|

시장보고서

상품코드

2073390

라이너리스 라벨 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Linerless Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

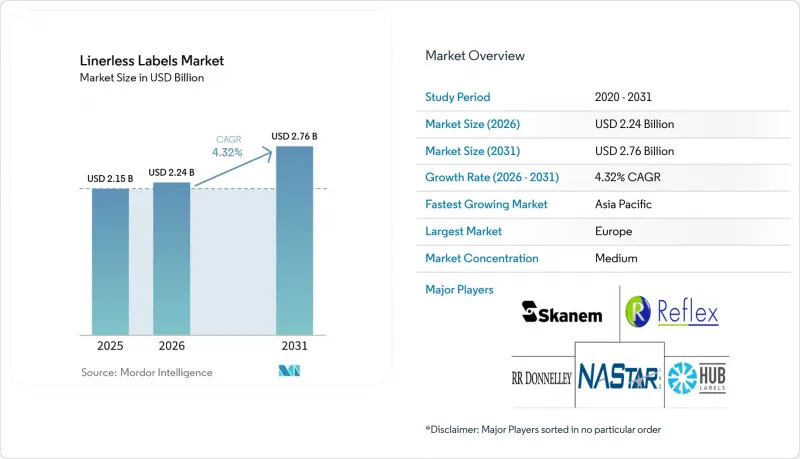

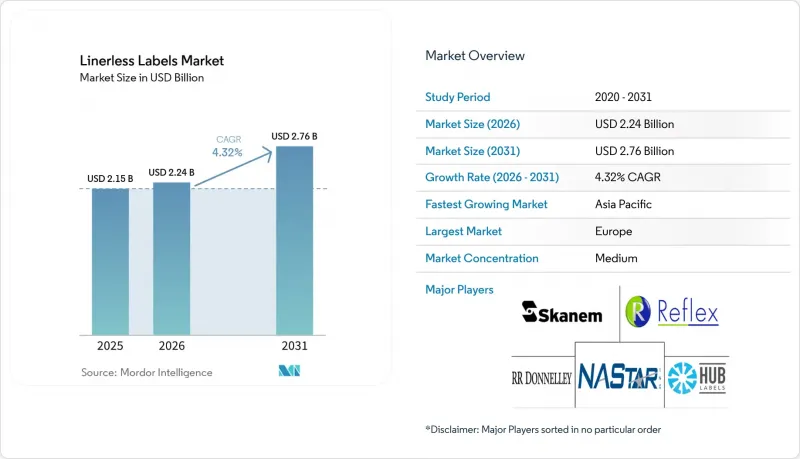

Mordor Intelligence에 의하면, 라이너리스 라벨 시장 규모는 2025년 21억 5,000만 달러로 평가되었습니다. 2026년에는 22억 4,000만 달러로 확대되어 2031년까지 27억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 4.26%로 성장할 전망입니다.

본 보고서는 인쇄 기술(디지털, 플렉소, 그라비아 등), 기판(종이, 필름, 특수·재활용 기판), 접착제 유형(아크릴계 접착제, 핫멜트 접착제 등), 최종 사용자 산업(식품, 음료, 헬스케어 및 의약품, 화장품 및 퍼스널케어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 라이너리스 라벨 시장 동향 및 인사이트

식품 및 음료 포장재에 대한 지속가능성 요구 사항 증가

포장 식품 및 음료 분야의 지속가능성 요건은 자발적인 목표에서 운영상의 요건으로 전환되고 있으며, 이러한 변화가 주요 포장 상품 카테고리 전반에 걸쳐 라이너리스 라벨 시장을 견인하고 있습니다. FINAT는 2026년 EU 시장에 출시될 포장재가 PPWR 체계 하에서 더욱 엄격한 재활용 가능성 요건을 충족해야 한다고 밝히며, 폐기물을 줄이고 자재 흐름을 간소화하는 라벨 형식의 중요성을 강조했습니다. Ravenwood Packaging사는 2025년에 라이너리스 방식이 박리 라이너를 제거함으로써 생산자들이 영국 및 EU의 정책 변화에 대응할 수 있도록 돕고, 이를 통해 폐기물 발생을 줄여 폐기물 처리 부담을 경감하는 데 기여할 것이라고 지적했습니다. 이는 라벨 사용량이 방대하고, 폐기물 처리 계약 재검토가 이미 진행되고 있는 냉장 식품 분야에서 가장 중요한 의미를 지닙니다. 그 결과, 라이너리스 라벨 시장은 성장세를 보이고 있으며, 조달 결정에 있어 지속가능성 목표가 비용 및 규정 준수와 함께 중요한 요소로 자리 잡고 있습니다.

전자상거래 물류의 급속한 성장으로 인해 길이가 가변적인 배송 라벨이 필요해지고 있습니다.

소포 증가로 인해 라이너리스 라벨 시장은 계속해서 성장세를 보이고 있습니다. 이는 연속 롤이 라벨 길이가 가변적이고 신속한 전환이 필요한 대량 출하 업무에 적합하기 때문입니다. 미국 인구조사국의 추산에 따르면, 2025년 소매 전자상거래 매출은 크게 증가했으며, 소매 주문 처리 및 제3자 물류(3PL) 네트워크 전반에 걸쳐 소포 수요가 높은 수준을 유지했습니다. Lowry Solutions사는 2025년에 라이너리스 라벨이 변화하는 포장 형태에 대응할 수 있는 효율적인 인쇄 및 부착 워크플로우가 필요한 물류 및 창고 환경에 가장 적합하다고 설명했습니다. 이 모델의 가치는 밀집된 도시 지역의 물류 거점에서 더욱 높아집니다. 이를 통해 작업자는 자재관리 공정이 줄어들고, 라벨 재고를 보관하는 데 필요한 공간도 줄일 수 있다는 이점을 누릴 수 있습니다. 이러한 상황으로 인해 라이너리스 라벨 시장은 기존의 푸드서비스 분야에 그치지 않고, 주류인 주문 처리 및 배송 용도로 확대되고 있습니다.

기존 라벨링 라인의 개조 비용

개조 비용은 라이너리스 라벨 시장에서 여전히 가장 두드러진 단기적 제약 요인 중 하나이며, 특히 기존 라이너 시스템을 중심으로 구축된 공장이나 물류 센터에서 더욱 두드러집니다. Lowry Solutions는 2025년, 일반적인 데스크톱 및 모바일용 열전사 프린터는 라이너리스 형식을 지원하지 않으며, 전용 시스템에는 비접착 롤러나 전용 활성화 장치와 같은 특수 부품이 필요하다고 지적했습니다. 이로 인해 식품 및 규제 대상 최종 용도 분야에서는 하드웨어 변경이 사내 인증 및 규정 준수 심사를 통과해야 하므로, 전환까지의 과정이 길어집니다. 따라서 라이너리스 라벨 시장은 처음부터 라이너리스 시스템을 도입할 수 있는 신규 사업장과, 투자에 앞서 더 확실한 비용 절감 근거를 필요로 하는 기존 사업장 사이에서 양극화되고 있습니다. 모듈식 업그레이드 방식이 등장하고 있음에도 불구하고, 자본 예산이 제한적인 중소규모의 변환업체나 위탁 포장업체의 경우, 라이너리스 라벨 시장의 보급 속도는 여전히 더딘 상황입니다.

부문별 분석

2025년, 플렉소 인쇄는 라이너리스 라벨 시장에서 40.43%의 점유율을 차지했습니다. 이는 오랜 기간에 걸친 도입 실적, 대량 생산 시의 뛰어난 경제성, 그리고 접착제가 코팅된 페이스 스톡과의 폭넓은 호환성을 반영한 것입니다. 그라비아 인쇄는 여전히 높은 이미지 일관성이 중요시되는 특정 프리미엄 음료 및 화장품 분야에서 보다 제한적인 선택지로 계속 활용되고 있습니다. 스크린 인쇄나 오프셋 하이브리드를 포함한 기타 인쇄 방식은 핵심인 대량 생산 수요보다는 소규모이면서 사양 요건이 까다로운 프로젝트에 대응해 왔습니다. 이러한 도입 실적이 있음에도 불구하고, 라이너리스 라벨 시장은 인쇄 효율뿐만 아니라 가변 데이터, 소량 생산, 통합 추적 기능과 같은 부가가치가 중시되는 디지털 방식으로 더욱 명확하게 전환되고 있습니다.

디지털(잉크젯 및 열전사) 인쇄 시장은 2031년까지 연평균 성장률(CAGR) 5.43%를 나타낼 것으로 예측되며, 이러한 시장 확대에 따라 라이너리스 라벨 업계의 각 변환업체들이 생산 능력, 로트 수, 데이터의 복잡성 간의 균형을 어떻게 맞출지에 대한 접근 방식이 변화하고 있습니다. 『Labels and Labeling』지는 2026년 보고서에서 소량 생산부터 대량 생산에 이르는 다양한 용도에서 일관된 품질과 확장 가능한 생산성을 추구하는 변환업체들에게 1,200 DPI 잉크젯 시스템이 점점 더 매력적인 선택지가 되고 있다고 보도했습니다. 하이브리드 잉크젯 시스템 역시 기존의 후가공 공정이나 기존 인쇄 설비를 포기하지 않으면서도 디지털 방식의 유연성을 더할 수 있기 때문에 보급이 확대되고 있습니다. 웹-투-라벨(Web-to-Label)을 통한 주문이 확대되고 스마트 라벨에 대한 요구 사항이 보편화됨에 따라, 라이너리스 라벨 시장은 플렉소 인쇄가 여전히 중요한 위치를 차지하는 한편, 디지털 인쇄가 빠르게 증가하는 작업량을 흡수하는 혼합 생산 체제로 계속 전환될 가능성이 높다고 볼 수 있습니다.

PP, PET, PE 등의 필름 기재는 식품, 음료, 퍼스널케어 분야에서 뛰어난 내습성, 내화학성, 치수 안정성을 갖추고 있어, 2025년 라이너리스 라벨 시장 규모의 48.23%를 차지했습니다. 한편, 종이 재질의 페이스 스톡은 상온 보관 식품 라벨, 감열 인쇄 용도, 패스트푸드점 영수증, 배송 라벨 등 인쇄 품질에 대한 요구가 비교적 낮고 비용 관리가 더욱 중시되는 분야에서 여전히 중요한 역할을 하고 있습니다. 특수 기재 및 재생 기재는 2031년까지 연평균 성장률(CAGR)이 5.72%를 나타낼 것으로 예측되며, 가장 빠르게 성장하고 있는 표면재 그룹을 형성하고 있습니다. 이러한 구성은 조달 기준에서 재활용성이나 사용 후 제품에서 유래한 소재의 함유 비율이 점점 더 중요시되고 있음에도 불구하고, 라이너리스 라벨 시장이 여전히 검증된 고성능 소재에 의해 지탱되고 있음을 보여줍니다.

UPM Adhesive Materials는 2026년 5월, 식품 및 음료 및 가정용·개인 위생 용도의 경질 PET 및 HDPE 포장재를 위한 ‘UPM ProCycle"포트폴리오를 발표했습니다. 이러한 소재들은 모든 유형의 포장재 및 시장에서 재활용이 가능하다는 점이 독립 기관에 의해 검증되었습니다. 또한, UPM Raflatac사는 2024년 10월, 반환 및 재사용이 가능한 플라스틱 식품 용기를 위해 “OptiCut WashOff"라이너리스 라벨을 출시했습니다. 이 제품은 산업용 세척 시 더 원활한 박리를 가능하게 하여, 포장재 재사용 주기와 더욱 잘 조화를 이룹니다. 라이너리스 라벨 업계에서 이러한 신제품 출시는 소재 혁신이 “참신함"보다는 실제 재활용 및 재사용 시스템과의 호환성을 입증하는 데 중점을 두고 있음을 보여줍니다. 이에 따라 라이너리스 라벨 시장은 지속가능성에 대한 주장이 막연한 메시지가 아닌, 실제 운영에서의 증거를 필요로 하는 용도로 점차 확대되고 있습니다.

지역별 분석

2025년, 유럽은 라이너리스 라벨 시장의 38.82%를 차지했으며, 규제, 변환 업체의 역량, 주요 소매 체인 등이 모두 도입을 뒷받침함에 따라 이 지역에서의 주도적 위치를 유지했습니다. FINAT는 2026년, PPWR(플라스틱 포장 규제)의 방향성이 재활용 가능성에 대한 기대에 부응하면서도 EU 시장 접근성을 유지할 수 있는 포장 방식의 상업적 중요성을 높이고 있다고 보고했습니다. 영국에서는 확대 생산자 책임(EPR)을 통해 병행되는 경제적 인센티브가 더해지면서, 재활용 가능성에 중점을 둔 요금 제도가 재활용이 불가능한 라이너 폐기물의 퇴출을 촉진했습니다. 독일과 프랑스는 여전히 유럽에서 가장 선진적인 국내 시장을 유지하고 있는 반면, 이탈리아 및 기타 유럽 국가에서의 도입은 대규모 식품·물류 업체를 중심으로 집중되는 양상이 지속되었습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.04%로 확대될 것으로 예상되며, 라이너리스 라벨 시장에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 사토 주식회사는 2025년 9월, 아스쿠루가 관동 물류 센터에서 자사의 ‘NonSepa"라이너가 없는 라벨을 도입하고, 전용 자동 라벨 인쇄·부착기를 사용하여 기존의 라이너가 있는 라벨을 대체했다고 발표했습니다. 중국의 물류 업체들도 1급 도시에서 폐기물 처리 비용이 톤당 300위안(톤당 42달러)을 초과하는 환경에서 사업을 전개하고 있으며, 라이너 폐기 문제가 운영 비용의 주요 부담으로 대두되고 있습니다. 따라서 인도, 인도네시아, 베트남, 일본, 한국, 호주는 소포 물량 증가와 라벨링 자동화가 동시에 진행되면서 이 지역의 성장 양상에 기여하고 있습니다.

북미는 여전히 라이너리스 라벨 시장에서 성숙한 지역이며, 이 시장의 확산은 광범위한 연방 정부의 포장 규제보다는 소매업체의 평가 기준, 물류 처리량 및 운영 효율성에 의해 주도되고 있습니다. 미국 인구조사국의 2025년 전자상거래 매출 전망은 소포 처리량이 지속적으로 증가했으며, 이것이 라이너리스 배송 방식에 대한 지속적인 수요의 원동력으로 작용할 것임을 보여주었습니다. 또한 Lowry Solutions사는 2025년에 라이너리스 방식이 효율적인 인쇄 및 부착 작업에 의존하는 창고, 물류 및 퀵서비스 레스토랑의 라벨 부착 이용 사례와 잘 부합한다고 지적했습니다. 남미는 도입 곡선의 초기 단계에 머물러 있으며, 브라질과 아르헨티나가 주요 성장 시장으로 두각을 나타내고 있는 반면, 중동 및 아프리카는 물류 현대화 및 콜드체인에 대한 투자로 이어지는 보다 장기적인 기회를 제시하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the linerless labels market size is expected to increase from USD 2.15 billion in 2025 to USD 2.24 billion in 2026 and reach USD 2.76 billion by 2031, growing at a CAGR of 4.26% over 2026-2031.

This report is Segmented by Printing Technology (Digital, Flexographic, Gravure, and More), Facestock Material (Paper, Film, and Specialty and Recycled Substrates), Adhesive Type (Acrylic Adhesives, Hot-Melt Adhesives, and More), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Linerless Labels Market Trends and Insights

Rising Sustainability Mandates in Food and Beverage Packaging

Sustainability requirements in packaged food and beverage are moving from voluntary goals toward operating requirements, and that shift is supporting the linerless labels market across major packaged goods categories. FINAT stated in 2026 that packaging placed on the EU market will need to meet stricter recyclability requirements under the PPWR framework, underscoring the importance of label formats that reduce waste and simplify material flows. Ravenwood Packaging noted in 2025 that linerless formats help producers respond to UK and EU policy shifts by removing the release liner, thereby reducing disposal needs and supporting lower waste-handling burdens. That matters most in chilled food lines, where label volumes are high, and disposal contracts are already under review. As a result, the linerless labels market is gaining traction, with sustainability goals now sitting alongside cost and compliance in procurement decisions.

E-Commerce Logistics Boom Requiring Variable-Length Shipping Labels

Parcel growth continues to support the linerless labels market, as continuous rolls suit high-volume shipping operations that require variable label lengths and fast changeovers. The United States Census Bureau estimated that retail e-commerce sales in 2025 grew significantly, keeping parcel demand elevated across retail fulfillment and third-party logistics networks. Lowry Solutions explained in 2025 that linerless labeling is well-suited to logistics and warehouse settings that need efficient print-and-apply workflows across changing package formats. The value of this model increases further in dense urban fulfillment sites, where operators benefit from fewer material-handling steps and lower space requirements for label stock. These conditions are helping the linerless labels market expand beyond its earlier food-service base into mainstream fulfillment and shipping applications.

Retrofit Costs for Legacy Labeling Lines

Retrofit spending remains one of the clearest near-term constraints on the linerless labels market, especially in plants and distribution centers built around conventional liner systems. Lowry Solutions noted in 2025 that standard thermal desktop and mobile printers do not support linerless formats, and that dedicated systems require specialized components, such as non-stick rollers and purpose-built activation units. This creates a longer conversion path for food and regulated end uses, where hardware changes must also pass internal qualification and compliance reviews. The linerless labels market is therefore splitting between newer sites that can specify linerless systems from the start and older sites that need a stronger savings case before investing. Even where modular upgrade paths are emerging, the linerless labels market still faces slower adoption among smaller converters and contract packagers with tighter capital budgets.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Waste-Reduction Mandates in Europe and North America

- RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- Raw-Material Price Volatility in Adhesives and Release Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexographic printing held a 40.43% share of the linerless labels market in 2025, reflecting its long installed base, efficient economics in long runs, and broad compatibility with adhesive-coated facestocks. Gravure printing remained a narrower option used in selected premium beverage and cosmetics applications where high image consistency still matters. Other printing formats, including screen and offset hybrids, served smaller, specification-heavy programs rather than core-volume demand. Even with that installed base, the linerless labels market is shifting more clearly toward digital formats where variable data, shorter runs, and integrated tracking functions carry more value than plate efficiency alone.

Digital (inkjet and thermal) printing is projected to grow at a 5.43% CAGR through 2031, and that expansion is changing how converters in the linerless labels industry balance capacity, run length, and data complexity. Labels and Labeling reported in 2026 that 1,200 DPI inkjet systems are becoming more attractive to converters seeking consistent quality and scalable productivity across short- to long-run applications. Hybrid inkjet systems are also gaining ground because they let converters add digital flexibility without abandoning existing finishing and conventional print assets. As web-to-label ordering expands and smart-label requirements become more common, the linerless labels market is likely to keep moving toward a mixed production base where flexo stays important but digital absorbs the faster-growing workloads.

Film substrates, including PP, PET, and PE, accounted for 48.23% of the linerless labels market size in 2025 because they offered strong moisture resistance, chemical durability, and dimensional stability across food, beverage, and personal care use. Paper facestocks remained important for ambient food labeling, direct thermal applications, quick-service restaurant ticketing, and shipping labels, where print quality needs are simpler and cost control matters more. Specialty and recycled substrates formed the fastest-growing facestock group, with a 5.72% CAGR expected through 2031. This mix shows that the linerless labels market is still anchored by proven performance materials, even as procurement standards are increasingly rewarding recyclability and post-consumer content.

UPM Adhesive Materials introduced the UPM ProCycle portfolio in May 2026 for rigid PET and HDPE packaging in food and beverage and home and personal care applications, with the materials independently verified as recycling-compatible across packaging types and markets. UPM Raflatac also launched the OptiCut WashOff linerless label in October 2024 for returnable and reusable plastic food containers, supporting cleaner removal during industrial washing and better alignment with packaging reuse cycles. Within the linerless labels industry, these launches show that material innovation is focused less on novelty and more on proving compatibility with real recycling and reuse systems. That is helping the linerless labels market expand into applications where sustainability claims now need operational evidence rather than broad messaging.

Complete Report Scope:

- By Printing Technology

- Digital (Inkjet and Thermal)

- Flexographic

- Gravure

- Other Printing Technologies

- By Facestock Material

- Paper

- Film (PP, PET, PE)

- Specialty and Recycled Substrates

- By Adhesive Type

- Acrylic Adhesives

- Hot-Melt Adhesives

- Specialty Adhesives

- Other Adhesive Types

- By End-User Industry

- Food

- Beverage

- Healthcare and Pharmaceuticals

- Cosmetics and Personal Care

- Household Chemicals

- Logistics and E-commerce

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Australia

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 38.82% of the linerless labels market in 2025, maintaining its leading regional position, as regulations, converter capabilities, and large retail chains all supported adoption. FINAT reported in 2026 that the PPWR direction strengthens the commercial importance of packaging formats that can meet recyclability expectations and maintain access to the EU market. The UK added a parallel economic driver through Extended Producer Responsibility, with recyclability-weighted fees reinforcing the case for eliminating non-recyclable liner waste. Germany and France remained the most advanced national markets in Europe, while adoption in Italy and the rest of the region stayed more concentrated among larger food and logistics operators.

Asia-Pacific is projected to expand at a 6.04% CAGR through 2031, which makes it the fastest-growing regional segment in the linerless labels market. SATO Corporation announced in September 2025 that ASKUL adopted its NonSepa linerless label at the Kanto Distribution Center, using dedicated automatic label-printing and application machines to replace conventional liner labels. China's logistics operators are also working in an environment where Tier-1 city waste fees above CNY 300 per tonne (USD 42 per tonne), make liner disposal a visible operating cost. India, Indonesia, Vietnam, Japan, South Korea, and Australia are therefore contributing to a regional growth pattern that combines parcel expansion with more automated labeling practices.

North America remained a mature region in the linerless labels market, where adoption was driven more by retailer scorecards, logistics throughput, and operating efficiency than by broad federal packaging mandates. The United States Census Bureau's 2025 e-commerce sales estimate shows why parcel intensity remains a durable demand driver for linerless shipping formats. Lowry Solutions also noted in 2025 that linerless formats align well with warehouse, logistics, and quick-service restaurant labeling use cases that depend on efficient print-and-apply operations. South America remained earlier in its adoption curve, with Brazil and Argentina standing out as the main growth markets, while the Middle East and Africa represented a longer-duration opportunity tied to logistics modernization and cold-chain investment.

- Avery Dennison Corporation

- CCL Industries Inc. and Innovia Films

- 3M Company

- Beontag

- UPM Raflatac

- Coveris

- Hub Labels Inc.

- Reflex Labels Ltd

- Skanem AS

- NAStar Inc.

- Optimum Group

- SATO Europe GmbH

- ProPrint Group

- Lexit Group AS

- R.R. Donnelley and Sons Company

- Gipako UAB

- Lintec Corporation

- HERMA GmbH

- Zebra Technologies Corporation

- Multi-Color Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Sustainability Mandates in Food and Beverage Packaging

- 4.2.2 E-commerce Logistics Boom Requiring Variable-Length Shipping Labels

- 4.2.3 Regulatory Waste-Reduction Mandates in Europe and North America

- 4.2.4 Quick-Service Restaurant Kitchen Automation Driving On-Demand Linerless Printing

- 4.2.5 RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- 4.2.6 Carbon Border Adjustment Mechanisms Elevating Demand for Low-Waste Labeling

- 4.3 Market Restraints

- 4.3.1 Retrofit Costs for Legacy Labeling Lines

- 4.3.2 Raw-Material Price Volatility in Adhesives and Release Coatings

- 4.3.3 Adhesive Build-Up Issues in Cold-Chain Environments

- 4.3.4 Shortage of High-Performance Silicone-Free Adhesives

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Digital (Inkjet and Thermal)

- 5.1.2 Flexographic

- 5.1.3 Gravure

- 5.1.4 Other Printing Technologies

- 5.2 By Facestock Material

- 5.2.1 Paper

- 5.2.2 Film (PP, PET, PE)

- 5.2.3 Specialty and Recycled Substrates

- 5.3 By Adhesive Type

- 5.3.1 Acrylic Adhesives

- 5.3.2 Hot-Melt Adhesives

- 5.3.3 Specialty Adhesives

- 5.3.4 Other Adhesive Types

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Household Chemicals

- 5.4.6 Logistics and E-commerce

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Australia

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc. and Innovia Films

- 6.4.3 3M Company

- 6.4.4 Beontag

- 6.4.5 UPM Raflatac

- 6.4.6 Coveris

- 6.4.7 Hub Labels Inc.

- 6.4.8 Reflex Labels Ltd

- 6.4.9 Skanem AS

- 6.4.10 NAStar Inc.

- 6.4.11 Optimum Group

- 6.4.12 SATO Europe GmbH

- 6.4.13 ProPrint Group

- 6.4.14 Lexit Group AS

- 6.4.15 R.R. Donnelley and Sons Company

- 6.4.16 Gipako UAB

- 6.4.17 Lintec Corporation

- 6.4.18 HERMA GmbH

- 6.4.19 Zebra Technologies Corporation

- 6.4.20 Multi-Color Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment