|

시장보고서

상품코드

2073282

유럽의 EOR(Employer of Record) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Employer Of Record - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

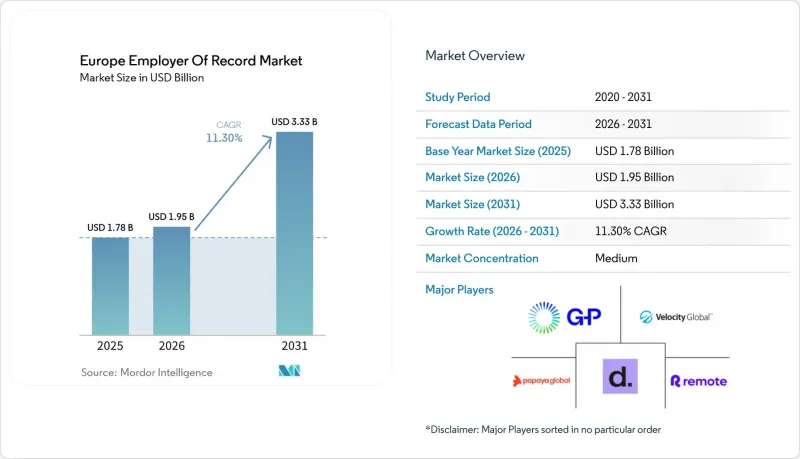

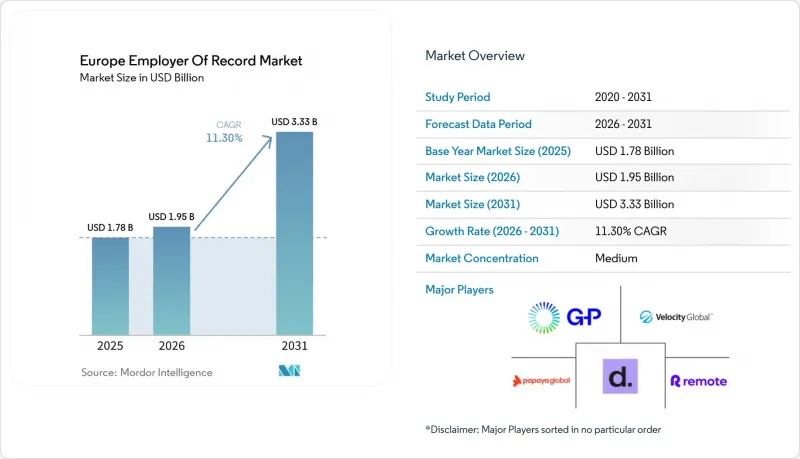

Mordor Intelligence에 의하면, 유럽의 EOR(Employer of Record) 시장 규모는 2025년에 17억 8,000만 달러로 평가되었습니다. 2026년에 19억 5,000만 달러에 달하고, 2031년까지 33억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.30%로 성장할 전망입니다.

본 보고서는 서비스 유형별(급여 계산·복리후생 관리, 컴플라이언스 관리, 세무 관리 등), 조직 규모별(중소기업 및 대기업), 업종별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 미디어 및 엔터테인먼트 등), 비즈니스 모델별(어그리게이터 모델 및 완전 자회사 모델), 그리고 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

유럽의 EOR(Employer of Record) 시장 동향 및 인사이트

국경을 초월한 원격 채용의 확대

인력 수요와 기업의 거점이 실무상 일치하지 않게 되면서, 국경을 초월한 채용은 유럽의 EOR 시장에 있어 여전히 가장 확실한 성장 동력 중 하나로 자리 잡고 있습니다. 2024년, 주요 EOR 플랫폼을 통해 채용된 신규 인력의 43%를 유럽이 차지하며, 국경을 초월한 인재 배치 활동에서 가장 많은 채용이 이루어진 지역이 되었습니다. 2025년에는 자금 조달을 완료한 스타트업 기업의 신규 해외 채용 중 12.2%를 차지한 영국이 채용 목적지로서 수요를 주도했으며, 독일이 8.8%로 그 뒤를 이었습니다. 또한, 유럽의 EOR 시장은 도입 의향의 변화로 인해 혜택을 보고 있습니다. 이는 더 많은 기업들이 인건비 절감을 목적으로 하는 것이 아니라, AI, 핀테크, 생명과학 분야의 희소 인재를 확보하기 위해 국경을 초월한 고용을 활용하고 있기 때문입니다. 1억 달러 이상의 자금을 조달한 스타트업은 첫 해외 채용을 시작한 지 18개월 이내에 국제적인 채용을 시작하는 경향이 강하며, 이로 인해 유럽의 주요 노동 시장 전반에 걸쳐 보다 철저한 규정 준수 체계를 갖춘 서비스 제공업체에 대한 프리미엄 수요가 뒷받침되고 있습니다.

복잡한 유럽 노동법 준수

유럽의 EOR(Employer of Record) 시장은 이 지역의 유례없이 세분화된 노동법 체계 덕분에 계속해서 지지를 얻고 있습니다. 이 지역에서는 채용, 해고, 급여 계산, 사회보장에 관한 의무가 통일된 체계가 아닌, 여전히 각국의 규정에 따르고 있습니다. 유럽 산업 원탁회의(European Round Table for Industry)는 2025년판 『단일 시장 개요(Single Market Compendium)』에서 노동법 및 근로자 파견에 관한 규정을 뿌리 깊은 국경 간 장벽으로 지적하고 있으며, 이는 유럽 각국을 개별적으로 대응하는 데 드는 비용이 높다는 사실을 뒷받침하고 있습니다. 실무 측면에서는 고용주가 여전히 프랑스, 독일, 이탈리아, 스페인 및 기타 주요 시장에서 서로 다른 계약 형태, 단체협약상의 의무, 근로자 보호 규정에 직면하고 있으며, 이로 인해 단일하고 표준화된 고용 체제의 가치가 제한되고 있습니다. 2025년 10월, 독일 연방고용청의 개정 지침에 따라 독일 국외에서만 근무하고 실제로 독일 국내에 입국하지 않는 직원은 AUG(라이선싱)의 라이선스 요건 대상에서 제외된다는 점이 명확히 밝혀진 것은 이러한 변동성을 여실히 보여주고 있습니다. 유럽의 “고용주 대리(Employer of Record)"시장은 이러한 규제 동향의 혜택을 받고 있습니다. 많은 다국적 기업의 인사팀은 모든 관할권에 걸친 해석의 변화를 실시간으로 파악할 수 없기 때문에 규정 준수 업무의 외부 위탁은 단순한 편의성에서 벗어나 사업 운영에 있어 필수 불가결한 요소로 변화하고 있습니다.

법정 고용 비용 부담의 무게

유럽의 EOR(Employer of Record) 시장은 서유럽 일부 국가에서 정규직 고용 비용이 높다는 과제에 여전히 직면해 있습니다. 프랑스, 이탈리아, 벨기에에서는 고용주 측의 법정 비용이 총 급여의 35%-47%를 추가로 부담하는 반면, 다른 많은 유럽 국가에서는 25%-35% 범위 내에 머물며, 덴마크, 루마니아, 헝가리에서는 5%-20%로 더욱 낮습니다. 이러한 비용은 EOR의 가격 책정에 직접 반영되므로, 사회보험료, 연금 부담금, 실업보험료, 건강보험료가 총 고용 비용에 완전히 포함될 경우, 고객사의 예산이 급증할 가능성이 있습니다. 그 결과, 실제로 인력 수요가 있는 경우에도 일부 구매 기업들은 비용이 높은 국가에서 정규직 전환을 미루거나 채용 계획을 축소하고 있습니다. 한편, 이러한 국가들에서는 해고에 관한 규제가 더 엄격하고 근로자 보호 제도도 보다 체계적으로 정비되어 있는 경우가 많기 때문에 고용 비용 부담이 전체 거래량 증가를 저해하는 경우에도 고용주는 업무상의 유연성을 중시하는 경향이 있어, 유럽의 EOR 시장은 여전히 중요한 위치를 차지하고 있습니다.

부문별 분석

2025년, 유럽의 EOR 시장 규모 중 급여 계산 및 복리후생 관리가 38.40%를 차지하며, 여전히 최대 서비스 유형으로서의 위상을 유지했습니다. 이러한 상황은 모든 EOR 계약이 여전히 현지 급여 계산의 이행, 법정 복리후생 가입 절차, 그리고 정확한 원천징수에 의존하고 있다는 현실을 반영하고 있습니다. 컴플라이언스 관리 부문은 현재 수익 점유율이 낮지만, 2026년부터 2031년까지 연평균 성장률(CAGR) 13.20%로 확대될 것으로 예상되며, 유럽의 EOR 시장에서 가장 빠르게 성장하고 있는 서비스 유형입니다. 이러한 성장 가속화는 “임금 투명성 지침",“플랫폼 근로 지침", 그리고 같은 시기에 유럽 전역에서 진행되고 있는 각국의 노동법 개정 잦은 개정이 맞물려 발생한 현상입니다. 세무 관리와 인사 아웃소싱은 여전히 서비스 구성의 중요한 부분을 차지하고 있으며, 특히 인사 아웃소싱은 고용 규정 준수 및 인사 운영을 단일 플랫폼에서 관리하고자 하는 구매자들 사이에서 지지를 넓혀가고 있습니다.

서비스 구성은 단순한 업무 처리에서 적극적인 모니터링으로 전환되고 있으며, 이에 따라 유럽의 EOR(Employer of Record) 시장에서 고객이 가치를 평가하는 방식도 변화하고 있습니다. 자동화된 규정 준수 알림과 급여 계산 처리를 결합한 서비스 제공업체는 인력 파견 중개업체라기보다는 규정 준수 인프라 파트너로서 평가받게 되었습니다. G-P가 2025년에 “G-P Gia"를 출범시킨 것은 이러한 방향성을 반영한 것입니다. 이 플랫폼은 180개국 이상의 고용법 변경 사항을 모니터링하고, 관련 문서를 작성하며, 규정 준수 조치를 안내하기 위해 구축되었습니다. 또한, 온보딩 지원 및 이민 절차 지원을 포함한 기타 서비스들도 기업들이 중동유럽으로 사업을 확장함에 따라 그 중요성이 커지고 있습니다. 해당 지역에서는 인재 공급이 사내 인사 부서의 대응 능력을 뛰어넘는 속도로 개선되고 있기 때문입니다. 기업의 실사 과정에서도 ISO 27001 인증 및 보다 광범위한 데이터 보안 대책이 중요시되고 있으며, 이에 따라 유럽의 고용주 대행 업계에서 유서 깊은 서비스 제공업체들에게는 차별화를 꾀할 수 있는 새로운 근거가 생겨나고 있습니다.

2025년, 유럽의 EOR(Employer of Record) 시장에서 대기업이 67.80%를 차지하며, 이 부문의 주요 수익 기반이 되었습니다. 이러한 우위는 규모에서 비롯된 것으로, 대기업 고객들은 단일 계약 체계 하에서 유럽 5개국 이상에서 급여 계산 및 고용 지원 서비스를 필요로 하는 경우가 많기 때문입니다. 유럽의 EOR(Employer of Record) 시장은 여러 관할 구역에 걸쳐 있는 노동평의회 조건 관리, 법정 복리후생 감사, 그리고 GDPR(EU 개인정보보호규정) 적용 대상인 직원 데이터 관리 부담을 경감하기 위해 이 그룹에게 여전히 매력적인 시장입니다. 또한, 여러 소규모 노동 시장을 아우르며 사업을 확장할 경우, 조달 팀이 규정 준수 책임 체계를 명확하게 통합할 수 있는 방안도 제공합니다. 이러한 요인들이 복합적으로 작용하여, 사업 확대 시기가 달라지더라도 대기업 수요는 비교적 견조한 추세를 보이고 있습니다.

중소기업(SME)은 2026년부터 2031년까지 연평균 성장률(CAGR) 13.80%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 조직 그룹이 될 전망입니다. 이러한 성장을 뒷받침하고 있는 것은 Deel, Remote, RemoFirst와 같은 ‘기술 우선"의 제공업체가 있다는 점입니다. 이 기업들은 계약 요건을 완화하고, 온보딩 절차를 간소화하며, 소규모 구매자를 대상으로 가격 책정을 더욱 투명하게 만들었습니다. 또한, Deel의 2026년 세계 채용 데이터에 따르면, 1억 달러 이상의 자금을 조달한 스타트업은 첫 해외 채용 후 18개월 이내에 국경을 넘어선 채용을 진행하는 경향이 뚜렷한데, 이는 중소기업 수요 일부가 단순한 유기적 성장뿐만 아니라 자금 조달 주기와도 관련이 있음을 시사합니다. 유럽의 고용주 대행(EOR) 시장에서 나타나는 또 다른 추세는 “하이브리드형 조달"입니다. 이는 해외 직원 수가 80-200명 규모인 기업이, 직원 수가 적은 국가의 경우 단일 세계 EOR을 이용하고, 독일이나 프랑스 등 복잡성이 높은 시장의 경우 전문 서비스 제공업체를 활용하는 형태를 말합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe employer of record market size is projected to be USD 1.78 billion in 2025, USD 1.95 billion in 2026, and reach USD 3.33 billion by 2031, growing at a CAGR of 11.30% from 2026 to 2031.

This report is Segmented by Service Type (Payrolling and Benefits Administration, Compliance Management, Tax Management, and More), Organization Size (SMEs, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Media and Entertainment, and More), Business Model (Aggregator Model, and Wholly-Owned Model), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Employer Of Record Market Trends and Insights

Cross-Border Remote Hiring Expansion

Cross-border hiring remains one of the clearest growth engines for the Europe employer of record market because talent demand and legal entity footprints no longer line up in a practical way. Europe captured 43% of all new hires processed on major EOR platforms in 2024, which made it the most-sourced region for cross-border placement activity. The United Kingdom led destination demand in 2025 with 12.2% of new international hires tracked among funded startups, while Germany followed with 8.8%. The Europe employer of record market is also benefiting from a change in hiring intent, because more companies now use cross-border employment to secure scarce talent in AI, fintech, and life sciences rather than to chase lower labor costs. Startups that raise at least USD 100 million are more likely to begin international hiring within 18 months of their first overseas hire, which supports premium demand for providers with deeper compliance infrastructure across major European labor markets.

Complex European Labor Law Compliance

The Europe employer of record market continues to draw support from the region's unusually fragmented labor law structure, where hiring, dismissal, payroll, and social security obligations still follow national rules rather than a unified framework. The European Round Table for Industry identified labor and posting-of-workers rules as a persistent cross-border obstacle in its 2025 Single Market Compendium, which reinforces the cost of navigating Europe country by country. In practical terms, employers still face different contract forms, collective agreement obligations, and worker protection rules in France, Germany, Italy, Spain, and other major markets, which limit the value of a single standardized employment setup. Germany illustrated this volatility in October 2025 when revised Federal Employment Agency guidance clarified that employees working exclusively outside Germany without physical travel into the country are not subject to AUG licensing requirements. The Europe employer of record market benefits from this kind of regulatory movement because many multinational HR teams cannot monitor shifting interpretations across all jurisdictions in real time, which turns outsourced compliance from a convenience into an operating necessity.

High Statutory Employment Cost Burden

The Europe employer of record market still faces friction from the high cost of formal employment in several Western European countries. In France, Italy, and Belgium, employer-side statutory costs can add 35%-47% to gross payroll, while many other European countries fall in the 25%-35% range, and Denmark, Romania, and Hungary sit lower at 5%-20%. Those charges are passed through directly in EOR pricing, which means client budgets can rise sharply once social contributions, pension obligations, unemployment insurance, and health coverage are fully loaded into total employment cost. The result is that some buyers delay permanent employee conversion or narrow hiring plans in high-cost countries even when talent demand is real. At the same time, those same countries often impose stricter termination frameworks and more formal worker protections, so the Europe employer of record market still retains relevance because employers value operational flexibility even when the employment cost burden weighs on overall volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Payroll, Benefits, and Tax Administration

- EU Pay Transparency Directive Readiness

- Regulatory Fragmentation Across European Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payrolling and benefits administration held 38.40% of the Europe employer of record market size in 2025, which kept it as the largest service type. This position reflects the practical reality that every EOR engagement still depends on local payroll execution, statutory benefits enrollment, and accurate tax withholding. Compliance management, while smaller in current revenue share, is projected to expand at a 13.20% CAGR from 2026 to 2031, which makes it the fastest-growing service type in the Europe employer of record market. That acceleration is tied to the combined effect of the Pay Transparency Directive, the Platform Work Directive, and frequent national labor law updates that are moving through the region at the same time. Tax Management and HR Outsourcing remain important parts of the service mix, and HR Outsourcing is gaining ground among buyers who want employment compliance and people operations handled on a single platform.

The service mix is shifting from transaction execution toward proactive monitoring, which changes how buyers assess value in the Europe employer of record market. Providers that combine automated compliance alerts with payroll processing are increasingly being evaluated as compliance infrastructure partners rather than as staffing intermediaries. G-P's launch of G-P Gia in 2025 reflected that direction because the platform was built to monitor employment law changes, create documentation, and guide compliance responses across more than 180 countries. Other service types, including onboarding support and immigration assistance, are also picking up relevance as companies expand into Central and Eastern Europe where talent supply is improving faster than internal HR coverage. Enterprise due diligence is now also placing more weight on ISO 27001 certification and broader data security controls, which gives established providers another basis for differentiation in the Europe employer of record industry.

Large enterprises accounted for 67.80% of the Europe employer of record market in 2025, which made them the core revenue base for the category. Their lead comes from scale, because enterprise clients often need payroll and employment support across 5 or more European countries under a single contractual framework. The Europe employer of record market remains attractive to this group because it reduces the burden of managing works council terms, statutory benefit audits, and GDPR-sensitive employee data across multiple jurisdictions. It also gives procurement teams a cleaner way to consolidate compliance ownership when expansion is spread across several smaller labor markets. That combination keeps enterprise demand relatively durable even when expansion timing changes.

SMEs are projected to expand at a 13.80% CAGR from 2026 to 2031, making them the fastest-growing organizational cohort. This growth has been helped by technology-first providers such as Deel, Remote, and RemoFirst, which lowered commitment thresholds, simplified onboarding, and made pricing more transparent for smaller buyers. Deel's 2026 global hiring data also showed that startups raising at least USD 100 million were more likely to hire across borders within 18 months of their first international hire, which links part of SME demand to funding cycles rather than only to organic growth. Another pattern in the Europe employer of record market is hybrid procurement, where companies with 80-200 international employees use one global EOR for lower-volume countries and specialist providers for high-complexity markets such as Germany and France.

Complete Report Scope:

- By Service Type

- Payrolling and Benefits Administration

- Compliance Management

- Tax Management

- HR Outsourcing

- Other Service Types

- By Organization Size

- SMEs

- Large Enterprises

- By Industry Vertical

- IT and Telecom

- BFSI

- Media and Entertainment

- Healthcare and Lifesciences

- Manufacturing

- Retail and E-commerce

- Other Industry Verticals

- By Business Model

- Aggregator Model

- Wholly-Owned Model

- By Geography

- United Kingdom

- Germany

- France

- Netherlands

- Nordics

- Spain

- Italy

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Globalization Partners LLC

- Deel Inc.

- Remote Technology, Inc.

- Velocity Global, LLC

- Papaya Global Ltd.

- Oyster HR, Inc.

- Multiplier Technologies Pte. Ltd.

- Atlas Technology Solutions, Inc.

- WorkMotion Software GmbH

- RemoFirst Inc.

- Safeguard Global

- Playroll Limited

- Native Teams Limited

- Boundless Technologies

- Lano Software GmbH

- Omnipresent

- Remote People

- Mauve Group

- Mercans

- Acumen International

- Skuad

- Horizons

- New Horizons Global Partners

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cross-Border Remote Hiring Expansion

- 4.2.2 Complex European Labor Law Compliance

- 4.2.3 Entity-Light Market Entry for Low-Headcount Expansion

- 4.2.4 Rising Demand for Payroll, Benefits, and Tax Administration

- 4.2.5 EU Pay Transparency Directive Readiness

- 4.2.6 Contractor-to-Employee Conversion After Reclassification Tightening

- 4.3 Market Restraints

- 4.3.1 High Statutory Employment Cost Burden

- 4.3.2 Regulatory Fragmentation Across European Jurisdictions

- 4.3.3 Labor Leasing Limits in Highly Regulated Markets

- 4.3.4 Customer Migration to Own-Entity Models at Scale

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Payrolling and Benefits Administration

- 5.1.2 Compliance Management

- 5.1.3 Tax Management

- 5.1.4 HR Outsourcing

- 5.1.5 Other Service Types

- 5.2 By Organization Size

- 5.2.1 SMEs

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Media and Entertainment

- 5.3.4 Healthcare and Lifesciences

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Other Industry Verticals

- 5.4 By Business Model

- 5.4.1 Aggregator Model

- 5.4.2 Wholly-Owned Model

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Netherlands

- 5.5.5 Nordics

- 5.5.6 Spain

- 5.5.7 Italy

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Globalization Partners LLC

- 6.4.2 Deel Inc.

- 6.4.3 Remote Technology, Inc.

- 6.4.4 Velocity Global, LLC

- 6.4.5 Papaya Global Ltd.

- 6.4.6 Oyster HR, Inc.

- 6.4.7 Multiplier Technologies Pte. Ltd.

- 6.4.8 Atlas Technology Solutions, Inc.

- 6.4.9 WorkMotion Software GmbH

- 6.4.10 RemoFirst Inc.

- 6.4.11 Safeguard Global

- 6.4.12 Playroll Limited

- 6.4.13 Native Teams Limited

- 6.4.14 Boundless Technologies

- 6.4.15 Lano Software GmbH

- 6.4.16 Omnipresent

- 6.4.17 Remote People

- 6.4.18 Mauve Group

- 6.4.19 Mercans

- 6.4.20 Acumen International

- 6.4.21 Skuad

- 6.4.22 Horizons

- 6.4.23 New Horizons Global Partners

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment