|

시장보고서

상품코드

2073303

AI 이력서 심사 및 매칭 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Resume Screening and Matching - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

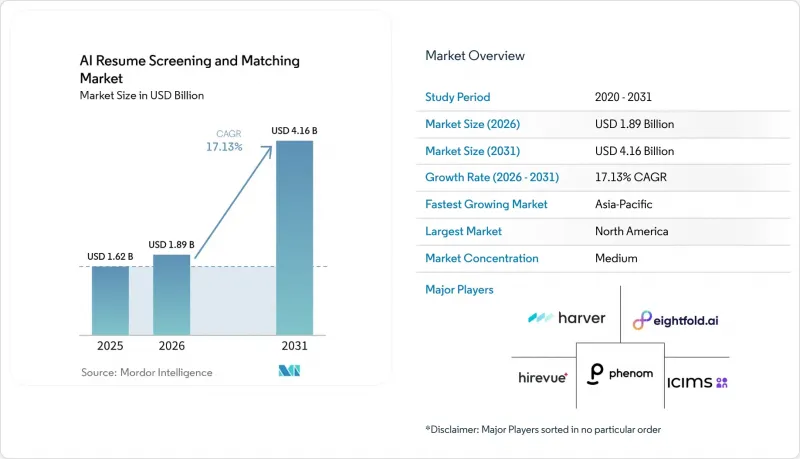

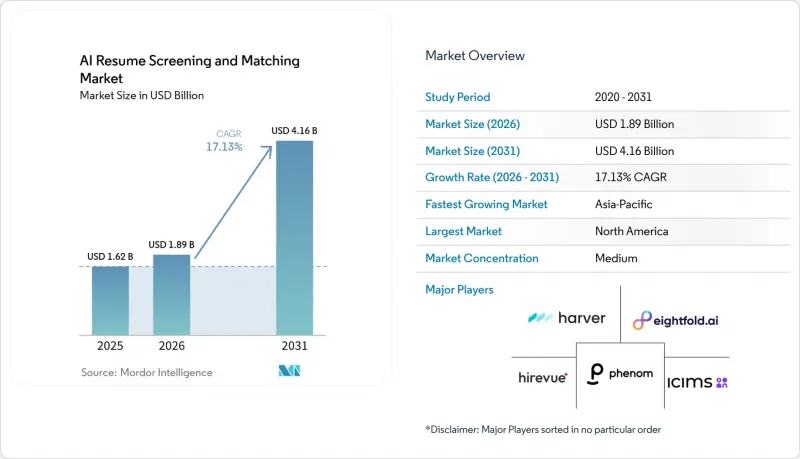

Mordor Intelligence에 의하면, AI 이력서 심사 및 매칭 시장 규모는 2025년 16억 2,000만 달러로 평가되었습니다. 2026년에는 18억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 17.13%로 성장을 지속하여, 2031년에는 41억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 모델(On-Premise 및 클라우드 기반), 조직 규모(중소기업 및 대기업), 최종 이용 산업(정보기술·통신, 헬스케어 및 생명과학, 소매 및 전자상거래 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 AI 이력서 심사 및 매칭 시장 동향 및 인사이트

온라인 구인 지원 건수의 급증

2021년부터 2025년에 걸쳐 지원 건수는 거의 두 배로 증가했으나, 채용 담당자의 대응 능력이 수요를 따라가지 못해 채용 완료 건수는 감소했습니다. 지원자가 AI로 생성된 이력서를 제출하는 사례가 늘어나면서 정보의 질이 떨어지고 있습니다. 따라서 고용주는 키워드 필터로는 50% 미만에 그치는 반면, 최대 89%의 적격 후보자를 발굴할 수 있는 시맨틱 검색을 도입할 수밖에 없습니다. 수동 선별 작업을 AI로 대체한 채용 담당자는 처리 속도가 5배 향상되고 채용 대응 능력이 40% 개선되었다고 보고하고 있지만, 현재 워크플로우의 병목 현상은 보상 조건 조정 및 승인 절차에 집중되어 있습니다. 고용주들은 이러한 과제를 해결하기 위해 첨단 채용 기술에 대한 투자를 확대되고 있습니다.

경쟁이 치열한 노동 시장에서 채용까지 걸리는 기간을 단축해야 한다는 압박

AI 네이티브 플랫폼은 일정 조정, 자격 확인, 근무 배정을 자동화함으로써 평균 채용 기간을 기존 중앙값의 절반인 14일로 단축했습니다. AI 검색을 활용하는 기술 분야 채용 담당자의 경우, 20일 이내에 인재를 배치할 수 있는 확률이 56% 높아졌으며, 이를 조기에 도입한 기업에는 선구자로서의 우위가 주어지고 있습니다. 신규 직책에 대해 과거 지원자나 직원을 선별하는 사내 이동 플랫폼을 통해 채용까지 소요되는 시간을 40% 단축하고 인재 확보 비용을 절감할 수 있게 되었으며, 2024년 채용자의 44%는 외부 파이프라인이 아닌 기존 후보자 데이터베이스에서 채용되었습니다.

알고리즘의 편향과 불균형한 영향에 관한 소송 위험

지원자 중 고작 26%만이 AI에 의한 공정한 평가를 신뢰하지 않으며, “Mobley v. Workday"와 같은 주목도가 높은 소송으로 인해 원고 측의 책임론이 벤더 자체로까지 확대되면서, 도입 비용이 급등하고 보급 속도가 둔화되고 있습니다. 기업은 구조적인 위험 완화 조치를 도입하여, AI 처리에 앞서 지원자의 성명 및 인구통계학적 속성을 익명화하고, 제3자에 의한 공정성 감사를 실시하며, 모든 최종 결정에 있어 “휴먼 인 더 루프"에 의한 심사를 유지하고 있습니다. 그러나 이러한 관리 조치는 비용과 처리 지연을 초래하여 효율성 향상으로 얻는 이점을 부분적으로 상쇄하고 있습니다. 또한, 규제의 파편화로 인해 여러 법역에 걸친 컴플라이언스 프로그램이 필요하게 되었으며, 소규모 공급업체의 경우 이를 유지하기가 어려워지고 있습니다.

부문별 분석

AI 이력서 선별 및 매칭 시장에서 2025년 매출의 67.21%를 소프트웨어가 차지했습니다. 그 핵심은 비정형 문서에서 정형화된 필드를 추출하는 파싱 엔진과, 8억 건 이상프로파일을 스캔하여 문맥적 적합성을 평가하는 매칭 엔진입니다. 이러한 도구 덕분에 1차 심사 소요 시간이 5분의 1로 단축되었으며, 2021년 이후 채용 담당자의 업무 처리 능력이 40% 향상되었습니다. 서비스 분야(도입, 교육, 관리형 심사)는 연평균 성장률(CAGR) 19.04%가 예상되며, 현재는 ISO 27001 인증을 획득한 워크플로우를 패키지화하여, 전문가의 감독 하에 매월 150건 이상의 후보자 평가를 수행하고 있습니다. 기업들은 소프트웨어만으로는 해결할 수 없는 편향성 감사나 여러 시스템 간의 통합에 대응하기 위해 이러한 서비스를 선택하고 있습니다.

소프트웨어가 여전히 핵심을 차지하고 있지만, 구매자들은 워크플로우 재설계나 변경 관리 지침서를 포함하는 컨설팅 서비스를 함께 도입하는 경향이 강해지고 있습니다. 채용 프로세스 아웃소싱 파트너 기업들은 자동화와 이중언어 구사 분석가 팀을 결합함으로써 운영 비용을 20-30% 절감할 수 있다고 주장하고 있지만, 인사 담당 임원의 88%는 여전히 그 가치가 충분히 실현되지 않고 있다고 보고하고 있으며, 이는 AI 이력서 심사·매칭 업계에서 도입 성숙도에 대한 더욱 집중된 노력이 필요함을 시사하고 있습니다.

2025년에는 On-Premise 도입 비중이 59.88%를 유지했습니다. 이는 현지화된 데이터 관리가 필요한 금융, 헬스케어 및 중동 고객들로부터 지지를 받았기 때문입니다. 이러한 환경에서는 감사에 대응할 수 있는 로그가 생성되며, 사용자 정의 API를 통해 기존 인사 정보 시스템과 통합됩니다. 한편, AI 이력서 심사·매칭 시장 솔루션의 클라우드 도입은 ISO 27001 및 SOC 2 Type II 인증이 최고정보보안책임자(CISO)의 요건을 충족하기 때문에 20.02%의 성장이 예상됩니다.

클라우드 플랫폼은 실시간 기능 출시, 사용량에 따른 과금 체계, 그리고 중소기업이 중요하게 여기는 120개 이상의 지원자 추적 시스템용 커넥터 등을 추진하고 있습니다. 하이브리드 모델도 널리 보급되어 있으며, 개인을 식별할 수 있는 정보는 On-Premise에 보관하는 한편, 벤더의 클라우드 환경에서 익명화된 학습을 가능하게 함으로써 데이터 주권과 알고리즘의 지속적인 업데이트 간의 균형을 맞추고 있습니다.

지역별 분석

북미는 초기 단계 벤처 자금 조달과 높은 신청 건수에 힘입어 2025년 AI 이력서 심사 및 매칭 시장 매출의 36.61%를 차지했습니다. 그러나 주마다 규정이 제각각이기 때문에 현재는 여러 관할 구역에 걸친 편향성 감사 및 후보자에 대한 통지가 의무화되어 있어, 공급업체들은 설정 가능한 규정 준수 엔진을 구축해야 하는 상황에 놓여 있습니다. 캐나다와 멕시코는 미국에 비해 뒤처져 있지만, 영어·프랑스어 및 영어·스페인어 워크플로우를 지원하는 이중 언어 분석을 통해 도입을 확대되고 있습니다.

유럽은 2025년 수요의 약 25-28%를 차지했습니다. 2026년 8월부터 시행되는 EU AI법은 데이터셋의 문서화와 인간에 의한 검토를 의무화하고 있으며, 기업들은 감사 대시보드 도입과 6개월간의 로그 보관을 요구받고 있습니다. GDPR(EU 개인정보보호규정)에 따른 특별 범주 데이터의 제한으로 인해, 공급업체는 직접적인 인구통계학적 항목을 사용하지 않고 공정성을 추론해야 하지만, 이는 여전히 발전 중인 관행입니다. 동유럽 시장은 서유럽 시장에 비해 뒤처져 있지만, 이탈리아와 스페인에서는 청년층 고용 촉진 정책에 힘입어 클라우드 도입이 가속화되고 있는 반면, 러시아는 제재의 영향을 받지 않는 국내 플랫폼에 의존하고 있습니다.

아시아태평양은 인도의 아웃소싱 거점, 중국의 제조업 분야 인재 채용, 그리고 고령화되는 노동력에 따른 일본의 후계자 양성 수요에 힘입어 연평균 성장률(CAGR) 18.77%를 나타낼 것으로 전망됩니다. 2026년 5월 항저우에서 내려진 판결에서는 AI에 의한 자동화만을 이유로 한 해고를 제한하고, 효율성과 고용 안정성 간의 균형을 도모하겠다는 규제 당국의 의지가 드러났습니다. 한국, 호주, 중동에서는 엄격한 데이터 거주지 규제를 준수하면서도 채용에 소요되는 시간을 60-75% 단축하기 위해 하이브리드형 도입으로 전환하고 있는 반면, 남미와 아프리카에서는 인프라 격차로 인해 도입이 여전히 초기 단계에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the AI resume screening and matching market size is expected to grow from USD 1.62 billion in 2025 to USD 1.89 billion in 2026 and is forecast to reach USD 4.16 billion by 2031 at a 17.13% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (On-Premises, and Cloud-Based), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-Use Industry (Information Technology and Telecom, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Resume Screening and Matching Market Trends and Insights

Accelerating Volume of Online Job Applications

Application volumes nearly doubled between 2021 and 2025, yet completed hires slipped as recruiter capacity lagged demand. Candidates increasingly submit AI-generated resumes, degrading signal quality and compelling employers to deploy semantic search that delivers up to 89% qualified-candidate discovery versus sub-50% for keyword filters. Recruiters that replaced manual screening with AI reported five-fold speed gains and 40% greater requisition capacity, though workflow bottlenecks now center on compensation alignment and approval cycles.Employers are increasingly investing in advanced recruitment technologies to address these challenges.

Tightening Time-to-Hire Pressures in Competitive Labor Markets

AI-native platforms compressed average time-to-fill to 14 days, half the traditional median, by automating scheduling, credential checks, and shift matching. Technical recruiters using AI search are 56% more likely to place talent within 20 days, giving early adopters a first-mover advantage. Internal mobility platforms that surface historical applicants and employees for new roles enable 40% faster fills and lower sourcing costs, with 44% of 2024 hires drawn from existing candidate databases rather than external pipelines.

Algorithmic Bias and Disparate Impact Litigation Risks

Only 26% of applicants trust AI to assess them fairly, and high-profile cases such as Mobley v. Workday have expanded plaintiffs' theories of liability to vendors themselves, raising implementation costs and slowing adoption. Enterprises are implementing structural mitigations, anonymizing candidate names and demographic attributes before AI processing, conducting third-party fairness audits, and maintaining human-in-the-loop review for all final decisions. Yet these controls add cost and latency that partially offset efficiency gains, and regulatory fragmentation requires multi-jurisdictional compliance programs that smaller vendors struggle to sustain.

Other drivers and restraints analyzed in the detailed report include:

- Growing Availability of Pre-Trained Large Language Models

- Rising Compliance Requirements for Fair-Hiring Regulations

- Data-Privacy Restrictions Limiting Candidate Data Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software commanded 67.21% of 2025 revenue in the AI resume screening and matching market, led by parsing engines that extract structured fields from unstructured documents and matching engines that scan 800 million-plus profiles for contextual fit. These tools shorten initial screening by 5 times and sustain recruiter bandwidth growth of 40% since 2021. The services segment, implementation, training, and managed screening, is forecast for a 19.04% CAGR and now packages ISO 27001-certified workflows that deliver 150+ monthly candidate evaluations with human oversight. Organizations select services to navigate bias audits and multi-system integrations that pure software cannot solve.

While software remains the backbone, buyers increasingly bundle consulting that redesigns workflows and embeds change-management playbooks. Recruitment process outsourcing partners claim 20-30% operating-expense savings by blending automation with bilingual analyst teams, yet 88% of HR leaders still report unrealized value, signaling that the AI resume screening and matching industry needs stronger focus on adoption maturity.

On-premises installations maintained 59.88% share in 2025, favored by finance, healthcare, and Middle East clients that require localized data stewardship. These environments produce audit-ready logs and integrate with legacy HR information systems through custom APIs. Cloud deployment of AI resume screening and matching market solutions, however, is projected to grow at 20.02% as ISO 27001 and SOC 2 Type II certifications satisfy chief information security officers.

Cloud platforms push real-time feature releases, usage-based pricing, and more than 120 applicant-tracking connectors that SMEs value. Hybrid models are spreading, keeping personally identifiable information on-premises while allowing anonymized learning in vendor clouds, balancing sovereignty against constant algorithm updates.

Complete Report Scope:

- By Component

- Software

- Resume Parsing Engines

- Candidate Matching Engines

- Screening and Ranking Tools

- Talent Intelligence / Skills Graph Platforms

- Other Software

- Services

- Implementation and Integration Services

- Training and Support Services

- Managed / Outsourced Screening Services

- Software

- By Deployment Model

- On-Premises

- Cloud-Based

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-Use Industry

- Information Technology and Telecom

- Banking, Financial Services and Insurance

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing

- Other End-Use Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America captured 36.61% of AI resume screening and matching market revenue in 2025, buoyed by early-stage venture funding and high application volumes. However, fragmented state rules now require multi-jurisdictional bias audits and candidate notices, prompting vendors to build configurable compliance engines. Canada and Mexico trail the United States but are scaling adoption through bilingual parsing that supports English-French and English-Spanish workflows.

Europe contributed roughly 25-28% of 2025 demand. The EU AI Act, enforceable from August 2026, mandates dataset documentation and human review, pushing enterprises to adopt audit dashboards and maintain six-month log retention. GDPR's limits on special-category data oblige vendors to infer fairness without direct demographic fields, a still-evolving practice. Eastern markets lag Western peers, yet Italy and Spain are accelerating cloud uptake under youth-employment initiatives, while Russia leans on domestic platforms insulated by sanctions.

Asia-Pacific is set to post an 18.77% CAGR, led by India's outsourcing hubs, China's manufacturing recruitment, and Japan's succession-planning needs tied to an aging workforce. A May 2026 Hangzhou ruling restricted terminations tied solely to AI automation, signaling regulatory intent to balance efficiency with job security. South Korea, Australia, and the Middle East are moving to hybrid deployments to navigate strict data-residency laws yet still achieve 60-75% hiring-time reductions, whereas South America and Africa remain nascent adoption zones hindered by infrastructure gaps.

- HireVue Inc.

- iCIMS Inc.

- Modern Hire, Inc.

- Eightfold AI, Inc.

- Phenom People, Inc.

- Harver B.V.

- Pymetrics, Inc.

- SeekOut, Inc.

- Lever, Inc.

- XOR Inc.

- Humanly.io, Inc.

- Talview, Inc.

- Restless Bandit, Inc.

- Textkernel B.V.

- Oleeo plc

- Beamery Limited

- PredictiveHire Ltd. (trading as Sapia.ai)

- Ideal Inc.

- Skillate Labs Pvt. Ltd.

- hireEZ Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Volume of Online Job Applications

- 4.2.2 Tightening Time-to-Hire Pressures in Competitive Labor Markets

- 4.2.3 Growing Availability of Pre-Trained Large Language Models

- 4.2.4 Rising Compliance Requirements for Fair-Hiring Regulations

- 4.2.5 Integration of Skills-Based Talent Intelligence Platforms

- 4.2.6 Adoption of AI-Driven Internal Mobility Programs

- 4.3 Market Restraints

- 4.3.1 Algorithmic Bias and Disparate Impact Litigation Risks

- 4.3.2 Data-Privacy Restrictions Limiting Candidate Data Use

- 4.3.3 Low AI Readiness Among Small Recruiting Teams

- 4.3.4 Budget Freezes Amid Macroeconomic Slowdowns

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Resume Parsing Engines

- 5.1.1.2 Candidate Matching Engines

- 5.1.1.3 Screening and Ranking Tools

- 5.1.1.4 Talent Intelligence / Skills Graph Platforms

- 5.1.1.5 Other Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Training and Support Services

- 5.1.2.3 Managed / Outsourced Screening Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud-Based

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-Use Industry

- 5.4.1 Information Technology and Telecom

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Other End-Use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HireVue Inc.

- 6.4.2 iCIMS Inc.

- 6.4.3 Modern Hire, Inc.

- 6.4.4 Eightfold AI, Inc.

- 6.4.5 Phenom People, Inc.

- 6.4.6 Harver B.V.

- 6.4.7 Pymetrics, Inc.

- 6.4.8 SeekOut, Inc.

- 6.4.9 Lever, Inc.

- 6.4.10 XOR Inc.

- 6.4.11 Humanly.io, Inc.

- 6.4.12 Talview, Inc.

- 6.4.13 Restless Bandit, Inc.

- 6.4.14 Textkernel B.V.

- 6.4.15 Oleeo plc

- 6.4.16 Beamery Limited

- 6.4.17 PredictiveHire Ltd. (trading as Sapia.ai)

- 6.4.18 Ideal Inc.

- 6.4.19 Skillate Labs Pvt. Ltd.

- 6.4.20 hireEZ Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment