|

시장보고서

상품코드

2073365

스페인의 결제 게이트웨이 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Payment Gateway - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

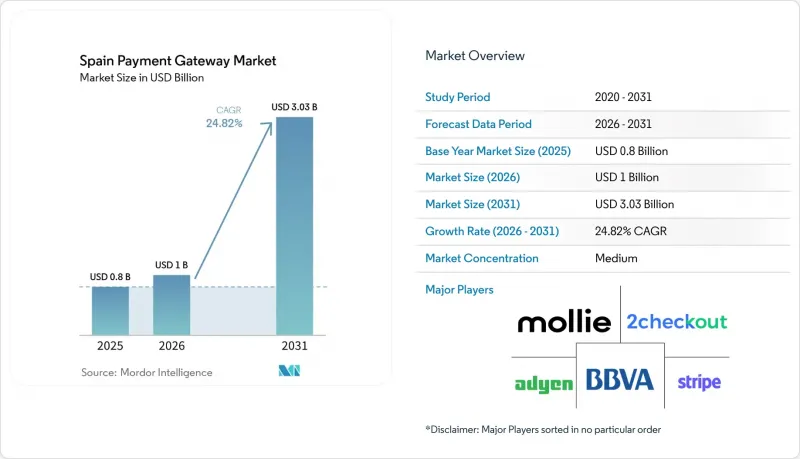

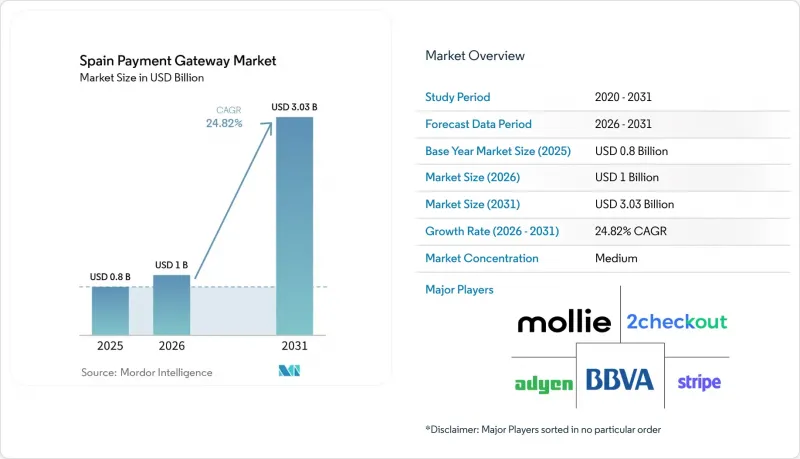

Mordor Intelligence에 의하면, 스페인의 결제 게이트웨이 시장 규모는 2025년 8억 달러로 평가되었습니다. 2026년에는 10억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 24.82%로 성장을 지속하여, 2031년에는 30억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 결제 수단(카드, 디지털 지갑 등), 게이트웨이 유형(호스팅형, 비호스팅형/API), 기업 규모(대기업, 중소기업), 최종 사용자 산업(소매 및 전자상거래, 여행·호텔업 등), 거래 채널(모바일, 데스크톱) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

스페인의 결제 게이트웨이 시장 동향 및 인사이트

대형 가맹점과의 Bizum 연동 이후, 모바일 지갑 이용이 급증했습니다.

Bizum이 P2P 송금에서 오프라인 및 온라인 가맹점 결제로 사업을 전환함에 따라, 은행 앱 이외의 상황에서도 이용이 확대되고 있습니다. 2025년에 시작된 ‘Bizum Pay"를 통해 기존 POS 단말기를 활용하고, 카드 네트워크 수수료를 배제함으로써 당좌예금 계좌에서 직접 NFC 비접촉 결제가 가능해집니다. 결제 시 Bizum을 도입한 대형 소매업체들은 장바구니 포기율이 감소하고 재구매율이 향상되었다고 보고하고 있습니다. 2,600만 명의 사용자(스페인 은행 계좌 보유 인구의 60%)를 보유한 Bizum은 현재 계좌 간 거래의 거의 절반을 차지하고 있습니다. 2029년까지 스마트폰 보급률이 97%에 육박함에 따라, Bizum을 원활하게 통합한 모바일 우선 결제 게이트웨이는 스페인의 결제 게이트웨이 시장에서 증가하는 거래량을 선점할 수 있는 위치에 있습니다.

EU 디지털 결제 패키지를 통한 중소기업 자금 지원

스페인의 30억 6,700만 유로 규모의 “Kit Digital"제도를 통해 중소기업에 대해 전자상거래 플랫폼, 사이버 보안 및 인증된 청구서 발행 소프트웨어 비용이 지원됩니다. 2024년 말까지 53만 건 이상의 보조금이 승인되면서, 온라인 결제 도구 도입이 선순환을 이끌어내는 형태로 급증하고 있습니다. 이전에는 현금에 의존하던 많은 소규모 사업자들이 청구서 발행 및 회계 모듈이 통합된 결제 게이트웨이를 도입함에 따라, 스페인의 결제 게이트웨이 시장의 가맹점 기반이 확대되고 총 처리액도 증가하고 있습니다.

3-D Secure 2.0이 전환율에 미치는 영향

PSD2에 기반한 3-D Secure 2.0의 전면적인 적용은 위험 기반 면제 조치가 무시될 경우 성사된 거래 건수를 최대 20%까지 감소시킬 가능성이 있습니다. 따라서 스페인의 가맹점들은 고위험 거래 흐름에 대해서만 단계적 인증 절차를 실행하는 적응형 리스크 스코어링 기능을 갖춘 결제 게이트웨이에 의존하고 있습니다. 규정 준수를 유지하면서도 원클릭 결제 경험을 제공할 수 있는 결제 서비스 제공업체는 시장 점유율을 확대하고 있는 반면, 세밀한 제어 기능을 갖추지 못한 업체들은 스페인의 결제 게이트웨이 시장에서 가맹점 이탈 위험에 직면해 있습니다.

부문별 분석

2025년, 스페인의 결제 게이트웨이 시장에서 카드는 44.30%의 점유율을 유지했습니다. 이는 주민의 85%가 적어도 한 장의 직불카드나 신용카드를 보유하고 있었기 때문입니다. 그럼에도 불구하고, 디지털 지갑 시장은 연평균 성장률(CAGR) 27.14%를 기록하며 성장하고 있으며, Apple Pay의 이용률이 30%, Google Pay의 보급률이 27%에 달하는 점을 고려할 때, 2031년까지 스페인의 결제 게이트웨이 시장에서 훨씬 더 큰 점유율을 차지할 것으로 전망됩니다.

이러한 성장세는 원활한 토큰화 결제, 생체 인증, 그리고 가맹점에서의 이용 확대에 기인합니다. Bizum이나 SEPA 즉시 송금은 소비자와 가맹점 모두에게 수수료가 없는 선택지를 제공하는 반면, BNPL(후불) 지갑은 재량권이 큰 부문에서 평균 거래액을 끌어올리고 있습니다. 이러한 동향들이 맞물리면서 카드 마진은 축소되는 반면, 처리 총액은 확대되어 스페인의 결제 게이트웨이 시장의 두 자릿수 성장이 지속되고 있습니다.

여행 예약, 렌터카, 법인 경비 결제 등에서는 로열티 프로그램과 전 세계적인 이용 네트워크의 지원 덕분에 카드가 여전히 없어서는 안 될 존재입니다. 그럼에도 불구하고, 발행사는 거래량을 유지하기 위해 카드 정보를 지갑에 통합하고 있으며, 기존의 플라스틱 카드와 모바일 토큰의 경계는 점차 모호해지고 있습니다. 곧 시작될 디지털 유로 시범 사업을 통해 향후 공공 부문의 지갑 옵션이 등장할 가능성도 있지만, 현재로서는 동적 지출 관리나 인라인 쿠폰과 같은 혁신을 주도하고 있는 것은 민간 지갑입니다.

호스트형 게이트웨이는 플러그 앤 플레이 방식의 도입과 PCI 준수 범위의 외부 위탁을 통해 2025년 매출의 68.20%를 차지했습니다. 한편, 데이터 기반 가맹점들이 브랜딩에 대한 완전한 통제권과 세밀한 분석을 요구하는 가운데, 비호스트형/API 모델은 연평균 성장률(CAGR) 26.12%를 기록하며 성장하고 있습니다. 이 변화는 스페인의 결제 게이트웨이 시장에 깊이를 더하고 있습니다. 왜냐하면 API 게이트웨이는 대개 가맹점 1곳당 평균 수익을 높여주는 부가가치 모듈을 함께 제공하고 있기 때문입니다.

주요 플랫폼들은 맞춤형 결제 절차, 네트워크 토큰화, 그리고 지능형 라우팅 방식의 승인 처리를 활용하여 승인률을 높이고 있습니다. 비호스트형 아키텍처에서는 원시 거래 데이터가 공개되므로, 가맹점은 이를 활용하여 코호트 분석, 생애 가치 추적 및 실시간 부정 사용에 대한 인사이트를 얻을 수 있습니다. 이에 반해, 호스팅형 제공업체는 하이브리드형 서비스(내장형 결제 위젯에 더해 선택적인 서버 간 통신)를 제공함으로써, 상위 서비스로 전환하려는 중소기업(SME) 고객을 유지하고자 하고 있습니다.

이러한 도입 경향은 전 세계적인 결제 수단 외에도, 특정 지역에 특화된 결제 수단이 필요한 패션 계열 마켓플레이스나 구독형 미디어 앱에서 두드러지게 나타납니다. 또한, API 게이트웨이는 결제 오케스트레이션 실험을 간소화하고, 가맹점이 비용과 신뢰성을 최적화하기 위해 인수사 간에 트래픽을 동적으로 라우팅할 수 있게 함으로써, 스페인의 결제 게이트웨이 시장에서 경쟁에 따른 고객 이탈을 더욱 심화시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 스페인의 결제 게이트웨이에 관한 애널리스트에 의한 순위

제8장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the spain payment gateway market size is expected to grow from USD 0.80 billion in 2025 to USD 1.00 billion in 2026 and is forecast to reach USD 3.03 billion by 2031 at 24.82% CAGR over 2026-2031.

This report is Segmented by Payment Method (Cards, Digital Wallets and More), Gateway Type (Hosted, Non-Hosted/API), Enterprise Size (Large Enterprise, Small & Medium Enterprise), End-User Industry (Retail & E-Commerce, Travel & Hospitality and More), Transaction Channel (Mobile, Desktop), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Spain Payment Gateway Market Trends and Insights

Surge in Mobile-Wallet Usage Post-Bizum Integration with Large Merchants

Bizum's pivot from peer-to-peer transfers to in-store and online merchant payments expands acceptance beyond banking apps. The 2025 launch of Bizum Pay will enable NFC contactless payments directly from current accounts, leveraging existing POS terminals and eliminating card network fees. Large retailers that embed Bizum at checkout report lower cart-abandonment and higher repeat purchase rates. With 26 million users-60% of Spain's banked population-Bizum now underpins nearly half of all account-to-account transactions. As smartphone penetration nears 97% by 2029, mobile-first gateways that integrate Bizum seamlessly are positioned to capture incremental volumes within the Spain payment gateway market.

EU Digital Payments Package Funding for SMEs

Spain's EUR 3.067 billion Kit Digital scheme reimburses SMEs for e-commerce platforms, cybersecurity, and certified billing software. More than 530,000 grants had been approved by late-2024, creating a self-reinforcing surge in online acceptance tools. Many micro-merchants that previously relied on cash now onboard gateways bundled with invoicing and accounting modules, widening the Spain payment gateway market's merchant base and lifting total processed value.

3-D Secure 2.0 Friction on Conversion Rates

Universal application of 3-D Secure 2.0 under PSD2 can cut completed transactions by up to 20% when risk-based exemptions are ignored. Spanish merchants therefore rely on gateways equipped with adaptive risk scoring that triggers step-up authentication only for high-risk flows. Providers able to sustain compliance while preserving one-click experiences gain share, whereas those lacking granular controls risk merchant attrition within the Spain payment gateway market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Instant-Payment Rails (SEPA Inst) Go Live Q4-2025

- Tourism Rebound Pushes Cross-Border Card Volumes

- AI-Driven Fraud Screening Lowers Gateway Switching Costs

- Interchange-fee cap squeezes PSP margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cards maintained a 44.30% share of the Spain payment gateway market in 2025 as 85% of residents held at least one debit or credit card. Nonetheless, digital wallets are growing at a 27.14% CAGR and are on track to seize a far larger slice of the Spain payment gateway market size by 2031 thanks to Apple Pay's 30% usage and Google Pay's 27% penetration.

The momentum stems from seamless tokenized checkout, biometric authentication, and widening merchant acceptance. Bizum and SEPA instant transfers provide a zero-fee alternative for both consumers and merchants, while BNPL wallets boost average ticket values in high-discretionary segments. Together these trends compress card margins yet expand overall processed value, sustaining double-digit expansion of the Spain payment gateway market.

Cards remain indispensable for travel bookings, car rentals, and corporate expenses, bolstered by loyalty schemes and global acceptance rails. Still, issuers are integrating card credentials into wallets to defend volumes, blurring lines between traditional plastic and mobile tokens. The impending digital euro pilot could later introduce public-sector wallet options, but private wallets presently lead innovations such as dynamic spending controls and inline couponing.

Hosted gateways captured 68.20% of 2025 revenues due to their plug-and-play deployment and outsourced PCI scope. Yet non-hosted/API models are advancing at a 26.12% CAGR as data-driven merchants seek full branding control and granular analytics. The shift adds depth to the Spain payment gateway market because API gateways often bundle value-added modules that raise average revenue per merchant.

Large platforms leverage custom checkout flows, network tokenization, and intelligently routed authorizations to lift approval rates. Non-hosted architectures expose raw transaction data that merchants mine for cohort analysis, lifetime-value tracking, and real-time fraud insights. Hosted providers respond with hybrid offers-embedded checkout widgets plus optional server-to-server calls-in an effort to retain SME customers migrating upward.

Adoption is visible in fashion marketplaces and subscription media apps that demand localized payment methods alongside global ones. API gateways also simplify experimentation with payment orchestration, allowing merchants to route traffic dynamically between acquirers for optimal cost and reliability, reinforcing competitive churn inside the Spain payment gateway market.

Complete Report Scope:

- By Payment Method

- Cards

- Digital Wallets

- Account-to-Account (Bizum, SEPA Inst)

- Buy-Now-Pay-Later

- By Gateway Type

- Hosted

- Non-Hosted / API

- By Enterprise Size

- Large Enterprise

- Small and Medium Enterprise

- By End-User Industry

- Retail and E-commerce

- Travel and Hospitality

- Banking, Financial Services and Insurance

- Media and Entertainment

- Others (Education, Utilities, etc.)

- By Transaction Channel

- Mobile

- Desktop / Other

List of Companies Covered in this Report:

- Adyen N.V.

- Stripe Inc.

- Mollie B.V.

- 2Checkout (Verifone Payments B.V.)

- Banco Bilbao Vizcaya Argentaria S.A.

- PayPal Holdings Inc.

- Authorize.Net (Visa Inc.)

- Amazon Payments Inc.

- Klarna Bank AB

- Bizum S.L.

- Redsys Servicios de Procesamiento S.L.

- Worldline S.A.

- Global Payments Inc.

- CaixaBank Payments and Consumer E.F.C. E.P. S.A.U.

- Banco Sabadell, S.A.

- ING Bank N.V.

- Apple Inc. (Apple Pay)

- Alphabet Inc. (Google Pay)

- PayXpert S.L.U.

- SumUp Payments Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in mobile-wallet usage post-Bizum integration with large merchants

- 4.2.2 EU Digital Payments Package funding for SMEs

- 4.2.3 Mandatory instant-payment rails (SEPA Inst) go live Q4-2025

- 4.2.4 Tourism rebound pushes cross-border card volumes

- 4.2.5 AI-driven fraud-screening lowers gateway switching-costs

- 4.2.6 "Green receipts" tax incentives for e-invoicing

- 4.3 Market Restraints

- 4.3.1 3-D Secure 2.0 friction on conversion rates

- 4.3.2 Interchange-fee cap squeezes PSP margins

- 4.3.3 Cyber-crime surge in account-to-account payments

- 4.3.4 Bank-led push for EPI ONE threatens independent gateways

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 PESTLE Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Payment Method

- 5.1.1 Cards

- 5.1.2 Digital Wallets

- 5.1.3 Account-to-Account (Bizum, SEPA Inst)

- 5.1.4 Buy-Now-Pay-Later

- 5.2 By Gateway Type

- 5.2.1 Hosted

- 5.2.2 Non-Hosted / API

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprise

- 5.3.2 Small and Medium Enterprise

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Travel and Hospitality

- 5.4.3 Banking, Financial Services and Insurance

- 5.4.4 Media and Entertainment

- 5.4.5 Others (Education, Utilities, etc.)

- 5.5 By Transaction Channel

- 5.5.1 Mobile

- 5.5.2 Desktop / Other

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adyen N.V.

- 6.4.2 Stripe Inc.

- 6.4.3 Mollie B.V.

- 6.4.4 2Checkout (Verifone Payments B.V.)

- 6.4.5 Banco Bilbao Vizcaya Argentaria S.A.

- 6.4.6 PayPal Holdings Inc.

- 6.4.7 Authorize.Net (Visa Inc.)

- 6.4.8 Amazon Payments Inc.

- 6.4.9 Klarna Bank AB

- 6.4.10 Bizum S.L.

- 6.4.11 Redsys Servicios de Procesamiento S.L.

- 6.4.12 Worldline S.A.

- 6.4.13 Global Payments Inc.

- 6.4.14 CaixaBank Payments and Consumer E.F.C. E.P. S.A.U.

- 6.4.15 Banco Sabadell, S.A.

- 6.4.16 ING Bank N.V.

- 6.4.17 Apple Inc. (Apple Pay)

- 6.4.18 Alphabet Inc. (Google Pay)

- 6.4.19 PayXpert S.L.U.

- 6.4.20 SumUp Payments Ltd.

7 ANALYST RANKING OF PAYMENT GATEWAYS IN SPAIN

8 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 8.1 White-space and Unmet-need Assessment