|

시장보고서

상품코드

2073562

동남아시아의 수력발전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Southeast Asia Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

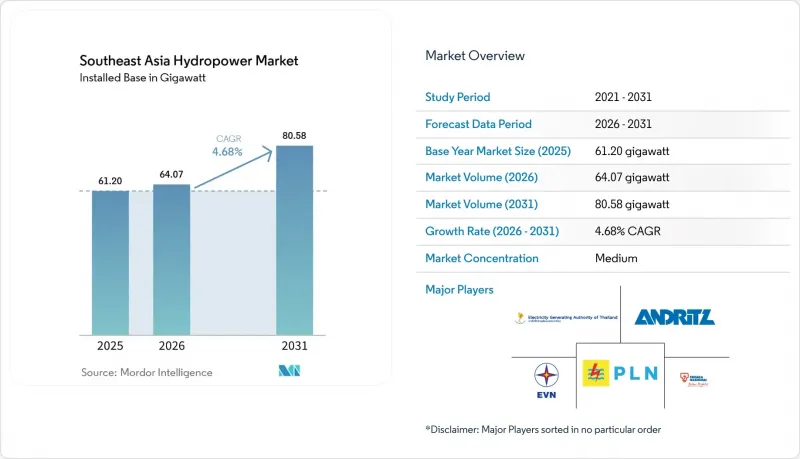

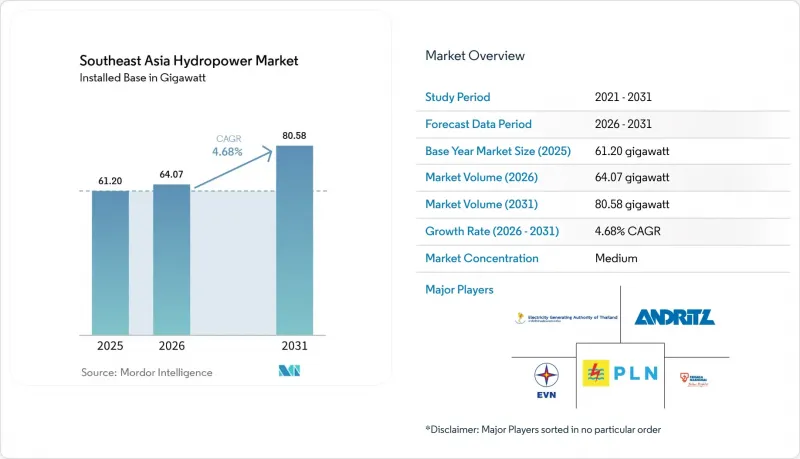

Mordor Intelligence에 의하면, 동남아시아의 수력발전 시장 규모는 2025년 61.20기가와트로 평가되었습니다. 2026년에는 64.07기가와트로 확대되고 2026년부터 2031년에 걸쳐 CAGR 4.68%로 성장을 지속하여, 2031년에는 80.58기가와트에 이를 것으로 예측됩니다.

본 보고서는 용량(대규모 수력, 중규모 수력, 소규모·초소형 수력), 기술(저수지식, 유입식, 양수식, 하천 내식 및 초소형 도관식), 최종 사용자(유틸리티, 독립발전사업자, 산업용 및 자가소비용), 지역(베트남, 라오스, 동티모르 등)별로 분류되어 있습니다. 시장 규모 및 전망은 설비 용량(GW) 단위로 제시되어 있습니다.

동남아시아 수력발전 시장 동향 및 인사이트

변동이 심한 태양광·풍력 발전의 도입에 따라 계통 안정화에 대한 수요가 급증하고 있습니다.

2023년 태국에서 가동을 시작한 배터리 저장 시스템은 2시간의 지속 시간을 제공하지만, 일몰 후 냉방 수요가 증가하는 저녁 시간대의 피크 수요는 여전히 지속되고 있습니다. 람 타 크론의 500 MW 양수 발전 타당성 조사에서는 일몰부터 심야에 이르는 수요 변동을 보완하기 위해 8-12시간의 방전 시간을 목표로 하고 있습니다. 필리핀에서는 5.7 GW 규모의 양수 발전 계획이 진행 중이며, 그 중심이 되는 루손섬 및 민다나오섬의 각 발전소는 계통 연계 우선권을 얻기 위해 에너지부가 정한 조절 가능한 에너지 저장 설비 설치 의무 규정을 충족하고 있습니다. 이와 유사한 전환은 베트남의 제8차 전력 개발 계획에서도 찾아볼 수 있습니다. 이 계획에서는 신규 대규모 수력발전 설비를 제한하는 한편, 16.5GW 규모의 태양광 발전 설비와 균형을 맞추기 위한 일일 주기형 양수 발전 설비에 대한 투자를 유도하고 있습니다. 인도네시아의 PLN은 ‘공정한 에너지 전환 파트너십’에 따라 9.2 GW 규모의 석탄 화력 발전 설비를 폐지하는 한편, 3.7 GW 규모의 양수 발전 설비를 계획하고 있습니다.

저금리 아세안 그린본드로의 자금 유입

2023년, 아세안(ASEAN)의 지속가능 채권 발행 잔액은 727억 달러에 달했으며, 조달 자금의 37%가 재생에너지에 투입되었습니다. ‘아세안 촉매형 그린 파이낸스 기금’예를 들어, 라오스나 필리핀의 유입식 수력발전 클러스터 등, ‘기후 채권 이니셔티브(Climate Bonds Initiative)’ 해당 기준을 충족하는 15개의 수력발전 프로젝트에 총 23억 달러를 지원했습니다. 인도네시아의 국채형 그린 수크크는 2024년에 30억 달러를 조달했으며, 이 자금은 서자바주 및 수마트라섬의 양수 발전 사전 개발에 사용되었습니다. 말레이시아의 SRI 스쿠크는 2027년 완공 예정인 1,285 MW 규모의 발레(Baleh) 댐과 관련해 사라왁 에너지사의 자금 조달 비용을 절감했습니다.

인도네시아 및 말레이시아의 데이터센터를 기반으로 한 민간 PPA

마이크로소프트, 구글, 아마존 웹 서비스(AWS)는 2024년에 총 120억 달러 규모의 데이터센터 투자를 발표했습니다. 광섬유 회선의 구축 현황과 부지 확보가 용이하기 때문에 투자는 자바섬과 조호르주에 집중되고 있습니다. 이러한 하이퍼스케일러 기업들은 연중무휴 24시간 탄소 제로 전력을 필요로 하고 있으며, 이에 따라 인도네시아 전력공사(PLN)는 아사한 연쇄 수력발전소에서 150MW를 할당하고, 1시간 단위로 블록체인을 통해 검증을 수행하는 이 회사 최초의 수력발전을 기반으로 한 기업용 전력구매계약(PPA)을 체결했습니다. 이에 이어 사라왁 에너지는 바쿤과 무룸에서 생산된 300 MW를, 상대적으로 높은 가격으로 책정된 계약에 따라 하이퍼스케일러에 배정했습니다. 아보이티즈 파워(Aboitiz Power)와 CK 파워(CK Power) 등 독립 발전 사업자(IPP)들은 현재 코로케이션 기업 및 가상화폐 채굴업체를 대상으로 20-50 MW 규모의 양수 발전 및 소규모 수력발전 전력구매계약(PPA) 체결을 목표로 하고 있습니다.

부문별 분석

10MW 미만의 소규모 및 초소규모 발전소는 개발업체들이 간소화된 인허가 절차와 사회적 수용성 위험이 낮다는 점을 높이 평가함에 따라 연평균 성장률(CAGR) 5.62%를 기록하며 가장 빠른 성장세를 보였습니다. 필리핀에서는 2024년까지 175 MW 규모의 소규모 수력발전소가 신설되었으며, 추가로 500 MW 규모의 발전소가 계획 중으로, 전력망에서 분리된 섬들의 디젤 발전 대체를 목표로 하고 있습니다. 베트남에는 2,500곳 이상의 소규모 발전소가 있지만, 누적 영향 평가 결과가 나올 때까지 2024년에 신규 허가 발급을 일시 중단했습니다.

2025년에도 100MW를 초과하는 대규모 수력발전은 바쿤(2,400MW)이나 스리나가린(720MW)과 같은 기존 자산을 핵심으로 하여, 동남아시아 수력발전 시장 점유율의 63.90%를 차지했습니다. 현재 신규 발전 용량은 라오스에 집중되어 있으며, 중국이 자금을 지원한 사이야브리(1,285 MW)는 2024년에 본격적으로 가동을 시작했습니다. 10-100 MW 규모의 중규모 수력발전은 중간 단계의 전략으로 자리매김하고 있습니다. PLN은 건설 기간, 발전 설비의 규모, 사회적 수용성 간의 균형을 맞추기 위해 수마트라섬과 칼리만탄섬에서 680 MW 규모의 유사한 프로젝트를 계획하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the southeast asia hydropower market size is expected to grow from 61.20 gigawatt in 2025 to 64.07 gigawatt in 2026 and is forecast to reach 80.58 gigawatt by 2031 at 4.68% CAGR over 2026-2031.

This report is Segmented by Capacity (Large Hydro, Medium Hydro, and Small and Micro Hydro), Technology (Reservoir-Based, Run-Of-River, Pumped-Storage, and In-Stream and Micro-Conduit), End-User (Utilities, Independent Power Producers, and Industrial and Captive), and Geography (Vietnam, Laos, Timor-Leste, and More). The Market Size and Forecasts are Provided in Terms of Installed Capacity (GW).

Southeast Asia Hydropower Market Trends and Insights

Surging Grid-Stabilization Need Amid Variable Solar and Wind Integration

Battery energy-storage systems commissioned in Thailand in 2023 offer a two-hour duration, yet evening peaks persist when air-conditioning demand climbs after sunset. Feasibility studies for 500 MW pumped-storage at Lam Ta Khlong target 8- to 12-hour discharge windows, bridging the sunset-to-midnight ramp. In the Philippines, a 5.7 GW pumped-storage pipeline is anchored by Luzon and Mindanao sites that satisfy a Department of Energy rule mandating dispatchable storage for grid-connection priority. Similar pivots appear in Vietnam's Power Development Plan 8, which caps new large hydro while steering investment toward daily-cycling pumped storage that balances a 16.5 GW solar fleet. Indonesia's PLN plans 3.7 GW of pumped storage as it retires 9.2 GW of coal capacity under the Just Energy Transition Partnership.

Low-Interest ASEAN Green-Bond Inflows

Outstanding ASEAN sustainable bonds climbed to USD 72.7 billion in 2023, with 37% of proceeds earmarked for renewable energy. The ASEAN Catalytic Green Finance Facility committed USD 2.3 billion across 15 hydropower projects that meet Climate Bonds Initiative criteria, including run-of-river clusters in Laos and the Philippines. Indonesia's sovereign green sukuk raised USD 3 billion in 2024, channeling funds to pumped-storage pre-development in West Java and Sumatra. Malaysia's SRI sukuk lowered Sarawak Energy's financing cost for the 1,285 MW Baleh dam scheduled for 2027 completion.

Data-Center-Backed Private PPAs in Indonesia and Malaysia

Microsoft, Google, and Amazon Web Services announced USD 12 billion in data-center investment during 2024, clustering in Java and Johor due to fiber connectivity and land availability. These hyperscalers require 24/7 carbon-free energy, spurring PLN's first hydro-backed corporate PPA that allocates 150 MW from the Asahan cascade with hourly blockchain verification. Sarawak Energy followed by assigning 300 MW from Bakun and Murum to a hyperscaler under a premium-priced contract. IPPs such as Aboitiz Power and CK Power now target 20-50 MW pumped-storage and small-hydro PPAs with colocation firms and cryptocurrency miners.

Other drivers and restraints analyzed in the detailed report include:

- Regional Power Trade Under ASEAN Power Grid Roadmap

- Cheaper Utility-Scale Battery Prices

- Escalating Anti-Dam Social Activism

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small and micro plants below 10 MW posted the fastest growth, expanding at a 5.62% CAGR as developers favored streamlined permitting and lower social-license risk. The Philippines added 175 MW of small hydro by 2024 with another 500 MW in the pipeline, targeting diesel displacement on off-grid islands. Vietnam hosts more than 2,500 small plants, but suspended new licenses in 2024 pending cumulative-impact studies.

Large hydro above 100 MW still held 63.90% of the Southeast Asia hydropower market share in 2025, anchored by legacy assets such as Bakun (2,400 MW) and Srinagarind (720 MW). New capacity now concentrates in Laos, where the Chinese-financed Xayaburi (1,285 MW) reached full operation in 2024. Medium hydro between 10-100 MW fulfills a middle-ground strategy; PLN scheduled 680 MW of such schemes in Sumatra and Kalimantan to balance build-time, unit size, and social acceptance.

Complete Report Scope:

- By Capacity

- Large Hydro (Above 100 MW)

- Medium Hydro (10 to 100 MW)

- Small and Micro Hydro (Below 10 MW)

- By Technology

- Reservoir-Based

- Run-of-River

- Pumped-Storage

- In-Stream and Micro-conduit

- By Component (Qualitative Analysis only)

- Turbines

- Generators

- Control and Automation

- Balance-of-Plant

- By End-User

- Utilities (State & Public)

- Independent Power Producers

- Industrial and Captive

- By Geography

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

- Singapore

- Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste)

List of Companies Covered in this Report:

- Vietnam Electricity (EVN)

- Electricity Generating Authority of Thailand (EGAT)

- PT Perusahaan Listrik Negara (PLN)

- Tenaga Nasional Berhad (TNB)

- Aboitiz Power Corp.

- Power Construction Corp. of China (PowerChina)

- Sinohydro

- Andritz AG

- Voith Hydro

- General Electric Vernova

- Toshiba Energy Systems

- Hitachi Energy

- China Yangtze Power

- China Three Gorges South-East Asia

- Datang Hydropower

- CK Power PLC

- Sarawak Energy Berhad

- Banpu Power

- AC Energy Holdings

- EDC Hydro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging grid-stabilization need amid variable solar & wind integration

- 4.2.2 Low-interest ASEAN green-bond inflows

- 4.2.3 Regional power-trade under ASEAN Power Grid roadmap

- 4.2.4 Data-centre backed private PPAs in Indonesia & Malaysia

- 4.2.5 Water-battery pumped-storage for solar over-generation

- 4.2.6 AI-assisted hydrology forecasting cuts O&M costs

- 4.3 Market Restraints

- 4.3.1 Cheaper utility-scale battery prices

- 4.3.2 Escalating anti-dam social activism

- 4.3.3 Prolonged La Nia/El Nio driven flow volatility

- 4.3.4 Cross-border ESG due-diligence delays Chinese EPC loans

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity

- 5.1.1 Large Hydro (Above 100 MW)

- 5.1.2 Medium Hydro (10 to 100 MW)

- 5.1.3 Small and Micro Hydro (Below 10 MW)

- 5.2 By Technology

- 5.2.1 Reservoir-Based

- 5.2.2 Run-of-River

- 5.2.3 Pumped-Storage

- 5.2.4 In-Stream and Micro-conduit

- 5.3 By Component (Qualitative Analysis only)

- 5.3.1 Turbines

- 5.3.2 Generators

- 5.3.3 Control and Automation

- 5.3.4 Balance-of-Plant

- 5.4 By End-User

- 5.4.1 Utilities (State & Public)

- 5.4.2 Independent Power Producers

- 5.4.3 Industrial and Captive

- 5.5 By Geography

- 5.5.1 Vietnam

- 5.5.2 Indonesia

- 5.5.3 Philippines

- 5.5.4 Thailand

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of Southeast Asia (Brunei, Cambodia, Laos, Myanmar, and Timor-Leste)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Vietnam Electricity (EVN)

- 6.4.2 Electricity Generating Authority of Thailand (EGAT)

- 6.4.3 PT Perusahaan Listrik Negara (PLN)

- 6.4.4 Tenaga Nasional Berhad (TNB)

- 6.4.5 Aboitiz Power Corp.

- 6.4.6 Power Construction Corp. of China (PowerChina)

- 6.4.7 Sinohydro

- 6.4.8 Andritz AG

- 6.4.9 Voith Hydro

- 6.4.10 General Electric Vernova

- 6.4.11 Toshiba Energy Systems

- 6.4.12 Hitachi Energy

- 6.4.13 China Yangtze Power

- 6.4.14 China Three Gorges South-East Asia

- 6.4.15 Datang Hydropower

- 6.4.16 CK Power PLC

- 6.4.17 Sarawak Energy Berhad

- 6.4.18 Banpu Power

- 6.4.19 AC Energy Holdings

- 6.4.20 EDC Hydro

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment