|

시장보고서

상품코드

2073467

1차 전지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Primary Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

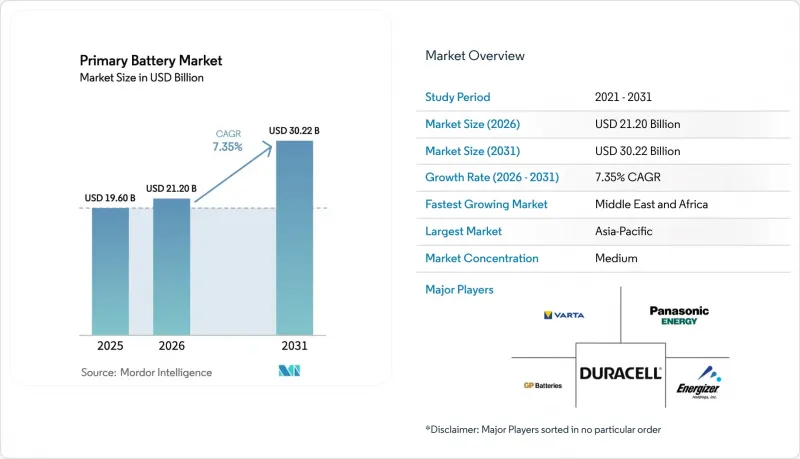

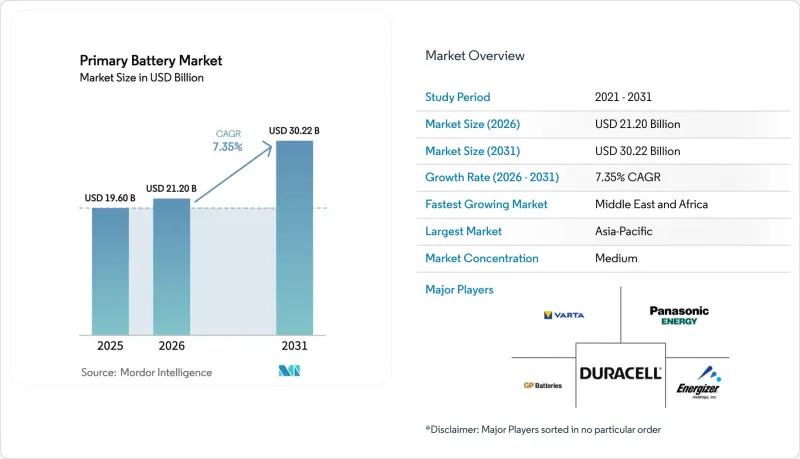

Mordor Intelligence에 의하면, 1차 전지 시장 규모는 2026년에 212억 달러에 달할 것으로 예상되며, 예측 기간(2026-2031년) CAGR7.35%로 성장을 지속하여, 2031년에는 302억 2,000만 달러에 이를 전망입니다.

본 보고서는 유형(알칼리 전지, 1차 리튬 전지, 아연-공기 전지, 아연-탄소/염화물 전지, 산화은 전지, 기타), 형태(원통형, 코인형 및 버튼형 전지, 각형/패키지형, 기타), 용도(소비자용 전자기기, 산업용 및 OEM, IoT 센서 및 스마트 인프라 등), 그리고 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계의 1차 전지 시장 동향 및 인사이트

스마트 홈 및 IoT용 일회용 센서에 대한 수요 급증

LoRaWAN 네트워크에 연결된 기기 수는 2024년에 1억 2,500만 대를 돌파하며 전년 대비 25%의 성장률을 기록했습니다. 도어 센서, 누수 센서, 재실 센서 등 이러한 엔드포인트의 대부분은 AA 알칼리 건전지 또는 코인형 건전지 1개로 최대 10년간 작동할 수 있도록 설계되어 있습니다. 도입 사업자는 충전 인프라를 추가할 때 발생하는 노드당 15-30달러의 비용을 절감할 수 있으므로, 총 소유 비용을 낮게 유지할 수 있습니다. 여러 공급업체가 제공하는 Wi-Fi HaLow 칩셋은 AA 알카라인 건전지 2개로 10년간의 작동을 보장하며, 이를 통해 상업용 건물에서 전원 배선 없이도 사후 설치가 가능해집니다. GSM 협회는 2030년까지 11억 대의 환경 IoT 기기가 보급될 것으로 예측하고 있지만, 에너지 수확에 충분한 빛을 확보할 수 없는 장소에서는 여전히 약 4억 7,300만 대가 1차 전지에 의존하게 될 것입니다. ITU-T L.1310에 규정된 슈퍼커패시터는 수십만 회의 충방전 주기를 견딜 수 있지만, 백업 시간이 매우 짧기 때문에 수명이 긴 1차 전지 화학 계열에 비해 대체재가 아닌 보완적인 역할을 한다는 것이 확인되었습니다.

신흥 시장에서 Off-grid 의료기기의 급속한 보급

세계보건기구(WHO)는 2024년, 사하라 이남 아프리카와 남아시아에서 10억 명의 주민에게 서비스를 제공하는 시설에 여전히 신뢰할 수 있는 전력 공급이 부족하다고 보고했습니다. 이에 따라 10년이라는 장기간 보관이 가능한 1차 리튬 전지를 전원으로 사용하는 맥박 산소 포화도 측정기, 휴대용 초음파 진단 기기, 백신 모니터의 도입이 촉진되고 있습니다. 다자간 은행이 자금을 지원하는 태양광 발전과 에너지 저장을 결합한 마이크로그리드에서는 배터리 관리 시스템의 비용이 정기적인 교체 비용을 초과하는 전력 소비량이 적은 기기를 위해 이러한 배터리가 종종 확보되어 있습니다. 2025년 중반, 웨어러블 의료기기의 전 세계 출하 대수는 5억 5,650만 대에 달했으나, 이 중 18%는 엄격한 부피 에너지 밀도 요건을 충족하기 위해 산화은 전지 또는 리튬 코인 전지가 필요합니다. 보청기의 경우, 아연-공기 버튼형 건전지가 여전히 주류를 이루고 있습니다. 이는 충전식 배터리로는 편의성을 희생하지 않고서는 실현할 수 없는 1.4V, 최대 650mAh의 용량을 극히 소형인 케이스에 담아 제공할 수 있기 때문입니다.

이차 전지 및 슈퍼커패시터와의 경쟁

2025년에는 충전식 리튬 이온 배터리가 전 세계 배터리용량의 83%를 차지하며, 팩 가격을 1kWh당 100달러 미만으로 끌어내렸고, 주변기기, 스피커, 미용 기기 분야에서 1차 전지 시장 점유율을 잠식했습니다. 에너지 밀도에는 한계가 있지만, 50만 사이클 이상의 충방전 횟수를 자랑하는 슈퍼커패시터는 통신 기기의 백업 용도로 입지를 다져가고 있습니다. 다만, 수년 단위의 저전력 공급에는 대응할 수 없습니다. 니켈수소(NiMH) AA 건전지는 중간 정도의 전력을 소비하는 가정용 기기에서 알칼리 1차 전지를 계속해서 대체하고 있지만, 위조 알칼리 건전지의 수입으로 인해 가격은 더욱 하락하고 있으며, 안전성도 훼손되고 있습니다.

부문별 분석

1차 리튬 전지의 각 유형은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.5%를 나타낼 것으로 예측되며, 이는 1차 전지 시장 내에서 가장 높은 성장률입니다. 이는 산업용 계측 기기 및 방위 통신 분야에서 셀당 3.0-3.6V, -40°C-+85°C의 온도 범위에서 작동하는 배터리로의 전환이 진행되고 있기 때문입니다. 한편, 알칼리 건전지는 소매 유통망이 널리 보급되어 있는 덕분에 2025년에는 매출 점유율의 63.5%를 차지했습니다. 보청기 시장에서는 출력 1.4V, 최대 650mAh 용량의 아연-공기 전지가 주류를 이루고 있습니다. 또한, 정밀 시계나 혈당 측정기에서는 산화은 버튼형 건전지가 고가 대를 유지하고 있습니다. 최근 미국의 수입 통계에 따르면, 각 제조업체들이 중국 정련 시장의 지배력에 따른 위험을 분산시키려 하는 가운데, 망간 광석의 수입량이 급증하고 있습니다.

알칼리 건전지의 기존 제조업체들은 재료 과학을 통해 시장 점유율을 지키고 있습니다. 파나소닉의 ‘“EVOLTA NEO”는 티타늄 첨가제가 함유된 고순도 이산화망간을 사용하여 구동 시간을 1.3배로 연장했습니다. 한편, 니켈·아연계 배터리는 보관 기간이 제한적이기 때문에 여전히 틈새 시장 제품으로 남아 있습니다. 아연·탄소 전지는 가격에 민감한 부문에서 여전히 굳건히 자리 잡고 있지만, 알칼리 전지와의 가격 차이가 점차 좁혀지고 있어 시장 점유율이 하락하고 있습니다. 이로 인해 1차 전지 시장에서 점진적인 프리미엄화가 더욱 가속화되고 있습니다.

지역별 분석

2025년, 아시아태평양은 매출의 46.1%를 차지했습니다. 이는 이산화망간의 정제, 아연 분말 생산, 배터리 조립에 이르는 중국의 수직 통합형 비용 우위를 반영한 것입니다. 인도의 "생산 연계형 인센티브(PLI)" 이 제도에 따라 주로 리튬이온 전기차용 배터리 팩을 위해 18GWh의 배터리 생산 능력이 배정되었기 때문에 1차 전지 생산은 소규모 국내 공장에 집중되어 있습니다. 2023년 하반기에 본격적인 생산에 들어간 일본의 니시키하마 공장에서는 매달 4,800만 개의 알카라인 건전지를 생산하고 있으며, 프리미엄 제품인 ‘“EVOLTA NEO”중국 이외공급처가 되고 있습니다. 신흥 아세안 거점인 태국, 베트남, 인도네시아에서는 낮은 인건비와 공급망의 근접성을 활용해 보청기용 코인형 배터리 조립 산업을 유치하고 있습니다.

중동 및 아프리카에서는 분산형 에너지 프로그램을 원동력으로 삼아 2031년까지 연평균 성장률(CAGR) 9.0%를 나타낼 것으로 예측됩니다. 세계은행의 추산에 따르면, 사하라 이남 아프리카에서는 여전히 6억 4,000만-6억 5,000만 명이 전력망에 연결되어 있지 않아, 이에 따라 태양광 발전과 마이크로그리드를 결합한 도입이 추진되고 있으며, 1차 전지는 전력 소비가 적은 모니터링 용도로만 제한적으로 사용되고 있습니다. 남아프리카공화국에서는 2024년 360 MW 규모의 배터리 입찰 및 1,200 MW 규모의 계획 사업에서 주로 장시간 방전이 가능한 재충전식 배터리가 채택되었으며, 1차 전지는 주변적인 원격 측정 용도로만 사용되었습니다. 위조 배터리는 여전히 만연해 있으며, 안전성을 저해할 뿐만 아니라 정품 브랜드 시장 점유율을 잠식하고 있습니다.

북미와 유럽에서는 프리미엄 틈새 시장을 중심으로 시장이 재편되고 있습니다. 에나자이저사는 2025 회계연도에 섹션 45X 세액 공제로 1억 1,240만 달러를 지원받아 국내 생산을 뒷받침하고 있습니다. 이 회사가 2025년 5월에 Advanced Power Solutions NV를 인수함에 따라 폴란드의 생산 능력이 추가되었으나, 단기적으로는 이익률 하락을 초래했습니다. EU의 EPR(확대 생산자 책임) 규제로 인해 규정 준수 비용은 계속해서 상승하고 있지만, 기존 기업들은 신규 진출기업들보다 이를 더 수월하게 감당할 수 있습니다. 남미에서는 전자상거래가 지방 수요를 촉진하고 있어 브라질과 아르헨티나가 성장의 중심이 되고 있지만, 아마존과 파타고니아 지역의 물류 문제가 시장 침투를 더욱 저해하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the primary battery market size is estimated at USD 21.20 billion in 2026, and is expected to reach USD 30.22 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

This report is Segmented by Type (Alkaline, Primary Lithium, Zinc-Air, Zinc-Carbon/Chloride, and Silver-Oxide and Others), Form Factor (Cylindrical, Coin and Button Cells, Prismatic/Packaged, and Others), Application (Consumer Electronics, Industrial and OEM, IoT Sensors and Smart-Infrastructure, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Primary Battery Market Trends and Insights

Surging Demand from Smart-Home & IoT Single-Use Sensors

LoRaWAN networks surpassed 125 million connected devices in 2024, growing 25% year over year, and most of these endpoints, such as door, leak, and occupancy sensors, are engineered for up to 10 years of operation on a single AA or coin-cell. Deployers avoid the USD 15-30 per node expense of adding recharging infrastructure, keeping the total cost of ownership low. Wi-Fi HaLow chipsets from multiple vendors promise a decade of runtime on two AA alkaline cells, which enables retrofits in commercial buildings without wiring for power. Although the GSM Association expects 1.1 billion ambient IoT devices by 2030, roughly 473 million units will still rely on primary batteries in locations that lack sufficient light for energy harvesting. Supercapacitors specified in ITU-T L.1310 offer hundreds of thousands of cycles but only fleeting backup time, confirming their complementary, not substitutive, role against long-duration primary chemistries.

Rapid Growth of Off-Grid Medical Devices in Emerging Markets

The World Health Organization reported in 2024 that facilities serving 1 billion people in sub-Saharan Africa and South Asia still lack reliable electricity, spurring adoption of pulse oximeters, portable ultrasound units, and vaccine monitors powered by primary lithium cells that deliver a decade-long shelf life. Solar-plus-storage microgrids financed by multilateral banks often reserve these cells for low-drain instrumentation where the cost of battery-management systems outweighs the price of periodic replacement. Global shipments of wearable medical devices reached 556.5 million units in mid-2025, 18% of which require silver-oxide or lithium coin cells to meet strict volumetric-energy-density needs. Zinc-air button cells remain dominant in hearing aids because they deliver 1.4 V and up to 650 mAh in tiny housings that rechargeable options cannot match without sacrificing comfort.

Competition from Secondary Batteries & Super-Capacitors

Rechargeable lithium-ion captured 83% of global battery capacity in 2025, pushing pack prices below USD 100 per kWh and eroding primary share in peripherals, speakers, and grooming devices. Despite energy-density limits, supercapacitors boasting 500,000-plus cycles are gaining ground in telecom backup, though they cannot supply multi-year, low-drain power. Nickel-metal-hydride AA cells continue to replace alkaline primaries in mid-drain consumer gear, while counterfeit alkaline imports further depress prices and compromise safety.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Defense Portable Electronics Budgets

- Shift Toward Mercury-Free Chemistries & Green Purchasing Mandates

- Extended Producer Responsibility Fees Inflating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary lithium variants are projected to post a 9.5% CAGR between 2026 and 2031, the quickest within the primary battery market, as industrial metering and defense communications migrate to cells that operate from -40 °C to +85 °C at 3.0-3.6 V per cell. Conversely, alkaline held 63.5% revenue share in 2025 thanks to ubiquitous retail distribution. Zinc-air dominates hearing aids with 1.4-V output and up to 650 mAh capacity, while silver-oxide button cells sustain premium pricing in precision watches and glucose monitors. Recent U.S. import data show manganese-ore volumes escalating as manufacturers hedge against Chinese refining dominance.

Alkaline incumbents defend share through materials science: Panasonic's EVOLTA NEO uses high-purity manganese dioxide with titanium additives to deliver 1.3 times longer runtime. Meanwhile, nickel-zinc variants remain niche due to limited shelf life. Zinc-carbon cells persist in price-sensitive segments but are losing ground as alkaline approaches price parity, reinforcing the gradual premiumization of the primary battery market.

Complete Report Scope:

- By Type

- Alkaline

- Primary Lithium (Li-MnO2, Li-SOCl2, Li-CFx)

- Zinc-Air

- Zinc-Carbon/Chloride

- Silver-Oxide and Others

- By Form Factor

- Cylindrical (AA, AAA, C, D)

- Coin and Button Cells

- Prismatic/Packaged

- Others (Special shapes)

- By Application

- Consumer Electronics

- Industrial and OEM

- Medical and Healthcare

- Defence and Aerospace

- IoT Sensors and Smart-Infrastructure

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific commanded 46.1% of revenue in 2025, reflecting China's vertically integrated cost leadership across manganese dioxide refining, zinc powder production, and cell assembly. India's Production-Linked Incentive scheme earmarked 18 GWh of battery capacity, largely for lithium-ion EV packs, leaving primary cell output concentrated in smaller domestic plants. Japan's Nishikinohama factory, ramped up in late 2023, produces 48 million alkaline cells monthly, providing a non-Chinese source for premium EVOLTA NEO products. Emerging ASEAN hubs, Thailand, Vietnam, and Indonesia, are attracting coin-cell assembly for hearing aids, leveraging low labor costs and supply-chain proximity.

The Middle East & Africa region is expected to post a 9.0% CAGR to 2031, driven by decentralized-energy programs. The World Bank estimates 640-650 million people in sub-Saharan Africa still lack grid power, prompting solar-plus-microgrid deployments that reserve primary batteries for low-drain monitoring. South Africa's 360 MW battery tender in 2024, and its 1,200 MW pipeline, principally features rechargeable chemistries for long-duration discharge, leaving primary cells in peripheral telemetry roles. Counterfeit batteries remain pervasive, undermining safety and eroding legitimate brand share.

North America and Europe are consolidating around premium niches. Energizer received USD 112.4 million in Section 45X credits in fiscal 2025, underpinning domestic production. Its May 2025 purchase of Advanced Power Solutions NV added Polish capacity, albeit at a short-term margin cost. EU EPR mandates continue to lift compliance expenses, which established players can absorb more readily than new entrants. South American growth centers on Brazil and Argentina as e-commerce unlocks rural demand, though logistics obstacles in the Amazon and Patagonia impede deeper penetration.

- Duracell Inc.

- Energizer Holdings Inc.

- Panasonic Energy Co., Ltd.

- GP Batteries International Ltd.

- Saft (TotalEnergies)

- Ultralife Corporation

- FDK Corporation

- Varta AG

- Maxell Holdings, Ltd.

- Sony (Murata Energy)

- Rayovac (Spectrum Brands)

- Fujitsu Batteries

- Camelion Battery Co., Ltd.

- Philips Lighting (Signify)

- Zhejiang Mustang Battery

- EVE Energy Co., Ltd.

- Tianqiu (T&E)

- Renata SA (Swatch Group)

- Xiamen 3-Circle Battery

- Tenergy Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from smart-home & IoT single-use sensors

- 4.2.2 Rapid growth of off-grid medical devices in emerging markets

- 4.2.3 Expansion of defence portable electronics budgets

- 4.2.4 Shift toward mercury-free chemistries & green purchasing mandates

- 4.2.5 Mainstream consumer-electronics replacement cycle

- 4.2.6 E-commerce penetration widening retail reach

- 4.3 Market Restraints

- 4.3.1 Competition from secondary batteries & super-capacitors

- 4.3.2 Extended Producer-Responsibility (EPR) fees inflating costs

- 4.3.3 Raw-material price volatility (zinc, lithium, manganese)

- 4.3.4 Counterfeit battery inflow in Asia & Africa

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Alkaline

- 5.1.2 Primary Lithium (Li-MnO2, Li-SOCl2, Li-CFx)

- 5.1.3 Zinc-Air

- 5.1.4 Zinc-Carbon/Chloride

- 5.1.5 Silver-Oxide and Others

- 5.2 By Form Factor

- 5.2.1 Cylindrical (AA, AAA, C, D)

- 5.2.2 Coin and Button Cells

- 5.2.3 Prismatic/Packaged

- 5.2.4 Others (Special shapes)

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Industrial and OEM

- 5.3.3 Medical and Healthcare

- 5.3.4 Defence and Aerospace

- 5.3.5 IoT Sensors and Smart-Infrastructure

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Duracell Inc.

- 6.4.2 Energizer Holdings Inc.

- 6.4.3 Panasonic Energy Co., Ltd.

- 6.4.4 GP Batteries International Ltd.

- 6.4.5 Saft (TotalEnergies)

- 6.4.6 Ultralife Corporation

- 6.4.7 FDK Corporation

- 6.4.8 Varta AG

- 6.4.9 Maxell Holdings, Ltd.

- 6.4.10 Sony (Murata Energy)

- 6.4.11 Rayovac (Spectrum Brands)

- 6.4.12 Fujitsu Batteries

- 6.4.13 Camelion Battery Co., Ltd.

- 6.4.14 Philips Lighting (Signify)

- 6.4.15 Zhejiang Mustang Battery

- 6.4.16 EVE Energy Co., Ltd.

- 6.4.17 Tianqiu (T&E)

- 6.4.18 Renata SA (Swatch Group)

- 6.4.19 Xiamen 3-Circle Battery

- 6.4.20 Tenergy Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment