|

시장보고서

상품코드

2073443

데스크톱 가상화 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Desktop Virtualization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

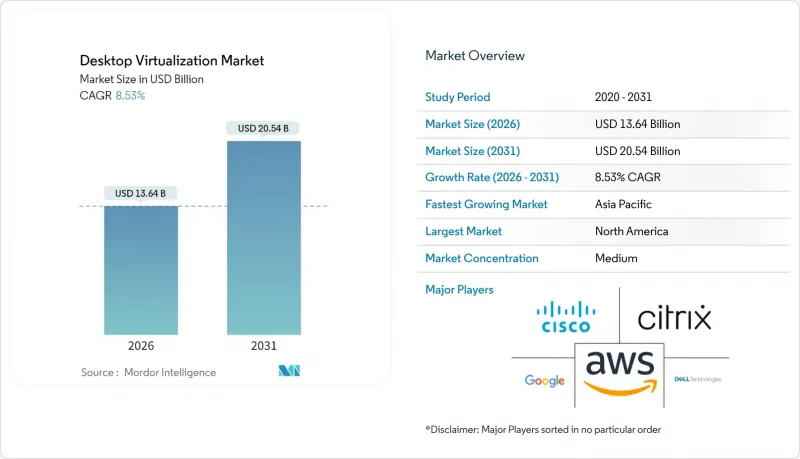

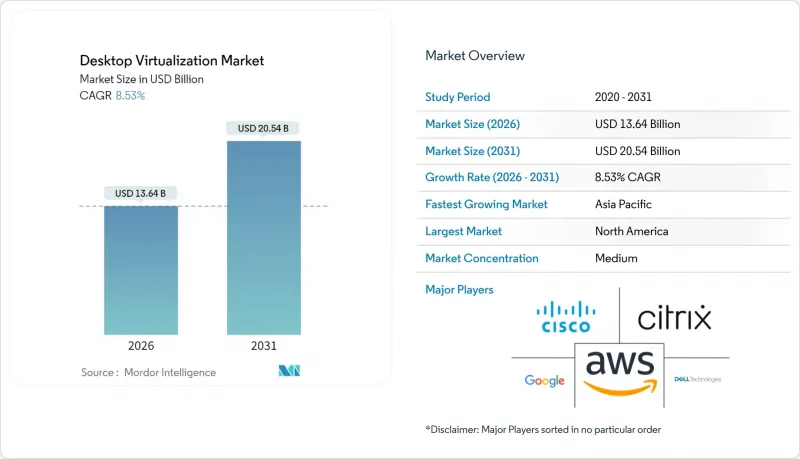

Mordor Intelligence에 의하면, 데스크톱 가상화 시장 규모는 2026년에 136억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR 8.53%로 성장을 지속하여, 2031년에는 205억 4,000만 달러에 이를 전망입니다.

본 보고서는 데스크톱 제공 플랫폼(호스트형 가상 데스크톱, 호스트형 공유 데스크톱, Desktop-As-A-Service), 도입 형태(On-Premise, 클라우드), 최종 사용자 업종(금융 서비스, 의료, 소매 및 전자상거래 등), 조직 규모(중소기업(SME), 대기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 데스크톱 가상화 시장 동향 및 인사이트

BYOD(개인 소유 단말기의 업무용 사용) 정책의 급증

기업들은 하드웨어 비용 절감과 하이브리드 근무 지원을 목적으로 BYOD 프로그램을 도입하고 있지만, 관리 대상에서 제외된 엔드포인트는 기업 자산을 악성코드 및 데이터 유출 위험에 노출시키고 있습니다. NIST 특별 간행물 800-46 Rev. 3에서는 연방 정부 기관에 대해 VDI 세션을 시작하기 전에 장치 상태 점검을 실시할 것을 요구하고 있으며, 민간 기업의 최고정보보안책임자(CISO)들도 사이버 보험 요건을 충족하기 위해 이 권고 사항을 채택하고 있습니다. 데스크톱 가상화는 개인용 기기로 픽셀 데이터만을 스트리밍함으로써, 기밀성이 높은 워크로드와 일반용 운영 체제 사이에 에어 갭을 구축합니다. JPMorgan Chase는 2025년에 6만 명의 트레이더에게 VDI를 도입하여, 직원들이 자택 네트워크를 통해 업무를 수행하는 동안에도 알고리즘 모델을 데이터센터의 엔클레이브 내에 유지할 수 있게 했습니다. 제로 트러스트 프레임워크가 성숙해짐에 따라, 세션 시작 전에 기기의 상태와 사용자의 신원을 확인하는 조건부 액세스 정책이 데스크톱 가상화 시장의 확산을 가속화하고 있습니다.

클라우드 호스팅형 데스크톱 및 DaaS의 급속한 확산

클라우드 네이티브 VDI가 On-Premise 구축을 대체하고 있습니다. 이는 IT 팀이 몇년전부터 피크 시간대의 용량을 예측할 필요가 없어졌기 때문입니다. 기존의 예측 방식에서는 유휴 하드웨어가 발생하거나 성능 병목 현상이 발생하곤 했습니다. Azure Virtual Desktop과 AWS WorkSpaces는 2025년에 자동 확장 기능을 도입하여, 평균 세션 밀도가 80%를 초과하면 90초 이내에 추가 컴퓨팅 리소스를 가동할 수 있게 되었습니다. 지멘스 등 기업들은 200개의 지역별 VDI 클러스터를 3개의 Azure 리전에 통합하고, 데이터센터 임대 계약을 해지함으로써 연간 1,800만 유로(1,944만 달러)의 비용 절감을 실현했습니다. 현재 멀티 클라우드 구축은 벤더 종속성을 방지하기 위한 수단으로 자리 잡고 있으며, 기업의 3분의 1은 데이터 주권 규정을 준수하기 위해 2개 이상의 하이퍼스케일러에서 데스크톱을 운영하고 있습니다.

On-Premise VDI 인프라의 높은 초기 비용

사내 VDI 스택을 구축하려면 하이퍼바이저 라이선스, 공유 스토리지 어레이 및 GPU 지원 서버가 필요하며, 네트워크를 업그레이드하기 전 단계에서 사용자 1인당 2,500달러 이상의 비용이 발생할 수 있습니다. 기업은 하드웨어 장애 시에도 서비스를 유지하기 위해 N+1의 중복성을 확보해야 하므로, 사실상 서버에 대한 지출이 2배가 됩니다. 하이퍼컨버지드 솔루션은 복잡성을 줄여주지만, 그럼에도 자본 투자가 필요하며, 중소기업의 경우 갱신 주기를 통해 그 비용을 상각하기 어렵습니다. 그 결과, 많은 중소기업은 인프라, 패치 적용, 지원을월이용료에 포함시킨 ‘"Desktop-as-a-Service(DaaS)" 구독 서비스를 선호하고 있으며, 이로 인해 비용 곡선이 변화하여 On-Premise 장비에 대한 지출이 감소하고 있습니다.

부문별 분석

호스트형 가상 데스크톱은 2025년 시장 매출의 45.92%를 차지했으나, Desktop-as-a-Service(DaaS) 기반 데스크톱 가상화 시장 규모는 2031년까지 연평균 11.52%의 성장률을 보일 것으로 전망됩니다. 클라우드를 통해 제공되는 데스크톱은 하이퍼바이저 관리가 필요 없게 할 뿐만 아니라, 관리자가 모든 세션에 동일한 보안 기준을 적용할 수 있게 해줍니다. 마이크로소프트는 2025년에 Azure Virtual Desktop과 Intune을 통합하여, 물리적 엔드포인트와 가상 엔드포인트 간에 정책을 상속할 수 있게 했습니다. 소매업 등 계절적 변동이 심한 업계에서는 휴가 기간 동안 사용자 수가 300% 증가하는데, 이는 호스팅형 공유 서버로는 감당할 수 없는 이용 사례입니다. 한편, 주식 거래에서 요구되는 저지연 조건은 여전히 거래소 엔진과 가까운 곳에 설치된 사설 VDI 클러스터의 사용을 정당화하는 요인입니다. 시트릭스의 보고서에 따르면, On-Premise 고객의 68%가 규제가 엄격한 틈새 시장에서 사업을 영위하고 있으며, 하이브리드 환경의 공존이 예측 기간 내내 지속될 것으로 나타났습니다. VMware Horizon Cloud Next-Gen으로 대표되는 새로운 컨테이너 배포 모델은 Docker로 패키지화된 Windows 용도를 HTML5 브라우저를 통해 스트리밍함으로써 경계를 더욱 모호하게 만들고 있습니다.

호스트형 공유 데스크톱은 표준화된 워크로드가 주류를 이루는 학술 연구소나 콜센터에서 틈새 시장을 중심으로 성장세를 보이고 있습니다. Desktop-as-a-Service(DaaS)는 공유 서버를 괴롭혀 온 관리상의 제약을 해소하여, 계약 업체가 인근 세션에 영향을 주지 않고 프로젝트별 플러그인을 설치할 수 있도록 합니다. GPU를 분할하여 활용함으로써, 클라우드 호스팅형 데스크톱은 렌더링 중에만 4GB의 슬라이스를 확보해 디자이너에게 제공할 수 있게 되어, 유휴 상태에서의 과도한 비용을 절감하고 있습니다. 각 벤더사는 블룸버그 단말기나 감사 로그 기능을 탑재한 금융용 DaaS 패키지 등 업계 특화형 번들을 판매하고 있으며, 범용 라이선스에 비해 20% 높은 가격을 책정하고 있습니다. 그 결과, 데스크톱 가상화 시장은 단일 아키텍처로 수렴되지 않고, 제공 방식의 다양화가 계속해서 진행되고 있습니다.

2025년에는 클라우드가 시장 가치의 60.44%를 차지했으며, 하이퍼스케일러가 CPU 사용률 70-80%를 달성함에 따라 데스크톱 가상화 시장에서 클라우드의 점유율은 더욱 확대될 전망입니다. 워크스테이션 프로비저닝에 소요되는 시간이 10분으로 단축되어, On-Premise 구축에 걸리는 3일의 리드타임을 능가하고 있습니다. AWS는 2025년에 195달러의 "WorkSpaces Thin Client" 를 출시했습니다. 이는 클라우드 세션에서 직접 실행되어 엣지 디바이스의 Windows 라이선스 비용을 절감합니다. 데이터 중력의 영향으로 지진 모델링이나 유전체 분석과 같은 워크로드는 여전히 On-Premise에 머물러 있지만, 이러한 분야에서도 외부 위탁 업체를 위해 클라우드 데스크톱을 확보하는 하이브리드 구성에 대한 실험이 진행되고 있습니다. 하이퍼 컨버지드 어플라이언스는 컴퓨팅, 스토리지, 네트워크를 스케일아웃형 노드에 통합함으로써 운영 부담을 줄이고, 기존 SAN에 비해 5년간의 총 소유 비용을 28% 절감합니다.

유럽의 GDPR(EU 개인정보보호규정)에 포함된 현지화 조항에 따라 많은 기업들이 지역 경계 내에서 호스팅되는 프라이빗 클라우드로 전환하고 있으며, 전 세계적인 전환 추세에도 불구하고 On-Premise에 대한 투자는 여전히 유지되고 있습니다. Nutanix AHV 7.0에서는 동적 GPU 할당 기능이 추가되어, 워크로드 통합과 하드웨어 교체 시기를 늦출 수 있게 되었습니다. 제조 현장의 로봇과의 왕복 지연 시간을 10밀리초 미만으로 억제해야 하는 엣지 공장에서는 로컬 노드가 여전히 필수적입니다. 그러나 AWS, Azure, Google Cloud는 주요 서비스를 도시권 내에서 제공하는 메트로·엣지 존을 구축하고 있어, 프라이빗 클러스터의 지연에 대한 주장의 설득력을 약화시키고 있습니다. 예측 기간 동안 대부분의 조직은 경영진을 위해 On-Premise 기반의 영구 데스크톱을 운영하면서, 임시 직원을 위해 클라우드 좌석을 필요에 따라 탄력적으로 활용하게 될 것입니다. 이는 이데올로기적인 것이 아니라, 실용적인 관점에 기반한 도입의 분기점을 보여줍니다.

지역별 분석

북미는 조기 하이브리드 근무 도입 의무화와 넉넉한 클라우드 예산 덕분에 2025년 매출의 37.21%를 차지하며 1위를 차지했습니다. 도입이 신규 도입에서 라이선스 갱신 및 용량 조정으로 전환됨에 따라, 현재 성장세는 둔화되는 추세입니다. 지역 공급업체들은 공공 부문과의 계약 수주를 가능하게 하는 FedRAMP High 및 StateRAMP 인증을 통해 타사와의 차별화를 꾀하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 13.26%를 기록하며, 세계에서 가장 빠른 성장이 예상됩니다. 중국의 '데이터 보안법'은 국내 데이터 저장을 의무화하고 있어, 다국적 기업들은 세션을 해외 지역을 경유하지 않고 현지 VDI 클러스터를 도입하도록 강요받고 있습니다. 인도의 '디지털 인디아' 계획에 따른 자금 투입으로 광섬유 네트워크와 하이퍼스케일 데이터센터가 확대되고 있으며, 이는 교육 기관 및 지방자치단체 산하 진료소에서의 대규모 도입을 위한 전제조건이 되고 있습니다. 차이나모바일 등 통신 사업자가 제공하는 엣지 노드 덕분에 왕복 지연 시간이 20밀리초 미만으로 단축되어, GPU를 많이 사용하는 편집 스위트도 눈에 띄는 지연 없이 클라우드상에서 실행할 수 있게 되었습니다.

유럽에서는 계속해서 꾸준한 도입이 진행되고 있습니다. GDPR(EU 개인정보보호규정)의 현지화 규정에 따라 프라이빗 클라우드 및 소버린 클라우드의 이용이 촉진되고 있으며, CISPE에 따르면 2025년에는 기업의 62%가 회원국 내에서 VDI를 운영하고 있었습니다. 중동 각국 정부는 국가 클라우드 인프라에 투자하고 있으며, 사우디아라비아의 공공투자기금(PIF)은 정부용 데스크톱을 호스팅하는 데이터센터에 64억 달러를 배정했습니다. 남미와 아프리카에서는 광대역 비용과 세제로 인해 총소유비용(TCO)이 상승하고 있어 아직 발전 단계에 머물러 있지만, 브라질과 케냐에서 진행 중인 5G 고정 무선 시범 사업은 2028년까지 전환점이 될 가능성을 시사하고 있습니다. 다국적 기업에게 있어 데스크톱 가상화 시장은 단일한 세계 전개 체제가 아니라, 데이터 소재지법에 따라 규정된 지역별 사일로로 세분화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the desktop virtualization market size is estimated at USD 13.64 billion in 2026, and is expected to reach USD 20.54 billion by 2031, at a CAGR of 8.53% during the forecast period (2026-2031).

This report is Segmented by Desktop Delivery Platform (Hosted Virtual Desktop, Hosted Shared Desktop, and Desktop-As-A-Service), Deployment (On-Premises, and Cloud), End-User Vertical (Financial Services, Healthcare, Retail and E-Commerce, and More), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Desktop Virtualization Market Trends and Insights

Surge in Bring-Your-Own-Device Policies

Organizations have embedded BYOD programs to reduce hardware outlay and support hybrid work, yet unmanaged endpoints expose corporate assets to malware and data exfiltration. NIST Special Publication 800-46 Rev. 3 urged federal agencies to conduct device-posture checks before launching VDI sessions, a recommendation private-sector chief information security officers adopted to satisfy cyber-insurance requirements. By streaming only pixel data to personal devices, desktop virtualization creates an air gap between sensitive workloads and consumer operating systems. JPMorgan Chase delivered VDI to 60,000 traders in 2025, enabling algorithmic models to remain within data-center enclaves while employees worked from home networks. As zero-trust frameworks mature, conditional-access policies that verify device health and user identity before session launch are accelerating desktop virtualization market adoption.

Rapid Adoption of Cloud-Hosted Desktops and DaaS

Cloud-native VDI displaces on-premises builds because IT teams no longer forecast peak capacity years ahead, a practice that created stranded hardware or performance bottlenecks. Azure Virtual Desktop and AWS WorkSpaces introduced autoscaling in 2025, spinning up additional compute within 90 seconds once average session density crosses 80%. Enterprises such as Siemens consolidated 200 regional VDI clusters into three Azure regions, eliminating data-center leases and saving EUR 18 million (USD 19.44 million) annually. Multi-cloud deployment is now a hedge against vendor lock-in, with one-third of enterprises running desktops across two or more hyperscalers to meet data-sovereignty rules.

High Upfront Cost of On-Premises VDI Infrastructure

Building an in-house VDI stack demands hypervisor licenses, shared storage arrays, and GPU-ready servers that can exceed USD 2,500 per user before networking upgrades. Enterprises must provision N+1 redundancy to preserve service during hardware failures, effectively doubling server spend. Hyper-converged alternatives reduce complexity yet still require capital that smaller firms struggle to amortize over refresh cycles. Consequently, many SMEs favor Desktop-as-a-Service subscriptions that bundle infrastructure, patching, and support into monthly fees, shifting the cost curve and drawing spend away from on-premises equipment.

Other drivers and restraints analyzed in the detailed report include:

- Need for Centralized Security and Compliance

- Cost Savings from GPU Virtualization for CAD/CAE Users

- Network Latency and Bandwidth Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hosted Virtual Desktop retained 45.92% of 2025 market revenue, yet the desktop virtualization market size for Desktop-as-a-Service is projected to grow at an annual rate of 11.52% to 2031. Cloud-provisioned desktops eliminate the need for hypervisor management while enabling administrators to enforce identical security baselines on every session. Microsoft integrated Azure Virtual Desktop with Intune in 2025, allowing policy inheritance between physical and virtual endpoints. Seasonal sectors, such as retail, scale seat counts by 300% during holidays, a use case that hosted shared servers cannot match. At the same time, low-latency demands in equities trading still justify the use of private VDI clusters located near exchange engines. Citrix reported 68% of on-premises customers operated in regulated niches, illustrating that hybrid coexistence will persist well into the forecast horizon. Emerging container delivery models, notably VMware Horizon Cloud Next-Gen, blur boundaries further by streaming Docker-packed Windows apps through HTML5 browsers.

Hosted Shared Desktop finds niche growth in academic labs and call centers where standardized workloads prevail. Desktop-as-a-Service (DaaS) removes administrator restrictions that plagued shared servers, allowing contractors to install project-specific plugins without jeopardizing neighboring sessions. GPU-fractionalization now lets cloud-hosted desktops serve designers with 4 GB slices reserved only during rendering, shrinking idle overspend. Vendors market vertical bundles, such as financial DaaS packages that embed Bloomberg terminals and audit logging, commanding 20% premiums over generic seats. Consequently, the desktop virtualization market continues to diversify delivery formats rather than converging on a single architecture.

Cloud held 60.44% of market value in 2025, and its desktop virtualization market share will deepen as hyperscalers achieve 70-80% CPU utilization. Ten-minute workstation provisioning is eclipsing the three-day lead time for on-premises builds. AWS launched a USD 195 WorkSpaces Thin Client in 2025 that boots directly into a cloud session and removes Windows license costs on edge devices. Data gravity keeps seismic modeling and genomic workloads on-premises, but even these sectors experiment with hybrid setups that reserve cloud desktops for contractors. Hyper-converged appliances reduce operational drag by bundling compute, storage, and networking into scale-out nodes, trimming five-year ownership costs by 28% compared with traditional SANs.

Europe's GDPR localization clause steers many enterprises toward private clouds hosted inside regional borders, sustaining on-premises investment despite global migration patterns. Nutanix AHV 7.0 added dynamic GPU assignment, consolidating workloads and postponing hardware refreshes. For edge factories requiring sub-10 ms round-trip to shop-floor robots, local nodes remain indispensable. However, AWS, Azure, and Google Cloud are deploying metro-edge zones that bring core services within city limits, undermining latency arguments for private clusters. Over the forecast horizon, most organizations will run persistent desktops on-premises for executives while bursting cloud seats for contingent staff, illustrating a pragmatic rather than ideological deployment split.

Complete Report Scope:

- By Desktop Delivery Platform

- Hosted Virtual Desktop (HVD)

- Hosted Shared Desktop (HSD)

- Desktop-as-a-Service (DaaS)/Other Forms

- By Deployment

- On-Premises

- Cloud

- By End-User Vertical

- Financial Services

- Healthcare

- Retail and E-commerce

- Manufacturing

- IT and Telecom

- Government and Public Sector

- Education

- Other End-Use Verticals

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America led 2025 revenue at 37.21% due to early hybrid-work mandates and substantial cloud budgets. Growth is now moderating as deployments shift from greenfield to license renewals and capacity tweaks. Regional vendors differentiate through FedRAMP High and StateRAMP certifications that unlock public-sector contracts.

Asia Pacific is projected to post a 13.26% CAGR, the fastest worldwide. China's Data Security Law compels in-country data storage, pushing multinationals to deploy local VDI clusters rather than route sessions through foreign regions. India's Digital India funding is expanding fiber networks and hyperscale data centers, prerequisites for mass rollouts in education and municipal health clinics. Edge nodes from carriers such as China Mobile cut round-trip latency below 20 ms, enabling GPU-intensive editing suites to run in the cloud without perceptible lag.

Europe remains a steady adopter. GDPR localization rules encourage private or sovereign clouds; 62% of enterprises operated VDI inside member-state borders in 2025, according to CISPE. Middle East governments invest in national-cloud infrastructure, with Saudi Arabia's Public Investment Fund allocating USD 6.4 billion for data centers to host government desktops. South America and Africa remain nascent because broadband costs and taxation schemes inflate total cost of ownership, but 5G fixed-wireless pilots in Brazil and Kenya signal a potential inflection by 2028. For multinationals, the desktop virtualization market is fragmenting into regional silos governed by data-residency laws rather than a single global deployment footprint.

- Amazon Web Services, Inc.

- Citrix Systems, Inc.

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Google LLC

- Fujitsu Limited

- Hewlett-Packard Inc.

- Huawei Technologies Co., Ltd.

- IGEL Technology GmbH

- Leostream Corporation

- Microsoft Corporation

- NEC Corporation

- Nutanix, Inc.

- NComputing Co., Ltd.

- Oracle Corporation

- Parallels International GmbH

- Red Hat, Inc.

- Sangfor Technologies Inc.

- Scale Computing, Inc.

- Stratodesk Corporation

- Tencent Cloud Computing (Beijing) Co., Ltd.

- Omnissa LLC

- VMware, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Bring-Your-Own-Device (BYOD) Policies

- 4.2.2 Rapid Adoption of Cloud-hosted Desktops and DaaS

- 4.2.3 Need for Centralized Security and Compliance

- 4.2.4 Cost Savings from GPU Virtualization for CAD/CAE Users

- 4.2.5 Edge-computing-enabled Low-latency VDI Roll-outs

- 4.2.6 Data-residency Regulations Spurring in-country VDI

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of On-premises VDI Infrastructure

- 4.3.2 Network Latency and Bandwidth Constraints

- 4.3.3 Complex Multi-session OS Licensing Models

- 4.3.4 Limited GPU Passthrough on ARM-based Endpoints

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Desktop Delivery Platform

- 5.1.1 Hosted Virtual Desktop (HVD)

- 5.1.2 Hosted Shared Desktop (HSD)

- 5.1.3 Desktop-as-a-Service (DaaS)/Other Forms

- 5.2 By Deployment

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 Financial Services

- 5.3.2 Healthcare

- 5.3.3 Retail and E-commerce

- 5.3.4 Manufacturing

- 5.3.5 IT and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Education

- 5.3.8 Other End-Use Verticals

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Citrix Systems, Inc.

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Google LLC

- 6.4.6 Fujitsu Limited

- 6.4.7 Hewlett-Packard Inc.

- 6.4.8 Huawei Technologies Co., Ltd.

- 6.4.9 IGEL Technology GmbH

- 6.4.10 Leostream Corporation

- 6.4.11 Microsoft Corporation

- 6.4.12 NEC Corporation

- 6.4.13 Nutanix, Inc.

- 6.4.14 NComputing Co., Ltd.

- 6.4.15 Oracle Corporation

- 6.4.16 Parallels International GmbH

- 6.4.17 Red Hat, Inc.

- 6.4.18 Sangfor Technologies Inc.

- 6.4.19 Scale Computing, Inc.

- 6.4.20 Stratodesk Corporation

- 6.4.21 Tencent Cloud Computing (Beijing) Co., Ltd.

- 6.4.22 Omnissa LLC

- 6.4.23 VMware, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment