|

시장보고서

상품코드

2073332

BFSI 부문 그린 IT 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Green IT Software For BFSI Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

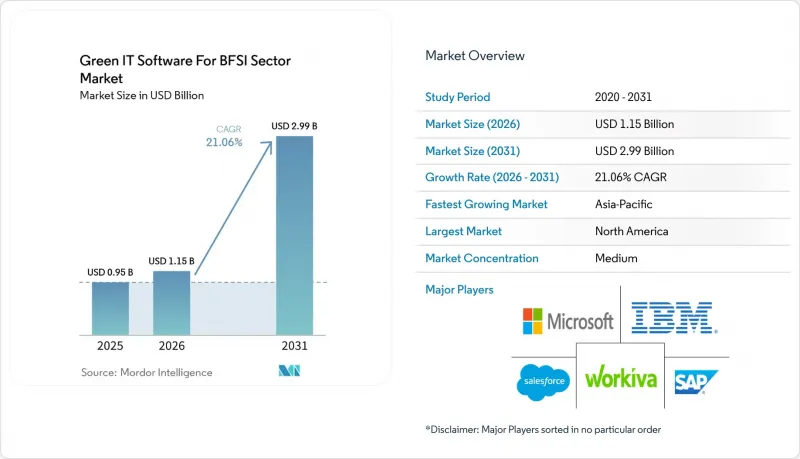

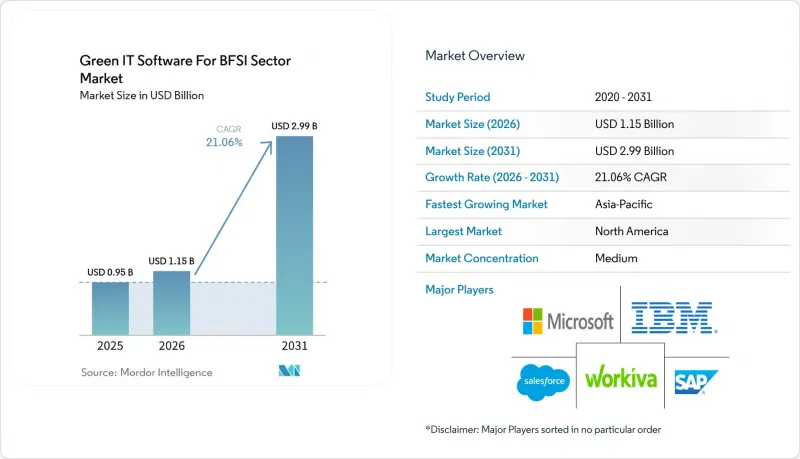

Mordor Intelligence에 의하면, BFSI 부문 그린 IT 소프트웨어 시장 규모는 2025년에 9억 5,000만 달러로 평가되었습니다. 2026년에 11억 5,000만 달러에 달하고, 2031년까지 29억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 21.06%로 성장할 것으로 전망됩니다.

본 보고서는 도입 형태(클라우드, On-Premise, 하이브리드), 소프트웨어 카테고리(탄소 관리 소프트웨어, 지속가능성 보고·관리 소프트웨어, 에너지·자원 최적화 소프트웨어 등), 기업 규모(대기업, 중소기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 BFSI 부문 그린 IT 소프트웨어 시장 동향 및 인사이트

BFSI 부문의 ESG 공시 의무화 및 감사 가능성

규제 대상 기관들은 더 이상 지속가능성 보고를 자발적인 활동으로 간주할 수 없게 되었기 때문에 공시 의무 규정은 BFSI 부문 그린 IT 소프트웨어 시장에 있어 당분간 가장 강력한 촉진요인이 되고 있습니다. 2026년 EU 옴니버스법은 제1단계에서 공익법인에 대한 보고 의무를 유지하면서, 체계적이고 감사에 대응할 수 있는 제출 서류의 필요성을 확보했습니다. 한편, 그 이후 단계에서는 대상이 더 대규모 기업으로 한정되었습니다. 일본 금융청도 프라임 시장에 상장된 대기업을 대상으로 한 연간 유가증권 보고서에서 SSBJ에 따른 공시를 공식적으로 의무화했습니다. 이는 BFSI 부문 그린 IT 소프트웨어 시장이 자발적인 지속가능성 보고가 아닌, 공식적인 유가증권 공시 요건에 의해 뒷받침되고 있음을 보여줍니다. 인도는 2025-26 회계연도부터 BRSR 코어의 보증 의무 적용 대상을 상위 250개사에서 상위 500개사로 확대하고, 2026-27 회계연도부터는 상위 1,000개사로 확대할 계획이며, 이에 따라 지속적인 도입 수요가 더욱 높아지고 있습니다. 여러 지역에서 사업을 전개하는 기관의 경우, 단일 보고 주기 내에서 중복된 중요성, 재무적 중요성 및 지역별 공시 요건의 차이를 모두 고려해야 하므로 그 부담은 더욱 커집니다. 따라서 BFSI 부문 그린 IT 소프트웨어 시장에서는 단일 기반 데이터 모델을 유지하면서 매번 제어 구조를 재구축할 필요 없이 여러 프레임워크의 출력을 생성할 수 있는 플랫폼이 점점 더 높이 평가받고 있습니다.

전체 대출 및 투자 포트폴리오에 걸친 자금 조달에 따른 배출량 측정

은행과 자산운용사는 자사의 사업 활동으로 인한 탄소 발자국을 훨씬 뛰어넘는 포트폴리오 차원의 탄소 회계가 필요하기 때문에 대출 및 투자 포트폴리오 전반에 걸친 “파이낸스 에미션(대출 및 투자를 통한 배출량)"의 측정은 BFSI 부문 그린 IT 소프트웨어 시장의 핵심 성장 동력으로 자리 잡고 있습니다. 제출된 초안에서는 금융 부문의 탄소 배출량이 금융 기관의 직접적인 탄소 발자국보다 100배에서 700배에 달할 가능성이 있다고 지적되고 있으며, 이로 인해 많은 BFSI 사용자에게 있어 카테고리 15 데이터는 시설의 에너지 데이터보다 더 중요해졌습니다. PCAF는 2025년 12월, 추가적인 자산군과 미래를 내다본 전환 금융 지표를 반영하기 위해 기준을 확대함에 따라, 기존의 추정 기법은 현재의 검토 및 보증 요구 사항에 부적합해지고 있습니다. 이에 반해, SAP Fioneer는 2025년 7월에 “Net Zero"모듈을 출시했으며, 라보뱅크는 이를 도입하여 은행 업무 워크플로우 내에서 포트폴리오, 거래 상대방, 자산 및 개별 대출 수준에서의 기후 성과 추적을 진행하고 있습니다. 이에 따라 BFSI 부문에서 그린 IT 소프트웨어의 역할은 변화하고 있습니다. 대출과 관련된 배출량 데이터는 더 이상 외부 공개에만 활용되는 것이 아니라, 신용 심사, 자본 배분, 대출 가격 책정 논리에도 영향을 미치게 되었기 때문입니다. 이러한 연관성이 강화됨에 따라, BFSI 부문 그린 IT 소프트웨어 시장은 독립적인 보고 비용에서 벗어나 위험 관리 예산 쪽으로 점차 이동하고 있습니다.

코어 뱅킹 시스템과 리스크 관리 시스템에 걸쳐 분산된 레거시 데이터

분산된 레거시 시스템 아키텍처는 BFSI 부문 그린 IT 소프트웨어 시장에 큰 걸림돌이 되고 있습니다. 많은 금융 기관들이 여전히 대출, 리스크, 회계 데이터를 지속가능성 메타데이터를 지원하도록 설계되지 않았고 상호 연동되지 않는 플랫폼에 분산하여 보관하고 있기 때문입니다. PCAF의 독자적인 데이터 품질 평가 프레임워크는 이 문제를 여실히 드러내고 있습니다. 왜냐하면, 양질의 대출에 수반되는 배출량 보고에는 검증된 차주 수준의 정보가 필수적인 반면, 많은 금융기관은 여전히 대략적인 추정치나 지역 평균에 의존하고 있기 때문입니다. 그 결과, BFSI 부문 그린 IT 소프트웨어가 기업 차원에서 가치를 제공할 수 있게 되려면, 대부분의 경우 비용이 많이 드는 데이터 추출, 변환 및 거버넌스 작업이 필요합니다. 이로 인해 도입까지 걸리는 기간이 길어지고 통합 비용이 증가하며, 소프트웨어 선정은 제품의 기능뿐만 아니라 데이터 준비 상황에도 크게 좌우되게 됩니다. 여러 관할 구역에서 사업을 영위하는 은행의 경우, 이 문제는 더욱 심각합니다. 지역별 시스템의 차이로 인해 전사적인 통합이 몇 달이 아니라 몇년단위로 지연될 가능성이 있기 때문입니다. 따라서 BFSI 부문 그린 IT 소프트웨어 시장은 레거시 시스템이 다수 존재하는 환경에서 여전히 장벽에 직면해 있으며, 특히 금융 기관이 리스크, 재무, 지속가능성 관련 기록을 단일 관리 프레임워크 내에서 통합하려는 경우 이러한 경향이 두드러집니다.

부문별 분석

2025년에는 클라우드 도입이 시장의 61.78%를 차지했으며, 도입 모델별로는 BFSI 부문 그린 IT 소프트웨어 시장 규모에서 가장 큰 점유율을 기록했습니다. 이러한 주도적인 위상은 BFSI 부문 그린 IT 소프트웨어 시장의 구매자들이 현지 인프라 업그레이드를 기다리지 않고, 규제 개정, 계산 방식 변경 및 보고 논리를 전체 사용자 기반에 반영하기를 원하고 있음을 반영합니다. 또한, 클라우드를 통한 제공은 버전 분산을 완화합니다. 이는 금융기관이 ESRS, PCAF, SSBJ의 각 보고 주기에서 일관된 보고 결과를 필요로 할 때 중요한 요소가 됩니다. 따라서 지속가능성 데이터가 재무, 리스크, 조달, 공급업체 관리 프로세스와 긴밀하게 연계되고 있는 조직에서 클라우드 플랫폼의 매력이 커지고 있습니다. 이러한 경향은 단순히 인프라 비용의 문제에 그치지 않고, 현재는 업데이트 속도, 공유된 통제, 그리고 기업 워크플로우와의 손쉬운 통합을 통해 얻는 가치가 주요 요인으로 작용하고 있습니다.

On-Premise형 시스템은 엄격한 데이터 거주 요건 및 주권 호스팅 규정의 적용을 받는 국영 은행, 보험사 및 정부 관련 기관에서 ESG 및 지속가능성 소프트웨어 업계 내에서 여전히 중요한 위치를 차지하고 있습니다. 이러한 경우, 기밀성이 높은 재무 및 ESG 기록을 어디에 보관할 수 있는지, 그리고 검토 및 보증 과정에서 해당 기록에 어떻게 접근할 수 있는지가 구매 결정의 요인이 됩니다. 하이브리드 모델은 가장 빠르게 성장하고 있는 모델로, 2031년까지 연평균 성장률(CAGR) 21.32%로 확대될 것으로 전망됩니다. 이는 BFSI 부문 그린 IT 소프트웨어 시장이 On-Premise 시스템에서 퍼블릭 클라우드로의 단순한 일방적 전환을 진행하고 있는 것은 아니라는 점을 보여줍니다. 각 기관은 핵심 금융 데이터를 On-Premise에 유지하면서, 분석, 워크플로우 자동화 및 보고서 생성은 클라우드 계층을 통해 실행되는 분할형 아키텍처를 구축하고 있습니다. AWS는 클라우드 기반 지속가능성 보고 환경이 완전한 재구현이 아닌 설정 변경을 통해 변화하는 보고 요건에 적응할 수 있음을 입증했으며, 이는 규제 환경에서의 하이브리드 도입에 대한 실용적인 근거를 뒷받침합니다. IBM의 “API 우선"라는 접근 방식도 이와 같은 방향성을 뒷받침하고 있습니다. 이는 구매자가 인프라를 즉시 교체해야 하는 부담을 지지 않고도 기존 시스템에 배출량 계산 로직을 추가할 수 있기 때문입니다. 이에 따라 BFSI 부문 그린 IT 소프트웨어 시장에서 속도와 더불어 제어성, 감사 가능성, 데이터 주권이 중요시되는 분야에서는 하이브리드 모델이 지속적인 역할을 수행하게 될 것입니다. 따라서 도입 비중은 규제 당국이나 내부 리스크 관리 팀이 설정한 운영상의 한계를 존중하면서도, 클라우드의 복원력을 중시하는 시장의 실태를 반영하고 있습니다.

지역별 분석

북미는 2025년에 시장 점유율의 41.62%를 차지하며, BFSI 부문 그린 IT 소프트웨어 시장에서 가장 규모가 큰 지역 점유율을 기록했고, 2026년에도 계속해서 주요 지역으로서의 위상을 유지하고 있습니다. 이 지역의 규모는 기업들의 조기 도입, 투자자들의 강력한 압력, 그리고 주 차원의 규제가 보고 및 배출량 관리를 기업의 핵심 시스템에 통합하는 데 기여한 역할을 반영하고 있습니다. 캘리포니아주의 SB-253 및 SB-261은 연방 상장 기준 중 어느 하나에도 해당하지 않는 기업이라 하더라도, 해당 주 내에서 실질적인 사업 활동을 수행하는 대기업에 대해 공시 의무를 확대하고 있다는 점에서 특히 중요합니다. 캐나다 역시 연방 규제 대상 금융기관에 기후 리스크에 관한 지침을 제공하고, 자본 시장에서 정보 공개 관행이 더 널리 채택되도록 장려함으로써 지역적 수요를 뒷받침하고 있습니다. 북미 BFSI 부문 그린 IT 소프트웨어 시장은 주요 플랫폼 공급업체들이 집중되어 있다는 점과, 전 세계 출시를 앞두고 많은 제품이 이 지역에서 먼저 테스트되는 역할을 하고 있다는 점에서도 혜택을 보고 있습니다.

유럽은 옴니버스 개정 이후에도 여전히 가장 체계적인 공식 보고 체계를 갖추고 있어, BFSI 부문 그린 IT 소프트웨어 시장 규모에서 구조적으로 중요한 부분을 계속 차지하고 있습니다. 지침(EU) 2026/470은 향후 단계에서 적용 범위를 축소했으나, 이미 적용 범위 내에 있는 사업체에 대해서는 감사 기준 의무, 체계적인 제출 요건 및 핵심적인 무결성에 대한 기대치를 계속해서 유지하고 있습니다. 유럽은행감독청(EBA)의 ESG 리스크 관리 지침은 공시 요건과 더불어 은행 업계에 새로운 수요층을 창출하고 있으며, 이에 따라 유럽 BFSI 부문 그린 IT 소프트웨어 시장에는 독자적인 BFSI 구매 기반이 형성되고 있습니다. 또한, 규제 변경으로 인해 플랫폼 업데이트가 반복되고, 제품의 기능적 깊이, 보증 지원, 데이터 관리가 구매 결정의 핵심 요소가 되기 때문에 유럽은 공급업체에게 여전히 까다로운 지역으로 남아 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 22.37%를 나타낼 것으로 예측되며, BFSI 부문 그린 IT 소프트웨어 시장에서 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 일본 금융청(FSA)이 2026년 2월부터 연차 유가증권 보고서에서 SSBJ 기준에 따른 공시를 의무화함에 따라, 프라임 시장에 상장된 대기업을 대상으로 기후 변화 보고의 필수 요소를 포함한 명확한 규정 준수 일정이 제시되었습니다. 중국의 주요 거래소도 2026년 1월에 지속가능성 보고 지침을 개정하여, 지수 연동형 발행사에 대해 2025년도 지속가능성 보고서를 2026년 4월 30일까지 제출하고, 보다 상세한 환경 보고 요건을 충족할 것을 의무화했습니다. 인도에서 BRSR Core가 도입됨에 따라 제3자 보증 의무가 단계적으로 확대되고 있으며, 더 많은 상장 기업이 의무 적용 대상에 포함됨에 따라 지속적인 조달 사이클이 뒷받침되고 있습니다. 남미에서는 브라질의 정보 공개 체계 구축 및 다국적 기업공급망에 대한 요구 사항을 통해 기여하고 있으며, 중동에서는 탄소 중립 공약과 정부 자본의 우선 과제를 통해 그 중요성이 커지고 있습니다. 또한 아프리카에서는 남아프리카공화국에서 이미 통합 보고 요건이 확립되어 있으며, 그 기세를 이어가고 있습니다. 이러한 상황들이 복합적으로 작용하여 아시아태평양이 주요 성장의 전초기지로 부상하고 있는 한편, 공급업체의 규정 준수 확산, 자본 시장의 기대, 그리고 보고 규정의 점진적인 공식화를 통해 더 광범위한 신흥 지역 전체도 활발한 움직임을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the green IT software for BFSI sector market size is projected to be USD 0.95 billion in 2025, USD 1.15 billion in 2026, and reach USD 2.99 billion by 2031, growing at a CAGR of 21.06% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Software Category (Carbon Management Software, Sustainability Reporting and Management Software, Energy and Resource Optimization Software, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Green IT Software For BFSI Sector Market Trends and Insights

Mandatory ESG Disclosure and Auditability in BFSI

Mandatory disclosure rules are the strongest immediate driver of the Green IT software for BFSI sector market, as regulated institutions can no longer treat sustainability reporting as a voluntary exercise. The 2026 EU Omnibus kept reporting obligations in place for Wave 1 public-interest entities and preserved the need for structured, audit-ready filings, even while later waves were narrowed to larger companies. Japan's Financial Services Agency also formalized SSBJ-aligned disclosure in annual securities reports for large Prime Market companies, indicating that the Green IT software for BFSI sector market is supported by formal securities filing requirements rather than voluntary sustainability statements. India extended BRSR Core assurance obligations from the top 250 to the top 500 listed companies from FY 2025-26, and planned to move to the top 1,000 from FY 2026-27, adding another layer of recurring implementation demand. The pressure is greater for institutions operating in more than one region because they must address double materiality, financial materiality, and local disclosure variations within a single reporting cycle. That is why the Green IT software for BFSI sector market is increasingly rewarding platforms that maintain a single underlying data model and generate multiple framework outputs without rebuilding controls each time.

Financed Emissions Measurement Across Lending and Investment Books

Financed emissions measurement is becoming a core growth engine for the Green IT software for the BFSI sector market, as banks and asset managers need portfolio-level carbon accounting that extends far beyond their own operational footprint. The supplied draft noted that financed emissions can exceed a financial institution's direct footprint by a factor of 100 to 700, which makes Category 15 data more material than facility energy data for many BFSI users. PCAF expanded its standard in December 2025 to include additional asset classes and forward-looking transition finance metrics, making earlier estimation approaches less suitable for current review and assurance needs. SAP Fioneer responded by launching its Net Zero module in July 2025, and Rabobank adopted it to track climate performance at the portfolio, counterparty, asset, and individual loan levels inside banking workflows. This is changing the role of Green IT software in the BFSI sector, as financed emissions data is no longer used solely for external disclosure; it is now affecting credit assessments, capital allocation, and loan pricing logic. As that link strengthens, the Green IT software for BFSI sector market moves closer to risk management budgets and away from isolated reporting spend.

Fragmented Legacy Data Across Core Banking and Risk Systems

Fragmented legacy system architecture is a meaningful brake on the green IT software for BFSI sector market because many financial institutions still store lending, risk, and accounting data across disconnected platforms that were never designed for sustainability metadata. PCAF's own data quality scoring framework makes the issue clear because higher-quality financed emissions reporting depends on verified borrower-level information, while many institutions still rely on broad estimates and regional averages. The result is that implementation often needs costly extraction, transformation, and governance work before the green IT software for BFSI sector market can deliver value at enterprise scale. This slows time-to-deployment, raises integration costs, and makes software selection depend as much on data readiness as on product capability. The problem is even harder for banks operating in several jurisdictions because local system variations can block enterprise-wide consolidation for years rather than months. That is why the green IT software for BFSI sector market still faces friction in legacy-heavy environments, especially when institutions try to align risk, finance, and sustainability records within a single control framework.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native Automation of Sustainability Data Workflows

- AI-Driven Scope 3 Ingestion and Validation

- Limited Availability of Financial-Grade Sustainability Data Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment held 61.78% of the market in 2025, which gives it the largest share of the Green IT software for BFSI sector market size across deployment models. The leading position reflects how buyers in the Green IT software for BFSI sector market want regulatory updates, calculation changes, and reporting logic to be pushed across the user base without waiting for local infrastructure upgrades. Cloud delivery also reduces version fragmentation, which matters when institutions need consistent outputs across ESRS, PCAF, and SSBJ reporting cycles. This has made cloud platforms more attractive in organizations where sustainability data is moving closer to finance, risk, procurement, and supplier management processes. The preference is not only about infrastructure costs, because the main value now comes from the speed of updates, shared controls, and easier integration into enterprise workflows.

On-premises systems remain relevant in the ESG and sustainability software industry for state-owned banks, insurance providers, and government-adjacent entities that operate under strict data-residency or sovereign-hosting rules. In these cases, the buying decision is shaped by where sensitive financial and ESG records can be stored and how they are accessed during review and assurance. Hybrid deployment is the fastest-growing model and is forecast to expand at a 21.32% CAGR through 2031, which shows that the Green IT software for BFSI sector market is not moving in a simple one-way shift from local systems to public cloud. Institutions are building split architectures in which core financial data remains on-premises, while analytics, workflow automation, and reporting outputs run through cloud layers. AWS has demonstrated that cloud-based sustainability reporting environments can adapt to changing reporting requirements through configuration rather than full reimplementation, which supports the practical case for hybrid adoption in regulated settings. IBM's API-first approach reinforces the same direction because buyers can add emissions logic to existing systems without forcing an immediate infrastructure replacement. This leaves the Green IT software for BFSI sector market with a durable role for hybrid models in sectors where control, auditability, and data sovereignty matter as much as speed. The deployment mix, therefore, reflects a market that values cloud resilience while still respecting operational boundaries set by regulators and internal risk teams.

Complete Report Scope:

- By Deployment Mode

- Cloud

- On-Premise

- Hybrid

- By Software Category

- Carbon Management Software

- Sustainability Reporting and Management Software

- Energy and Resource Optimization Software

- Compliance and Risk Management Software

- Supply Chain Sustainability Software

- Environment, Health, and Safety Software

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-pacific

- China

- Japan

- India

- Australia

- South Korea

- Singapore

- Rest of Asia-pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 41.62% of the market in 2025, which gave it the largest regional position in the Green IT software for BFSI sector market share and kept it as the leading geography in 2026. The region's scale reflects early enterprise adoption, strong investor pressure, and the role of state-level regulation in pushing reporting and emissions management into mainstream corporate systems. California's SB-253 and SB-261 are particularly important because they extend disclosure obligations across large companies with material operations in the state, even when those firms are not defined by one federal listing route. Canada also supports regional demand by providing climate risk guidance for federally regulated financial institutions and by promoting the broader adoption of disclosure practices in capital markets. The Green IT software for BFSI sector market in North America also benefits from the concentration of large platform vendors and the region's role as the first testing ground for many product launches before wider global rollout.

Europe remains a structurally important part of the Green IT software for BFSI sector market size because the region still has the deepest formal reporting architecture even after the Omnibus revision. Directive (EU) 2026/470 narrowed the mandatory population for later waves, but it kept audit-grade obligations, structured filing requirements, and core alignment expectations in place for entities already inside scope. The EBA's ESG risk management guidelines create an additional demand layer in banking that operates alongside disclosure requirements, which gives the European Green IT software for BFSI sector market a distinct BFSI purchasing base. Europe also remains a demanding region for vendors because regulatory changes force repeated platform updates and keep product depth, assurance support, and data controls at the center of buying decisions.

Asia-Pacific is forecast to expand at a 22.37% CAGR through 2031, making it the fastest-growing regional block in the Green IT software for BFSI sector market. Japan's February 2026 FSA mandate for SSBJ-aligned disclosures in annual securities reports created a clear compliance timetable for large Prime Market companies, including mandatory climate reporting elements. China's major exchanges also updated their sustainability reporting guidance in January 2026, requiring index-linked issuers to submit 2025 sustainability reports by April 30, 2026, and to meet more detailed environmental reporting expectations. India's BRSR Core rollout is extending third-party assurance obligations incrementally, supporting a continuous procurement cycle as more listed companies enter the mandatory scope. South America contributes through Brazil's developing disclosure framework and multinational supply-chain demands, while the Middle East is gaining relevance through net-zero commitments and sovereign capital priorities, and Africa retains momentum, with integrated reporting requirements already established in South Africa. Together, these conditions make Asia-Pacific the main growth frontier while keeping the broader emerging regional set active through supplier compliance transmission, capital market expectations, and the gradual formalization of reporting rules.

- Microsoft Corporation

- IBM Corporation

- SAP SE

- Salesforce, Inc.

- Workiva Inc.

- Persefoni Inc.

- Watershed Technology Inc.

- Novata, Inc.

- EcoVadis SAS

- Diligent Corporation

- Wolters Kluwer N.V.

- Schneider Electric SE

- Enablon

- Cority Software Inc.

- Sphera Solutions, Inc.

- GreenFi

- SAP Fioneer

- Temenos AG

- Greenly SAS

- Plan A Earth GmbH

- Carbmee GmbH

- Nasdaq, Inc.

- BenchMark Digital Partners LLC

- Measurabl, Inc.

- Intelex Technologies ULC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory ESG Disclosure and Auditability in BFSI

- 4.2.2 Financed Emissions Measurement Across Lending and Investment Books

- 4.2.3 Cloud-Native Automation of Sustainability Data Workflows

- 4.2.4 AI-Driven Scope 3 Ingestion and Validation

- 4.2.5 Convergence of ESG, Risk, and Finance Platforms

- 4.2.6 Green IT Cost Optimization For Branch, Data Center, and Workplace Operations

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Data Across Core Banking and Risk Systems

- 4.3.2 Limited Availability of Financial-Grade Sustainability Data Talent

- 4.3.3 High Integration Burden With Core Banking and Data Warehouses

- 4.3.4 Data Sovereignty and Cross-Border Cloud Compliance Constraints

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Software Category

- 5.2.1 Carbon Management Software

- 5.2.2 Sustainability Reporting and Management Software

- 5.2.3 Energy and Resource Optimization Software

- 5.2.4 Compliance and Risk Management Software

- 5.2.5 Supply Chain Sustainability Software

- 5.2.6 Environment, Health, and Safety Software

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 Singapore

- 5.4.4.7 Rest of Asia-pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 SAP SE

- 6.4.4 Salesforce, Inc.

- 6.4.5 Workiva Inc.

- 6.4.6 Persefoni Inc.

- 6.4.7 Watershed Technology Inc.

- 6.4.8 Novata, Inc.

- 6.4.9 EcoVadis SAS

- 6.4.10 Diligent Corporation

- 6.4.11 Wolters Kluwer N.V.

- 6.4.12 Schneider Electric SE

- 6.4.13 Enablon

- 6.4.14 Cority Software Inc.

- 6.4.15 Sphera Solutions, Inc.

- 6.4.16 GreenFi

- 6.4.17 SAP Fioneer

- 6.4.18 Temenos AG

- 6.4.19 Greenly SAS

- 6.4.20 Plan A Earth GmbH

- 6.4.21 Carbmee GmbH

- 6.4.22 Nasdaq, Inc.

- 6.4.23 BenchMark Digital Partners LLC

- 6.4.24 Measurabl, Inc.

- 6.4.25 Intelex Technologies ULC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment