|

시장보고서

상품코드

2073659

미국의 디지털 전환 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

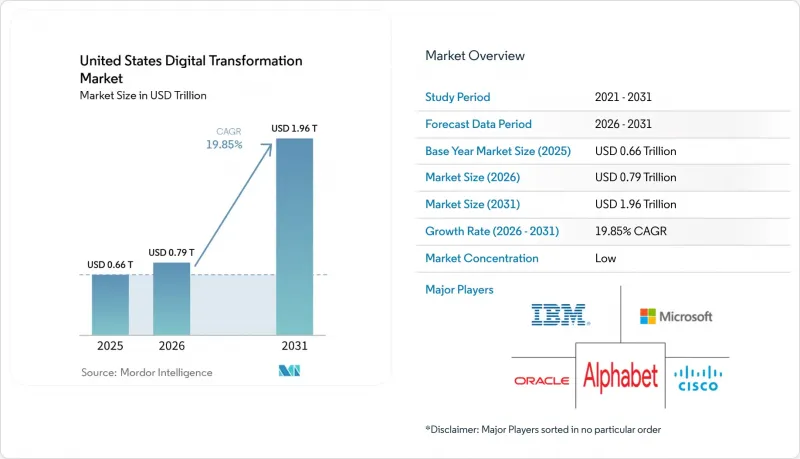

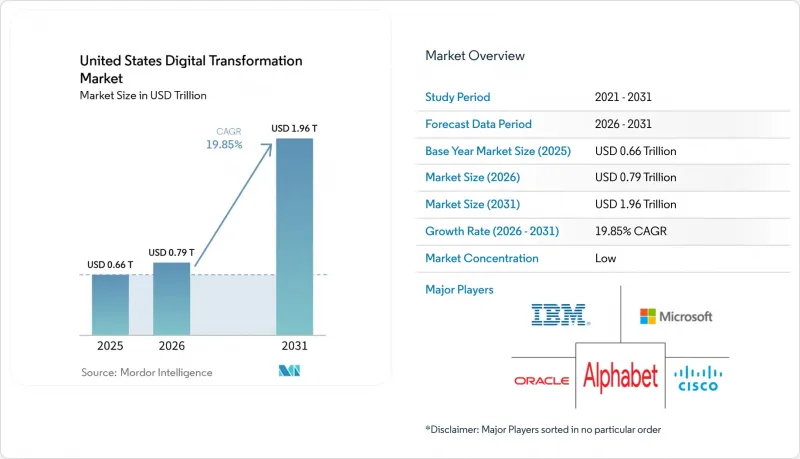

Mordor Intelligence에 의하면, 미국 디지털 전환 시장 규모는 2025년에 6,600억 달러로 평가되었고 2026년 7,900억 달러에서 2031년까지 1조 9,600억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 19.85%를 나타낼 전망입니다.

본 보고서는 구성 요소(솔루션, 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(대기업, 중소기업), 유형(애널리틱스, AI 및 ML, 확장 현실(XR) 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 제조업 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 디지털 전환 시장 동향과 인사이트

연방 정부의 “Cloud-Smart” 및 “FedRAMP 20x”프로그램의 급증

FedRAMP 20x에서는 영향이 적은 워크로드에 대해 정부 기관의 승인이 필요 없어지고 보안 심사가 자동화되므로, 연방 정부의 클라우드 전환이 60% 더 빠르게 완료될 수 있게 됩니다. 2025년 민간 IT 지출 중 740억 달러가 현대화에 배정되며, 이 중 127억 달러가 사이버 보안에 사용될 예정입니다. 법제화된 FedRAMP 승인법에 따라 솔루션을 사전 인증받은 공급업체는 우선 공급업체 지위를 획득하며, 주 및 지방 자치 단체 기관 전반에 걸쳐 확산되는 수요를 주도하게 됩니다.

초개인화된 고객 경험(CX)을 위한 생성형 AI 도입

현재 미국 기업의 78%가 생성형 AI를 도입하고 있으며, 포춘 500대 기업이 OpenAI를 활용한 채팅 및 디자인 도구를 확대함에 따라 ROI는 3.7배에 달하고 있습니다. 2025년 말까지 기업의 25%가 일선 업무를 자동화하는 에이전트 기반 시스템을 도입할 계획입니다. 의료, 금융, 소매 업계를 위한 업종 특화형 대규모 언어 모델은 규정 준수를 유지하면서 서비스 품질을 향상시키고 있습니다.

주별 개인정보 보호 규제의 차이(CPRA 등)

19개 주에서 종합적인 개인정보 보호법을 제정함에 따라, 캘리포니아주, 텍사스주, 버지니아주의 집행팀으로 인해 규정 준수 위험이 높아지고 있습니다. 연방 차원의 통일된 체계가 없기 때문에 여러 주에서 사업을 영위하는 기업의 규정 준수 관련 비용은 30-50% 증가했으며, 중소기업은 상대적으로 높은 비용 부담을 감수해야 하고 있습니다.

부문별 분석

2025년 미국 디지털 전환 시장에서 솔루션이 67.40%라는 압도적인 점유율을 차지했습니다. 이는 클라우드, 사이버 보안, 분석 플랫폼에 대한 기업의 투자가 뒷받침한 결과입니다. 한편, 서비스 분야의 경우 기업들이 통합, AI 모델 튜닝, 관리형 운영을 컨설팅 회사에 위탁하는 경향이 강해짐에 따라 연평균 성장률(CAGR) 20.74%를 나타낼 것으로 전망됩니다. IT 리더의 53%가 지적하는 데이터 사이언스 분야의 기술 격차 확대가 외부 전문 지식에 대한 수요를 부추기고 있습니다.

지속적인 최적화에 대한 수요로 인해, 서비스 포트폴리오는 일회성 도입에서 성과 기반 계약으로 재편되고 있습니다. 각 통신사는 가치 실현까지 걸리는 시간을 단축하는 변경 관리 및 AI 거버넌스에 관한 자문 서비스를 패키지화하고 있습니다. 디지털 성숙도가 높아짐에 따라, 미국 디지털 전환 시장의 서비스 부문 규모는 2031년까지 솔루션 부문과의 매출 격차를 해소할 것으로 예측됩니다.

2025년 기준으로 On-Premise형 플랫폼은 미국 디지털 전환 시장 규모의 50.12%를 차지하고 있으며, 이는 BFSI(은행 및 금융 및 보험) 및 헬스케어 분야의 엄격한 데이터 주권 규제를 반영한 것입니다. 연평균 성장률(CAGR) 20.35%로 성장하고 있는 클라우드 솔루션은 FedRAMP의 간소화와 하이브리드 클라우드 청사진의 혜택을 받고 있습니다. Oracle과 Google의 상호 연동을 통해 기업은 크로스 클라우드 요금을 지불하지 않고도 OCI 데이터베이스와 Google Analytics를 병행하여 운영할 수 있게 됩니다.

하이브리드 아키텍처는 On-Premise 환경에서의 제어 기능과 퍼블릭 클라우드의 탄력적인 컴퓨팅 능력을 결합함으로써, 지연 시간 및 규정 준수 관련 우려를 완화하면서 AI 워크로드를 지원합니다. 2031년까지는 클라우드 보안이 강화되고, 미션 크리티컬 워크로드가 레거시 스택에서 점차 이전됨에 따라 도입 모델 간의 균형이 이루어질 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states digital transformation market size was valued at USD 0.66 trillion in 2025 and estimated to grow from USD 0.79 trillion in 2026 to reach USD 1.96 trillion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise, Hybrid), Enterprise Size (Large Enterprises, Small and Medium Enterprises), Type (Analytics, AI and ML, Extended Reality (XR), and More), End-User Industry (BFSI, Healthcare and Life Sciences, Manufacturing, and More) and by Region. The Market Forecasts are Provided in Terms of Value (USD).

United States Digital Transformation Market Trends and Insights

Surge in Federal Cloud-Smart & FedRAMP Programs

FedRAMP 20x removes agency-sponsorship for low-impact workloads and automates security reviews, enabling federal cloud migrations to finish 60% faster. Civilian IT outlays allocate USD 74 billion for modernization in 2025, with USD 12.7 billion ring-fenced for cybersecurity. Vendors that pre-certify solutions under the codified FedRAMP Authorization Act gain preferred-supplier status, driving spillover demand across state and local agencies.

Generative-AI Adoption for Hyper-Personalized CX

Seventy-eight percent of U.S. firms now embed generative AI, producing a 3.7X ROI as Fortune 500 groups scale OpenAI-powered chat and design tools. By end-2025, 25% of enterprises plan agent-based deployments that automate frontline tasks. Sector-specific large-language models in healthcare, finance, and retail sustain compliance while boosting service quality.

State-Level Privacy Patchwork (CPRA etc.)

Nineteen states have enacted comprehensive privacy statutes, and enforcement teams in California, Texas, and Virginia elevate compliance risk. Compliance spending rises 30-50% for multi-state businesses, with SMEs bearing higher proportional costs in the absence of a single federal framework.

Other drivers and restraints analyzed in the detailed report include:

- CMS-Backed "Digital Front Door" Funding in Healthcare

- IoT & Digital-Twin Uptake from U.S. Reshoring Wave

- Legacy Mainframe Lock-in across Tier-1 Banks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for a dominant 67.40% of the United States digital transformation market share in 2025, underpinned by enterprise investments in cloud, cybersecurity, and analytics platforms. The services arena, however, is forecast to post a 20.74% CAGR as firms turn to consultancies for integration, AI model tuning, and managed operations. A widening data-science skills gap-cited by 53% of IT leaders-reinforces demand for external expertise.

Demand for continuous optimization is reshaping services portfolios from one-time installs to outcome-based contracts. Providers bundle change-management and AI-governance advisories that accelerate time-to-value. As digital maturity grows, the United States digital transformation market size for services is expected to close the revenue gap with solutions by 2031.

On-premise platforms retained 50.12% of the United States digital transformation market size in 2025, reflecting strict data-sovereignty rules in BFSI and healthcare. Cloud solutions, climbing at a 20.35% CAGR, benefit from FedRAMP streamlining and hybrid-cloud blueprints. Oracle-Google interconnects let firms run OCI databases alongside Google Analytics without cross-cloud fees.

Hybrid architectures combine on-premise control with elastic public-cloud compute, mitigating latency and compliance concerns while supporting AI workloads. By 2031, equilibrium between deployment models is plausible as cloud security hardens and mission-critical workloads gradually exit legacy stacks.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Mid-sized Enterprises (SMEs)

- By Type

- Analytics, AI and ML

- Internet of Things (IoT)

- Cyber-security

- Cloud and Edge Computing

- Extended Reality (XR)

- Blockchain

- Industrial Robotics

- Additive Manufacturing / 3-D Printing

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Transportation and Logistics

- Oil, Gas and Utilities

- Telecom and IT Services

- Government and Public Sector

- Others

- By Region

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Microsoft Corporation

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Cisco Systems, Inc.

- Oracle Corp.

- Amazon Web Services, Inc.

- Accenture plc

- Adobe Inc.

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- ServiceNow, Inc.

- Salesforce, Inc.

- Cognizant Technology Solutions

- Capgemini SE

- Infosys Ltd.

- Deloitte Touche Tohmatsu Ltd.

- PwC LLP

- DXC Technology Co.

- Tata Consultancy Services Ltd.

- Schneider Electric SE

- Siemens AG

- NTT DATA Corp.

- Ericsson AB

- KPMG LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Federal Cloud-Smart and FedRAMP Programs

- 4.2.2 Generative-AI Adoption for Hyper-Personalized CX

- 4.2.3 CMS-Backed "Digital Front Door" Funding in Healthcare

- 4.2.4 IoT and Digital-Twin Uptake from U.S. Reshoring Wave

- 4.2.5 ESG Data-Platform Investments Driven by SEC Climate Rules

- 4.2.6 5G SA Roll-outs Unlocking Edge-Computing Use Cases

- 4.3 Market Restraints

- 4.3.1 State-Level Privacy Patchwork (CPRA etc.)

- 4.3.2 Legacy Mainframe Lock-in across Tier-1 Banks

- 4.3.3 Cloud-Security Talent Shortage Inflating TCO

- 4.3.4 Pandemic-Era Technical Debt Hindering Integration

- 4.4 Value / Supply-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Current Market Scenario and Evolution of Practices

- 4.7 Key Metrics

- 4.7.1 Technology Spending Trends

- 4.7.2 Number of IoT Devices

- 4.7.3 Cyber-attack Volume

- 4.7.4 Cloud-Adoption Rate

- 4.7.5 Digital Competitiveness Ranking

- 4.8 Regulatory and Technological Outlook

- 4.9 Key Transformative Technologies

- 4.9.1 Quantum Computing

- 4.9.2 Manufacturing-as-a-Service (MaaS)

- 4.9.3 Cognitive Process Automation

- 4.9.4 Nanotechnology

- 4.10 Porter's Five Forces

- 4.10.1 Competitive Rivalry

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Bargaining Power of Suppliers

- 4.10.4 Threat of New Entrants

- 4.10.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By Type

- 5.4.1 Analytics, AI and ML

- 5.4.2 Internet of Things (IoT)

- 5.4.3 Cyber-security

- 5.4.4 Cloud and Edge Computing

- 5.4.5 Extended Reality (XR)

- 5.4.6 Blockchain

- 5.4.7 Industrial Robotics

- 5.4.8 Additive Manufacturing / 3-D Printing

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Manufacturing

- 5.5.4 Retail and E-commerce

- 5.5.5 Transportation and Logistics

- 5.5.6 Oil, Gas and Utilities

- 5.5.7 Telecom and IT Services

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Google LLC (Alphabet Inc.)

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Oracle Corp.

- 6.4.6 Amazon Web Services, Inc.

- 6.4.7 Accenture plc

- 6.4.8 Adobe Inc.

- 6.4.9 SAP SE

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Hewlett Packard Enterprise Co.

- 6.4.12 ServiceNow, Inc.

- 6.4.13 Salesforce, Inc.

- 6.4.14 Cognizant Technology Solutions

- 6.4.15 Capgemini SE

- 6.4.16 Infosys Ltd.

- 6.4.17 Deloitte Touche Tohmatsu Ltd.

- 6.4.18 PwC LLP

- 6.4.19 DXC Technology Co.

- 6.4.20 Tata Consultancy Services Ltd.

- 6.4.21 Schneider Electric SE

- 6.4.22 Siemens AG

- 6.4.23 NTT DATA Corp.

- 6.4.24 Ericsson AB

- 6.4.25 KPMG LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment