|

시장보고서

상품코드

2073352

미국의 특급 배송 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Express Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

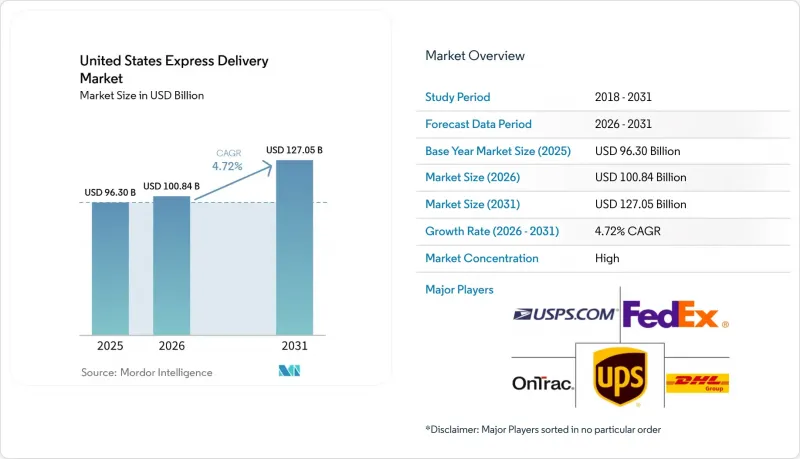

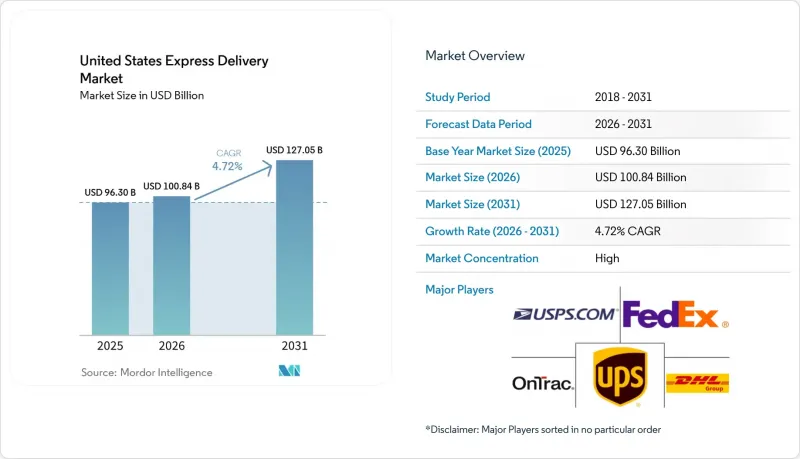

Mordor Intelligence에 의하면, 미국 속달 배송 시장 규모는 2025년에 963억 달러로 평가되었습니다. 2026년 1,008억 4,000만 달러에서 2031년까지 1,270억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.72%를 나타낼 전망입니다.

본 보고서는 최종 사용자 산업별(전자상거래 등), 배송지별(국내 및 국제), 배송 약정별(시간 지정 특송 및 날짜 지정 특송), 운송 수단별(항공, 육상, 기타), 출하 중량별(중량 화물 등), 그리고 모델별(B2B 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 특급 배송 시장 동향 및 인사이트

상위 60개 MSA에서 전자상거래 소포의 당일·익일 배송이 폭발적으로 성장

아마존은 2024년 일본 내에서 당일 또는 익일 배송 주문 40억 건을 처리하며, 지역 밀착형 물류 모델이 업무에 미치는 영향을 밝혀냈습니다. 이러한 성과로 인해 경쟁사들에게도 동등한 배송 속도가 요구되는 연쇄적인 수요가 발생했으며, 미국 당일 배송 시장의 주요 기업 중 99%가 2025년까지 어떤 형태로든 당일 배송 서비스를 제공할 것을 목표로 했습니다. 택배 업체들은 고수익 노선을 확보하기 위해 당일 배송 시설을 두 배로 늘리고, 도시 지역의 분류 능력을 재분배하고 있습니다. 그 때문에 미국의 택배 시장에서는 인구 밀도가 높은 대도시권에 자본이 집중되어 있어, 전국적인 서비스 커버리지 문제가 대두되고 있습니다. 지방 지역에서는 사업자들이 비용이 많이 드는 트럭 운송 경로의 대체 수단으로 드론이나 자율주행 밴의 시범 운행을 실시하고 있으며, 기술 주도의 종합적인 서비스 제공 범위 확대가 추진되고 있습니다.

소매업체들의 마이크로 풀필먼트 센터로의 전환이 "존 0/1"의 특급 배송 물량을 늘리고 있습니다.

자동화된 마이크로 풀필먼트 센터는 소포의 평균 운송 거리를 5마일 미만으로 단축하여, 일반 육로 배송에서도 특급 배송 수준의 속도 목표를 달성할 수 있게 해줍니다. 아마존의 '프로젝트 주니퍼' 이러한 전개는 모듈식 로봇 기술을 통해 이용률이 낮은 소매점을 1시간 이내의 주문 처리 거점으로 개조할 수 있음을 보여줍니다. 익스프레스 사업자들은 이러한 도시형 거점을 기반으로, 구역을 넘나드는 배송, 예약제 수거, 체계적인 반품 서비스를 제공함으로써 추가 수익을 창출하고 있습니다. 그렇긴 하지만, 마이크로 풀필먼트의 규모 확대에는 여전히 막대한 자본이 필요하며, 당초 식료품 분야를 중심으로 고조되었던 열기도 취급량이 정상화됨에 따라 점차 가라앉고 있습니다. 로봇 기술의 지속적인 업그레이드와 유연한 랙 시스템 덕분에 투자 수익률(ROI)이 향상되고 있으며, 붐이 사그라들고 있는 상황에서도 미국의 특급 배송 시장은 프리미엄급이며 지역 밀착형 배송 수요를 확보하고 있습니다.

비용 최적화를 위해 화주가 서비스 등급을 낮추는 가운데, 육상 배송과 특급 배송 간의 모달 전환이 진행되고 있습니다.

화주들은 인플레이션 압력을 완화하기 위해 UPS Ground Saver와 같은 경제적인 서비스 등급으로 전환하고 있습니다. 소비자 조사에 따르면, 구매자의 90%가 무료 배송을 대가로 배송 기간 연장을 수용하고 있으며, 과거 특급 배송에만 국한되었던 ‘"긴급성 프리미엄" 점차 희미해지고 있습니다. 페덱스와 UPS는 2025년에 5.9-6.6%의 전반적인 요금 인상을 단행했으나, 서비스의 신뢰성을 유지하기 위해 육상 운송과 특송 서비스를 통합 운영하고 있습니다. USPS의 "지상 우위"는 신뢰할 수 있는 2-5일 배송 옵션을 경쟁력 있는 가격으로 제공하고 있어, 이익률 압박을 가중시키고 있습니다. 지연 배송 플랜으로의 총 취급량 전환으로 인해, 미국의 특급 배송 시장의 단기적인 수익 확대세가 둔화되고 있습니다.

부문별 분석

2025년, 전자상거래는 미국의 특급 배송 시장 규모의 39.62%를 차지하며, 일일 처리량 전망의 기반이 되었습니다. 의류 및 미용 관련 상품이 배송 건수의 상당 부분을 차지하고 있어, 반품 관리는 중요한 부가 서비스로 자리 잡고 있습니다.

도매·소매업(오프라인)의 수주량은 오프라인 매장 체인이 매장에서 자택으로의 특급 배송 서비스를 시작함에 따라 온라인 전문 경쟁사들과의 서비스 격차가 좁혀짐에 따라, 연평균 성장률(CAGR) 5.62%(2026-2031년)로 가장 빠르게 성장할 것으로 예측됩니다. 제조업은 생산 차질을 최소화하기 위해 익일 배송을 통한 부품 공급에 의존하고 있는 반면, 의료 분야에서는 콜드체인 관리 미흡이 규정 준수 위반으로 인한 벌금으로 이어질 수 있기 때문에 프리미엄 요금을 통한 수익이 주도하고 있습니다. 금융 서비스 업계에서는 소포 발송 건수가 적음에도 불구하고 엄격한 보관 이력 관리가 요구되고 있어, 보안 수준이 높은 특급 배송 서비스에 대한 틈새 프리미엄이 유지되고 있습니다. 따라서 수직적 전문화는 미국의 특급 배송 시장에서 수익성을 유지하기 위한 지속 가능한 전략으로 자리 잡고 있습니다.

국제 특송 시장은 연평균 성장률(CAGR) 5.73%(2026-2031년)을 기록할 것으로 예상되지만, 국내 시장은 2025년 기준으로 미국 특송 시장 규모의 62.10%를 차지하며 더 큰 기반을 유지했습니다. 서류 확인, 관세 계산, 반품 물류 증가로 인해 통관 업무에 강점을 가진 통합 서비스 제공업체는 가격 결정력을 확보하게 되었습니다. USMCA 체제 하에서의 니어쇼어링은 멕시코-미국 등의 역내 운송 경로를 활성화하여 평균 간선 운송 거리를 단축하면서도, 프리미엄 서비스에 대한 수요를 저해하지 않습니다.

국내 시장의 성장세는 둔화되고 있지만, 전자상거래의 집중화, 예비 부품에 대한 긴급한 수요, 운송 지연을 용납할 수 없는 온도 관리가 필요한 의약품 등 수요에 힘입어 성장하고 있습니다. 아마존의 지역별 재고 배치 덕분에 미국 본토 전역에서 24시간 이내 배송에 대한 고객의 기대가 높아졌습니다. 따라서 미국의 특급 배송 시장은 국내 처리량이 네트워크의 밀도를 확보해 주고, 국제 소포가 더 높은 수익을 창출한다는 두 가지 원동력을 갖춘 모델을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united states express delivery market size was valued at USD 96.30 billion in 2025 and estimated to grow from USD 100.84 billion in 2026 to reach USD 127.05 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031).

This report is Segmented by End User Industry (E-Commerce and More), by Destination (Domestic and International), by Delivery Commitment (Time-Definite-Express and Day-Definite-Express), by Mode of Transport (Air, Road and Others), by Shipment Weight (Heavy Weight Shipments and More), and by Model (Business-To-Business and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Express Delivery Market Trends and Insights

Explosive Growth of Same-Day and Next-Day E-Commerce Parcels in Top-60 MSAs

Amazon fulfilled 4 billion same-day or next-day orders domestically in 2024, showcasing the operational impact of its regionalized fulfillment model. This achievement created a cascading requirement for comparable velocity among competitors, with 99% of large players in the United States same day delivery market aiming to offer some form of same-day delivery by 2025. Express carriers are doubling same-day facilities and reallocating urban sortation capacity to protect high-yield corridors. The United States express delivery market is therefore concentrating capital in the densest metropolitan areas, leading to a two-tier service structure that challenges nationwide coverage economics. In rural zones, carriers are piloting drones and autonomous vans as viable substitutes for costly truck-based routes, highlighting a technology-led push for inclusive service reach.

Retailers' Shift to Micro-Fulfillment Centers Boosting "Zone-0/1" Express Volumes

Automated micro-fulfillment centers shorten average parcel miles to under five, enabling ground-priced shipments to meet express-level speed targets. Amazon's Project Juniper roll-out illustrates how modular robotics can retrofit underutilized retail footprints into sub-hour fulfillment nodes. Express providers gain incremental revenue by offering zone-skipping, scheduled pick-ups, and managed returns tailored to these urban nodes. Yet, scaling micro-fulfillment remains capital intensive, and early grocery-focused enthusiasm has moderated as volumes normalize. Continuous robotics upgrades and flexible racking are improving ROI, allowing the United States express delivery market to capture premium, ultra-local traffic despite cooling hype cycles.

Ground-Express Modal Substitution as Shippers Trade Down for Cost Optimization

Shippers are gravitating toward economical tiers such as UPS Ground Saver to mitigate inflationary pressures. Consumer research confirms that 90% of buyers accept longer waits in exchange for free shipping, eroding the urgency premium once unique to express. FedEx and UPS instituted 5.9-6.6% general rate increases for 2025 but are blending ground and express operations to preserve service dependability. USPS's Ground Advantage compounds the margin squeeze by offering reliable two-to-five-day options at aggressive pricing. Aggregate volume migration toward deferred tiers dampens near-term revenue expansion across the United States express delivery market.

Other drivers and restraints analyzed in the detailed report include:

- As Healthcare Cold-Chain Compliance Tightens, Premium Express Services Stand to Gain

- International Inbound Growth on Cross-Border Returns from China-Origin Marketplaces

- Labor Union Agreements Escalating Last-Mile Cost per Stop

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-Commerce held a 39.62% share of the United States express delivery market size in 2025, anchoring daily volume expectations. Apparel and beauty items dominate shipment counts, and returns management is a critical ancillary service.

Wholesale and Retail Trade (Offline) bookings are expected to grow fastest at 5.62% CAGR (2026-2031) as brick-and-mortar chains launched store-to-door express fulfillment, narrowing the service gap with online-only rivals. Manufacturing relies on overnight parts to minimize production disruption, while healthcare drives premium yields because cold chain failures carry compliance penalties. Financial services send fewer parcels but require ironclad chain-of-custody controls, sustaining a niche premium for secure express. Vertical specialization thus remains a durable strategy for margin preservation in the United States express delivery market.

International express is projected to record a 5.73% CAGR (2026-2031) trajectory, while the domestic channel sustained a larger base with 62.10% of the United States express delivery market size in 2025. Increased document verification, tariff calculations, and return logistics confer pricing power on integrators possessing brokerage depth. Nearshoring under the USMCA framework accelerates intra-regional lanes such as Mexico-United States, producing shorter average line-haul distances yet not eroding premium service demand.

Domestic growth, though slower, benefits from e-commerce densification, spare-parts urgency, and temperature-controlled pharmaceuticals that cannot tolerate deferred transit. Amazon's regional inventory placement elevated customer expectations for 24-hour delivery windows across the continental footprint. The United States express delivery market, therefore, maintains a dual-engine model in which domestic volume secures network density and international parcels deliver a higher yield.

Complete Report Scope:

- Destination

- Domestic

- International

- By Route

- Inter-Region

- Intra-Region

- By Route

- Delivery Commitment

- Time-Definite-Express (TDE)

- Day-Definite-Express (DDE)

- Mode of Transport

- Air

- Road

- Others

- Shipment Weight

- Heavy Weight Shipments

- Light Weight Shipments

- Medium Weight Shipments

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- End User Industry

- E-Commerce

- Financial Services (BFSI)

- Healthcare

- Manufacturing

- Primary Industry

- Wholesale and Retail Trade (Offline)

- Others

List of Companies Covered in this Report:

- American Expediting

- Breakaway Courier Systems

- Canada Post Corporation (Including Purolator, Inc.)

- Courier Express

- DHL Group

- Dropoff, Inc.

- ExpressIt Delivery

- FedEx

- International Distribution Services PLC (Inculding GLS)

- Jet Delivery, Inc.

- King Courier

- MedSpeed

- Need It Now Delivers (Formerly A1-SameDay)

- NOW Delivery

- OnTrac (Formerly LaserShip/OnTrac)

- Priority One Courier and Logistics

- Spee-Dee Delivery Service, Inc.

- TFI International, Inc. (Including TForce Logistics)

- United Parcel Service of America, Inc. (UPS)

- United States Postal Service (USPS)

- WeDo Logistics, Ltd. (Including Lone Star Overnight, Inc.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive Growth of Same-Day and Next-Day E-commerce Parcels in Top-60 MSAs (Amazon Prime Effect)

- 4.15.2 Retailers' Shift to Micro-Fulfillment Centers Boosting "Zone-0/1" Express Volumes

- 4.15.3 As Healthcare Cold-Chain Compliance Tightens, Premium Express Temperature-Controlled Services Stand to Gain

- 4.15.4 International Express Inbound Thrives on Rising Cross-Border Returns from China-Origin Marketplaces

- 4.15.5 Subscription Commerce and Direct-to-Consumer Brands Driving Predictable Express Volume Growth

- 4.15.6 "2-hour" Drone/Van Hybrid Networks Gain Traction in B2B Time-Critical Spare-Parts Programs

- 4.16 Market Restraints

- 4.16.1 Ground-Express Modal Substitution as Shippers Trade-Down for Cost Optimization

- 4.16.2 Labor Union Agreements Escalating Last-Mile Cost per Stop

- 4.16.3 Airport Capacity Curfews Limiting Night-Sort Expansion in Tier-1 Hubs

- 4.16.4 Rising Fuel Costs Pressuring Delivery Economics and Route Optimization

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Suppliers

- 4.18.3 Bargaining Power of Buyers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.1.2.1 By Route

- 5.1.2.1.1 Inter-Region

- 5.1.2.1.2 Intra-Region

- 5.1.2.1 By Route

- 5.2 Delivery Commitment

- 5.2.1 Time-Definite-Express (TDE)

- 5.2.2 Day-Definite-Express (DDE)

- 5.3 Mode of Transport

- 5.3.1 Air

- 5.3.2 Road

- 5.3.3 Others

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Model

- 5.5.1 Business-to-Business (B2B)

- 5.5.2 Business-to-Consumer (B2C)

- 5.5.3 Consumer-to-Consumer (C2C)

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 American Expediting

- 6.4.2 Breakaway Courier Systems

- 6.4.3 Canada Post Corporation (Including Purolator, Inc.)

- 6.4.4 Courier Express

- 6.4.5 DHL Group

- 6.4.6 Dropoff, Inc.

- 6.4.7 ExpressIt Delivery

- 6.4.8 FedEx

- 6.4.9 International Distribution Services PLC (Inculding GLS)

- 6.4.10 Jet Delivery, Inc.

- 6.4.11 King Courier

- 6.4.12 MedSpeed

- 6.4.13 Need It Now Delivers (Formerly A1-SameDay)

- 6.4.14 NOW Delivery

- 6.4.15 OnTrac (Formerly LaserShip/OnTrac)

- 6.4.16 Priority One Courier and Logistics

- 6.4.17 Spee-Dee Delivery Service, Inc.

- 6.4.18 TFI International, Inc. (Including TForce Logistics)

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 United States Postal Service (USPS)

- 6.4.21 WeDo Logistics, Ltd. (Including Lone Star Overnight, Inc.)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment