|

시장보고서

상품코드

2073308

지속적 성과 관리 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Continuous Performance Management Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

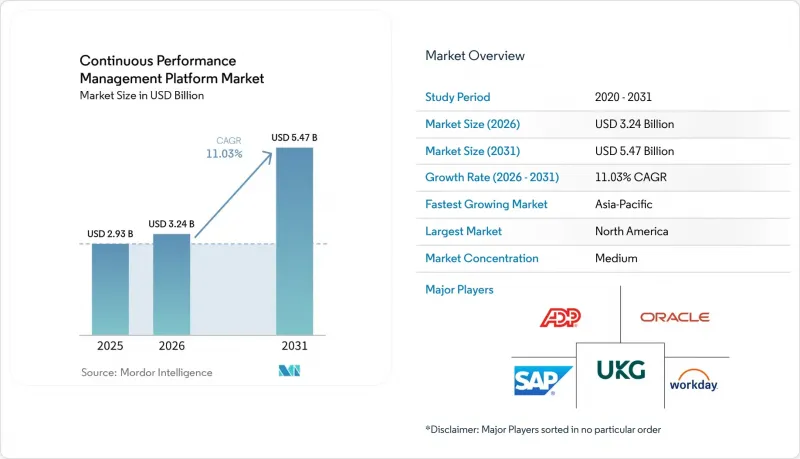

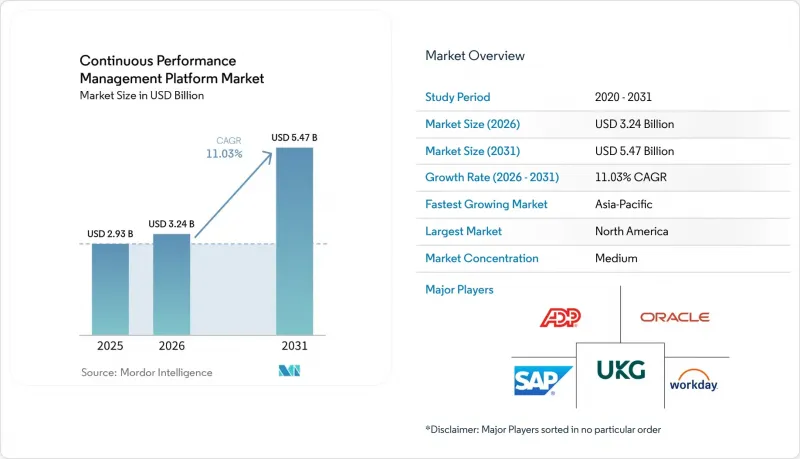

Mordor Intelligence에 의하면, 지속적 성과 관리 플랫폼 시장 규모는 2025년에 29억 3,000만 달러로 평가되었습니다. 2026년에 32억 4,000만 달러에 달하고, 2031년까지 54억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.03%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(클라우드 기반 및 On-Premise형), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(IT 및 통신, 헬스케어 및 생명과학, 소매 및 소비재, 제조업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 지속적 성과 관리 플랫폼 시장 동향 및 인사이트

연례 평가에서 지속적인 피드백 체계로의 광범위한 전환

조직에서는 연 1회 평가를 단계적으로 폐지하고 있습니다. 이는 단편적인 평가만으로는 역할의 진화나 전략적 전환의 속도를 제대로 파악할 수 없기 때문입니다. Betterworks의 조사에 따르면, 인재 관련 의사결정을 “예측 가능"라고 보는 기업은 고작 16%에 불과한 반면, 73%는 추진을 가로막는 정보 격차를 인식하고 있습니다. Slack이나 Teams에 피드백 기능을 통합하면, 맥락을 전환할 필요가 없어져 업무 흐름 속에서 성과 지표를 파악하고, 보다 신속하게 방향을 수정할 수 있게 됩니다. SAP의 “2026년 상반기 목표 설정 및 목표 진행 상황 관리 도구"는 시대에 뒤떨어진 목표를 적극적으로 지적하여, 평가 주기 종료 시 발생할 수 있는 예기치 못한 상황을 줄여줍니다. 이러한 변화는 소매 업계에서 특히 두드러지며, 고위 관리직의 이직률은 평균 22%에 달하고 있어 끊임없이 변화하는 팀 간의 실시간 협력이 요구되고 있습니다. 조달 주기가 단축되고 있는 가운데, 매일 밤 HRIS 동기화와 실시간 캘리브레이션 분석을 함께 제공하는 공급업체가 계약을 따내고 있습니다.

확장성과 비용 효율성을 추구하며, 클라우드 기반 HR 솔루션 도입이 확대되고 있습니다.

클라우드 도입을 통해 On-Premise 시스템의 운영에 걸림돌이 되었던 설비 투자나 수개월에 걸친 업그레이드가 필요 없어집니다. 2026년에 발표된 동료 심사를 거친 연구에 따르면, 분산 컴퓨팅을 통합한 클라우드 기반 HRM 플랫폼이 중소기업에서 데이터의 정확성, 평가의 신뢰성 및 업무 대응 능력을 향상시키는 것으로 밝혀졌습니다. ICON Corporate Finance의 추산에 따르면, 기업의 60%가 AI 기반 HCM 플랫폼에 대한 투자를 확대할 계획이며, 매주 기능을 개선할 수 있는 공급업체가 우대를 받을 것으로 보입니다. Lattice의 로드맵에서는 AI를 활용한 평가안 작성과 Workday 및 Rippling과의 원활한 연동을 통해 인재 데이터의 일관성을 유지합니다. Workday Flex Credits와 같은 종량제 요금 모델은 조달 프로세스의 마찰을 더욱 줄여주며, 계약 재협상 없이도 AI 활용 규모를 확대할 수 있게 해줍니다.

GDPR(EU 개인정보보호규정) 및 CCPA에 따른 데이터 개인정보 보호 및 규정 준수 관련 우려 사항

성과 관리 플랫폼은 기밀성이 높은 평가, 코칭 노트, 감정 점수 등을 수집하기 때문에 고용주는 엄격한 데이터 보호 규정의 적용을 받게 됩니다. 영국 정보위원회(ICO)는 2024년부터 2025년에 걸쳐 약 4만 3,000건의 민원을 접수했으며, 2026년 6월 19일부터는 민원인이 제출한 자료만을 바탕으로 예비 조사 결과를 발표할 수 있게 됩니다. AI를 통해 생성된 요약본은 개인 데이터의 정의에 해당하므로, 공급업체는 데이터 최소화 조치, 보존 기간 수립 및 역할 기반 접근 제어를 제공해야 합니다. EU의 AI법에서는 평가 알고리즘을 “고위험"로 분류되며, 투명성 확보 및 편향 완화에 관한 추가 요건이 부과되고 있습니다. SOC 2, ISO 및 GDPR(EU 개인정보보호규정) 준수 인증을 취득한 공급업체는 구매자가 규정 준수 관련 위험을 줄이려고 노력하는 상황에서 경쟁 우위를 확보할 수 있습니다.

부문별 분석

고객들이 AI 출력 통합, 데이터 흐름 매핑, 지속적인 피드백에 관한 관리자 교육에 어려움을 겪고 있어 서비스 수익이 가속화되고 있습니다. 2025년에도 소프트웨어는 지속적인 성능 관리 플랫폼 시장의 61.45%를 차지했으나, 도입 및 통합 관련 계약은 연평균 성장률(CAGR) 12.21%를 나타낼 것으로 전망됩니다. 전문 서비스 분야의 지속적인 성과 관리 플랫폼 시장 규모가 확대되고 있는 이유는 Oracle의 25D 기능이나 SAP의 에이전트 릴리스에서 구성, 거버넌스, 변경 관리에 관한 전문 지식이 요구되기 때문입니다. 또한, 인사 부서에는 AI의 성과 지표를 측정할 능력이 부족하기 때문에 지원 계약도 급증하고 있으며, 이는 기업의 56%가 AI의 ROI를 추적하지 않고 있다는 SHRM의 조사 결과를 뒷받침하는 것입니다.

두 번째 성장 동력은 컴플라이언스 컨설팅입니다. AI가 대규모 모니터링에 해당하는 경우, 데이터 보호 영향 평가 및 역할 기반 접근 권한 설계는 여전히 필수적입니다. 컨설팅과 정기적인 매니지드 서비스를 결합할 수 있는 공급업체는 수년에 걸쳐 수익을 확보할 수 있으며, 이에 따라 지속적인 성과 관리 플랫폼 시장은 라이선스 중심 모델을 넘어선 형태로 진화하고 있습니다.

예측 기간 동안 클라우드 도입은 On-Premise를 능가할 것으로 보이며, 기업들이 원활한 업그레이드, 설비 투자(CapEx) 절감 및 유연한 AI 활용을 추구함에 따라 연평균 성장률(CAGR) 13.01%로 성장할 전망입니다. 2025년 시점에서 레거시 시스템은 지속적인 성능 관리 플랫폼 시장의 68.19% 점유율을 유지하고 있었으나, 벤더의 로드맵을 살펴보면 On-Premise 환경에서는 1년에 한 번 패치가 제공되는 반면, 클라우드 환경에서는 거의 매주 새로운 기능이 출시되고 있음을 알 수 있습니다. Workday Flex Credits는 “성장에 따른 과금(pay-as-you-grow)"의 대표적인 사례이며, 2026년 학술 연구에 따르면 클라우드 아키텍처가 평가 주기의 응답성과 데이터의 정확성을 향상시킨다는 사실이 확인되었습니다.

규제가 엄격한 업계에서는 데이터 주권에 관한 규정을 충족하기 위해 여전히 On-Premise 버전이 도입되고 있으며, 상당한 규모의 도입 기반이 유지되고 있습니다. 그러나 조달 과정에서 비용 산정 방식은 변화하고 있습니다. 전문 SaaS 공급업체는 도입 기간을 4-8주로 예상하고 있으며, 이는 제품군 업그레이드에 소요되는 9-18개월보다 훨씬 짧은 기간입니다. 이로 인해 가치 실현까지 걸리는 시간이 단축되었으며, 지속적인 성과 관리 플랫폼 시장에서 클라우드의 우위가 확고해졌습니다.

지역별 분석

북미는 2025년 매출의 36.86%를 차지했으며, HCM 벤더, 컨설턴트, 조기 도입 기업으로 구성된 긴밀한 생태계의 지원을 받아 여전히 가장 큰 기여를 하는 지역으로 남아 있습니다. 미국 기업들은 미완성된 AI의 시범 도입에 대해 높은 수용도를 보이고 있지만, 현재 19개 주에서 고용주의 AI 사용이 규제되는 등 규제 환경은 점점 더 엄격해지고 있습니다. 캐나다와 멕시코는 도입에 있어 뒤처져 있지만, 대륙 전체에서 프로세스를 표준화하는 다국적 기업의 클라우드 확장의 혜택을 누리고 있습니다.

아시아태평양은 CHRO(최고 인사 책임자)들이 인력 계획에서 역량 기반 전략으로의 전환을 추진하고 있는 것을 배경으로, 연평균 성장률(CAGR) 11.98%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도의 IT 서비스 집적지나 호주의 성숙한 서비스 경제는 북미의 도입 곡선과 유사하지만, 중국에서는 성과 데이터와 제조 KPI를 융합하고 있습니다. 데이터 소재지에 관한 법률 및 규제의 파편화로 인해 국경을 넘는 도입은 복잡해지고 있지만, 현지 언어를 지원하는 인터페이스와 지역 데이터센터의 확충을 통해 이러한 장벽은 점차 낮아지고 있습니다.

유럽의 상황은 복잡합니다. 독일과 영국에서는 클라우드 도입이 활발하지만, GDPR(EU 개인정보보호규정) 의무와 근로자 대표 위원회와의 협의로 인해 판매 주기가 길어지고 있습니다. 영국 정보위원회(ICO)의 새로운 민원 처리 규정에 따라 규정 준수 위험이 높아지고 있으며, EU의 AI 법에서는 성능 알고리즘이 고위험으로 분류되고 있어, 공급업체들은 투명성 확보를 위한 기능에 막대한 투자를 할 수밖에 없는 상황입니다. 중동 및 아프리카 및 남미는 아직 개발도상국이지만 미래가 기대되는 지역이며, 사우디아라비아, 아랍에미리트, 브라질, 아르헨티나에서는 “디지털 우선" 정부 프로그램의 일환으로, 클라우드 기반 인사 관리 시스템의 시범 도입이 진행되고 있습니다. 인프라 부족과 환율 변동이 성장을 저해하고 있지만, 다국적 기업의 자회사들이 수요의 씨앗을 뿌리고 있으며, 이것이 점차 현지 기업들로 파급되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the continuous performance management platform market size is expected to be USD 2.93 billion in 2025, USD 3.24 billion in 2026, and reach USD 5.47 billion by 2031, growing at a CAGR of 11.03% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Retail and Consumer Goods, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Continuous Performance Management Platform Market Trends and Insights

Widespread Shift From Annual Reviews to Continuous Feedback Frameworks

Organizations are abandoning once-a-year appraisals because episodic reviews fail to capture the speed of role evolution and strategic pivots. Betterworks research reported that only 16% of firms view talent decisions as predictive, while 73% acknowledge intelligence gaps that derail initiatives. Embedding feedback into Slack and Teams removes context-switching, captures performance signals in flow-of-work, and delivers faster course corrections. SAP's 1H 2026 Goal Creation and Goal Progress Agents proactively flag outdated objectives, cutting end-of-cycle surprises. The shift is acute in retail, where senior-leader turnover averages 22%, forcing real-time alignment among constantly changing teams. Procurement cycles are compressing, and vendors offering nightly HRIS synchronizations alongside real-time calibration analytics are winning deals.

Rising Adoption of Cloud-Based HR Solutions for Scalability and Cost Efficiency

Cloud deployment eliminates capital expense and multi-month upgrades that hamper on-premises systems. A 2026 peer-reviewed study found that cloud HRM platforms integrating distributed computing raised data accuracy, appraisal reliability, and operational responsiveness in SMEs. ICON Corporate Finance estimated that 60% of enterprises intend to increase investment in AI-driven HCM platforms, rewarding vendors able to iterate features weekly. Lattice's roadmap delivers AI-powered review drafts and seamless Workday and Rippling integrations that keep talent data aligned. Consumption-based models such as Workday Flex Credits further reduce procurement friction and let firms scale AI usage without contract renegotiations.

Data Privacy and Compliance Concerns Under GDPR And CCPA

Performance platforms capture sensitive ratings, coaching notes, and sentiment scores, exposing employers to strict data-protection rules. The UK ICO logged nearly 43,000 complaints in 2024-2025, and from 19 June 2026 it can issue preliminary findings based solely on complainant submissions. AI-generated summaries fall under personal-data definitions, forcing vendors to offer minimization controls, retention schedules, and role-based access. The EU AI Act classifies evaluation algorithms as high risk, layering extra transparency and bias-mitigation requirements. Providers sporting SOC 2, ISO, and GDPR-ready attestations gain an edge as buyers de-risk compliance exposure.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models Requiring Real-Time Performance Visibility

- Integration of AI And Analytics for Data-Driven Talent Decisions

- Organizational Resistance to Cultural Change in Performance Evaluation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is accelerating as customers struggle to integrate AI outputs, map data flows, and train managers on continuous feedback. In 2025 software still commanded 61.45% of the continuous performance management platform market, yet implementation and integration engagements are expanding at a 12.21% CAGR. The continuous performance management platform market size for professional services grows because Oracle's 25D features and SAP's agent releases demand configuration, governance, and change-management expertise. Support contracts also balloon as HR teams lack the capacity to measure AI success metrics, corroborating SHRM's finding that 56% of firms never track AI ROI.

A second growth engine is compliance consulting: data-protection impact assessments and role-based access design remain mandatory when AI qualifies as large-scale monitoring. Vendors able to bundle consultancy with recurring managed services lock in multi-year revenue, pushing the continuous performance management platform market beyond a license-centric model.

Cloud adoption is set to eclipse on-premises during the forecast, expanding at a 13.01% CAGR as enterprises seek frictionless upgrades, lower CapEx, and elastic AI consumption. Although legacy installations retained 68.19% of the continuous performance management platform market share in 2025, vendor roadmaps reveal weekly cloud feature drops versus annual on-premises patches. Workday Flex Credits exemplify the pay-as-you-grow model, and a 2026 academic study confirmed cloud architectures improve appraisal-cycle responsiveness and data accuracy.

Highly regulated sectors still deploy on-premises versions to satisfy data-sovereignty rules, preserving a sizable installed base. Yet procurement math is shifting: specialized SaaS vendors quote four-to-eight-week implementations, well below the nine-to-eighteen-month timelines of suite upgrades, accelerating time-to-value and solidifying cloud's ascendancy within the continuous performance management platform market.

Complete Report Scope:

- By Component

- Software

- Continuous Feedback Software

- Performance Review Workflow Software

- Talent and Skill Development Tracking Software

- Integration and API Management Modules

- Other Software

- Services

- Implementation and Integration Services

- Support and Maintenance Services

- Software

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Retail and Consumer Goods

- Manufacturing

- Government and Public Sector

- Education

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.86% of 2025 revenue and remains the largest regional contributor, buoyed by dense ecosystems of HCM vendors, consultants, and early adopters. U.S. firms show a high tolerance for piloting unfinished AI, but the regulatory backdrop is tightening as 19 states now regulate employer AI. Canada and Mexico trail in adoption yet benefit from multinational cloud rollouts that standardize processes across the continent.

Asia-Pacific is the fastest-growing region at an 11.98% CAGR, underpinned by CHRO mandates to shift from headcount planning to skills-based strategies. India's IT services clusters and Australia's mature services economy mirror North American adoption curves, while China blends performance data with manufacturing KPIs. Data-residency laws and fragmented regulations complicate cross-border implementations, but local-language interfaces and regional data centers are lowering barriers.

Europe presents a mixed picture: cloud uptake is strong in Germany and the UK, but GDPR obligations and works-council consultations elongate sales cycles. The UK ICO's new complaint rules elevate compliance risk, and the EU AI Act classifies performance algorithms as high risk, forcing vendors to invest heavily in transparency features. Middle East and Africa plus South America are nascent yet promising, with Saudi Arabia, the United Arab Emirates, Brazil, and Argentina piloting cloud HR stacks under digital-first government programs. Infrastructure gaps and currency volatility temper growth, but multinational subsidiaries are seeding demand that gradually radiates to local firms.

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP, Inc.

- UKG Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Lattice HR, Inc.

- 15Five, Inc.

- Betterworks Systems, Inc.

- Reflektive, Inc.

- Culture Amp Pty Ltd

- PerformYard LLC

- Trakstar, Inc.

- ClearCompany, Inc.

- Engagedly, Inc.

- Synergita Software Pvt. Ltd.

- Small Improvements GmbH

- WorkTango Inc.

- Paycor, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Shift from Annual Reviews to Continuous Feedback Frameworks

- 4.2.2 Rising Adoption of Cloud-Based HR Solutions for Scalability and Cost Efficiency

- 4.2.3 Expansion of Remote and Hybrid Work Models Requiring Real-Time Performance Visibility

- 4.2.4 Integration of AI and Analytics for Data-Driven Talent Decisions

- 4.2.5 Growing Demand for Objective and Key Results Alignment Within Agile Project Teams

- 4.2.6 Emergence of Employee Sentiment Analysis Using Passive Listening Data Streams

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Compliance Concerns Under GDPR and CCPA

- 4.3.2 Organizational Resistance to Cultural Change in Performance Evaluation

- 4.3.3 Algorithmic Bias Risks in AI-Powered Evaluation Models

- 4.3.4 Overload of Micro-Feedback Leading to Manager Burnout

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Continuous Feedback Software

- 5.1.1.2 Performance Review Workflow Software

- 5.1.1.3 Talent and Skill Development Tracking Software

- 5.1.1.4 Integration and API Management Modules

- 5.1.1.5 Other Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Support and Maintenance Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and Consumer Goods

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 ADP, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Cornerstone OnDemand, Inc.

- 6.4.7 BambooHR LLC

- 6.4.8 Lattice HR, Inc.

- 6.4.9 15Five, Inc.

- 6.4.10 Betterworks Systems, Inc.

- 6.4.11 Reflektive, Inc.

- 6.4.12 Culture Amp Pty Ltd

- 6.4.13 PerformYard LLC

- 6.4.14 Trakstar, Inc.

- 6.4.15 ClearCompany, Inc.

- 6.4.16 Engagedly, Inc.

- 6.4.17 Synergita Software Pvt. Ltd.

- 6.4.18 Small Improvements GmbH

- 6.4.19 WorkTango Inc.

- 6.4.20 Paycor, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment