|

시장보고서

상품코드

1686299

무선 센서 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Wireless Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

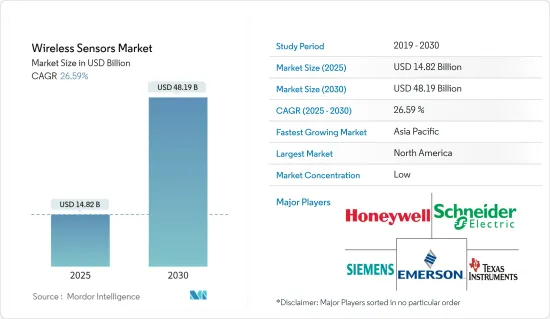

무선 센서 시장 규모는 2025년에 148억 2,000만 달러, 2030년에는 481억 9,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 26.59%를 나타낼 전망입니다.

무선 센서는 RFID와 블루투스와 같은 다양한 혁신적인 기술의 도움으로 정확성과 신뢰성과 같은 몇 가지 장점을 제공하여 전자 장비의 통합을 용이하게 할 수 있습니다.이 센서들은 주로 생산 흐름을 모니터링하기 위한 공장 환경에서 사용됩니다. 또, 자동차, 방위, 빌딩 오토메이션, 기타 자재관리이나 식음료등의 산업에도 응용되고 있습니다.신에너지원의 탐구 증가, 정부 규제, 재생 가능 에너지 개척, 급속한 기술 진보에 의해 무선 센서 시장은 추진하고 있습니다.

주요 하이라이트

- 무선 센서는 스마트 그리드에서 송전선 및 변압기의 원격 감시에 필수적인 구성 요소로 여겨지고 있습니다.

- 안전성을 높이기 위한 센서의 사용 증가에 대한 정부 규제 증가로 무선 센서 수요가 증가하고 있습니다. 예를 들어, 석유 시추 시설과 보일러와 같은 엄격한 환경 조건을 가진 지역에서는 고압, 고온 등이 존재합니다. 무선 센서를 사용하면 안전한 거리에서 시설을 제어 및 감시하는 것이 용이해집니다.

- 기계가 보다 밝고 직관적인 인더스트리 4.0 혁명은 무선 센서의 산업 용도에 대한 필요성을 높이고 있습니다. 새로운 장치는 보다 효율적이고, 안전하며, 유연하게 설계되었으며, 성능, 사용 및 고장을 자율적으로 모니터링하는 기능을 갖추고 있습니다. 따라서 이러한 용도는 고감도 센서 수요에 박차를 가하고 있습니다.

- IoT의 채택이 증가하고 있는 것도 시장 성장을 가속하는 큰 요인입니다. 이러한 IoT 접속 기기 증가는 무선 센서 수요를 촉진할 것으로 예측되고 있습니다. 또한 스마트 홈, 스마트 빌딩, 스마트 시티, 지능형 공장 개발에는 소형 폼 팩터, 고정밀, 저전력 및 주변 파라미터를 제어하는 능력으로 무선 센서가 필요합니다.

- 이러한 센서는 설치 비용을 절감하고 작업자 및 내부에 미치는 영향을 최소화할 수 있으므로 무선 센서 시스템을 설치하려면 배선 및 건물 구조를 변경할 필요가 없습니다. 많은 기업들이 비용 효율적이고 안전하고 편리한 무선 기술에 투자하고 있습니다.

- 예를 들어 Monnit Corporation은 최근 AgriTech 시장 수요를 충족시키는 ALTA Soil Moisture Sensor의 발매를 발표했습니다.이 혁신적인 토양 수분 센서는 농가, 상업 재배자, 온실 관리자가 정밀 관개 작업을 물건의 인터넷(IoT)에 간단하게 접속할 수 있도록 지원합니다.방위 분야는 무선 센서 기술을 채용하고 있습니다.

- 그러나 고성능으로 비용 효율이 뛰어나 신뢰성이 높은 센서 수요가 높아져 시장 벤더에 의한 연구 개발 활동에 대한 지출이 증가하고 있습니다.

무선 센서 시장 동향

에너지 및 전력이 큰 시장 점유율을 차지

- 기업의 전력 소비와 관련 비용을 줄이고 생태 발자국을 포함한 환경에 미치는 영향을 최소화하기 위해 에너지 절약은 점점 더 중요 해지고 있습니다. 네르기 시스템, 디젤 트럭의 배기 가스 검사 장치, 새로운 건물의 설계 공역학에 관한 풍력 공학, 고도 기상 조사 풍선, 해양 조사, 수질 오염 장치, 대기 조사, 굴뚝 수은 샘플링 등으로 정확한 무선 센서 측정이 필요합니다.

- 제로 파워 무선 센서는 트랜스듀서의 출력 전력을 모니터링하고 에너지를 축적하고 무선 센서의 나머지 부분에 전력을 공급하기 위해 에너지 처리 저전력 관리 회로를 필요로 합니다. 케이션에 있어서의 무선 센서 네트워크의 전력 공급에 도움이 됩니다.

- 전기자동차나 자율주행차와 같은 미래적인 기술 혁신으로 이러한 무선압력 센서 수요는 자동차 분야에서 증가할 것으로 예상됩니다.

- 에너지 수확을 기반으로 한 자율 무선 센서 노드는 편리하고 비용 효율적인 솔루션입니다. 공급에 필요한 특성을 가지고 있습니다. 제로 무선 센서가 하드 와이어 솔루션에 비해 전개되는 경우 경제적으로 큰 이점이 실현됩니다.

현저한 성장을 이루는 아시아태평양

- 아시아태평양은 전기 및 전자 기기 제조 시장에서 가장 규모가 큰 지역 중 하나입니다.이 지역은 특히 중국과 일본에서 무선 센서 기술의 중요한 공급업체이기도합니다. 생산 거점이기도 하고, 큰 성장의 가능성을 숨기고 있습니다.중국 기차 공업 협회(CAAM)에 의하면, 최근, 중국에서는 약 31만 7,000대의 상용차가 판매되었습니다.

- 이 산업은 무선 센서 시장의 상당 부분을 차지하고 있기 때문에 이 지역은 예측 기간 동안 기회를 제공합니다.

- 자동차에서 유압 브레이크는 승객의 안전에 매우 중요한 요소입니다. 브레이크를 사용하여 차량을 제어하는 능력은 압력 센서를 포함한 구성 요소의 복잡한 조합에 의한 것입니다.

- 무선 센서의 채용이 증가하고 있는 또 다른 이유는 성장하는 IT 헬스 케어 시장을 강화해, 새로운 헬스 케어 기기나 디바이스를 혁신하기 위해서, 이 지역에서 무선 센서의 도입이 활발하게 행해지고 있는 것입니다.

- 최근 Yokogawa Electric Corporation는 OpreX 브랜드의 무선 솔루션인 Sushi Sensor를 일본에서 발매한다고 발표했습니다.

무선 센서 산업 개요

무선 압력 센서 시장은 경쟁이 심합니다. R&D, 파트너십, 제휴 및 인수에 높은 비용을 들이는 것은 지역 기업이 치열한 경쟁을 유지하기 위해 채택하는 주요 성장 전략입니다. 이 시장의 주요 기업은 하니웰 인터내셔널, 슈나이더 일렉트릭, 에머슨 일렉트릭, 텍사스 기기, 지멘스, ABB, 로크웰 오토메이션, 파스코 사이언티픽 등입니다.

- 2022년 10월 - 지멘스는 Volta Trucks와 제휴하여 상용차의 전동화를 가속. 전기자동차의 액체 냉각 시스템에서 압력은 매우 중요한 매개 변수입니다. 압력 센서는 냉각 시스템의 조정 및 최적화를 위한 피드백과 누출을 암시하는 압력 손실을 감지하는 데 필수적입니다.

- 2022년 6월 - 무선 압력 센서는 분쇄, 산성 세척 및 시멘팅 용도에서도 유사한 압력 모니터링 및 제어 목적으로 사용됩니다. 무선 압력 센서는 배관 내의 기체와 액체의 게이지 압력을 측정하는 기능을 가지고 있습니다. ABB는 도시 가스 분배 회사 Think Gas와 제휴하여 Think Gas의 전체 가스 네트워크 운영을 자동화했습니다. 무선 압력 센서는 배관에 직접 설치를 지원하므로 생산 현장에서 쉽게 설치할 수 있으며, 습식 재료는 부식에 매우 강합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19가 무선 센서 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 무선 기술 채용 증가(특히 가혹한 환경에서)

- 스마트 팩토리 구상의 등장(산업 오토메이션)

- 시장의 과제

- 센서 제품과 관련된 높은 보안 요구와 비용

- IoT 분야에서의 사이버 보안에 대한 우려와 최근의 동향

제6장 시장 세분화

- 유형별

- 압력 센서

- 온도 센서

- 화학 및 가스 센서

- 위치 및 근접 센서

- 기타 센서

- 최종 사용자 산업별

- 자동차

- 헬스케어

- 항공우주 및 방위

- 에너지 및 전력

- 식음료

- 기타 최종 사용자 산업

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

제7장 경쟁 구도

- 기업 프로파일

- Honeywell International Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Texas Instruments Incorporated

- Siemens AG

- ABB Ltd.

- Rockwell Automation, Inc.

- Pasco Scientific

- Monnit Corporation

- Phoenix Sensors LLC

제8장 투자 분석

제9장 시장의 미래

SHW 25.04.29The Wireless Sensors Market size is estimated at USD 14.82 billion in 2025, and is expected to reach USD 48.19 billion by 2030, at a CAGR of 26.59% during the forecast period (2025-2030).

Wireless sensors offer several advantages, such as accuracy and reliability, with the help of various innovative technologies, such as RFID and Bluetooth, and the potential to make electronic devices easy to integrate. As a result, they gained significant traction in the past few years. These sensors are primarily used in factory settings for data monitoring production flow. These also find applications in Automotive, defense, building automation, and other industries, like materials handling and food and beverage. Due to the increasing quest for new energy sources, government regulations, renewable energy development, and rapid technological advancements, the wireless sensors market is propelling.

Key Highlights

- Wireless sensors are considered a vital component in smart grids for remote monitoring of power lines and transformers. They are present in service to monitor line temperature and weather conditions. Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT - connected devices, are among the significant factors driving the wireless sensors market.

- Due to the increased government regulation for the increased use of the sensor for safety, the demand for wireless sensors is growing. For instance, the areas with challenging environmental conditions, such as Oil rigs, Boilers, etc., present high pressure, high temperature, etc. Wireless sensors make it easy to control and monitor the facility from a safe distance.

- The industry 4.0 revolution, in which machines are becoming brighter and more intuitive, is increasing the need for wireless sensors' industrial applications. The new devices are designed to be more efficient, safe, and flexible, with the ability to monitor their performance, usage, and failure autonomously. These applications, therefore, spur the demand for highly- sensitive sensors.

- The rising adoption of IoT is another major factor driving the market's growth. This growth in IoT-connected devices is projected to fuel the demand for wireless sensors. Further, transforming the development of smart homes and buildings, smart cities, and intelligent factories demands wireless sensors, owing to the small form factor, high precision, low power consumption, and ability to control ambient parameters.

- These sensors have reduced installation costs and minimal disruption to the workforce and interiors; therefore, installing wireless sensor systems requires no wiring or structural building changes. Many companies are investing in wireless technologies, which are cost-effective, safe as well as convenient.

- For instance, Monnit Corporation recently announced its ALTA Soil Moisture Sensor's availability to meet the AgriTech market's demands. The innovative Soil Moisture Sensor assists farmers, commercial growers, and greenhouse managers in easily connecting their precision irrigation operations to the Internet of Things (IoT). The defense sector is embracing wireless sensor technology, as these sensors can monitor their premises, identify suspicious activity, and track valuable assets.

- However, the demand for high-performance, cost-efficient, and reliable sensors has increased, leading to higher spending in R&D activities by market vendors. These technological advancements in nanotechnology and micro-technology are expected to propel the market growth of wireless sensors over the forecast period.

Wireless Sensors Market Trends

Energy and Power to Hold Significant Market Share

- Energy conservation is increasingly essential to reduce any enterprise's power consumption and associated costs and minimize the environmental impact, including a business's ecological footprint. For improved energy conservation, accurate wireless sensor measurements are required in portable and stationary weather stations, wind energy systems, testing devices for diesel truck emissions, wind engineering concerning new building design aerodynamics, high-altitude weather research balloons, ocean research, water pollution devices, atmospheric studies, and smokestack mercury sampling.

- Zero-power wireless sensors require energy processing low power management circuitry to monitor the transducer output power, store energy, and deliver power to the rest of the wireless sensor. Energy harvesting helps in powering wireless sensor networks in industrial apps. Advancements in low-power and reliable wireless communications and sensor and energy harvesting technologies make this type of communication more practical and efficient than a wired infrastructure.

- With futuristic innovations, like electric cars and self-driving cars, the demand for these wireless pressure sensors is assumed to increase in the automotive sector. Powertrain applications represent more than 50% of the business, followed by safety, with tire pressure management systems (TPMS) being the most significant single automotive application. Driven by carbon dioxide emission reduction and automation, wireless pressure sensors will increasingly be adopted and used in the future.

- Energy harvesting-based autonomous wireless sensor nodes are a convenient and cost-effective solution. Using energy harvesting removes one of the critical factors limiting the proliferation of wireless nodes. The scarcity of power sources has the characteristics necessary to deliver the energy and power to the sensor node for years without battery replacement. Significant economic advantages are realized when zero wireless power sensors are deployed vs. hard-wired solutions. According to BP, primary energy consumption in India recently amounted to some 35.4 exajoules, thus driving the demand for wireless sensors in the energy and power industry.

Asia Pacific to Witness Significant Growth

- The Asia Pacific is one of the largest regions in the electrical and electronics manufacturing market. The region is also a significant vendor of wireless sensor technologies, especially in China and Japan. China is also the world's largest car market and the world's largest production site for cars, including electric cars, with much growth potential. According to the China Association of Automobile Manufacturers (CAAM), recently, approximately 317,000 commercial vehicles were sold in China. Sales in China accounted for about 32.56% of global motor vehicle sales.

- As these industries account for a significant portion of the wireless sensor market, the region offers an opportunity over the forecast period. The growing concept of connected cars and regulations regarding automotive safety is also expected to drive the adoption of wireless sensors in the region.

- In automobiles, hydraulic brakes are a crucial component in passenger safety. The ability to control a vehicle using brakes is down to a complex blend of components, including pressure sensors. According to Auto Punditz, In the financial year 2022, the leading type of electric vehicle sold in India was two-wheelers, reaching around 231 thousand units, thus driving the demand for wireless pressure sensors in the automotive industry.

- Another reason for increasing the adoption of wireless sensors is the region's high activity level in deploying them to enhance its growing IT healthcare market and innovate new healthcare equipment and devices.

- Recently, Yokogawa Electric Corporation announced the release of the Sushi Sensor, an OpreX brand wireless solution, in Japan. The sensor is a compact wireless device with integrated sensing and communication functions that are intended to monitor plant equipment vibration and surface temperature.

Wireless Sensors Industry Overview

The Wireless Pressure Sensors Market is highly competitive. The high expense on research and development, partnerships, collaborations, and acquisitions are the prime growth strategies adopted by the regional companies to sustain the intense competition. Key players in the market are Honeywell International Inc., Schneider Electric SE, Emerson Electric Co., Texas Instruments Incorporated, Siemens AG, ABB Ltd., Rockwell Automation Inc, Pasco Scientific, and many more.

- October 2022 - Siemens partnered with Volta Trucks to accelerate commercial fleet electrification. Pressure is a crucial parameter in an electric vehicle's liquid cooling system. Pressure sensors are vital for feedback for cooling system regulation and optimization and to detect pressure loss that could suggest a leak.

- June 2022 - Wireless pressure sensors are also used during fracturing, acidizing, and cementing applications for similar pressure monitoring and control purposes. The wireless pressure sensor has the function of measuring the gauge pressure of gases and liquids in piping. ABB Partnered with Think Gas, a city gas distribution company, to automate operations across Think Gas' gas network. The wireless pressure sensors help easy installation for a production site to support direct installation into piping, and wetted material is highly resistant to corrosion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Wireless Sensors Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Wireless Technologies (Especially in Harsh Environments)

- 5.1.2 Emergence of Smart Factory Concepts (Industrial Automation)

- 5.2 Market Challenges

- 5.2.1 Higher Security Needs and Cost associated with the Sensor Products

- 5.2.2 Concerns pertaining to cybersecurity in the IoT space and recent developments

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pressure Sensors

- 6.1.2 Temperature Sensors

- 6.1.3 Chemical and Gas Sensors

- 6.1.4 Position and Proximity Sensors

- 6.1.5 Other Types of Sensors

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Aerospace and Defense

- 6.2.4 Energy and Power

- 6.2.5 Food and Beverage

- 6.2.6 Other End-user Industries

- 6.3 ***By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 Schneider Electric SE

- 7.1.3 Emerson Electric Co.

- 7.1.4 Texas Instruments Incorporated

- 7.1.5 Siemens AG

- 7.1.6 ABB Ltd.

- 7.1.7 Rockwell Automation, Inc.

- 7.1.8 Pasco Scientific

- 7.1.9 Monnit Corporation

- 7.1.10 Phoenix Sensors LLC