|

시장보고서

상품코드

2073550

중동의 태양광발전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East Solar Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

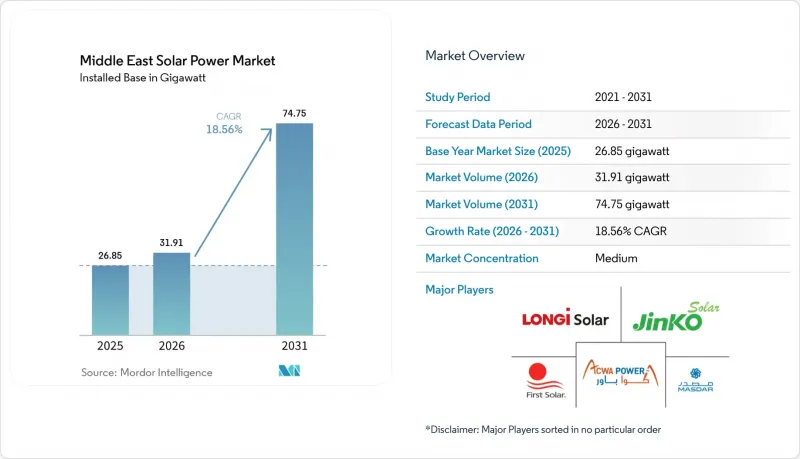

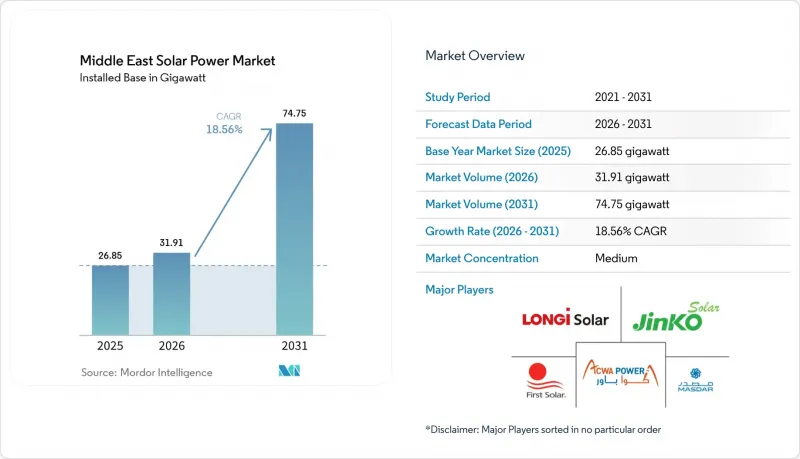

Mordor Intelligence에 의하면, 중동의 태양광발전 시장 규모(설치용량 기반)는 2025년 26.85기가와트로 평가되었습니다. 2026년에는 31.91기가와트로 확대되어 2026년부터 2031년에 걸쳐 CAGR 18.56%로 성장을 지속하여, 2031년에는 74.75기가와트에 이를 것으로 예측됩니다.

본 보고서는 기술별(태양광발전 및 집광형 태양광발전), 계통 연결 유형별(계통 연계형 및 독립형), 최종 사용자별(유틸리티 규모, 상업 및 산업용, 주거용), 그리고 지역별(사우디아라비아, 아랍에미리트, 오만, 쿠웨이트, 카타르, 바레인, 요르단, 이스라엘 및 기타 중동 국가)로 분류되어 있습니다. 시장 규모 및 전망은 설치 용량(GW) 단위로 표시되어 있습니다.

중동의 태양광발전 시장 동향 및 인사이트

각국의 재생에너지 목표와 대규모 입찰

전국 규모의 프로그램은 시범 입찰에서 수 기가와트 규모의 블록으로 확대되고 있으며, 중동의 태양광발전 시장에 안정적인 전력 구매 파이프라인을 창출하고 있습니다. 2025년 10월에 실시된 사우디아라비아의 제6차 입찰에서는 8개 부지에서 4.5GW가 kWh당 1.09682 미국 센트라는 사상 최저가로 낙찰되었으며, 이를 통해 태양광발전을 기저부하 자산으로 자리매김하겠다는 정부의 의지가 강조되었습니다. 이에 이어, UAE의 전력 회사인 EWEC는 1GW 규모의 태양광발전과 400MW 규모의 배터리 저장 설비를 결합한 RFP(제안 요청서)를 발표했으며, 안정적인 전력 공급을 요건으로 제시함으로써 조절 가능한 재생에너지로의 전환을 시사했습니다. 오만의 이브리 III 프로젝트 최종 후보 선정과 쿠웨이트의 알 디브디바 입찰이 더해지면서, 지역 전체의 프로젝트 총량은 15GW를 넘어섰습니다. 현재 입찰 규정에서는 IEC-61215 및 IEC-61730 인증을 의무화하고 있어, 품질 기준이 강화되고 보증 위험이 감소하고 있습니다. 입찰부터 금융 마감까지의 기간이 15개월로 단축됨에 따라, 공급업체는 해당 지역 내에 재고를 보유할 수밖에 없게 되었으며, 이에 따라 기존의 조달 주기가 40% 가까이 단축되었습니다.

MONO-PERC 및 TOPCon 태양전지 모듈의 LCOE 감소

TOPCon 기술의 급속한 보급으로 모듈의 변환 효율은 25%를 넘어섰으며, PERC와 비교했을 때의 가격 차이는 5% 미만으로 줄어들었습니다. JinkoSolar가 사우디아라비아 공공투자기금(PIF)과 공동으로 설립한 10억 달러 규모의 TOPCon 합작 사업은 2026년 초부터 연간 10GW를 공급했으며, 생산 단가를 최대 12% 절감할 것으로 전망됩니다. 2024년에 Desert Technologies사가 제다에서 가동을 시작한 5GW 규모의 발전소는 현지 공급 체계를 한층 더 확대할 것입니다. 양면 수광형 TOPCon 모듈은 사막의 높은 알베도 지역에서 10%에서 15%의 추가 발전량을 가져옵니다. 이로 인해 현지 발전 규모가 확대되고, 입찰 체계에서 국산 부품 사용 시 할인 혜택이 적용됨에 따라 전기 요금이 인하되어 가스 발전과의 비용 격차가 더욱 벌어지면서, 중동의 태양광발전 시장은 거의 전면적인 도입으로 나아가고 있습니다.

송전망의 혼잡 및 간헐성 관리 비용

송전망의 업그레이드가 유틸리티 규모의 확장을 따라가지 못하고 있어, 개발업체들은 변전소 건설 비용을 부담할 수밖에 없으며, 이로 인해 설비 투자(CAPEX)가 최대 12% 증가하고 있습니다. 사우디아라비아 동부 주에서는 정오 시간대에 평균 8%-15%의 출력 제한이 발생하고 있어, 내부수익률(IRR)을 저하시키고 있습니다. 2024년 Sungrow사가 낙찰받은 7.8 GWh 규모의 배터리 입찰은 2030년까지 10 GW의 저장 용량을 목표로 하는 것이지만, 인산철리튬계 시스템의 비용은 250-350달러/kWh이며, 내부수익률(IRR)을 150-200 베이시스 포인트 낮추고 있습니다. UAE 북부 에미리트에서도 유사한 과제가 나타나고 있으며, EWEC는 400 MW/800 MWh의 저장 용량을 요구하고 있습니다. 쿠웨이트의 알 디브디바 프로젝트에서는 전용 400kV 송전선이 필요하게 되면서 공사 기간이 2배인 7년으로 늘어났고, 송전망에 대한 투자액이 1억 8,000만 달러 증가했습니다. 무효 전력 공급 의무와 동기 진상기 도입으로 인해 시스템 외부 설비(BOS) 예산이 더욱 늘어나면서, 중동의 태양광발전 시장의 단기적인 확장에 제동이 걸리고 있습니다.

부문별 분석

2025년, 중동의 태양광발전 시장에서 태양광발전 설비 도입이 시장의 96.5%를 차지했습니다. 중동의 태양광발전 시장 규모는 2026년에 30GW를 돌파했으며, 신규 건설의 경제성 측면에서 다른 모든 발전원을 앞질렀습니다. 25% 이상의 TOPCon 방식의 효율과 약 12%에 달하는 양면 수광으로 인한 이점으로 인해, 부지 이용 밀도와 와트당 설비 투자액이 감소하고 있습니다. JinkoSolar의 사우디아라비아 10GW 합작 사업은 이미 ACWA Power사의 Haden 및 Al-Khushaybi 프로젝트에 공급할 물량을 사전 판매했으며, 향후 10년에 걸친 전력 구매 계약을 확보했습니다.

집광형 태양광발전(CSP)은 3.5%라는 틈새 시장 점유율에 그치고 있지만, 2031년까지 연평균 성장률(CAGR) 30.44%로 확대될 것으로 전망됩니다. 두바이의 950 MW 규모 MBR 4단계 프로젝트는 700 MW 규모의 CSP, 250 MW 규모의 태양광발전, 5,907 MWh 규모의 용융염 축열 시스템을 결합한 것으로, 여전히 대표 프로젝트로 자리매김하고 있습니다. CSP의 1kW당 4,500-5,500달러에 달하는 비용 때문에 그 도입은 하이브리드 프로젝트나 현지 헬리오스태트 제조를 의무화하는 사업으로 제한되고 있습니다. 배터리와 결합된 태양광발전은 거의 모든 시나리오에서 CSP의 균등화 발전 비용을 밑돌고 있으며, 중동의 태양광발전 시장에서 향후 설비 용량은 태양광발전 쪽으로 전환될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the middle east solar power market size in terms of installed base is expected to grow from 26.85 gigawatt in 2025 to 31.91 gigawatt in 2026 and is forecast to reach 74.75 gigawatt by 2031 at 18.56% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), End-User (Utility-Scale, Commercial and Industrial, and Residential), and Geography (Saudi Arabia, United Arab Emirates, Oman, Kuwait, Qatar, Bahrain, Jordan, Israel, and Rest of Middle East). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Middle East Solar Power Market Trends and Insights

National Renewable-Energy Targets And Mega-Tenders

Nationwide programs are scaling from pilot auctions to multi-gigawatt blocks, creating a stable offtake pipeline for the Middle East solar power market. Saudi Arabia's Round 6 tender in October 2025 awarded 4.5 GW across eight sites at a record 1.09682 US cents/kWh, underscoring sovereign resolve to treat solar as a baseload asset. The UAE's utility EWEC followed with a 1 GW solar plus 400 MW battery RFP that required firm power delivery, signaling a shift to dispatchable renewables. Oman's Ibri III shortlist and Kuwait's Al Dibdibah tender round out a region-wide queue topping 15 GW. Tender rules now mandate IEC-61215 and IEC-61730 certification, lifting quality standards and reducing warranty risk. Compressed bid-to-financial-close milestones of 15 months are forcing suppliers to hold inventory regionally, shortening historical procurement cycles by almost 40%.

Falling LCOE Of Mono-PERC And TOPCon PV Modules

Rapid diffusion of TOPCon has pushed module conversion efficiencies beyond 25% while narrowing price premiums to under 5% relative to PERC. JinkoSolar's USD 1 billion TOPCon joint venture with Saudi Arabia's Public Investment Fund will deliver 10 GW/year from early 2026, cutting landed costs by up to 12%. A 5 GW plant inaugurated by Desert Technologies in Jeddah in 2024 further broadens local supply. Bifacial TOPCon modules yield an additional 10% to 15% in the desert's high-albedo terrain, pushing the Middle East solar power market toward near-universal PV adoption as localized output scales and tender frameworks grant bid discounts for domestic content, lowering tariffs and deepening the cost gap with gas generation.

Grid Congestion And Intermittency Management Costs

Transmission upgrades lag utility-scale rollouts, forcing developers to fund substations that add as much as 12% to capex. Curtailment in Saudi Arabia's Eastern Province averages 8%-15% at midday, eroding internal rates of return. A 7.8 GWh battery tender awarded to Sungrow in 2024 aims for 10 GW of storage by 2030, yet lithium-iron-phosphate systems cost USD 250-350/kWh and trim IRR by 150-200 bps. The UAE's Northern Emirates mirror the challenge, with EWEC seeking 400 MW/800 MWh of storage capacity. Kuwait's Al Dibdibah timeline doubled to seven years due to the need for a dedicated 400 kV line, adding USD 180 million in grid spend. Reactive-power mandates and synchronous condensers further inflate balance-of-system budgets, tempering short-term expansion in the Middle East solar power market.

Other drivers and restraints analyzed in the detailed report include:

- High Solar Irradiation Exceeding 2,000 kWh/m2/yr

- GCC Cross-Border Grid Trade Initiatives

- High Soiling And Water-Intensive O&M In Desert Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Photovoltaic installations represented 96.5% of the Middle East solar power market in 2025. The Middle East solar power market size for PV surpassed 30 GW in 2026, outpacing every other generation source on new-build economics. TOPCon efficiencies above 25% and bifacial gains around 12% are lowering land-use intensity and capex per watt. JinkoSolar's 10 GW Saudi venture has already pre-sold production to ACWA Power's Haden and Al-Khushaybi projects, locking in offtake through the decade.

Concentrated solar power clings to a 3.5% niche share but is projected to expand at a 30.44% CAGR to 2031. Dubai's 950 MW MBR Phase 4 remains the flagship, combining 700 MW of CSP with 250 MW of PV and 5,907 MWh molten-salt storage. CSP's USD 4,500-5,500/kW price tag confines replication to hybrid projects or mandates for local heliostat manufacturing. Battery-paired PV now beats CSP on levelized cost in almost every scenario, steering future capacity toward photovoltaics inside the Middle East solar power market.

Complete Report Scope:

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

- By Geography

- Saudi Arabia

- United Arab Emirates

- Oman

- Kuwait

- Qatar

- Bahrain

- Jordan

- Israel

- Rest of Middle East

List of Companies Covered in this Report:

- ACWA Power

- Masdar (Abu Dhabi Future Energy Co.)

- JinkoSolar Holding Co. Ltd.

- First Solar Inc.

- Trina Solar Co. Ltd.

- JA Solar Technology Co. Ltd.

- Canadian Solar Inc.

- Longi Green Energy Technology Co. Ltd.

- Sungrow Power Supply Co. Ltd.

- Huawei Digital Power

- Enerwhere Sustainable Energy DMCC

- Hitachi Energy Ltd.

- Array Technologies Inc.

- Nextracker Inc.

- Alsa Solar Systems LLC

- Enviromena Power Systems

- ACWA POWER BARKA SAOG

- Desert Technologies (KSA)

- Yellow Door Energy

- TotalEnergies Renewables Middle East

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National renewable-energy targets & mega-tenders

- 4.2.2 Falling LCOE of mono-PERC & TOPCon PV modules

- 4.2.3 High solar irradiation (above 2,000 kWh/m2/yr)

- 4.2.4 GCC cross-border grid trade initiatives

- 4.2.5 Surge in corporate PPAs from data-center & industrial clusters

- 4.2.6 Utility-scale green-hydrogen developments needing solar feedstock

- 4.3 Market Restraints

- 4.3.1 Grid congestion & intermittency management costs

- 4.3.2 High soiling & water-intensive O&M in desert climates

- 4.3.3 Political-risk premium elevating project finance costs

- 4.3.4 Import-dependency exposure to trade restrictions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Oman

- 5.5.4 Kuwait

- 5.5.5 Qatar

- 5.5.6 Bahrain

- 5.5.7 Jordan

- 5.5.8 Israel

- 5.5.9 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ACWA Power

- 6.4.2 Masdar (Abu Dhabi Future Energy Co.)

- 6.4.3 JinkoSolar Holding Co. Ltd.

- 6.4.4 First Solar Inc.

- 6.4.5 Trina Solar Co. Ltd.

- 6.4.6 JA Solar Technology Co. Ltd.

- 6.4.7 Canadian Solar Inc.

- 6.4.8 Longi Green Energy Technology Co. Ltd.

- 6.4.9 Sungrow Power Supply Co. Ltd.

- 6.4.10 Huawei Digital Power

- 6.4.11 Enerwhere Sustainable Energy DMCC

- 6.4.12 Hitachi Energy Ltd.

- 6.4.13 Array Technologies Inc.

- 6.4.14 Nextracker Inc.

- 6.4.15 Alsa Solar Systems LLC

- 6.4.16 Enviromena Power Systems

- 6.4.17 ACWA POWER BARKA SAOG

- 6.4.18 Desert Technologies (KSA)

- 6.4.19 Yellow Door Energy

- 6.4.20 TotalEnergies Renewables Middle East

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment