|

시장보고서

상품코드

1640464

유전 통신 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Oilfield Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

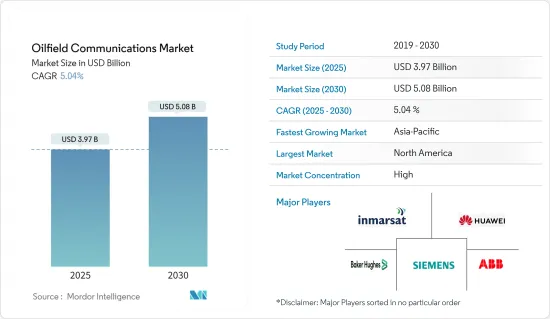

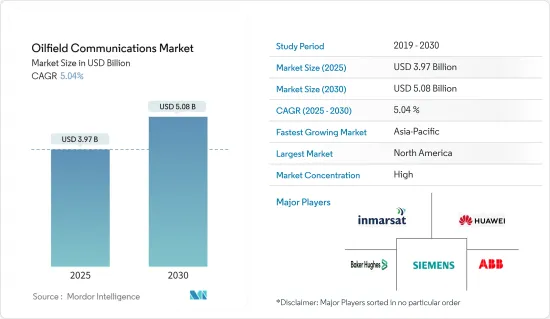

유전 통신 시장 규모는 2025년에 39억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.04%로, 2030년에는 50억 8,000만 달러에 이를 것으로 예측됩니다.

유전 통신 시장은 머신러닝, 인공지능, 인지 인텔리전스, 클라우드 등의 첨단 기술이 급격히 확대되고 널리 받아들여지고 있으며, 안정적인 통신에 의존하는 유전의 미션 크리티컬한 활동에는 신뢰성 높은 하드웨어가 필요하기 때문에 네트워크 인프라를 개선하기 위한 투자가 증가하고 있습니다.

주요 하이라이트

- GCC와 같은 일부 국가는 통신 인프라 업그레이드에 많은 투자를 하고 있습니다. 기업은 인지 기술 및 인공지능(AI) 기술과 자동화를 융합함으로써 비즈니스 프로세스 능력을 급속히 확대하고 있습니다. 인프라는 직원의 복리 후생, 자원 관리, 네트워크 연결성, 안전 및 위생 규정을 개선하는 데 도움이 됩니다.

- 이러한 장점은 디지털 전환 목표를 달성하기 위한 노력으로 이어져 네트워크 통신에 대한 투자를 증가시켰으며, 이는 유전 통신 제품 수요를 끌어올려 산업의 확대를 예견하고 있습니다.

- 또한 석유 및 가스산업에서는 클라우드 기반의 최신 기술 채용이 증가하고 있어 시장의 성장을 뒷받침하고 있습니다. 이러한 서비스는 더 나은 실시간 데이터, 인프라 비용 유연성, 데이터 관리 및 스토리지 확장성을 제공합니다. 생산 유닛, 유정, 유전의 유지 보수 및 모니터링은 컴퓨팅 서비스와 같은 클라우드 기반 기술로 가능해진 매력적인 옵션입니다. 기업은 자산을 디지털화하고 데이터 처리를 분산하며 운영을 위한 SaaS 솔루션을 구축하기 위해 엣지 서비스와 클라우드 서비스에 의존하고 변화하고 있습니다. 최첨단 획기적인 기술을 통해 클라우드 솔루션은 참신하고 다양한 유전 옵션을 변화시키고 구축할 수 있습니다.

- 에너지 부문은 클라우드 플랫폼이 제공하는 높은 컴퓨팅 능력으로 클라우드 기반 서비스 기능을 대량으로 활용하고 있으며, 물리적 자산의 지능적인 관리 등 다른 기술의 채용도 촉진하여 업무 효율성 향상을 촉진하고 있습니다. 따라서 석유 및 가스산업에서는 클라우드 기반의 최신 기술의 채용이 진행되고 있어 유전 통신의 요구가 높아질 것으로 예상됩니다.

- 석유는 제한된 자원이며 유통 기한도 짧습니다. 또한 유전 통신의 수급 변화와 지정학적 사건으로 인해 석유가격은 수년에 걸쳐 변동하고 있습니다. 지구과학자들은 항상 새로운 석유 공급원을 발견하고 미발견의 매장량을 조사하기 위해 노력하고 있습니다. 한편, 연구자들은 비전통적인 에너지원에도 눈을 돌리고 있습니다. 코로나바이러스가 발생한 시점에서 유전통신 수요와 시장의 미래 동향은 하락세에 접어들었으며 이대로 수년간 지속될 경우 시장은 쇠락할 우려가 있습니다.

유전 통신 시장 동향

클라우드 기반 서비스 채용이 시장 성장을 견인

- 클라우드 기반 서비스의 채택이 진행됨에 따라 석유 회사는 유전 통신을 이용할 수밖에 없습니다. 이렇게 하면 오프쇼어 사이트와 인쇼어 사이트가 생산 통계에 포함되어 더 나은 공급사슬 관리에 도움이 됩니다. 석유 회사의 경우 재료의 원활한 흐름은 매우 중요합니다. 수익성은 회전율에 크게 좌우되므로 다운타임은 피해야 합니다.

- 예를 들어, 석유 및 가스 회사에 서비스를 제공하는 GE 석유 및 가스는 지난 2년 반 동안 350개 애플리케이션을 Amazon 클라우드 서비스인 AWS로 마이그레이션했습니다. GE는 클라우드 애플리케이션에서 엔터프라이즈 애플리케이션을 운영함으로써 총 소유 비용을 평균 52% 절감할 수 있음을 발견했습니다. 이는 이 부문에서 가장 진보된 기업의 지배적인 동향입니다.

- Siemens AG에 따르면 데이터 솔루션은 효율성 향상과 비용 절감 측면에서 큰 이점을 제공한다고 합니다. Siemens에 따르면 디지털화를 통해 배럴당 브렌트 가격 비용을 45% 절감할 수 있는 반면 업스트림 자본 비용 지수를 25%, 조업 비용 지수를 18% 절감할 수 있다고 합니다.

- 클라우드 기술은 이전에는 채용을 억제하고 있던 보안 우려에 효과적으로 대처하였고 그 결과, 시대에 뒤쳐진 온프레미스 시스템에 혁명을 일으키는 투명성을 갖춘 선구 기업이 보상받게 되었습니다.

북미가 주요 점유율을 차지

- 북미는 이 시장의 선구자이자 최대의 석유 및 가스 산출국이기 때문에 큰 점유율을 차지할 것으로 예상됩니다. 북미에서는 온쇼어와 오프쇼어 유전 조업을 위해 선진적인 디지털 통신 솔루션을 요구하는 기업이 많습니다.

- 많은 산유 기업들이 미국에 본사를 두고 있습니다. 대부분의 기업들은 세계 시장에 진입하기 전에 미국에서 새로운 서비스를 테스트하고 있습니다.

- 미국의 신기술 도입 속도와 세계 통신에 대한 관심 증가가 시장을 밀어 올립니다.

- 또한 새롭게 발견된 셰일 자원과 OCS가 승인한 대륙외 리스 프로그램에 의한 탐사 생산 활동의 급속한 증가로 이 지역은 예측 기간 동안 유전 통신이 가장 급성장하는 시장 중 하나가 될 것으로 예상됩니다.

유전 통신 산업 개요

유전 통신 시장에는 토탈 솔루션을 제공하는 여러 기업이 있습니다. 주요 진출기업으로는 Siemens AG, ABB Ltd, Huawei Technologies, Baker Hughes(General Electric Company), Inmarsat PLC, Speedcast International Limited 등이 있습니다. M&A는 시장의 주요 성장 전략 중 하나이며 이 산업의 경쟁을 변화시키고 신제품 개발 기회를 늘릴 것으로 예상됩니다.

2022년 7월 Baker Hughes는 인공 리프트 솔루션의 최첨단 기술 공급업체 중 하나인 AccessESP를 인수한다고 발표했습니다. AccessESP의 "GoRigless ESP System"은 리그를 사용하거나 와이어 라인, 코일 튜빙, 유정 시추기와 같은 갱정 생산관을 통한 펌핑 대신 일반 경량 도구를 사용하여 전기 수중 펌프(ESP)의 설치 및 해체를 가능하게 하는 자체 솔루션을 제공합니다. 오프쇼어 및 원격지 상황에서 점점 더 중요해지고 있는 ESP 교체 작업의 중요성은 비용과 다운타임 측면에서 이러한 솔루션에 의해 크게 줄어듭니다.

2022년 5월, 미국을 기반으로 하는 유전 통신 업체 Baker Hughes는 리그 가동 횟수를 줄임으로써 유정의 총 설치 비용을 줄이기 위해 MS-2 애널러스 씰이라고 불리는 새로운 해저 유정 기술을 발표했습니다. 2022년 휴스턴에서 개최된 해외 기술 회의에서는 북미와 남미의 여러 고객이 이 통합 실링 시스템을 발표, 전시 및 채택했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 산업 가치사슬 분석

제5장 시장 역학

- 촉진요인

- 클라우드 기반 서비스 채용 확대

- 지리적 과제에 의해 유전의 회복과 생산성 향상을 위한 디지털 통신에의 의존도가 높아진다

- 효과적인 통신 기술 개발과 채용

- 억제요인

- 엄격한 규제 프레임 워크와 데이터 자산 보안 위험 증가

제6장 시장 세분화

- 솔루션별

- M2M 통신

- 통합 통신(UC) 솔루션

- 화상회의

- VoIP

- 유선/무선 인컴

- 기타 솔루션

- 통신 네트워크별

- 셀룰러 통신 네트워크

- VSAT 통신 네트워크

- 광섬유 통신 네트워크

- 마이크로파 통신 네트워크

- 테트라 네트워크

- 사이트별

- 온쇼어 통신

- 오프쇼어 통신

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 기타 아시아태평양

- 라틴아메리카

- 멕시코

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Huawei Technologies Co. Ltd.

- Siemens AG

- Speedcast International Limited

- ABB Ltd.

- Commscope, Inc.

- Inmarsat PLC(Triton Bidco)

- Tait Communications

- Baker Hughes(General Electric Company)

- Alcatel-Lucent France, SA

- Ceragon Networks Ltd.

- Rad Data Communications, Inc.

- Rignet, Inc.

- Hughes Network Systems LLC

- Airspan Networks, Inc.

- Commtel Networks Pvt. Ltd.

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

CSM 25.02.13The Oilfield Communications Market size is estimated at USD 3.97 billion in 2025, and is expected to reach USD 5.08 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030).

The oilfield communication market is being driven by the exponential expansion and widespread acceptance of cutting-edge technologies like machine learning, artificial intelligence, cognitive intelligence, and cloud, owing to the rising investment in improving network infrastructure as dependable hardware is needed for mission-critical activities in the oilfields, which depend on consistent communication.

Key Highlights

- Several nations, like the GCC, have significantly invested in upgrading their telecommunications infrastructure. Companies are quickly expanding the capabilities of business processes by fusing automation with cognitive and artificial intelligence (AI) technology. The infrastructure helps to improve staff welfare, resource management, network connectivity, and health and safety regulations.

- These advantages are driving up investments in network communication to support their ambitious digital transformation ambitions, which is driving up demand for oilfield communications products and has foreseen the industry's expansion.

- Additionally, the rising adoption of contemporary cloud-based technologies in the oil and gas industry propels market growth. These services provide better real-time data, more flexibility in infrastructure costs, and the capacity to scale data management and storage. Maintenance and monitoring of production units, wells, and oilfields are now appealing options made possible by cloud-based technologies, such as computing services. Businesses are transforming and relying on edge and cloud services to digitalize their assets, decentralize data processing, and deploy SaaS solutions for operations. With cutting-edge breakthrough technology, cloud solutions can transform and open up a wealth of novel and exciting oilfield options.

- A significant amount of cloud-based service capabilities are being used in the energy sector due to the high computing power made available by cloud platforms, which also encourages the adoption of other technologies like the intelligent management of physical assets and promotes greater operational efficiency. Therefore, the oil and gas industry's growing embrace of contemporary cloud-based technology is anticipated to drive the need for oilfield communications.

- Oil is a limited resource that has a little shelf life. Oil prices have also fluctuated throughout the years because of shifting supply and demand for oilfield communication and geopolitical events. Geoscientists are constantly working to find new oil sources and investigate undiscovered reserves. On the other hand, researchers are looking at non-traditional energy sources nonstop. At the coronavirus outbreak, the demand for oilfield communications and market future trends were waning. It will be disastrous for the market if the situation worsens for several years.

Oilfield Communications Market Trends

Growing Adoption of Cloud-based Services to Drive the Market Growth

- With the growing adoption of cloud-based services, oil companies are compelled to use oil field communication. This keeps their offshore sites connected with the inshore site about production stats, which helps in better supply chain management. The smooth flow of materials is very important for oil companies as their profitability is highly dependent upon the turnover, and downtime needs to be avoided.

- For instance, over the past two and a half years, GE Oil & Gas, the service provider to oil and gas companies, has shifted 350 of its applications to Amazon's cloud offering, AWS. GE found that the total cost of ownership of running its enterprise applications on the cloud systems provided a saving of 52% on average. This is the dominant trend in the sector's most progressive companies.

- According to Siemens AG, data-based solutions will lead to huge gains in terms of efficiency gains and cost savings. According to Siemens, digitization can reduce Brent price cost per barrel by 45% while reducing the upstream capital cost index and operations cost index by 25% and 18%, respectively.

- Cloud technology has effectively addressed security concerns that previously restrained its adoption, thereby rewarding pioneering companies with the transparency to revolutionize their outdated on-premise systems.

North America to Account for a Major Share

- North America is the pioneer in this market and is expected to hold a significant share as it is the largest oil and gas producer, with companies seeking advanced digital communication solutions for their onshore and offshore field operations.

- Many oil-producing companies are headquartered in the United States. Most companies pilot new services in the country before global launches and deployment.

- This country's fast adoption of new technology and the growing focus on global communication push the market forward.

- Moreover, with newfound shale resources and rapidly increasing exploration and production activities due to the Outer Continental Shelf Leasing Program approved by OCS, the region is expected to be one of the fastest-growing markets for oilfield communications over the forecast period.

Oilfield Communications Industry Overview

The oilfield communications market has a few major players who provide the entire spectrum of solutions. The major players include Siemens AG, ABB Ltd, Huawei Technologies Co. Ltd, Baker Hughes (General Electric Company), Inmarsat PLC, and Speedcast International Limited. Merger and Acquisition are expected to be one of the key growth strategies of the market, which will change the dynamics of competition in this industry and increase opportunities for new product development.

In July 2022, Baker Hughes announced it would acquire AccessESP, one of the top cutting-edge technology suppliers for artificial lift solutions. Oil and gas operations might be modernized by cutting operational expenses and downtime and becoming considerably more productive.AccessESP's "GoRigless ESP System" offers its unique solutions that enable the installation and dismantling of an electrical submersible pump (ESP) using common, light-duty intervention tools instead of a rig or pulling well production tubings, such as a wireline, coiled tubing, or well tractors. The importance of ESP replacement workovers, which are becoming increasingly crucial in offshore and remote situations, is considerably reduced by these solutions in terms of cost and downtime.

In May 2022, to reduce total wellhead installation costs due to fewer rig visits, Baker Hughes, a US-based oilfield communications business, introduced a novel subsea wellhead technology called the MS-2 Annulus Seal. At the offshore technology conference in Houston in 2022, several clients in North and South America presented, displayed, and adopted this integrated sealing system.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Cloud-based Services

- 5.1.2 Geographically Challenging Locations will Increase Reliance on Digital Communication for Oilfield Recovery and Productivity

- 5.1.3 Development and Adoption of Effective Communication Technologies

- 5.2 Market Restraints

- 5.2.1 Stringent Regulatory Framework and the Rising Risk of Inadequate Data and Asset security

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 M2M Communication

- 6.1.2 Unified Communication Solutions

- 6.1.3 Video Conferencing

- 6.1.4 VoIP

- 6.1.5 Wired/Wireless Intercom

- 6.1.6 Other Solutions

- 6.2 By Communication Network

- 6.2.1 Cellular Communication Network

- 6.2.2 VSAT Communication Network

- 6.2.3 Fiber Optic-Based Communication Network

- 6.2.4 Microwave Communication Network

- 6.2.5 Tetra Network

- 6.3 By Field Site

- 6.3.1 Onshore Communications

- 6.3.2 Offshore Communications

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Mexico

- 6.4.4.2 Brazil

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 Rest of Middle-East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Huawei Technologies Co. Ltd.

- 7.1.2 Siemens AG

- 7.1.3 Speedcast International Limited

- 7.1.4 ABB Ltd.

- 7.1.5 Commscope, Inc.

- 7.1.6 Inmarsat PLC (Triton Bidco)

- 7.1.7 Tait Communications

- 7.1.8 Baker Hughes (General Electric Company)

- 7.1.9 Alcatel-Lucent France, S.A.

- 7.1.10 Ceragon Networks Ltd.

- 7.1.11 Rad Data Communications, Inc.

- 7.1.12 Rignet, Inc.

- 7.1.13 Hughes Network Systems LLC

- 7.1.14 Airspan Networks, Inc.

- 7.1.15 Commtel Networks Pvt. Ltd.