|

시장보고서

상품코드

1686633

의약품 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

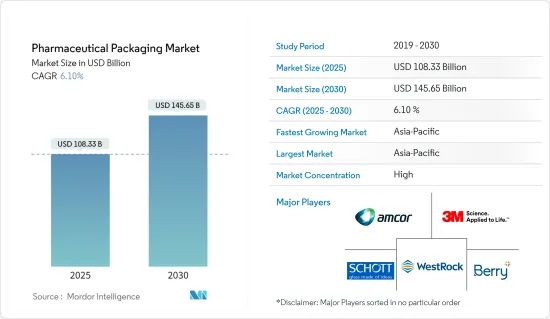

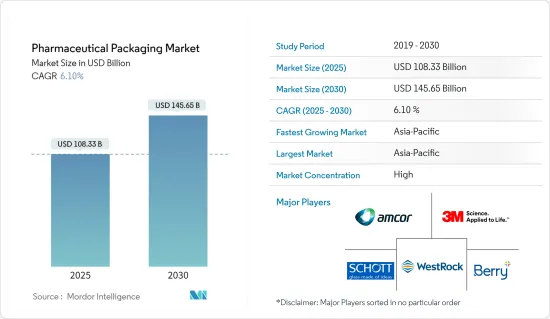

의약품 포장 시장 규모는 2025년에 1,083억 3,000만 달러, 2030년에는 1,456억 5,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 6.1%를 나타낼 것으로 예상됩니다.

규제 상황이 포장 혁신을 형성 :

의약품 포장 시장은 엄격한 규제 기준과 위조품 대책으로 큰 성장을 이루고 있습니다. 세계 각국의 정부는 제품의 안전성을 확보하고 위조 의약품과 싸우기 위해 엄격한 규제를 실시했습니다. 유럽 연합(EU) 지침은 모든 의약품에 일련 번호를 부여해야 하며 미국, 중국, 인도, 터키에도 유사한 규제가 존재합니다. 이러한 조치가 고급 포장 솔루션의 채택을 뒷받침하고 있습니다.

주요 하이라이트

- FDA 지침 : FDA는 OTC 제품의 소아용 포장 및 탬퍼 방지 포장에 대한 지침을 제정합니다.

- 인증 기술 : 제약 회사는 홀로그램 및 숨겨진 배치 번호와 같은 인증 기술에 투자하고 있습니다.

- 직렬화 방법 : 직렬화 방법에는 선형 바코드, 2차원 바코드, 무선 자동 식별(RFID) 등이 있습니다.

- 스마트 포장 : RFID 및 NFC 태그를 사용한 스마트 포장은 제품 추적 및 환자 참여를 위해 널리 사용되고 있습니다.

나노기술이 포장 솔루션에 혁명을 일으킵니다.

나노기술이 의약품 포장에 미치는 영향은 혁신적인 차세대 솔루션으로 업계를 변화시키고 있습니다. 이러한 진보는 위조품 대책뿐만 아니라 공급망 전반에 걸쳐 제품의 안전성과 추적성을 강화합니다.

주요 하이라이트

- 추적 능력 : 나노기술은 제조에서 최종 사용자까지 제품을 추적할 수 있는 스마트 포장의 창출을 가능하게 합니다.

- 스마트 포장 개발 : Schott AG와 같은 기업은 명확한 컨테이너 기반 추적성을 제공하는 스마트 패키징 캡슐화 솔루션을 개발하고 있습니다.

- 제품 출시 : ENTOD Pharmaceuticals는 나노기술을 이용한 안과용 미용 제품 시리즈를 인도에서 출시하여 나노포장의 다용도성을 나타냈습니다.

- 생물의학에 적용 : 나노입자는 질병의 검출, 예방, 약물 전달을 위해 생물의학에서 이용됩니다.

시장 동향과 성장 촉진요인:

의약품 포장 시장은 몇 가지 주요 촉진요인에 의해 강력한 성장을 이루고 있습니다. 신흥국의 의약품산업 확대와 헬스케어 지출 증가가 시장 성장을 가속하고 있습니다.

주요 하이라이트

- 플라스틱 부문 : 플라스틱 부문은 2028년까지 544억 5,000만 달러, CAGR 6.17%로 성장할 것으로 예상됩니다.

- 병 부문 : 병 분야는 2022년에 182억 4,000만 달러로 평가되었고, 2028년에는 273억 달러에 이를 것으로 예측됩니다.

- FDI 성장 : 인도와 같은 신흥국은 현저한 성장을 이루고 있으며, 2020-2021년에는 의약품 업계에 대한 FDI가 200% 증가합니다.

- 아시아태평양 성장 : 아시아태평양은 2023년부터 2028년까지 연평균 복합 성장률(CAGR) 6.99%를 나타낼 전망이며 2028년에는 545억 9,000만 달러에 이를 것으로 예상됩니다.

경쟁 구도와 주요 기업:

의약품 포장 시장은 세분화되고 있으며, 여러 선도 기업들이 업계를 지배하고 있습니다. 이러한 기업들은 시장 포지션을 유지하기 위해 기술 혁신, 지속가능성, 전략적 확대에 주력하고 있습니다.

주요 하이라이트

- Amcor PLC : 1860년 설립. 경구 투여 형식과 의료기기 패키지 등 다양한 패키징 솔루션을 제공합니다.

- Shot AG : 1853년에 설립되었으며 의약품 튜브 및 약물 캡슐화 솔루션을 전문으로 합니다.

- Berry Global Group : 1967년 설립. 의료용 포장, 병, 바이알을 제공합니다.

- 게레스하이머 AG : 게레스하이머 AG는 바이알 생산 능력을 강화하기 위해 미국 생산 시설에 9,400만 달러를 투자할 것이라고 발표했습니다.

지속가능성과 미래 동향 :

의약품 포장 업계에서는 지속가능성과 친환경 솔루션에 대한 관심이 높아지고 있습니다. 이 추세는 규제 압력과 환경 친화적인 포장을 요구하는 소비자의 요구에 의해 발생합니다.

주요 하이라이트

- GSK 이니셔티브 글락소 스미스크라인 소비자 헬스케어는 Pulpex 종이 병 파트너 컨소시엄에 참여하여 재활용 가능한 종이 병을 모색하고 있습니다.

- 바이오플라스틱에 대한 투자 : 기업은 기존의 플라스틱을 대체하는 바이오플라스틱 및 기타 생분해성 소재에 투자하고 있습니다.

- 첨단 인쇄 기술 : Essentra Packaging의 Landa S10 나노 그래픽 인쇄기와 같은 고급 인쇄 기술은 패키징 능력을 향상시킵니다.

- 3차원 시각화 : 3D 시각화 및 인쇄 전략의 채택은 1차 및 2차 포장 설계의 한계를 넓혀가고 있습니다.

의약품 포장 시장 동향

플라스틱 부문이 소재 카테고리를 지배

플라스틱 부문은 의약품 포장 시장에서 가장 큰 재료 카테고리로 부상하고 있습니다. 2022년, 이 부문은 시장 점유율의 41.84%를 차지해 380억 3,000만 달러에 달했습니다. 이 부문은 예측 기간 동안 CAGR 6.17%를 나타낼 전망이며, 2028년까지 541억 5,000만 달러에 달할 것으로 예측됩니다. 이러한 성장은 이 부문의 범용성, 비용 효율성, 플라스틱 포장 솔루션의 지속적인 기술 혁신 등 여러 요인에 의해 야기됩니다.

- 시장 점유율 2022년 의약품 포장 시장의 41.84%를 플라스틱이 차지했습니다.

- 비용 효과 : 플라스틱은 합리적인 가격이므로 의약품 포장의 인기 상품입니다.

- 혁신적인 솔루션 : 기업은 지속가능성 기준을 충족하기 위해 생분해성 및 재활용 가능한 플라스틱 솔루션을 도입하고 있습니다.

- 향후 성장 : 이 분야는 2028년까지 541억 5,000만 달러에 달할 것으로 예측됩니다.

- 규제 기준이 플라스틱 포장의 혁신을 촉진합니다. 기업은 이러한 요구 사항을 충족하기 위해 혁신적인 솔루션을 개발하고 있습니다. 예를 들어, Bormioli Pharma는 2022년 5월 재생 플라스틱, 바이오, 생분해성, 퇴비화 가능한 플라스틱 솔루션 등 지속 가능한 패키징 제품의 라벨인 EcoPositive를 출시했습니다. 이 이니셔티브는 규제 압력과 지속 가능한 포장 옵션에 대한 수요 증가에 대한 업계 대응을 보여줍니다.

- Ecopositive Initiative Bormio Repharma의 EcoPositive는 바이오 및 퇴비화 가능한 플라스틱을 포함한 지속 가능한 패키징 옵션을 소개합니다.

- 위조 방지 : 플라스틱 포장의 위조 방지 대책은 세계 표준에 대응하기 때문에 점점 고도화되고 있습니다.

- 규제 압력 : 세계 규제 기준 증가는 의약품 플라스틱 포장 부문을 형성합니다.

- 지속가능성에 대한 노력 : 생분해성 플라스틱 솔루션에 대한 투자 증가는 환경 규제와 일치합니다.

- 나노기술의 플라스틱 포장 개발에 미치는 영향 : 나노기술의 영향은 플라스틱 부문에서 차세대 패키징 솔루션의 개발을 촉진하고 있습니다. 이 기술적 진보로 장벽 기능과 항균 기능 향상 등 특성이 강화된 패키징 재료의 창출이 가능해지고 있습니다. 플라스틱 의약품 포장에서 나노기술의 통합은 향후 수년간 같은 부문의 성장과 시장 우위에 크게 기여할 것으로 예상됩니다.

- 장벽 기능 : 나노기술은 플라스틱 의약품 포장에서 강화된 장벽 특성을 창출할 수 있습니다.

- 항균 솔루션 : 기업은 포장의 안전과 수명을 향상시키기 위해 항균 나노 기술을 통합합니다.

- 특성 강화 : 나노기술 혁신은 플라스틱 포장을 보다 똑똑하고 효율적으로 만드는 데 사용됩니다.

- 미래 전망 : 나노기술의 통합은 플라스틱 포장 분야의 성장을 가속합니다.

아시아태평양이 큰 점유율을 차지

아시아태평양은 의약품 포장 시장에서 가장 급성장하는 부문으로 두드러집니다. 2022년 이 지역 시장 점유율은 40.12%로 시장 규모는 366억 달러였습니다. 이 시장은 2028년까지 545억 9,000만 달러에 달할 것으로 예측되며, 예측 기간 중 CAGR은 6.99%를 나타낼 것으로 예상됩니다. 이 성장률은 다른 지역을 능가하고 있으며, 아시아태평양은 세계 의약품 포장 시장의 중요한 견인 역할을 하고 있습니다.

- 시장 점유율 : 아시아태평양은 세계 의약품 포장 시장의 40.12%를 차지합니다.

- 성장률 : 이 지역은 2023년부터 2028년에 걸쳐 CAGR 6.99%로 성장할 것으로 예상됩니다.

- 지역 이점: 중국과 인도는 아시아태평양의 의약품 포장 시장을 선도하고 있습니다.

- 새로운 동향 : 이 지역의 급성장은 혁신적이고 지속 가능한 패키징에 대한 수요 증가가 원동력이 되고 있습니다.

의약품 포장 산업 개요

세계 기업이 통합 시장을 독점

의약품 포장 시장은 다양한 제품 포트폴리오를 가진 세계 기업이 지배적인 것이 특징입니다. Amcor PLC, Schott AG, Berry Global Group Inc.와 같은 기업이 시장을 선도하고 병과 바이알에서 블리스터 팩 및 주사기에 이르기까지 광범위한 패키징 솔루션을 제공합니다. 시장 구조는 상당히 통합된 것으로 보이며, 이러한 대기업은 광범위한 제품 라인, 세계의 존재, 기술력으로 인해 큰 시장 점유율을 유지하고 있습니다.

Amcor PLC: 의약품 포장의 세계 리더로 블리스터 팩부터 소아용 병까지 다양한 솔루션을 제공합니다.

샷 AG: 유리 기반 패키징 및 의약품 튜브를 전문으로 하여 봉쇄 솔루션의 혁신을 추진.

베리 세계 그룹 병에서 프리필러블 주사기까지 다양한 플라스틱 패키징 솔루션을 제공합니다.

연결 시장 : 시장은 기술적인 전문 지식과 제품 다양성을 가진 대기업에 의해 지배됩니다.

혁신과 지속가능성이 시장의 리더십을 견인 :

시장을 선도하는 기업은 혁신과 지속가능성에 중점을 둡니다. 예를 들어 Amcor PLC는 22년도에 종이 기반 AmFiber 제품군과 의료용 PVC 프리 AmSky 블리스터 시스템을 발표했습니다. 베리세계그룹은 내소아용으로 변조 방지 시럽과 액체 의약품 포장을 위한 완벽한 번들 솔루션을 출시했습니다. 이 회사들은 또한 지속 가능한 패키징 솔루션에 많은 투자를 하고 있으며, Amcor는 2030년까지 포트폴리오 전반에 걸쳐 30% 재활용 재료를 목표로 하고 있습니다. 시장에서의 리더십은 인도 방갈로르에 있는 베리 세계의 새로운 제조 시설과 같은 전략적 확장을 통해 더욱 견고해지고, 첨단 건강 관리 솔루션에 대한 지역적, 세계적 접근을 강화하고 있습니다.

지속가능성의 중요성 : 기업은 지속가능성 목표를 달성하기 위해 재활용 가능하고 친환경적인 소재를 선호합니다.

혁신적인 솔루션 : PVC 프리 블리스터 팩과 소아용 병은 보다 안전하고 지속 가능한 대안으로 인기를 끌고 있습니다.

전략적 확대 : 신흥 시장에 새로운 시설을 마련함으로써 세계 기업은 지역 수요를 받아 시장 점유율을 확대할 수 있습니다.

R&D 투자 : 주요 기업은 R&D에 투자하고 의약품 포장의 지속 가능한 혁신을 추진하고 있습니다.

시장의 미래 성공 요인 :

시장 기업이 성공을 거두고 시장 점유율을 확대하기 위해서는 몇 가지 중요한 요인이 떠오릅니다. 첫째, Amcor의 혁신적인 제품 도입으로 대표되는 것처럼 R&D 투자는 중요합니다. 둘째, 인도의 베리 세계 신시설처럼 신흥 시장에서의 생산능력 확대는 수요를 끌어들이는데 필수적입니다. 셋째, Klockner Pentaplast가 재활용 가능한 PET 블리스터 필름을 도입하는 등 지속가능성에 대한 주목이 점점 중요해지고 있습니다. 마지막으로 Aptar Pharma가 Metaphase Design Group을 인수하는 것과 같은 전략적 인수와 제휴는 제품 제공과 서비스 능력을 강화할 수 있습니다. 이러한 전략은 향후 몇 년동안 자사의 지위를 강화하거나 시장을 혼란시키려는 기업에게 매우 중요합니다.

R&D 투자 : 급속히 진화하는 업계에서 경쟁력을 유지하기 위해서는 기업이 혁신을 계속해야 합니다.

신흥 시장 : 아시아태평양과 같은 고성장 지역으로의 진출은 미래 시장 성공에 필수적입니다.

지속가능성 : 기업은 재활용 가능한 소재와 생분해성 소재를 우선적으로 사용하여 환경 문제를 해결해야 합니다.

전략적 인수: 인수 및 파트너십은 의약품 포장의 제품 라인업을 확대하고 혁신을 가속화하는 데 도움이 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 포장에 관한 규제 기준과 위조품에 대한 엄격한 규범

- 혁신적인 차세대 포장 솔루션에 의한 나노기술의 영향

- 규제 상황이 포장 혁신을 형성한다

- 시장의 과제

- 공급기업의 협상력에 의한 원재료 비용의 변동

제6장 시장 세분화

- 재료별

- 플라스틱

- 유리

- 기타 재료

- 제품 유형별

- 병

- 주사기

- 바이알 앰풀

- 튜브

- 캡과 마개

- 라벨

- 기타 제품 유형

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Amcor PLC

- 3M Company

- Schott AG

- WestRock Company

- Berry Global Group Inc.

- McKesson Corporation

- AptarGroup Inc.

- Klockner Pentaplast Group

- CCL Industries Inc.

- FlexiTuff International Ltd

- Gerresheimer AG

- West Pharmaceutical Services Inc.

- Becton, Dickinson and Company

- Vetter Pharma International GmbH

- Catalent Inc.

- WL Gore & Associates Inc.

- Nipro Corporation

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

SHW 25.04.01The Pharmaceutical Packaging Market size is estimated at USD 108.33 billion in 2025, and is expected to reach USD 145.65 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

Regulatory Landscape Shapes Packaging Innovation:

The pharmaceutical packaging market is experiencing significant growth driven by stringent regulatory standards and anti-counterfeit measures. Governments worldwide are implementing strict regulations to ensure product safety and combat counterfeit drugs. The European Union's Directive mandates serialization numbers on all pharmaceutical products, while similar regulations exist in the United States, China, India, and Turkey. These measures are propelling the adoption of advanced packaging solutions.

Key Highlights

- FDA Guidelines: The FDA has established guidelines for child-resistant packaging and tamper-resistant packaging for OTC products.

- Authentication Technologies: Pharmaceutical companies are investing in authentication technologies like holograms and hidden batch numbers.

- Serialization Methods: Serialization methods include linear barcodes, two-dimensional barcodes, and radio frequency identification (RFID).

- Smart Packaging: Smart packaging with RFID and NFC tags is gaining traction for product tracking and patient engagement.

Nanotechnology Revolutionizes Packaging Solutions:

The impact of nanotechnology on pharmaceutical packaging is transforming the industry with innovative and new-generation solutions. These advancements not only combat counterfeiting but also enhance product safety and traceability throughout the supply chain.

Key Highlights

- Tracking Capability: Nanotechnology enables the creation of smart packaging that can track products from manufacturing to end-user.

- Smart Packaging Development: Companies like Schott AG are developing smart packaging containment solutions for clear container-based traceability.

- Product Launches: ENTOD Pharmaceuticals launched a nanotechnology-based ocular aesthetic range in India, showcasing the versatility of nano-packaging.

- Biomedicine Applications: Nanoparticles are being utilized in biomedicine for disease detection, prevention, and drug delivery.

Market Drivers and Growth Trends:

The pharmaceutical packaging market is witnessing robust growth, fueled by several key drivers. The expansion of the pharmaceutical industry in emerging economies, coupled with increasing healthcare spending, is propelling market growth.

Key Highlights

- Plastics Segment: The plastics segment is expected to reach USD 54.45 billion by 2028, growing at a CAGR of 6.17%.

- Bottles Segment: The bottles segment was valued at USD 18.24 billion in 2022 and is projected to reach USD 27.30 billion by 2028.

- FDI Growth: Emerging economies like India are experiencing significant growth, with a 200% increase in FDI in the pharmaceutical industry in 2020-2021.

- Asia-Pacific Growth: The Asia-Pacific region is expected to grow at a CAGR of 6.99% from 2023 to 2028, reaching USD 54.59 billion by 2028.

Competitive Landscape and Key Players:

The pharmaceutical packaging market is fragmented, with several major players dominating the industry. These companies are focusing on innovation, sustainability, and strategic expansions to maintain their market positions.

Key Highlights

- Amcor PLC: Established in 1860, Amcor offers a wide range of packaging solutions, including oral dose formats and medical device packaging.

- Schott AG: Founded in 1853, Schott specializes in pharmaceutical tubing and drug containment solutions.

- Berry Global Group: Established in 1967, Berry Global provides medical packaging, bottles, and vials.

- Gerresheimer AG: Gerresheimer AG announced a USD 94 million investment in a US production facility to increase its vial production capacity.

Sustainability and Future Trends:

The pharmaceutical packaging industry is increasingly focusing on sustainability and eco-friendly solutions. This trend is driven by both regulatory pressures and consumer demand for more environmentally responsible packaging.

Key Highlights

- GSK's Initiative: GlaxoSmithKline Consumer Healthcare joined the Pulpex paper bottle partner consortium to explore recyclable paper bottles.

- Bioplastics Investment: Companies are investing in bioplastics and other biodegradable materials as alternatives to traditional plastics.

- Advanced Printing Technologies: Advanced printing technologies, such as Essentra Packaging's Landa S10 Nanographic Printing Machine, are enhancing packaging capabilities.

- 3-D Visualization: The adoption of 3-D visualization and printing strategies is pushing the boundaries of both primary and secondary packaging design.

Pharmaceutical Packaging Market Trends

Plastics Segment Dominates Material Category

The Plastics segment emerges as the largest material category in the Pharmaceutical Packaging Market. In 2022, this segment accounted for 41.84% of the market share, valued at USD 38.03 billion. The segment is projected to reach USD 54.15 billion by 2028, growing at a CAGR of 6.17% during the forecast period. This growth is driven by several factors, including the segment's versatility, cost-effectiveness, and ongoing innovations in plastic packaging solutions.

- Market Share: Plastics accounted for 41.84% of the pharmaceutical packaging market in 2022.

- Cost-Effectiveness: The affordability of plastics makes it a popular choice in pharmaceutical packaging.

- Innovative Solutions: Companies are introducing biodegradable and recyclable plastic solutions to meet sustainability standards.

- Future Growth: The segment is projected to reach USD 54.15 billion by 2028.

- Regulatory Standards Drive Plastic Packaging Innovation: Stringent regulatory standards and norms against counterfeit products are propelling advancements in plastic pharmaceutical packaging. Companies are developing innovative solutions to meet these requirements. For instance, Bormioli Pharma launched EcoPositive in May 2022, a label for sustainable packaging offerings, including recycled plastics, bio-based, biodegradable, and compostable plastic solutions. This initiative demonstrates the industry's response to regulatory pressures and the growing demand for sustainable packaging options.

- EcoPositive Initiative: Bormioli Pharma's EcoPositive showcases sustainable packaging options, including bio-based and compostable plastics.

- Counterfeit Prevention: Anti-counterfeit measures in plastic packaging are becoming increasingly sophisticated to meet global standards.

- Regulatory Pressure: The rise of global regulatory standards is shaping the pharmaceutical plastic packaging segment.

- Sustainability Efforts: Increased investment in biodegradable plastic solutions aligns with environmental regulations.

- Nanotechnology Impacts Plastic Packaging Development: The impact of nanotechnology is driving the development of new-generation packaging solutions in the plastics segment. This technological advancement is enabling the creation of packaging materials with enhanced properties, such as improved barrier functions and antimicrobial capabilities. The integration of nanotechnology in plastic pharmaceutical packaging is expected to contribute significantly to the segment's growth and market dominance in the coming years.

- Barrier Functions: Nanotechnology enables the creation of enhanced barrier properties in plastic pharmaceutical packaging.

- Antimicrobial Solutions: Companies are integrating antimicrobial nanotechnology to improve the safety and longevity of packaging.

- Enhanced Properties: Nanotech innovations are being used to make plastic packaging smarter and more efficient.

- Future Prospects: The integration of nanotechnology is set to propel growth in the plastic packaging sector.

Asia-Pacific to Occupy Major Share

The Asia-Pacific region stands out as the fastest-growing segment in the Pharmaceutical Packaging Market. In 2022, this region held a 40.12% market share, valued at USD 36.60 billion. The market is projected to reach USD 54.59 billion by 2028, exhibiting a robust CAGR of 6.99% during the forecast period. This growth rate outpaces other regions, positioning Asia-Pacific as a key driver of the global pharmaceutical packaging market.

- Market Share: Asia-Pacific holds 40.12% of the global pharmaceutical packaging market.

- Growth Rate: The region is expected to grow at a CAGR of 6.99% from 2023 to 2028.

- Regional Dominance: China and India lead the pharmaceutical packaging market in Asia-Pacific.

- Emerging Trends: The region's rapid growth is driven by increasing demand for innovative and sustainable packaging.

Pharmaceutical Packaging Industry Overview

Global Players Dominate Consolidated Market:

The pharmaceutical packaging market is characterized by the dominance of global players with diverse product portfolios. Companies like Amcor PLC, Schott AG, and Berry Global Group Inc. lead the market, offering a wide range of packaging solutions from bottles and vials to blister packs and syringes. The market structure appears fairly consolidated, with these major players holding significant market share due to their extensive product lines, global presence, and technological capabilities.

Amcor PLC: A global leader in pharmaceutical packaging, with solutions ranging from blister packs to child-resistant bottles.

Schott AG: Specializes in glass-based packaging and pharmaceutical tubing, driving innovation in containment solutions.

Berry Global Group Inc.: Offers extensive plastic packaging solutions, from bottles to prefillable syringes, and is expanding in emerging markets.

Consolidated Market: The market is dominated by large companies with significant technological expertise and product diversity.

Innovation and Sustainability Drive Market Leadership:

Market leaders are distinguished by their focus on innovation and sustainability. Amcor PLC, for instance, introduced the AmFiber family of paper-based products and the PVC-free AmSky blister system for healthcare applications in FY22. Berry Global Group launched a complete bundle solution for child-resistant and tamper-evident syrup and liquid medicine packaging. These companies are also investing heavily in sustainable packaging solutions, with Amcor targeting 30% recycled material across its portfolio by 2030. Their market leadership is further solidified by strategic expansions, such as Berry Global's new manufacturing facility in Bangalore, India, enhancing regional and global access to advanced healthcare solutions.

Sustainability Focus: Companies are prioritizing recyclable and eco-friendly materials to meet sustainability goals.

Innovative Solutions: PVC-free blister packs and child-resistant bottles are gaining traction as safer, sustainable alternatives.

Strategic Expansions: New facilities in emerging markets enable global players to tap into regional demand and grow market share.

R&D Investment: Leading companies invest in R&D to drive sustainable innovation in pharmaceutical packaging.

Factors for Future Success in the Market:

For market players to succeed and grow their market share, several key factors emerge. Firstly, investment in research and development is crucial, as exemplified by Amcor's introduction of innovative products. Secondly, expanding manufacturing capabilities in emerging markets, like Berry Global's new facility in India, is essential for tapping into growing demand. Thirdly, a focus on sustainability is becoming increasingly important, with companies like Klockner Pentaplast introducing recyclable PET blister films. Lastly, strategic acquisitions and partnerships, such as Aptar Pharma's acquisition of Metaphase Design Group, can enhance product offerings and service capabilities. These strategies will be critical for companies looking to strengthen their position or disrupt the market in the coming years.

R&D Investment: Companies must continue to innovate to stay competitive in a rapidly evolving industry.

Emerging Markets: Expansion in high-growth regions like Asia-Pacific is crucial for future market success.

Sustainability Mandate: Companies must address environmental concerns by prioritizing recyclable and biodegradable materials.

Strategic Acquisitions: Acquisitions and partnerships will help expand product offerings and accelerate innovation in pharmaceutical packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Assessment of Impact of the COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Regulatory Standards on Packaging and Stringent Norms Against Counterfeit Products

- 5.1.2 Impact of Nanotechnology due to Innovative and New- generation Packaging Solutions

- 5.1.3 Regulatory Landscape Shapes Packaging Innovation

- 5.2 Market Challenges

- 5.2.1 Fluctuations in Raw Material Cost Due to Suppliers Bargaining Power

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastics

- 6.1.2 Glass

- 6.1.3 Other Materials

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Syringes

- 6.2.3 Vials and Ampoules

- 6.2.4 Tubes

- 6.2.5 Caps and Closures

- 6.2.6 Labels

- 6.2.7 Other Product Types

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 3M Company

- 7.1.3 Schott AG

- 7.1.4 WestRock Company

- 7.1.5 Berry Global Group Inc.

- 7.1.6 McKesson Corporation

- 7.1.7 AptarGroup Inc.

- 7.1.8 Klockner Pentaplast Group

- 7.1.9 CCL Industries Inc.

- 7.1.10 FlexiTuff International Ltd

- 7.1.11 Gerresheimer AG

- 7.1.12 West Pharmaceutical Services Inc.

- 7.1.13 Becton, Dickinson and Company

- 7.1.14 Vetter Pharma International GmbH

- 7.1.15 Catalent Inc.

- 7.1.16 W. L. Gore & Associates Inc.

- 7.1.17 Nipro Corporation