial companies unlocked debt funding pathways, while the gig workforce vaulted beyond 7.7 million. Regional players use this regulatory runway to scale pan-Asian footprints, leveraging real-time payment infrastructure such as Australia's New Payments Platform and Singapore's FAST system. China, Japan, and South Korea report mid-tier uptake, anchored by the e-commerce and manufacturing sectors.

Europe maintains a steady trajectory as SEPA Instant participation becomes mandatory, standardizing immediate settlement across member states. GDPR compliance inflates upfront security costs, elongating procurement cycles, but once integrated, enterprises report fewer chargebacks and higher employee satisfaction. South America records solid momentum as regulatory discussions in Argentina about wallet-based payroll catalyze platform partnerships, while Brazil and Colombia start to craft open-finance guidelines conducive to earned wage access expansion. In the Middle East, large expatriate workforces underpin adoption, exemplified by eight-figure joint ventures, whereas Africa remains nascent due to patchy instant-payment rails and varying consumer financial literacy.

- Payactiv Inc.

- Earnin, Inc.

- DailyPay Inc.

- Wagestream Holdings Limited

- Instant Financial USA Inc.

- FlexWage Solutions LLC

- Even Responsible Finance, Inc.

- Branch Technologies Inc.

- Rain Technologies Inc.

- ZayZoon Inc.

- Clair Inc.

- Hastee Technologies Limited

- SalaryFinance Limited

- Refyne Tech Private Limited

- Tapcheck Inc.

- FinFit Ops LLC

- Immediate Solutions, Inc.

- Payflow S.L.

- Line Financial PBC

- Instapay Technologies Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Earned Wage Access as a Financial-Wellness Benefit

- 4.2.2 Expansion of Real-Time Payments Infrastructure in Developed Markets

- 4.2.3 Increasing Gig-Economy Workforce Across Asia-Pacific

- 4.2.4 Intensifying Competition for Hourly Talent in Retail and Hospitality

- 4.2.5 Growing Strategic Partnerships Between FinTechs and Traditional Payroll Vendors

- 4.2.6 Emergence of Embedded-Finance APIs Enabling White-Label EWA

- 4.3 Market Restraints

- 4.3.1 Regulatory Ambiguity Around Lending vs. Non-Lending Classification

- 4.3.2 Data-Security and Privacy Concerns Among Large Enterprises

- 4.3.3 Limited Financial Literacy Slowing User Uptake in Africa

- 4.3.4 Interchange-Fee Compression Pressuring Unit Economics

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Model

- 5.1.1 Employer-Integrated Earned Wage Access (EWA)

- 5.1.2 Direct-to-Consumer Earned Wage Access (EWA)

- 5.1.3 Hybrid Models

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Retail and E-Commerce

- 5.4.2 Healthcare

- 5.4.3 Manufacturing

- 5.4.4 Hospitality and Food Service

- 5.4.5 Transportation and Logistics

- 5.4.6 Banking, Financial Services and Insurance (BFSI)

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Payactiv Inc.

- 6.4.2 Earnin, Inc.

- 6.4.3 DailyPay Inc.

- 6.4.4 Wagestream Holdings Limited

- 6.4.5 Instant Financial USA Inc.

- 6.4.6 FlexWage Solutions LLC

- 6.4.7 Even Responsible Finance, Inc.

- 6.4.8 Branch Technologies Inc.

- 6.4.9 Rain Technologies Inc.

- 6.4.10 ZayZoon Inc.

- 6.4.11 Clair Inc.

- 6.4.12 Hastee Technologies Limited

- 6.4.13 SalaryFinance Limited

- 6.4.14 Refyne Tech Private Limited

- 6.4.15 Tapcheck Inc.

- 6.4.16 FinFit Ops LLC

- 6.4.17 Immediate Solutions, Inc.

- 6.4.18 Payflow S.L.

- 6.4.19 Line Financial PBC

- 6.4.20 Instapay Technologies Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment