|

시장보고서

상품코드

2073294

기지국 안테나 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Base Station Antenna - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

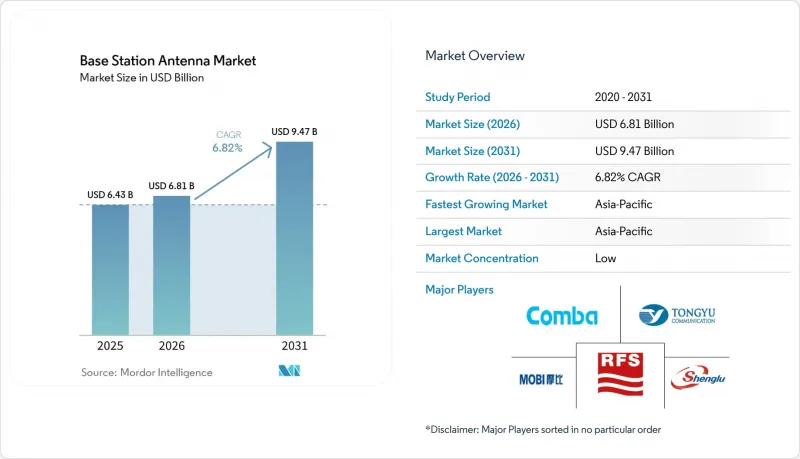

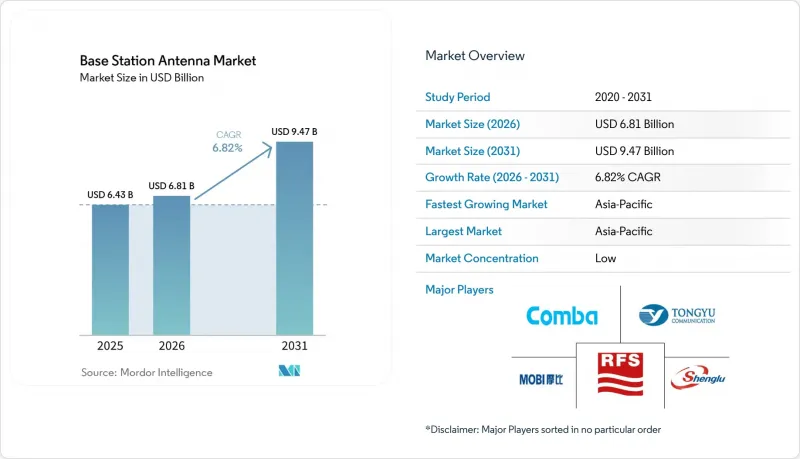

Mordor Intelligence에 의하면, 기지국 안테나 시장 규모는 2025년 64억 3,000만 달러로 평가되었습니다. 2026년에는 68억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.82%로 성장을 지속하여, 2031년에는 94억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 안테나 유형(매크로셀 안테나, 스몰셀 안테나), 기술(3G, 4G/LTE, 5G), 주파수 대역(저대역, 1GHz 미만, 중대역, 1GHz-6GHz, 고대역 등), 구축 방식(타워 설치형, 옥상 설치형, 폴 설치형, 벽면 설치형, 기타), 편파(단일 편파, 이중 편파, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 기지국 안테나 시장 동향 및 인사이트

5G 및 5G-Advanced 매크로 네트워크 구축 가속화

기지국 안테나 시장은 상용 5G 네트워크의 기반 확대와 5G-Advanced로의 조기 전환에 힘입어 꾸준한 성장세를 보이고 있습니다. 2026년 4월, 전 세계적으로 392개의 통신 사업자가 5G 네트워크를 상용화했으며, 35개사가 5G-Advanced에 대한 투자를 진행했습니다. 이에 따라 안테나 수요는 새로운 서비스 범위 확대와 업그레이드 프로그램 모두와 밀접한 관련이 있습니다. 이는 비스탠드얼론(NSA)에서 스탠드얼론(SA)으로, 그리고 5G-Advanced로 전환되는 과정에서 단순히 무선 장비를 교체하는 것이 아니라 새로운 안테나 교체 주기가 생겨나기 때문에 중요한 의미를 지닙니다. 에릭슨과 T-Mobile은 2026년에 AI 네이티브 RAN 스케줄링을 통해 실제 운영 네트워크에서 성과를 보고했습니다. 여기에는 스펙트럼 효율 10% 향상과 다운링크 처리량 최대 15% 개선이 포함되어 있으며, 이는 사이트 수준에서 더욱 정교한 안테나와 무선 장비의 조합이 갖는 가치를 입증합니다. 이러한 전개 과정에서는 더 넓은 대역폭과 높은 이득을 가진 어레이가 선호됩니다. 왜냐하면 업링크 강화, 캐리어 어그리게이션, 그리고 멀티밴드 운용은 기존의 4G 시대 안테나 장착 방식으로는 대응하기 어렵기 때문입니다. 그 결과, 네트워크의 진화가 새로운 하드웨어 주기를 주도하고 있기 때문에 이미 광범위한 지역을 커버하고 있는 국가들에서도 기지국 안테나 시장은 계속해서 확대되고 있습니다.

모바일 데이터 트래픽 증가와 도시 지역의 네트워크 고밀도화

기지국 안테나 시장은 모바일 데이터 트래픽의 지속적인 성장과 인구 밀집 도시 지역에서 나타나는 트래픽 집중 현상에 힘입어 성장하고 있습니다. 에릭슨의 예측에 따르면, 전 세계 모바일 네트워크 데이터 트래픽은 2031년까지 월간 310 엑사바이트에 달할 것이며, 5G 트래픽의 비중은 2024년 말 34%에서 2031년까지 83%로 상승할 전망입니다. 미국에서만 2024년 모바일 데이터 사용량은 132조 메가바이트를 기록하며 전년 대비 35% 증가했습니다. 이는 성숙한 시장에서도 용량에 대한 부담이 여전히 증가하고 있음을 보여줍니다. 이로 인해 투자 양상이 양극화되고 있습니다. 예를 들어, 인구 밀도가 높은 도심 지역에서는 용량 확보를 위해 보다 정교한 빔포밍이나 섹터 안테나가 필요한 반면, 교외나 도시 외곽 지역에서는 더 넓은 커버리지를 확보하기 위해 여전히 고이득 어레이가 요구되고 있습니다. 스몰셀 포럼은 2026년을 확장 가능한 스몰셀 구축에 있어 중요한 해로 보고 있습니다. 이는 안테나 공급업체들이 현재 매크로 기지국의 업그레이드뿐만 아니라, 더 고밀도인사이트 구축에 필요한 운영 프레임워크에도 관여하고 있음을 의미합니다. 따라서 기지국 안테나 시장은 단기적인 설비 투자의 급증보다는 구조적인 트래픽 패턴의 혜택을 받고 있으며, 이것이 장기적인 업그레이드 여지를 뒷받침하고 있습니다.

높은 사이트 투자 비용과 장기화되는 인허가 절차

기지국 안테나 시장은 여전히 사이트 경제성과 지방자치단체의 승인 절차 지연이라는 현실적인 장벽에 직면해 있습니다. Alpha Wireless는 2025년, 미국에서 기존 매크로 타워의 허가를 취득하는 데 평균 12개월이 소요된 반면, 여러 지자체가 관여하는 경우 5G의 완전한 고밀도화에 대한 승인을 받는 데는 수년이 걸릴 수도 있다고 지적했습니다. 또한 FCC는 워싱턴주 서스턴 카운티의 건당 신청 수수료 2만 5,776달러와 뉴멕시코주 그랜트 카운티의 1만 7,500달러 등, 규정을 준수하지 않은 것으로 간주될 수 있는 지방자치단체의 수수료를 특정했습니다. 이러한 수수료는 새로운 안테나 설치 비용을 하드웨어 자체의 비용을 훨씬 웃도는 수준으로 끌어올릴 가능성이 있으므로 중요한 문제입니다. 2025년 9월에 발효된 FCC의 “Build America"규정 제정은 이러한 장벽을 낮추는 것을 목표로 하고 있지만, 그 과정에는 시간이 소요되며, 사업 전개에 있어 경제성은 당장 바뀌지 않습니다. 승인 절차가 단축되고 요금 체계가 더 예측 가능해질 때까지는 통신 사업자들이 네트워크 고밀도화에 대해 선택적인 태도를 유지할 것이며, 그 결과 단기적인 안테나 설치 수는 트래픽 증가만으로는 정당화될 수 있는 수준에 미치지 못한 채로 남아 있을 것입니다.

부문별 분석

2025년, 매크로셀 안테나는 61.33%의 시장 점유율을 차지하며 기지국 안테나 시장의 상업적 기반을 형성했습니다. 이러한 위상은 5G 미드밴드 프로그램에서 광역 커버리지에 대한 지속적인 수요와, 구형 듀얼밴드 어레이를 포트 수가 많은 멀티밴드 제품으로 교체하는 추세를 반영하고 있습니다. 인구가 밀집된 도시 지역에서는 통신 사업자들이 용량과 주파수 대역 효율을 우선시함에 따라, 능동형 안테나 시스템과 매시브 MIMO 장치가 기존의 수동형 섹터 하드웨어를 대체하는 추세가 강해지고 있습니다. 에릭슨의 2025년 무선·안테나 제품 출시 주기를 통해, 프로그래밍이 가능하고 개방형 표준을 지원하는 매크로 안테나 제품군이 신규 사이트 구축 및 업데이트 활동에서 핵심적인 역할을 담당하고 있음이 드러났습니다.

반면, 트래픽 부하가 하이엔드 빔 스티어링에 수반되는 추가 비용이나 복잡성을 정당화할 수 없는 교외나 지방의 네트워크에서는 기존의 섹터형 및 멀티빔 제품이 여전히 그 입지를 유지하고 있습니다. 콤바 텔레콤은 MWC 2026에서 에너지 효율이 뛰어난 매크로 안테나를 통신 사업자의 조달 요구에 보다 직접적으로 부응하도록 포지셔닝하며, 자사의 “Helifeed 3.0" 아키텍처와 전 대역에 걸쳐 20% 이상의 에너지 효율 향상을 강조했습니다. 스몰 셀 안테나는 가장 빠르게 성장하고 있는 부문으로, 2031년까지 연평균 성장률(CAGR)이 7.21%를 나타낼 것으로 전망됩니다. 이는 실내 시스템의 중요성이 커지고, 거리 수준의 밀집도가 높아지며, 특정 대상에 초점을 맞춘 용량 증강이 이루어지고 있음을 반영한 것입니다. 스몰 셀 포럼은 2026년을 “도입의 결정적인 해"라고 규정하고 있으며, 알파 와이어리스는 이에 부응하기 위해 AW4032 Fusion 플랫폼 등, 도로 시설에 설치할 수 있는 설계를 이미 제공합니다. 이 플랫폼은 경관을 고려해야 하는 장소에서도 듀얼 밴드 지원과 360° 전방향 성능을 구현하고 있습니다.

5G 부문은 기지국 안테나 시장에서 가장 빠르게 성장하고 있는 기술 분야로, 2031년까지의 연평균 성장률(CAGR)은 7.42%입니다. 이러한 성장은 전 세계적으로 이어지고 있는 서비스 출시 추세, 독립형 코어로의 전환, 그리고 5G-Advanced의 초기 단계에서의 보급을 지속적으로 반영하고 있습니다. 2026년 4월, 전 세계적으로 392개의 통신 사업자가 5G 네트워크를 상용화했으며, 35개사가 5G-Advanced에 대한 투자를 진행하고 있습니다. 이를 통해 성숙 시장과 신흥 시장 모두에서 업그레이드 경로가 유지되고 있습니다. 5G 중에서도 Sub-6GHz 대역은 주류 구축의 커버리지 특성에 부합하기 때문에 여전히 안테나 출하 대수가 가장 많습니다. 한편, 고주파 대역의 시스템은 인구 밀집 지역이나 고정 무선 접속 분야에서 보다 선택적으로 활용되고 있습니다. KDDI와 교세라는 2025년, 소형 리피터 및 메쉬 설계를 통해 도쿄 지역의 mm파 도로 커버리지를 대폭 개선할 수 있음을 입증했습니다. 이는 전면적인 확대가 아니라, 대상을 좁혀 고주파 대역을 도입하는 것이 장기적으로 효과적임을 뒷받침하는 것입니다.

2025년에도 4G/LTE는 기지국 안테나 시장 규모의 45.89%를 차지했으며, 향후 성장의 초점이 대부분 5G에 맞추어져 있음에도 불구하고 LTE가 여전히 상당한 상업적 비중을 차지하고 있음을 보여줍니다. 이는 특히 아프리카, 남아시아, 남미에서 두드러지게 나타나며, 이들 지역에서는 통신 사업자들이 5G 전환을 위한 3GHz 미만 대역의 주파수 재할당을 추진하는 한편, LTE의 밀도 향상도 지속적으로 추진하고 있습니다. 화웨이의 FDD 트라이밴드 Massive MIMO 플랫폼은 이 ‘브리지 전략"의 명확한 예입니다. 이는 동일한 설치 면적 내에서 현재의 LTE 용량을 향상시키면서, 향후 5G로의 진화를 위한 현실적인 로드맵을 확보하기 때문입니다. 그 결과, 하나의 안테나 플랫폼이 현재의 4G 트래픽과 향후 5G 확장을 모두 지원해야 하기 때문에 기존의 기술 업데이트 주기는 짧아지고 그 경계도 모호해지고 있습니다.

지역별 분석

아시아태평양은 2025년 기지국 안테나 시장 규모의 37.32%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.74%로 확대될 것으로 전망됩니다. 이 지역은 중국이 대규모 5G 교체 주기를 맞이하고, 인도가 활발한 고밀도화 단계에 있으며, 일본과 한국 등 선진 시장이 네트워크 아키텍처를 발전시키고 있는 만큼, 다층적인 성장 패턴의 혜택을 누리고 있습니다. 이를 통해 매크로 안테나의 대량 수요와 매시브 MIMO 및 광대역 안테나와 관련된 고부가가치 업그레이드 모두를 뒷받침하고 있습니다. 일본은 이러한 두 가지 패턴을 모두 구현하고 있으며, 에릭슨의 4.5GHz 매시브 MIMO 무선 장비가 NTT 도코모의 본격적인 운용 네트워크에 도입되었고, 소프트뱅크는 실외에서 7GHz 현장 검증을 진행하고 있습니다. 아시아태평양은 매크로, 실내, 멀티밴드 구성에 걸친 제품의 발전을 주도하면서, 기지국 안테나 시장의 주요 수요 거점으로 자리매김하고 있습니다.

북미는 아시아태평양에 비해 출하 대수는 적지만, 금액 기준으로는 기지국 안테나 시장에서 확고한 입지를 차지하고 있습니다. 에릭슨은 2030년까지 북미의 활성 스마트폰 1대당 모바일 데이터 트래픽이 증가할 것으로 전망하고 있으며, 이 회사의 FWA(고정 무선 액세스)에 대한 전망에 따르면 주요 통신 사업자의 고정 무선 가입자 수가 증가할 것으로 예상되어, 고부가가치 안테나 도입을 촉진하고 있습니다. 프라이빗 5G는 새로운 수요층을 창출하고 있으며, 대기업 및 산업용 프로그램을 통해 공공 통신 사업자의 설비 투자 주기와는 별개로 안테나 수요 기회가 만들어지고 있습니다. FCC가 무선망 구축의 장벽을 낮추기 위한 노력을 통해 허가 취득 기간이 단축된다면, 북미는 아시아태평양에 비해 타워 수 증가세가 둔화되고 있음에도 불구하고 사이트당 수익을 평균 이상으로 유지할 수 있을 것입니다.

유럽에서는 5G 안테나에 대한 투자가 견조한 추세를 보이고 있는 반면, 중동 및 아프리카와 남미에서는 각각 다른 성장 양상을 보이고 있습니다. 유럽의 견조한 상황은 독립형 방식의 확산과 FWA에 대한 관심 고조에 힘입은 바가 크며, 노키아가 EOLO와 공동으로 이탈리아에서 진행한 사업은 도시 및 지방의 광대역 통신 분야에서 mm파가 수행하는 역할을 여실히 보여주고 있습니다. 중동은 주파수 경제 측면에서 유리한 여건을 갖추고 있으며, GSMA는 사우디아라비아의 광범위한 주파수 할당과 통신 사업자의 낮은 주파수 비용을 지적하고 있는데, 이로 인해 기지국 및 안테나 조달이 가속화되고 있습니다. 아프리카와 남미에서는 통신 사업자들이 4G 네트워크 밀도를 높이고 5G를 단계적으로 도입함에 따라, 주파수 효율이 뛰어나고 멀티밴드를 지원하며 커버리지를 고려한 설계에 대한 수요가 증가하고 있으며, 이것이 성장의 원동력이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the base station antenna market size is expected to grow from USD 6.43 billion in 2025 to USD 6.81 billion in 2026 and is forecast to reach USD 9.47 billion by 2031 at 6.82% CAGR over 2026-2031.

This report is Segmented by Antenna Type (Macro Cell Antenna, and Small Cell Antenna), Technology (3G, 4G/LTE, and 5G), Frequency Band (Low Band, Sub-1 GHz, Mid Band, 1 GHz-6 GHz, High Band, and More), Deployment Type (Tower-Mounted, Rooftop, Pole-Mounted, Wall-Mounted, and More), Polarization (Single Polarized, Dual Polarized, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Base Station Antenna Market Trends and Insights

Accelerating 5G and 5G-Advanced Macro Network Rollouts

The base station antenna market is drawing steady support from the widening base of commercial 5G networks and the early move toward 5G-Advanced. By April 2026, 392 operators had launched 5G networks globally, and 35 operators were investing in 5G-Advanced, which keeps antenna demand tied to both new coverage and upgrade programs. This matters because the move from non-standalone to standalone, and then to 5G-Advanced, creates another round of antenna replacements rather than a one-time radio swap. Ericsson and T-Mobile reported live-network gains from AI-native RAN scheduling in 2026, including a 10% increase in spectral efficiency and up to a 15% improvement in downlink throughput, reinforcing the value of more advanced antenna and radio combinations at the site level. These rollout paths favor wider-bandwidth and higher-gain arrays, because enhanced uplink, carrier aggregation, and multi-band operation are difficult to support with legacy 4G-era mounts. The result is that the base station antenna market continues to expand, even in countries where macro coverage is already broad, as network evolution drives new hardware cycles.

Rising Mobile Data Traffic and Urban Network Densification

The base station antenna market is also being lifted by sustained growth in mobile data traffic and the heavier traffic concentration now seen in dense urban zones. Ericsson forecast that global mobile network data traffic will reach 310 exabytes per month by 2031, while 5G traffic share will rise from 34% at the end of 2024 to 83% by 2031. The United States alone recorded 132 trillion megabytes of mobile data usage in 2024, up 35% from the prior year, which shows that capacity pressure is still increasing even in mature markets. This creates a split investment pattern, such as dense urban sites require more advanced beamforming and sector antennas for capacity, while suburban and peri-urban sites still need higher-gain arrays for broader coverage. Small Cell Forum has identified 2026 as a critical year for scalable small-cell deployment, which means antenna suppliers are now tied not only to macro upgrades but also to the operational frameworks needed for denser site rollouts. The base station antenna market, therefore, benefits from a structural traffic pattern rather than a short-term capex spike, which supports a longer upgrade runway.

High Site CapEx and Lengthy Permitting Cycles

The base station antenna market still faces a practical brake from site economics and the slow pace of local approvals. Alpha Wireless noted in 2025 that a traditional macro tower permit in the United States averaged 12 months, while full 5G densification approvals could stretch across several years when multiple municipalities were involved. The FCC also identified local fees that it viewed as potentially non-compliant, including single-application charges of USD 25,776 in Thurston County, Washington, and USD 17,500 in Grant County, New Mexico. Those charges matter because they can push the cost of a new antenna placement well above the hardware cost itself. The FCC's Build America rulemaking, issued in September 2025, seeks to lower these barriers, but the process will take time and not immediately change deployment economics. Until approval cycles shorten and fee structures become more predictable, operators will remain selective about densification, which keeps near-term antenna volumes below what traffic growth alone would justify.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Massive MIMO and Higher-Port Multiband Antennas

- Expansion of Private 5GaAnd Fixed Wireless Access Networks

- Spectrum Allocation Delays and Regulatory Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Macro cell antennas held a 61.33% share in 2025, making them the commercial foundation of the base station antenna market. Their position reflects the continuing need for wide-area coverage in 5G mid-band programs and the replacement of older dual-band arrays with higher-port multiband products. In dense urban sites, active antenna systems and massive MIMO units have increasingly displaced conventional passive sector hardware as operators prioritize capacity and spectral efficiency. Ericsson's 2025 radio and antenna launch cycle showed that programmable, open-ready macro portfolios are becoming central to new site builds and refresh activity.

At the same time, traditional sector and multibeam products still hold their place in suburban and rural networks where traffic loads do not justify the added cost and complexity of high-end beam steering. Comba Telecom used MWC 2026 to position energy-efficient macro antennas more directly in line with operator procurement needs, highlighting its Helifeed 3.0 architecture and an energy-efficiency improvement of more than 20% across the full band. Small cell antennas are the fastest-growing segment, with a 7.21% CAGR through 2031, reflecting the rising role of indoor systems, street-level densification, and targeted capacity builds. The Small Cell Forum has described 2026 as a decisive deployment year, and Alpha Wireless has already responded with street-furniture-ready designs, such as the AW4032 Fusion platform, which supports dual-band coverage and 360° omnidirectional performance in visually sensitive locations.

The 5G segment is the fastest-growing technology layer in the base station antenna market, with a 7.42% CAGR through 2031. That growth continues to reflect ongoing global launch activity, the shift toward standalone cores, and the early spread of 5G-Advanced. By April 2026, 392 operators had launched 5G networks worldwide, and 35 were investing in 5G-Advanced, which keeps the upgrade path active across both mature and emerging markets. Within 5G, Sub-6 GHz continues to generate the most antenna volume because it aligns with the coverage geometry of mainstream rollouts, while higher-band systems are used more selectively in dense zones and for fixed wireless access. KDDI and Kyocera demonstrated in 2025 that compact repeater mesh designs could materially improve mmWave street coverage in Tokyo, supporting the long-term case for targeted high-band deployment rather than blanket rollout.

4G/LTE retained 45.89% of the base station antenna market size in 2025, which shows that LTE still carries real commercial weight even as 5G absorbs most of the future growth focus. This is especially true in Africa, South Asia, and South America, where operators continue LTE densification while also refarming sub-3 GHz assets for 5G migration. Huawei's FDD tri-band Massive MIMO platform is a clear example of this bridge strategy, because it improves current LTE capacity while preserving a practical path toward later 5G evolution on the same site footprint. The result is that the traditional technology replacement cycle is becoming shorter and less distinct, because one antenna platform now has to support both current 4G traffic and future 5G expansion.

Complete Report Scope:

- By Antenna Type

- Macro Cell Antenna

- Sector Antenna

- Active Antenna System

- Massive MIMO Antenna

- Multibeam Antenna

- Small Cell Antenna

- Outdoor Small Cell Antenna

- Indoor Small Cell Antenna

- Macro Cell Antenna

- By Technology

- 3G

- 4G/LTE

- 5G

- 5G Sub-6 GHz

- 5G mmWave

- By Frequency Band

- Low Band, Sub-1 GHz

- Mid Band, 1 GHz-6 GHz

- 1 GHz-2.6 GHz

- 3.3 GHz-4.2 GHz

- 4.4 GHz-6.0 GHz

- High Band and Above 24 GHz

- By Deployment Type

- Tower-Mounted

- Rooftop

- Pole-Mounted

- Wall-Mounted

- Ground-Based

- By Polarization

- Single Polarized

- Vertical Polarization

- Horizontal Polarization

- Dual-Polarized

- Circular-Polarized

- Single Polarized

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific accounted for 37.32% of the base station antenna market size in 2025 and is projected to expand at a 7.74% CAGR through 2031. The region benefits from a layered growth pattern, with China undergoing a large-scale 5G refresh cycle, India in an active densification phase, and advanced markets like Japan and South Korea advancing network architecture. This supports both high-volume macro demand and higher-value upgrades tied to massive MIMO and wider-band antennas. Japan exemplifies this dual-track pattern, with Ericsson's 4.5 GHz massive MIMO radios entering NTT DOCOMO's production network and SoftBank advancing outdoor 7 GHz field verification. Asia-Pacific remains the main volume center of the base station antenna market while driving product evolution across macro, indoor, and multiband configurations.

North America holds a strong position in the base station antenna market by value, despite lower unit volumes compared to Asia-Pacific. Ericsson projects rising mobile data traffic per active smartphone in North America through 2030, with its FWA outlook showing increased fixed wireless subscriptions among major operators, supporting higher-value antenna deployments. Private 5G adds another demand layer, with large enterprise and industrial programs creating antenna opportunities outside the public carrier capex cycle. If FCC efforts to reduce wireless deployment barriers improve permitting timelines, North America will maintain above-average revenue per site despite slower tower growth compared to Asia-Pacific.

Europe maintains steady 5G antenna investment, while the Middle East, Africa, and South America show distinct growth patterns. Europe's position is supported by standalone rollout activity and growing FWA interest, with Nokia's Italy deployment with EOLO highlighting mmWave's role in urban and rural broadband. The Middle East benefits from supportive spectrum economics, with the GSMA noting Saudi Arabia's broad spectrum assignment and lower operator spectrum costs, which accelerate base-station and antenna procurement. In Africa and South America, growth is driven by the need for spectrum-efficient, multiband, and coverage-aware designs as operators expand 4G density and gradually adopt 5G.

- Comba Telecom Systems Holdings Limited

- Tongyu Communication Inc.

- Radio Frequency Systems GmbH

- Alpha Wireless Ltd.

- CellMax Technologies AB

- Quintel USA, Inc.

- MatSing

- Guangdong Broadradio Communication Technology Co., Ltd.

- Guangdong Shenglu Telecommunication Tech. Co., Ltd.

- Mobi Antenna Technologies (Shenzhen) Co., Ltd.

- MTI Wireless Edge Ltd.

- Antenna Technologies Limited Company

- Airplux Technologies Limited

- POYNTING Antennas (Pty) Ltd.

- Galtronics USA, Inc.

- Xi'an Haitian Antenna Technologies Co., Ltd.

- Sanny Telecom Equipment Co.,Ltd.

- Kathreiin SE

- ACE Technologies Corp.

- JMA, LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Accelerating 5G and 5G-Advanced Macro Network Rollouts

- 4.3.2 Rising Mobile Data Traffic and Urban Network Densification

- 4.3.3 Shift Toward Massive MIMO and Higher-Port Multiband Antennas

- 4.3.4 Expansion of Private 5G and Fixed Wireless Access Networks

- 4.3.5 Mid-Band Spectrum Refarming Driving Tri-Band Retrofit Cycles

- 4.3.6 Open RAN and Neutral-Host Architectures Expanding Interoperable Antenna Demand

- 4.4 Market Restraints

- 4.4.1 High Site CapEx and Lengthy Permitting Cycles

- 4.4.2 Spectrum Allocation Delays and Regulatory Fragmentation

- 4.4.3 Tower Loading and Wind-Load Limits on Large Array Upgrades

- 4.4.4 Tariffs, Localization Rules, and RF Component Sourcing Volatility

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Antenna Type

- 5.1.1 Macro Cell Antenna

- 5.1.1.1 Sector Antenna

- 5.1.1.2 Active Antenna System

- 5.1.1.3 Massive MIMO Antenna

- 5.1.1.4 Multibeam Antenna

- 5.1.2 Small Cell Antenna

- 5.1.2.1 Outdoor Small Cell Antenna

- 5.1.2.2 Indoor Small Cell Antenna

- 5.1.1 Macro Cell Antenna

- 5.2 By Technology

- 5.2.1 3G

- 5.2.2 4G/LTE

- 5.2.3 5G

- 5.2.3.1 5G Sub-6 GHz

- 5.2.3.2 5G mmWave

- 5.3 By Frequency Band

- 5.3.1 Low Band, Sub-1 GHz

- 5.3.2 Mid Band, 1 GHz-6 GHz

- 5.3.2.1 1 GHz-2.6 GHz

- 5.3.2.2 3.3 GHz-4.2 GHz

- 5.3.2.3 4.4 GHz-6.0 GHz

- 5.3.3 High Band and Above 24 GHz

- 5.4 By Deployment Type

- 5.4.1 Tower-Mounted

- 5.4.2 Rooftop

- 5.4.3 Pole-Mounted

- 5.4.4 Wall-Mounted

- 5.4.5 Ground-Based

- 5.5 By Polarization

- 5.5.1 Single Polarized

- 5.5.1.1 Vertical Polarization

- 5.5.1.2 Horizontal Polarization

- 5.5.2 Dual-Polarized

- 5.5.3 Circular-Polarized

- 5.5.1 Single Polarized

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Comba Telecom Systems Holdings Limited

- 6.4.2 Tongyu Communication Inc.

- 6.4.3 Radio Frequency Systems GmbH

- 6.4.4 Alpha Wireless Ltd.

- 6.4.5 CellMax Technologies AB

- 6.4.6 Quintel USA, Inc.

- 6.4.7 MatSing

- 6.4.8 Guangdong Broadradio Communication Technology Co., Ltd.

- 6.4.9 Guangdong Shenglu Telecommunication Tech. Co., Ltd.

- 6.4.10 Mobi Antenna Technologies (Shenzhen) Co., Ltd.

- 6.4.11 MTI Wireless Edge Ltd.

- 6.4.12 Antenna Technologies Limited Company

- 6.4.13 Airplux Technologies Limited

- 6.4.14 POYNTING Antennas (Pty) Ltd.

- 6.4.15 Galtronics USA, Inc.

- 6.4.16 Xi'an Haitian Antenna Technologies Co., Ltd.

- 6.4.17 Sanny Telecom Equipment Co.,Ltd.

- 6.4.18 Kathreiin SE

- 6.4.19 ACE Technologies Corp.

- 6.4.20 JMA, LLC.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment