|

시장보고서

상품코드

2073307

BFSI 분야 급여 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Payroll Software In BFSI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

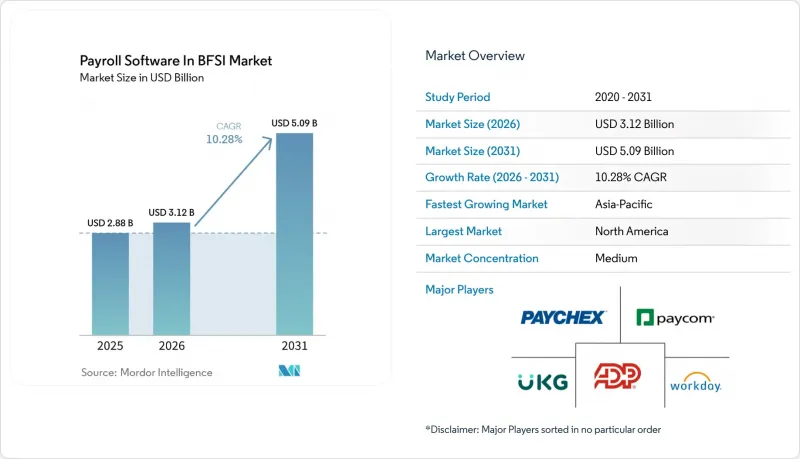

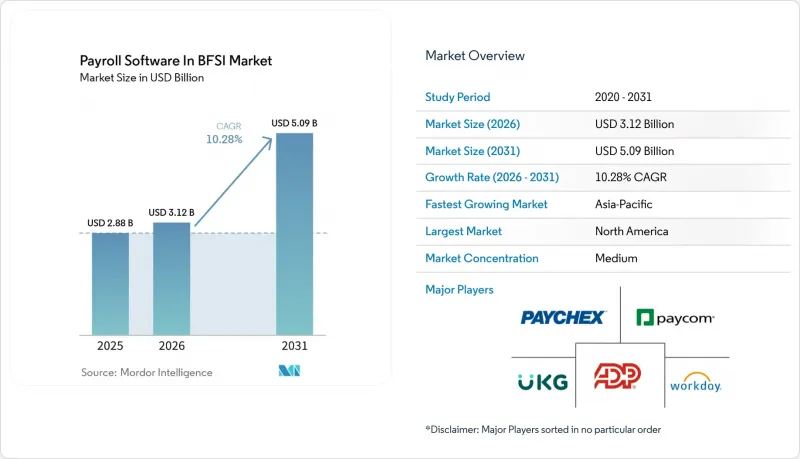

Mordor Intelligence에 의하면, BFSI 분야 급여 소프트웨어 시장 규모는 2025년 28억 8,000만 달러로 평가되었습니다. 2026년 31억 2,000만 달러에서 2031년까지 50억 9,000만 달러로 확대될 것으로 예측되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.28%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 조직 규모(대기업 및 중소기업), 배포 방식(클라우드 및 기타), 기능(핵심 급여 계산 처리, 근태 관리 및 기타), 기관 유형(은행, 보험사, 투자·증권사 및 기타), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

BFSI 분야 급여 소프트웨어 시장 동향 및 인사이트

은행 업계에서 디지털 전환(DX)의 가속화

은행들은 고립된 인사 시스템의 업그레이드에서 더 광범위한 운영 모델의 재설계로 전환하고 있으며, 급여 계산은 현재 그 핵심적인 기술 혁신 주기의 일부가 되었습니다. Zalaris사의 조사에 따르면, 덴스케 은행은 맞춤형 설정을 적용하지 않는 방식을 통해 북유럽의 4개 급여 계산 업체를 하나의 클라우드 플랫폼으로 통합하여 2만 명의 직원을 대상으로 서비스를 제공했습니다. 이 사례는 BFSI 분야 급여 소프트웨어 분야에서 중요한 의미를 지닙니다. 왜냐하면, 파편화된 급여 계산 시스템은 시스템의 복잡성을 가중시키고, 직원 정보 및 보수 기록의 일관성을 해치기 때문입니다. 은행들이 최신 API를 중심으로 시스템을 재구축함에 따라, 급여 계산은 재무, 인사, 결제 각 워크플로우를 뒷받침하는 공유 데이터 계층의 일부가 됩니다. ADP는 2025년 11월, 140개국을 대상으로 자사의 HCM 플랫폼 전반에 걸쳐 통합된 세계 인재 관리 제품군을 출시하며 이러한 방향성을 한층 더 강화했습니다. 따라서 BFSI 분야 급여 소프트웨어는 디지털 전환에서 시작되어 표준화된 급여 계산 인프라에 대한 수요로 마무리되는 현대화 프로그램의 혜택을 누리고 있습니다.

AI를 활용한 규정 준수 감시를 통한 수동 감사 비용 절감

BFSI 분야 급여 소프트웨어는 처리 후 오류 점검에서 지급 파일이 릴리스되기 전에 문제를 감지할 수 있는 예측형 모니터링으로 점차 전환되고 있습니다. UKG는 2026년 5월, “UKG Pro Pay with Workforce AI"를 출시했습니다. 이 제품은 급여 계산 결과를 최대 5년 치의 과거 급여 데이터와 비교합니다. ADP 역시 2026년 1월, 급여 및 인사 워크플로우 전반에 걸쳐 발생하는 급여 차이, 납세자 번호 누락, 기타 규정 준수상의 미비 사항을 파악할 수 있는 AI 에이전트를 도입하며, 이와 유사한 방향으로 사업을 확장했습니다. 은행과 보험사에게 있어 이러한 변화는 중요합니다. 왜냐하면 급여 기록은 내부 감사나 규제 당국의 검사에서 통제 증거로서의 역할을 점점 더 많이 수행하고 있기 때문입니다. 톰슨 로이터는 2026년 4월, 급여 계산에 AI를 활용하는 경우에도 최종 처리를 진행하기 전에 감사 가능한 워크플로우와 명확한 인적 검토가 여전히 필요하다고 지적했습니다. 이러한 요건에 따라 BFSI 분야 급여 소프트웨어는 변경 불가능한 로그, 역할 기반 통제, 그리고 규정 준수 팀이 적법성을 입증할 수 있는 거버넌스 기능을 갖춘 플랫폼으로 발전하고 있습니다.

API 상호 운용성이 제한적인 레거시 핵심 시스템

많은 금융 기관이 여전히 구식 파일 기반 프로세스를 통해 급여 계산을 수행하고 있기 때문에 레거시 은행 핵심 시스템은 BFSI 분야 급여 소프트웨어에 있어 여전히 직접적인 걸림돌이 되고 있습니다. CloudPay는 2025년 말까지 전 세계 기업의 62%가 엔드투엔드 급여 계산 프로세스 전반에 걸쳐 API를 도입하는 데 필요한 자원이나 전문 지식이 부족할 것이라고 보고했습니다. 해당 조사에 따르면, 응답 기업의 38%가 예산 제약을 이유로 꼽았으며, 규제가 엄격한 BFSI 환경에서는 이러한 제약이 더욱 심해집니다. TechHQ 역시 많은 다국적 기업들이 여전히 ‘API 우선’ 방식의 급여 계산 통합 모델 대신 파일 전송에 의존하고 있다고 지적하고 있습니다. 이로 인해 도입이 지연되고 테스트 주기가 길어지며, 현대화 프로그램이 시작된 후에도 급여 계산 팀은 수작업에 의존할 수밖에 없는 상황이 계속됩니다. 따라서 BFSI 분야 급여 소프트웨어는 특히 변경 관리 주기가 긴 금융 기관에서 전략적 의도와 운영 준비 사이에 시기적 격차를 겪고 있습니다.

부문별 분석

2025년, 소프트웨어는 시장 매출의 78.84%를 차지하며 BFSI 분야 급여 소프트웨어 부문에서 가장 큰 점유율을 기록했습니다. BFSI 기관들은 설정, 보안 규칙 및 재무·인사 시스템과의 통합을 보다 강력하게 제어하고자 하는 이유로, 예전부터 소프트웨어 플랫폼을 선호해 왔습니다. 이러한 경향은 여러 관할 구역에서 사업을 영위하며, 복잡한 공제 논리, 감사 추적 기록 및 다중 통화 급여 계산 처리를 지원해야 하는 대규모 기관에서 특히 두드러집니다. 워크데이는 2026 회계연도 1분기에 246억 달러 규모의 구독 계약 잔고를 보고했는데, 이는 기업의 급여 계산 및 HCM 계약이 일단 도입되면 높은 유지율을 유지한다는 관점을 뒷받침하는 것입니다.

서비스 부문은 규모는 작지만, 2031년까지 연평균 성장률(CAGR) 11.04%라는 비교적 빠른 속도로 성장할 것으로 전망됩니다. 규제 요건이 엄격한 관할 구역에서 급여 계산 업무를 관리할 수 있는 전문가를 채용하고 유지하는 데 많은 금융 기관이 어려움을 겪고 있어, 이에 대한 수요가 증가하고 있습니다. 하우페사는 급여 계산 업무를 담당하는 독일 세무 컨설턴트의 절반 이상이 50세 이상이라고 지적하고 있으며, 이는 급여 관리 분야의 인력 공급원이 점차 줄어들고 있음을 시사합니다. 이러한 압력을 배경으로, 중견 은행이나 보험사는 방침 관리 및 보고에 대한 감독 권한을 사내에 유지하면서 급여 관리 업무를 외부에 위탁하는 경향을 보이고 있습니다. 따라서 BFSI 분야 급여 소프트웨어 시장에서 금융 기관들이 인력 부족 및 사업 연속성 위험에 대응해 나감에 따라 소프트웨어는 계속해서 핵심적인 수익 기반이 될 것으로 보이며, 동시에 서비스 시장 점유율은 확대될 것으로 전망됩니다.

2025년에는 대기업이 시장의 69.22%를 차지했으며, 이는 대형 은행 그룹, 보험사, 투자사 전체에서 필요한 급여 관리 지출 규모를 반영하고 있습니다. 이러한 기관들은 대개 서로 다른 법인, 통화, 복리후생 제도, 보고 규정을 아우르며 수천 명의 직원을 관리하고 있습니다. 또한, 제한적인 단일 기능 도구에 의존하기보다는 급여 관리를 인사 관리, 재무, 인력 분석과 연계하는 종합적인 엔터프라이즈 제품군을 도입하는 경향이 있습니다. 이러한 환경 속에서 대규모 계약이 계속해서 BFSI 분야 급여 소프트웨어 수익 기반을 형성하고 있습니다.

중소기업(SME)은 2031년까지의 연평균 성장률(CAGR)이 10.58%로, 조직 규모별로는 가장 빠르게 성장하고 있으며, 이는 다음 성장의 물결이 조직 규모 스펙트럼에서 더 소규모 분야로 이동하고 있음을 보여줍니다. 직원 1인당 월 25-35달러의 가격 책정으로 인해, 과거 지역 은행이나 소규모 보험사들이 수작업이나 스프레드시트 중심의 업무 방식에 머물게 했던 자본적 장벽이 낮아졌습니다. 지역 신용조합, 부티크형 투자 회사, 소규모 보험사는 기존의 엔터프라이즈 시스템과 같은 막대한 초기 도입 비용을 부담하지 않고도 클라우드 기반 급여 계산 서비스를 도입할 수 있게 되었습니다. 또한 소규모 금융기관에 대해서도 규정 준수(컴플라이언스)에 대한 기대가 높아지고 있으며, 특히 심사나 검사 시 감사 기준을 충족하는 급여 기록이 요구되는 사례가 늘고 있습니다. 진입 가격의 하락과 규정 준수 압박의 강화로 인해 소규모 금융 기관들이 대상 시장에 포함되면서, BFSI 분야 급여 소프트웨어 시장 규모가 확대되고 있습니다.

지역별 분석

2025년, 북미는 BFSI 분야 급여 소프트웨어 시장 규모에서 37.96%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역이 주도적인 위치를 차지하고 있는 것은 성숙한 클라우드 인프라, 복잡한 급여 계산 규정, 그리고 금융 기관의 높은 기술 투자가 어우러져 이 세 가지 요소가 결합되었기 때문입니다. 미국은 여전히 제품 및 규정 준수 분야의 주요 최전선이며, ADP가 2025년 11월 140개국을 대상으로 시작한 인력 관리 서비스는 이 지역에 기반을 둔 기업들의 급여 계산 수요 규모를 반영하고 있습니다. 또한, 2026년 3월에 시행된 ACH 설명자 의무화 조치 역시 결제 네트워크 규정이 은행 및 관련 금융기관 전반에 걸쳐 급여 계산 시스템의 업그레이드를 어떻게 촉발할 수 있는지를 보여주고 있습니다. 캐나다에서는 주별 급여세, 노동 규제, 복리후생 관리의 차이가 수요를 뒷받침하고 있는 반면, 멕시코에서는 보다 광범위한 핀테크 및 은행 고객 기반을 통해 이 지역의 비즈니스 기회를 확대되고 있습니다.

2025년, 유럽은 기업용 급여 계산 수요 측면에서 여전히 비교적 성숙한 지역 중 하나였으며, 영국, 독일, 프랑스가 가장 발전된 구매 시장으로 두각을 나타냈습니다. 특히 독일은 급여 계산이 매우 복잡하기 때문에 금융 기관 입장에서 규정 준수 대응 소프트웨어의 가치가 높아진다는 점에서 중요합니다. 2026년 6월로 예정된 급여 투명성 보고 일정에 따라, 여러 EU 시장에서 사업을 영위하는 은행 및 보험사들 사이에서 분석 및 보고 기능에 대한 수요가 증가하고 있습니다. 또한, HiBob의 급여 계산 워크플로우와 Modulr의 통합은 유럽의 플랫폼이 급여 계산, 지급 처리, 세무 신고 간의 마찰을 어떻게 완화하고 있는지를 보여줍니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 11.42%로 가장 빠르게 성장하고 있는 지역이며, BFSI 분야 급여 소프트웨어를 이끄는 주요 성장 동력으로 자리 잡고 있습니다. 중국에서는 대형 은행들이 급여 계산을 독립된 소프트웨어 판매로 취급하지 않고, 예금 유지 및 고객 관계 심화를 위해 내장형 급여 계산 플랫폼을 구축하고 있어, 이 지역 특유의 모델이 형성되고 있습니다. 상하이 푸동 발전은행이 업그레이드한 원스톱 인사·급여 계산 서비스 플랫폼도 이와 같은 방향성을 보여주고 있으며, 급여 계산이 보다 광범위한 법인 대상 은행 서비스 제안의 일부로 자리 잡고 있습니다. 인도의 노동법 개정에 따라 2027년까지 디지털 급여 계산 규정 준수 플랫폼에 대한 수요가 확대될 것으로 예측됩니다. 일본에서도, “Bakuraku Payroll" 등의 플랫폼이 성장을 뒷받침하고 있으며, 이 회사는 99% 이상의 서비스 유지율을 보고하는 한편, ISO/IEC 27001 인증을 핵심 운영 기능으로 강조하고 있습니다. 중동 수요는 사우디아라비아와 아랍에미리트에 집중되어 있습니다. 이는 금융기관의 확대와 WPS(급여 지급 시스템) 규정 준수로 인해 급여 계산에 대한 투자가 활발하게 이어지고 있기 때문입니다. 아프리카는 아직 발전의 초기 단계에 있지만, 모바일 우선 네오뱅크와 내장형 급여 계산 모델을 통해 BFSI 분야 급여 소프트웨어 분야에서 장기적인 비즈니스 기회가 점차 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the payroll software in BFSI market size is projected to expand from USD 2.88 billion in 2025 and USD 3.12 billion in 2026 to USD 5.09 billion by 2031, registering a CAGR of 10.28% between 2026 to 2031.

This report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, and SMEs), Deployment (Cloud, and More), Functionality (Core Payroll Processing, Time and Attendance Management, and More), Institution Type (Banking Companies, Insurance Companies, Investment and Brokerage Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Payroll Software In BFSI Market Trends and Insights

Accelerating Digital Transformation Initiatives In Banking

Banks have moved from isolated HR upgrades to broader operating model redesign, and payroll now sits inside that core technology refresh cycle. Zalaris showed that Danske Bank consolidated 4 Nordic payroll vendors into 1 cloud platform covering 20,000 employees under a no-customization approach. That example matters in the Payroll software in BFSI market because fragmented payroll stacks raise system complexity and weaken consistency across employee and compensation records. When banks rebuild around modern APIs, payroll becomes part of the shared data layer that supports finance, workforce, and payment workflows. ADP reinforced this direction in November 2025 when it launched a unified global workforce management suite across its HCM platforms for 140 countries. The payroll software in BFSI market is therefore benefiting from modernization programs that begin with digital transformation but end with demand for standardized payroll infrastructure.

AI-Driven Compliance Monitoring Reducing Manual Audit Costs

The Payroll software in BFSI market is moving from post-run error checks toward predictive monitoring that can flag problems before payment files are released. UKG launched UKG Pro Pay with Workforce AI in May 2026, and the product compares payroll runs against up to 5 years of historical payroll data. ADP expanded in the same direction in January 2026 with AI agents that can identify payroll variances, missing tax IDs, and other compliance gaps across payroll and HR workflows. For banks and insurers, that shift is important because payroll records increasingly serve as control evidence for internal reviews and regulatory examinations. Thomson Reuters noted in April 2026 that AI in payroll still requires auditable workflows and clear human review before final action. That requirement is steering the Payroll software in BFSI market toward platforms with immutable logs, role-based controls, and governance features that compliance teams can defend.

Legacy Core Systems With Limited API Interoperability

Legacy banking cores remain a direct brake on the Payroll software in BFSI market because many institutions still run payroll through older file-based processes. CloudPay reported in late 2025 that 62% of global businesses lacked the resources or expertise to adopt APIs across end-to-end payroll processes. The same research said 38% of enterprise respondents cited budget constraints, which becomes more restrictive in regulated BFSI settings. TechHQ also noted that many multinational organizations still rely on file transfers rather than API-first payroll integration patterns. That slows implementation, extends testing cycles, and keeps payroll teams exposed to manual workarounds even after modernization programs begin. The Payroll software in BFSI market, therefore, faces a timing gap between strategic intent and operational readiness, especially in institutions with long change-control cycles.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Regulatory Demand For Real-Time Payroll Reporting

- Growing Adoption Of Cloud-Native Core Banking Platforms

- Cyber-Security And Data Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 78.84% of market revenue in 2025, giving it the largest share of the payroll software in BFSI market. BFSI institutions have historically favored software platforms because they want stronger control over configuration, security rules, and integrations with finance and HR systems. That preference is especially strong in large institutions that operate across multiple jurisdictions and need support for complex deduction logic, audit trails, and multi-currency payroll processing. Workday reported a subscription backlog of USD 24.6 billion in Q1 FY2026, which supports the view that enterprise payroll and HCM contracts remain highly sticky once deployed.

The services segment is projected to grow faster at an 11.04% CAGR through 2031, even though it starts from a smaller base. Demand is rising because many financial institutions struggle to recruit and retain specialists who can manage payroll operations in compliance-heavy jurisdictions. Haufe noted that more than half of German tax consultants handling payroll accounts were over 50, which points to a narrowing labor pipeline in payroll administration. That pressure is encouraging mid-tier banks and insurers to outsource payroll administration while still keeping policy control and reporting oversight internally. The Payroll software in BFSI market is therefore likely to keep software as the core revenue base, while services gains share as institutions respond to talent scarcity and operating continuity risk.

Large enterprises accounted for 69.22% of the market in 2025, reflecting the scale of payroll spending required across large banking groups, insurers, and investment firms. These institutions usually manage thousands of employees across different legal entities, currencies, benefit structures, and reporting rules. They also tend to buy broad enterprise suites that connect payroll with talent, finance, and workforce analytics rather than relying on narrow point tools. In that environment, larger contracts continue to set the revenue base for the Payroll software in BFSI market.

SMEs are the fastest-growing organization size at a 10.58% CAGR through 2031, which shows that the next expansion wave is shifting lower in the institution-size spectrum. Pricing at USD 25 to USD 35 per employee per month has lowered the capital barrier that once kept regional banks and smaller insurers on manual or spreadsheet-led processes. Community credit unions, boutique investment houses, and smaller insurance carriers can now adopt cloud payroll services without the heavy upfront implementation burden of legacy enterprise systems. Compliance expectations are also rising for smaller institutions, especially where audit-grade payroll records are required during reviews or examinations. The Payroll software in BFSI market is widening because lower entry pricing and stronger compliance pressure are now moving smaller financial institutions into the addressable base.

Complete Report Scope:

- By Component

- Software

- Services

- By Organization Size

- Large Enterprises

- SMEs

- By Deployment Mode

- Cloud

- On-Premises

- By Functionality

- Core Payroll Processing

- Time and Attendance Management

- Payroll Analytics and Reporting

- Tax and Compliance Management

- Other Functionalities

- By Financial Institution Type

- Banking Companies

- Insurance Companies

- Investment and Brokerage Firms

- Credit Unions

- Other Financial Institutions Types

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America accounted for 37.96% share of the payroll software in BFSI market size in 2025, making it the largest regional contributor. The region leads because it combines mature cloud infrastructure, complex payroll regulation, and high technology spending by financial institutions. The United States remains the main product and compliance frontier, and ADP's November 2025 workforce management launch for 140 countries reflects the scale of enterprise payroll demand anchored in the region. The March 2026 ACH descriptor mandate also illustrates how payment-network rules can trigger payroll system upgrades across banks and related financial institutions. Canada adds demand through province-level variation in payroll taxes, labor rules, and benefits administration, while Mexico expands the regional opportunity through a broader fintech and banking customer base.

Europe remained one of the more developed regions for enterprise payroll demand in 2025, with the UK, Germany, and France standing out as the most sophisticated buyer markets. Germany is especially important because payroll complexity is high, which increases the value of compliance-grade software for financial institutions. The June 2026 pay-transparency reporting timetable is raising demand for analytics and reporting functions among banks and insurers that operate across multiple EU markets. HiBob's payroll workflow integration with Modulr also shows how European platforms are reducing friction between payroll calculation, payment execution, and tax submission.

Asia-Pacific is the fastest-growing geography at an 11.42% CAGR through 2031, which makes it the main expansion engine for the Payroll software in BFSI market. China is shaping an unusual regional model because major banks are building embedded payroll platforms to retain deposits and deepen client relationships rather than treating payroll as a separate software sale. Shanghai Pudong Development Bank's upgraded one-stop HR and payroll service platform shows the same direction, where payroll becomes part of a wider enterprise banking proposition. India's labor code reforms are expected to widen demand for digital payroll compliance platforms by 2027. Japan also supports growth through platforms such as Bakuraku Payroll, which reported a service continuation rate above 99% and highlighted ISO/IEC 27001 certification as a core operating feature. Middle East demand is concentrated in Saudi Arabia and the United Arab Emirates because financial institution expansion and WPS compliance keep payroll investment active. Africa remains earlier in development, but mobile-first neobanks and embedded payroll models are gradually broadening the long-term opportunity for the Payroll software in BFSI market.

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Paycom Software, Inc.

- SAP SE

- Workday, Inc.

- Dayforce, Inc.

- Intuit Inc.

- Ultimate Kronos Group (UKG Inc.)

- Ramco Systems Limited

- Sage Group plc

- Paylocity Holding Corporation

- Deel, Inc.

- Papaya Global Ltd.

- Rippling People Center Inc.

- Neeyamo Enterprise Solutions Private Limited

- Datamatics Global Services Limited

- Zalaris ASA

- Safeguard World International Limited

- PayAsia Management Pvt Ltd

- Ascender HCM Pty Limited

- Unit4 N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Digital Transformation Initiatives in Banking

- 4.2.2 Heightened Regulatory Demand for Real-Time Payroll Reporting

- 4.2.3 Growing Adoption of Cloud-Native Core Banking Platforms

- 4.2.4 Embedded Payroll Functionality in Banking-as-a-Service (BaaS) Offerings

- 4.2.5 Expansion of Neo-Banks Targeting Gig and Freelance Workforce

- 4.2.6 AI-Driven Compliance Monitoring Reducing Manual Audit Costs

- 4.3 Market Restraints

- 4.3.1 Legacy Core Systems with Limited API Interoperability

- 4.3.2 High Switching Costs from On-Premise Payroll Engines

- 4.3.3 Cyber-Security and Data Sovereignty Concerns

- 4.3.4 Shortage of Domain-Specific Payroll Talent in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 SMEs

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By Functionality

- 5.4.1 Core Payroll Processing

- 5.4.2 Time and Attendance Management

- 5.4.3 Payroll Analytics and Reporting

- 5.4.4 Tax and Compliance Management

- 5.4.5 Other Functionalities

- 5.5 By Financial Institution Type

- 5.5.1 Banking Companies

- 5.5.2 Insurance Companies

- 5.5.3 Investment and Brokerage Firms

- 5.5.4 Credit Unions

- 5.5.5 Other Financial Institutions Types

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Paychex, Inc.

- 6.4.3 Paycom Software, Inc.

- 6.4.4 SAP SE

- 6.4.5 Workday, Inc.

- 6.4.6 Dayforce, Inc.

- 6.4.7 Intuit Inc.

- 6.4.8 Ultimate Kronos Group (UKG Inc.)

- 6.4.9 Ramco Systems Limited

- 6.4.10 Sage Group plc

- 6.4.11 Paylocity Holding Corporation

- 6.4.12 Deel, Inc.

- 6.4.13 Papaya Global Ltd.

- 6.4.14 Rippling People Center Inc.

- 6.4.15 Neeyamo Enterprise Solutions Private Limited

- 6.4.16 Datamatics Global Services Limited

- 6.4.17 Zalaris ASA

- 6.4.18 Safeguard World International Limited

- 6.4.19 PayAsia Management Pvt Ltd

- 6.4.20 Ascender HCM Pty Limited

- 6.4.21 Unit4 N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

(주말 및 공휴일 제외)