|

시장보고서

상품코드

2073442

숙신산 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Succinic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

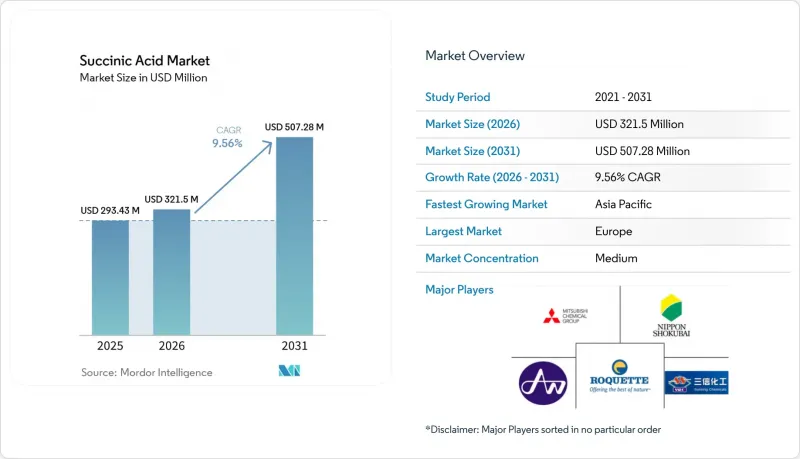

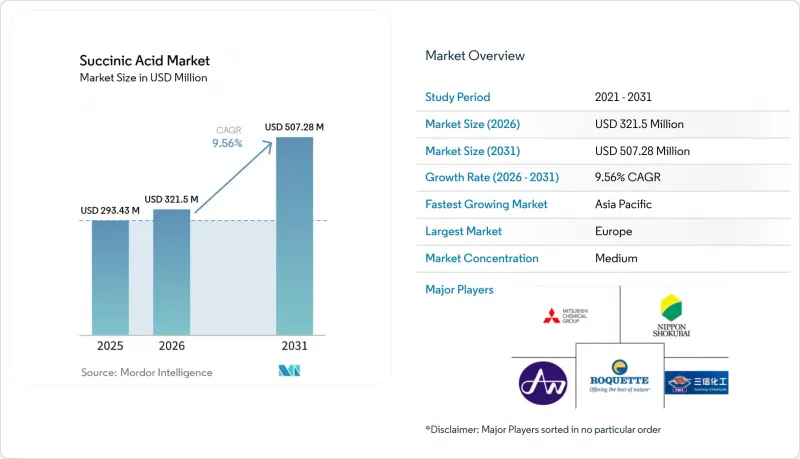

Mordor Intelligence에 의하면, 2026년 숙신산 시장 규모는 3억 2,150만 달러에 달할 것으로 예상되고, 2025년 2억 9,343만 달러에서 확대해, 2031년에는 5억 728만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 9.56%로 성장할 것으로 전망됩니다.

본 보고서는 제품 유형(석유 유래 및 바이오 유래), 등급(공업용/기술용, 식품용, 의약품용, 화장품용), 용도(공업용 화학제품, 식품 및 음료, 의약품, 퍼스널케어 및 화장품, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 숙신산 시장 동향 및 인사이트

생분해성 폴리머에 대한 수요 증가

폴리부틸렌 숙신산(PBS)의 생산은 숙신산 수요의 주요 성장 요인으로 부상하고 있으며, 자동차 및 포장 업계에서는 기존 플라스틱을 대체할 생분해성 대체재의 사용이 의무화되고 있습니다. 뮌헨 공과대학교 연구진은 해양 세균인 Vibrio natriegens를 활용해 발효 효율을 획기적으로 향상시켰으며, 기존의 24-48시간 주기에 비해 생산 시간을 2-3시간으로 단축했습니다. 이러한 기술적 진보로 인해, 그동안 바이오 유래 숙신산의 경쟁력을 제한해 왔던 발효 공정의 확장성이라는 중대한 병목 현상이 해소되었습니다. 폴리머 제조업체들은 순환형 경제 관련 규제를 준수하기 위해 PBS 생산에 바이오 유래 숙신산의 사용을 점점 더 많이 지정하고 있습니다. 특히 유럽에서는 확대 생산자 책임(EPR) 제도에 따라 생분해되지 않는 포장재에 대해 벌칙이 부과되고 있기 때문입니다.

생물 유래 화학 물질에 대한 규제 측면의 지원

바이오 유래 화학물질에 대한 인센티브를 둘러싼 정부의 정책 체계가 구체화되고 있으며, 미국 에너지부가 2025년에 개최한 ‘지속 가능한 화학 원탁 회의’ 이에 따라 숙신산이 산업의 탈탄소화를 위한 우선 플랫폼 화학물질로 지정되었습니다. 바이오 유래 화학물질에 대한 수요가 증가함에 따라, 각국은 생명공학 분야에 막대한 투자를 하고 있습니다. 2024년 과학기술부의 자료에 따르면, 인도 정부는 국내에서 고성능 생명공학 제품 생산을 촉진하기 위해 “BioF3(경제·환경·고용을 위한 생명공학) 정책을 발표했습니다. FDA가 식품 용도의 숙신산을 "일반적으로 안전하다고 인정되는 물질(GRAS)" 이를 승인함으로써 식품 및 음료의 배합에 있어 사용 확대를 가로막던 규제상의 장벽이 제거되었으며, 조미료와 육류 제품에 대해서는 최대 허용 수준이 설정되었습니다. 이러한 규제상의 승인으로 인해, 바이오 유래 숙신산 생산업체에는 우대적인 시장 접근이 보장되는 한편, 검증된 생산 능력을 갖춘 기존 제조업체에 유리한 품질 기준이 확립되어 있습니다.

상업적 규모의 생산 인프라 부족

BioAmber를 비롯한 몇몇 선구적인 기업들의 파산으로 인해, 가용 생산 능력이 감소했을 뿐만 아니라 제조 인프라에 대한 신규 투자도 저해되고 있습니다. 개발도상 지역에서는 발효 시설 건설에 필요한 기술적 전문 지식과 자금 조달 수단이 부족하여, 생산이 기존의 화학 제조 거점에 집중되어 있습니다. 바이오 생산의 특수성으로 인해 기존 화학 플랜트와는 다른 설비 및 공정이 요구되므로, 기존 시설의 용도 변경이 제한되고 자본 요건이 증가하고 있습니다. 원료 공급망의 구축은 생산 능력에 대한 수요를 따라가지 못하고 있으며, 특히 전처리 인프라에 대한 투자가 필요한 비식품계 바이오매스 원료의 경우 그 지연이 두드러집니다.

부문별 분석

바이오 유래 숙신산은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.02%를 나타낼 것으로 예측되는 반면, 석유 유래 숙신산은 2025년 기준 58.82%의 시장 점유율을 유지하고 있습니다. 바이오 생산의 성장률이 높은 것은 규제 요건과 기업의 환경 목표에 힘입어 지속 가능한 제조 방식의 도입이 확대되고 있음을 반영합니다. 바이오 생산으로의 전환은 전 세계적인 지속가능성 노력과 업계 전반에 걸쳐 높아지고 있는 환경 의식과 부합합니다. 석유 기반 생산은 확립된 인프라와 낮은 비용 덕분에 시장에서 주도적인 위치를 유지하고 있으며, 특히 가격에 대한 민감도가 환경적 우려보다 더 큰 산업용 분야에서 이러한 경향이 두드러집니다.

석유 기반 생산의 비용 측면에서의 우위는 수십 년에 걸친 공정 최적화와 기존 시설에서의 규모의 경제에 기인합니다. 바이오 유래 대체품은 식품, 의약품, 화장품 등의 프리미엄 부문에서 지지를 넓혀가고 있습니다. 이러한 분야에서는 지속가능성에 대한 요구가 높은 가격을 정당화하며, 소비자의 선호도가 구매 결정에 영향을 미치고 있습니다. 이러한 프리미엄 부문에서는 친환경 제품에 대한 최종 소비자 수요가 뒷받침되면서, 바이오 유래 생산 방식에 따른 추가 비용을 감수하려는 의지가 높아지고 있습니다.

지역별 분석

유럽은 바이오 유래 화학 물질을 지원하는 확립된 규제 체계와 성숙한 제조 인프라를 바탕으로, 2025년에는 31.64%의 시장 점유율을 차지했습니다. 독일과 프랑스는 다운스트림 공정의 가공 및 유통을 원활하게 하는 통합형 화학 단지를 보유하고 있으며, 지역 내 생산 능력을 주도하고 있습니다. 해당 지역의 포장재에 대한 확대 생산자 책임(EPR) 체계는 바이오 유래 숙신산으로 제조된 생분해성 폴리머에 대한 우선적인 수요를 창출하고 있습니다.

아시아태평양은 중국, 인도, 동남아시아의 급속한 산업화와 제조 능력 확대에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 10.31%를 기록하며 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 베트남에서 바이오 1,4-부탄디올 생산을 위해 효성사가 10억 달러를 투자한 것은 해당 지역이 바이오 화학물질 제조 분야에서 전략적 위치를 차지하고 있음을 보여주는 좋은 사례이며, 이 시설은 2026년까지 연간 5만 메트르톤의 생산 능력을 목표로 하고 있습니다. 화학 제조 분야에서 중국의 우위는 숙신산 생산 규모 확대를 위한 확고한 인프라를 제공하고 있는 반면, 인도에서는 지속적으로 성장하는 제약 및 퍼스널케어 산업이 고품질 제품에 대한 수요 증가를 이끌고 있습니다. 이 지역은 바이오 생산을 위한 비용 대비 효과가 높은 원료인 볏짚이나 옥수수 줄기 등 풍부한 농업 폐기물 원료의 혜택을 누리고 있습니다. 산업의 탈탄소화와 순환형 경제 발전을 지원하는 정부의 정책은 지역 전체에 걸쳐 바이오 화학물질의 도입에 유리한 여건을 조성하고 있습니다.

북미는 저비용 아시아 생산국들의 경쟁 압박에 직면해 있음에도 불구하고, 시장에서 중요한 입지를 유지하고 있습니다. 미국 농무부의 2024년 바이오매스 공급망 보고서는 풍부한 원료의 확보 가능성을 주요 경쟁 우위로 꼽았으며, 확립된 농업 인프라가 재생 가능 원료공급을 뒷받침했습니다. 미국 에너지부의 지속가능한 화학 원탁회의는 산업의 탈탄소화를 위한 플랫폼 화학물질로 숙신산을 우선순위로 삼고 있으며, 국내 생산 발전을 위한 정책 지원을 실시했습니다. 캐나다에서 BioAmber사의 상업화 실패 경험은 리스크 관리 및 시장 개발 전략에 있어 교훈이 되고 있으며, 현실적인 비용 예측과 시장 가격 전망의 중요성을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, succinic acid market size in 2026 is estimated at USD 321.5 million, growing from 2025 value of USD 293.43 million with 2031 projections showing USD 507.28 million, growing at 9.56% CAGR over 2026-2031.

This report is Segmented Into Product Type (Petro and Bio-Based), Grade (Industrial/Technical, Food, Pharmaceuticals, and Cosmetic), Application (Industrial Chemicals, Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Succinic Acid Market Trends and Insights

Rising demand for biodegradable polymers

Polybutylene succinate (PBS) production has emerged as the primary growth catalyst for succinic acid demand, with automotive and packaging industries mandating biodegradable alternatives to conventional plastics. Technical University of Munich researchers achieved breakthrough fermentation efficiency using the marine bacterium Vibrio natriegens, reducing production time to 2-3 hours compared to traditional 24-48 hour cycles. This technological advancement addresses the critical bottleneck of fermentation scalability that previously limited bio-based succinic acid competitiveness. Polymer manufacturers increasingly specify bio-based succinic acid for PBS production to meet circular economy regulations, particularly in Europe, where extended producer responsibility frameworks penalize non-biodegradable packaging materials.

Regulatory support for bio-based chemicals

Government policy frameworks have crystallized around bio-based chemical incentives, with the U.S. Department of Energy's 2025 sustainable chemistry roundtable identifying succinic acid as a priority platform chemical for industrial decarbonization . Owing to the rising demand for bio-based chemicals, various countries are investing heavily in biotechnology initiatives. According to the Ministry of Science and Technology data from 2024, the Government of India launched the BioF3 (Biotechnology for Economy, Environment and Employment) policy to foster high-performance biotechnology manufacturing in the country . FDA recognition of succinic acid as Generally Recognized as Safe (GRAS) for food applications removes regulatory barriers for expanded usage in food and beverage formulations, with maximum allowable levels established for condiments and meat products. These regulatory endorsements create preferential market access for bio-based succinic acid producers while establishing quality standards that favor established manufacturers with proven production capabilities.

Limited commercial-scale production infrastructure

The collapse of several pioneering companies, including BioAmber, has reduced available production capacity while deterring new investment in manufacturing infrastructure. Developing regions lack the technical expertise and capital access required for fermentation facility construction, concentrating production in established chemical manufacturing hubs. The specialized nature of bio-based production requires different equipment and processes compared to traditional chemical plants, limiting the ability to repurpose existing facilities and increasing capital requirements. Feedstock supply chain development lags behind production capacity needs, particularly for non-food biomass sources that require preprocessing infrastructure investment.

Other drivers and restraints analyzed in the detailed report include:

- Expanding food and beverage usage as acidity regulator and flavor enhancer

- Growing demand in personal care and cosmetics

- Competition from alternative bio-based acids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bio-based succinic acid is projected to grow at a CAGR of 11.02% during 2026-2031, while petro-based succinic acid maintains a 58.82% market share in 2025. The higher growth rate of bio-based production reflects increasing adoption of sustainable manufacturing methods, driven by regulatory requirements and corporate environmental goals. The shift toward bio-based production aligns with global sustainability initiatives and growing environmental consciousness across industries. Petro-based production retains its market leadership due to established infrastructure and lower costs, particularly in industrial applications where price sensitivity outweighs environmental concerns.

The cost advantage of petro-based production stems from decades of process optimization and economies of scale in existing facilities. Bio-based alternatives are gaining traction in premium segments such as food, pharmaceuticals, and cosmetics, where sustainability requirements justify higher prices and consumer preferences influence purchasing decisions. These premium segments demonstrate increasing willingness to absorb the additional costs associated with bio-based production methods, driven by end-user demand for environmentally responsible products.

Complete Report Scope:

- By Product Type

- Petro-based

- Bio-based

- By Grade

- Industrial/Technical Grade

- Food Grade

- Pharmaceutical Grade

- Cosmetic Grade

- By Application

- Industrial Chemicals

- Food and Beverage

- Pharmaceuticals

- Personal Care and Cosmetics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Europe commands 31.64% market share in 2025, leveraging established regulatory frameworks supporting bio-based chemicals and mature manufacturing infrastructure. Germany and France lead regional production capacity with integrated chemical complexes that facilitate downstream processing and distribution. The region's extended producer responsibility frameworks for packaging materials create preferential demand for biodegradable polymers derived from bio-based succinic acid.

Asia-Pacific emerges as the fastest-growing region with 10.31% CAGR for 2026-2031, driven by rapid industrialization and expanding manufacturing capacity across China, India, and Southeast Asia. Hyosung's USD 1 billion investment in Vietnam for bio-based 1,4-butanediol production exemplifies the region's strategic positioning in bio-based chemical manufacturing, with the facility targeting 50,000 metric tons of annual capacity by 2026. China's dominance in chemical manufacturing provides established infrastructure for succinic acid production scale-up, while India's growing pharmaceutical and personal care industries create expanding demand for higher-grade products. The region benefits from abundant agricultural waste feedstocks, including rice straw and corn stalks that provide cost-effective raw materials for bio-based production. Government policies supporting industrial decarbonization and circular economy development create favorable conditions for bio-based chemical adoption across the region.

North America maintains a significant market presence despite facing competitive pressure from lower-cost Asian production. The U.S. Department of Agriculture's 2024 biomass supply chain report identifies abundant feedstock availability as a key competitive advantage, with established agricultural infrastructure supporting renewable raw material supply . The U.S. Department of Energy's sustainable chemistry roundtable prioritizes succinic acid as a platform chemical for industrial decarbonization, providing policy support for domestic production development. Canada's experience with BioAmber's failed commercialization provides lessons for risk management and market development strategies, highlighting the importance of realistic cost projections and market pricing assumptions.

- Roquette Freres

- Mitsubishi Chemical Group

- Nippon Shokubai Co., Ltd.

- Air Water Performance Chemical Inc.

- Jinan Finer Chemical Co., Ltd

- Anhui Sunsing Chemicals

- Haihang Group

- Henan GP Chemicals Co.,Ltd

- Kunshan Odowell Co. Ltd

- Royal DSM (Reverdia)

- Wenzhou Blue Dolphin New Material Co., Ltd

- Ensince Industry Co., Ltd

- Carl Roth GmbH + Co. KG

- Axiom Chemicals Pvt. Ltd.

- LCY Biosciences Inc.

- Fengchen Group Co.,Ltd

- Shandong Biotech

- Shandong Feiyang Chemical

- Spectrum Chemical Mfg.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for biodegradable polymers

- 4.2.2 Regulatory support for bio-based chemicals

- 4.2.3 Expanding food and beverage usage as acidity regulator and flavor enhancer

- 4.2.4 Growing demand in personal care and cosmetics

- 4.2.5 Advancements in bio-based production technologies

- 4.2.6 Rising demand for green solvents and industrial chemicals

- 4.3 Market Restraints

- 4.3.1 High production costs

- 4.3.2 Limited commercial-scale production infrastructure

- 4.3.3 Energy-intensive purification undermining eco-benefits

- 4.3.4 Competition from alternative bio-based acids

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Petro-based

- 5.1.2 Bio-based

- 5.2 By Grade

- 5.2.1 Industrial/Technical Grade

- 5.2.2 Food Grade

- 5.2.3 Pharmaceutical Grade

- 5.2.4 Cosmetic Grade

- 5.3 By Application

- 5.3.1 Industrial Chemicals

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceuticals

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Roquette Freres

- 6.4.2 Mitsubishi Chemical Group

- 6.4.3 Nippon Shokubai Co., Ltd.

- 6.4.4 Air Water Performance Chemical Inc.

- 6.4.5 Jinan Finer Chemical Co., Ltd

- 6.4.6 Anhui Sunsing Chemicals

- 6.4.7 Haihang Group

- 6.4.8 Henan GP Chemicals Co.,Ltd

- 6.4.9 Kunshan Odowell Co. Ltd

- 6.4.10 Royal DSM (Reverdia)

- 6.4.11 Wenzhou Blue Dolphin New Material Co., Ltd

- 6.4.12 Ensince Industry Co., Ltd

- 6.4.13 Carl Roth GmbH + Co. KG

- 6.4.14 Axiom Chemicals Pvt. Ltd.

- 6.4.15 LCY Biosciences Inc.

- 6.4.16 Fengchen Group Co.,Ltd

- 6.4.17 Shandong Biotech

- 6.4.18 Shandong Feiyang Chemical

- 6.4.19 Spectrum Chemical Mfg.

- 6.4.20 Thermo Fisher Scientific