|

시장보고서

상품코드

1849871

보안 및 취약성 관리 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Security And Vulnerability Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

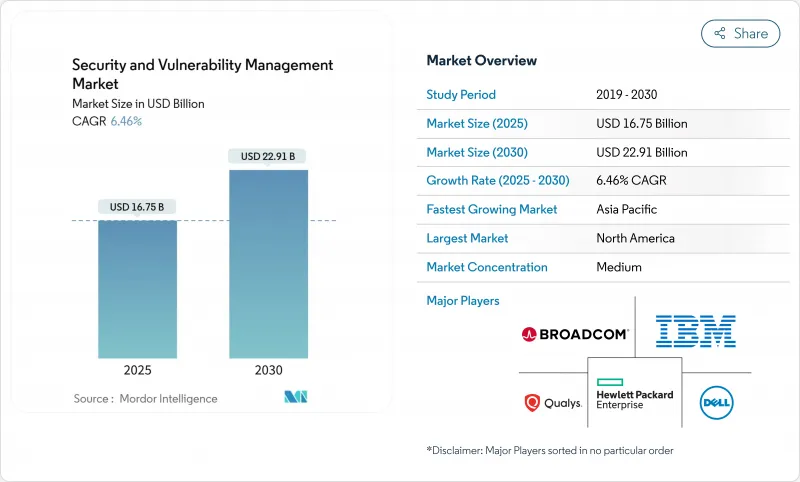

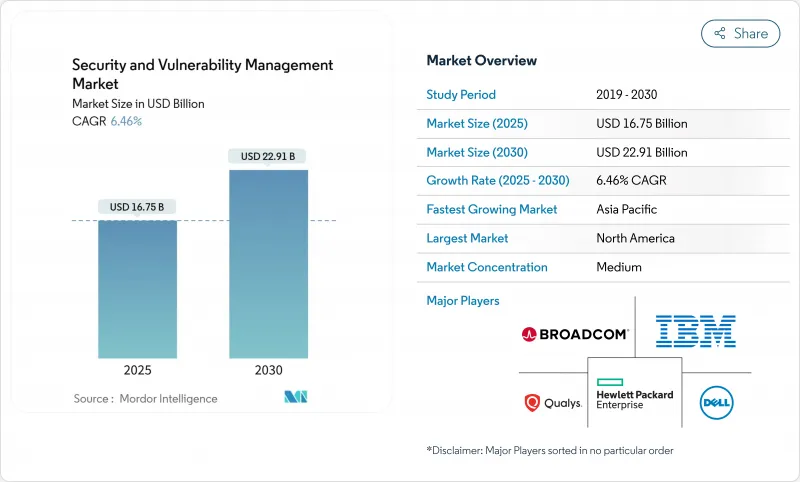

보안 및 취약성 관리 시장 규모는 2025년에 167억 5,000만 달러에 이르고, 2030년에는 229억 1,000만 달러로 확대될 것으로 예상되며, 기간 중 CAGR은 6.5%를 나타낼 전망입니다.

보안 및 취약성 관리 시장은 사이버 리스크 규제의 의무화, 이사회의 의식 증가, 도구 난립을 억제하는 통합 노출 관리 플랫폼으로의 전략적 이동 등의 혜택을 계속 받고 있습니다. 급속한 디지털화, AI를 활용한 공격, 제로 트러스트의 채택은 거시 경제의 압력에도 불구하고 예산의 성장을 유지하고 보안 및 취약성 관리 시장이 기업 탄력성의 핵심 기둥임을 보여줍니다. 4분의 3 기업이 적은 공급업체를 요구하기 때문에 공급업체의 통합은 여전히 결정적인 힘이 되고 있으며 플랫폼 기업은 스캐닝에서 자동 복구로 전환하고 있습니다. 리스크 기반 애널리틱스는 이제 원시 심각도 계산을 능가하고 있으며 보안 및 취약성 관리 시장이 인수 판단을 위해 지속적인 시각화를 요구하는 보험 회사와 어떻게 일치하는지 반영합니다.

세계의 보안 및 취약성 관리 시장 동향 및 인사이트

사이버 공격 증가와 고도화

IBM은 피싱에 의한 정보 절취가 전년 대비 84% 증가한 것을 기록했으며, ChatGPT-4는 식별자를 제시한 경우 하루 동안 CVE의 87%를 악용했습니다. 제조업은 운영기술의 갭이 공갈자를 유혹하기 때문에 여전히 가장 노리는 업종이 되고 있습니다. 아시아태평양에서는 2024년 인시던트가 13% 증가하여 보안 및 취약성 관리 시장의 우선순위가 더욱 높아졌습니다. ID를 중심으로 한 침입은 현재 침해의 30%를 차지하고 있으며, 자격증 도난이 주된 액세스 벡터가 되고 있습니다. 그러므로 보안 및 취약성 관리 시장은 종합적인 패치 적용보다 악용 가능성에 중점을 둔 우선순위화에 축 발을 옮깁니다.

클라우드와 DevOps의 신속한 도입으로 공격 대상 확대

Microsoft에서 실시한 멀티클라우드의 위험 조사를 통해 38%의 조직이 심각한 취약성을 가진 공개적으로 고도로 특권화된 워크로드를 실행하고 있음을 확인했습니다. Palo Alto Networks는 익스포저의 80%가 컨테이너화된 환경에 존재한다는 사실을 발견했으며 DevOps의 복잡성을 돋보이게 했습니다. 소규모 기업의 68%는 DevSecOps를 실천하고 있다고 주장하고 있지만, 커밋마다 스캔하는 것은 불과 12%이며, 보안 및 취약성 관리 시장이 임베디드 스캔을 제공할 기회를 창출하고 있습니다. Google Cloud의 Security Command Center로 대표되는 에이전트리스 커버리지는 배포 시 마찰을 없애고 보안 및 취약성 관리 시장에서 채택을 가속화합니다.

중소기업에게 높은 총 소유비용

중소기업 경영진의 93%가 사이버 리스크를 인식하고 있음에도 불구하고 새로운 도구에 투자하는 것은 36%를 나타낼 전망입니다. 유럽 조사는 침해된 중소기업의 60%가 6개월 이내에 폐쇄되어 예산이 희박한 것으로 나타났습니다. 뉴욕 병원에서는 소규모 시설에서는 연간 5만 달러, 대규모 네트워크에서는 연간 200만 달러의 규정 준수 비용을 예상하고 있습니다. 보안 및 취약성 관리 시장은 스캔, 위험 점수 및 대시보드 분석을 단일 클라우드 라이선스로 번들로 제공하는 구독 모델을 지원합니다.

부문 분석

보안 및 취약성 관리 시장 규모는 취약성 평가 및 보고가 2024년 56억 달러에 이르렀으며 총 매출의 33.5%에 해당합니다. RBVM은 CAGR 7.1%를 나타내지만, 이는 구매자가 진정한 위험을 초래하는 3% 결함을 목표로 하기 때문이며, 이는 Tenable의 Vulcan Cyber 인수에 의해 검증된 전략입니다. 컨테이너 및 클라우드 워크로드 스캔은 Kubernetes 채택과 함께 증가하고 용도 보안 테스트는 코드, 파이프라인 및 런타임 아티팩트를 다루는 자세 관리 플랫폼에 통합됩니다.

RBVM 제품은 현재 위협 인텔리전스 피드, 자산 중요도 점수, 익스플로잇 가용성을 포함하여 정적 목록이 아닌 순위가 지정된 백로그를 생성합니다. 따라서 보안 및 취약성 관리 시장은 감지에서 의사 결정 지원으로 전환하고 있습니다. 패치 및 구성 모듈은 규제된 수직 시장에서 여전히 중요하며 IoT/OT 스캐너는 펌웨어의 약점을 발견하기 위해 자체 프로토콜을 분석합니다. 이러한 모듈의 다양성은 기업 업데이트주기를 지원하는 단일 유리 비전의 징후입니다.

은행, 방위 프라임 및 유틸리티이 물리적 경계 내에서 기밀 데이터를 보호하기 위해 2024년 보안 및 취약성 관리 시장의 68.9%를 On-Premise 배포가 차지했습니다. 그럼에도 불구하고 클라우드 도입은 2030년까지 연평균 복합 성장률(CAGR) 8.1%를 나타낼 전망입니다. Google Cloud의 에이전트 없는 취약성 검색은 소프트웨어 롤아웃을 필요로 하지 않으며 개념 입증 노력을 가속화하기 위해 SaaS 딜리버리의 매력을 높입니다.

하이브리드 모델은 내부 네트워크의 낮은 대기 시간 스캔과 탄력적인 클라우드 분석을 결합하여 대기업 로드맵을 지배합니다. 따라서 보안 및 취약성 관리 시장은 On-Premise 컬렉터, 프라이빗 클라우드 노드 및 하이퍼스케일 분석 메쉬로 진화합니다. 정책 페더레이션을 통해 고객은 클라우드의 이점을 활용하면서 NIS2 및 CMMC의 의무를 충족할 수 있으며 모든 배포 모델만으로 모든 제어 프레임워크를 만족시킬 수 있습니다.

지역 분석

2024년 보안 및 취약성 관리 시장은 북미가 37.4%의 점유율을 차지했습니다. CMMC 2.0 및 대통령령 14144와 같은 연방 정부의 지침은 지속적인 취약성 거버넌스를 조달 규칙에 통합합니다. 캐나다와 멕시코는 국경을 넘어서는 중요한 인프라 프로젝트에 유사한 기준선을 채택하여 지출의 연속성을 보장합니다. 높은 침해 비용, 대규모 기술 벤더 기반, 활발한 사이버 보험 시장이 리더십을 유지.

아시아태평양의 향후 CAGR은 7.5%를 나타낼 전망입니다. PwC는 세계 사이버 인시던트의 31%를 수용하기 위해 2027년 지역 사이버 보안 지출을 520억 달러로 예측했습니다. 호주 사이버 보안법 2024는 스마트 장치의 기준을 시행하고 랜섬웨어 지불에 관한 정보 공개를 의무화하고 있으며, 뉴질랜드의 NCSC는 공공 부문의 관리를 실시했습니다. 중국, 일본, 인도, 한국은 제조 주도 수요를 견인하고 보안 및 취약성 관리 시장을 공장 바닥과 클라우드 스택으로 밀어 올립니다.

유럽에서는 NIS2가 27개 회원국에서 시행되고 에너지, 운송, 금융, 건강 관리 사업자에게 1,000만 유로(1,160만 달러)에 달하는 벌칙이 부과됩니다. 독일, 프랑스, 이탈리아, 스페인, 영국은 이 지침에 따라 국내법을 개정하고 꾸준한 프로젝트 파이프라인을 구축하고 있습니다. 남미와 중동 및 아프리카는 디지털 서비스의 성장으로 새로운 공격대상이 출현해 각국이 EU와 미국의 틀을 참고로 한 전략을 입안하게 되었기 때문에 새로운 기세를 기록하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 사이버 공격 증가와 교묘화

- 클라우드와 DevOps의 급속한 도입으로 공격 대상 영역이 확대

- 규제 준수 및 데이터 주권의 의무

- 중요 인프라에서 IoT/OT 자산의 급증

- 사이버 보험의 인수에는 지속적인 취약성의 가시화가 필요

- 공급망 전체에 걸친 소프트웨어 부품표(SBOM)의 의무

- 시장 성장 억제요인

- 중소기업에 있어서 높은 총 소유비용

- 숙련된 사이버 보안 인력의 부족

- 취약성 데이터의 과부하에 의한 경고 피로

- 벤더 통합과 플랫폼 락인의 우려

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 유형별

- 취약성 평가 및 보고

- 패치 및 구성 관리

- 위험 기반 취약성 관리(RBVM)

- 컨테이너 및 클라우드 워크로드 스캐닝

- 애플리케이션 보안 테스트

- IoT/OT 취약성 관리

- 배포 모드별

- On-Premise

- 클라우드

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자별

- BFSI

- 헬스케어 및 생명과학

- 정부 및 방위

- IT 및 통신

- 제조 및 산업

- 소매 및 전자상거래

- 에너지 및 유틸리티

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Tenable Holdings Inc.

- Qualys Inc.

- Rapid7 Inc.

- IBM Corporation

- Cisco Systems Inc.

- Microsoft Corporation

- Broadcom Inc.(Symantec)

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Trend Micro Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- McAfee Corp.

- Tripwire Inc.(Belden)

- Ivanti

- ServiceNow Inc.

- ATandT Cybersecurity(AlienVault)

- Skybox Security Inc.

- F-Secure Corporation

- Flexera Software LLC(Secunia Research)

- Netskope Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.03The Security and Vulnerability Management market size reached USD 16.75 billion in 2025 and is forecast to climb to USD 22.91 billion by 2030, delivering a 6.5% CAGR over the period.

The Security and Vulnerability Management market continues to benefit from mandatory cyber-risk regulations, heightened board awareness, and a strategic shift toward unified exposure-management platforms that limit tool sprawl. Rapid digitization, AI-enabled attacks, and zero-trust adoption sustain budget growth despite macroeconomic pressure, showing the Security and Vulnerability Management market as a core pillar of enterprise resilience. Vendor consolidation remains a defining force because three-quarters of organizations want fewer suppliers, urging platform players to stretch from scanning to automated remediation. Risk-based analytics now outrank raw severity counts, reflecting how the Security and Vulnerability Management market aligns with insurers that demand continuous visibility for underwriting decisions.

Global Security And Vulnerability Management Market Trends and Insights

Rising Volume and Sophistication of Cyber-Attacks

IBM recorded an 84% year-on-year rise in infostealers delivered through phishing, while ChatGPT-4 exploited 87% of one-day CVEs when presented with identifiers, signalling a critical shift in adversarial capabilities. Manufacturing remains the most targeted industry as operational-technology gaps tempt extortionists. The Asia-Pacific region saw a 13% incident increase in 2024, reinforcing its priority within the Security and Vulnerability Management market. Identity-centric intrusions now make up 30% of breaches, turning credential theft into the main access vector. The Security and Vulnerability Management market therefore pivots toward exploitability-led prioritisation rather than blanket patching.

Rapid Cloud and DevOps Adoption Enlarging Attack Surface

Microsoft's multicloud risk study found that 38% of organisations run publicly exposed, highly privileged workloads with critical vulnerabilities. Palo Alto Networks discovered that 80% of exposures sit in containerised environments, underscoring the complexity DevOps introduces. Although 68% of small firms claim DevSecOps practices, only 12% scan at each commit, creating opportunity for the Security and Vulnerability Management market to deliver embedded scanning. Agentless coverage, exemplified by Google Cloud's Security Command Center, removes deployment friction and accelerates adoption across the Security and Vulnerability Management market.

High Total Cost of Ownership for SMEs

Ninety-three percent of SME executives recognise cyber risk, yet only 36% invest in new tools because two-thirds cite cost hurdles. European studies reveal that 60% of breached SMEs shut within six months, illustrating budget tension. Hospitals in New York estimate yearly compliance bills that range from USD 50,000 for small facilities to USD 2 million for large networks. The Security and Vulnerability Management market answers with subscription models that bundle scanning, risk scoring, and dashboard analytics into a single cloud licence.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Compliance and Data Sovereignty Mandates

- Proliferation of IoT/OT Assets in Critical Infrastructure

- Shortage of Skilled Cybersecurity Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Security and Vulnerability Management market size attributed to Vulnerability Assessment and Reporting stood at USD 5.6 billion in 2024, equivalent to 33.5% of total revenue. RBVM is expanding at 7.1% CAGR because buyers target the 3% of flaws that raise real risk, a strategy validated by Tenable's Vulcan Cyber acquisition. Container and cloud workload scanning rise in tandem with Kubernetes adoption, while Application Security Testing integrates into posture-management platforms that cover code, pipeline, and runtime artefacts.

RBVM products now ingest threat-intelligence feeds, asset criticality scores, and exploit availability, generating ranked backlogs rather than static lists. The Security and Vulnerability Management market therefore migrates from detection to decision support. Patch-and-configuration modules remain crucial for regulated verticals, and IoT/OT scanners parse proprietary protocols to uncover firmware weaknesses. This diversity of modules foreshadows a single-pane-of-glass vision that anchors enterprise renewal cycles.

On-premise deployments controlled 68.9% of the Security and Vulnerability Management market in 2024 as banks, defence primes, and utilities protect sensitive data inside physical boundaries. Nonetheless, cloud deployment is surging at an 8.1% CAGR through 2030. Google Cloud's agentless vulnerability scanning eliminates software rollouts and speeds proof-of-concept efforts, raising the attractiveness of SaaS delivery.

Hybrid models dominate large-enterprise roadmaps because they combine low-latency scanning of internal networks with elastic cloud analytics. The Security and Vulnerability Management market thus evolves into a mesh of on-premise collectors, private-cloud nodes, and hyperscale analytics. Policy federations allow customers to meet NIS2 or CMMC obligations while capitalising on cloud benefits, ensuring that no deployment model alone will satisfy every control framework.

The Security and Vulnerability Management Market Report is Segmented by Type (Vulnerability Assessment and Reporting, Patch and Configuration Management, and More), Deployment Mode (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated the Security and Vulnerability Management market with a 37.4% share in 2024. Federal mandates such as CMMC 2.0 and Executive Order 14144 embed continuous vulnerability governance into procurement rules. Canada and Mexico adopt similar baselines for cross-border critical-infrastructure projects, ensuring spending continuity. High breach costs, a large technology vendor base, and active cyber-insurance markets sustain leadership.

Asia-Pacific registers the highest future CAGR at 7.5%. PwC projects regional cybersecurity outlays of USD 52 billion in 2027 as boards react to a 31% slice of global cyber incidents. Australia's Cyber Security Act 2024 enforces baselines for smart devices and requires ransomware payment disclosure, while New Zealand's NCSC implements public-sector controls. China, Japan, India, and South Korea drive manufacturing-led demand, pushing the Security and Vulnerability Management market into factory floors and cloud stacks alike.

Europe follows a firm path as NIS2 takes effect across 27 member states, subjecting energy, transport, finance, and healthcare operators to penalty levels that reach EUR 10 million (USD 11.60 million). Germany, France, Italy, Spain, and the United Kingdom have adapted domestic legislation to align with the directive, creating steady project pipelines. South America and the Middle East and Africa record emerging momentum because digital services growth exposes fresh attack surfaces, prompting nations to draft strategies that reference EU and U.S. frameworks.

- Tenable Holdings Inc.

- Qualys Inc.

- Rapid7 Inc.

- IBM Corporation

- Cisco Systems Inc.

- Microsoft Corporation

- Broadcom Inc. (Symantec)

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Trend Micro Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- McAfee Corp.

- Tripwire Inc. (Belden)

- Ivanti

- ServiceNow Inc.

- ATandT Cybersecurity (AlienVault)

- Skybox Security Inc.

- F-Secure Corporation

- Flexera Software LLC (Secunia Research)

- Netskope Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising volume and sophistication of cyber-attacks

- 4.2.2 Rapid cloud and DevOps adoption enlarging attack surface

- 4.2.3 Regulatory compliance and data sovereignty mandates

- 4.2.4 Proliferation of IoT/OT assets in critical infrastructure

- 4.2.5 Cyber-insurance underwriting now requires continuous vulnerability visibility

- 4.2.6 Software Bill of Materials (SBOM) mandates across supply-chains

- 4.3 Market Restraints

- 4.3.1 High total cost of ownership for SMEs

- 4.3.2 Shortage of skilled cybersecurity talent

- 4.3.3 Alert-fatigue from vulnerability data overload

- 4.3.4 Vendor consolidation and platform lock-in concerns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Vulnerability Assessment and Reporting

- 5.1.2 Patch and Configuration Management

- 5.1.3 Risk-Based Vulnerability Management (RBVM)

- 5.1.4 Container and Cloud Workload Scanning

- 5.1.5 Application Security Testing

- 5.1.6 IoT / OT Vulnerability Management

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Defense

- 5.4.4 IT and Telecom

- 5.4.5 Manufacturing and Industrial

- 5.4.6 Retail and E-Commerce

- 5.4.7 Energy and Utilities

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tenable Holdings Inc.

- 6.4.2 Qualys Inc.

- 6.4.3 Rapid7 Inc.

- 6.4.4 IBM Corporation

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Microsoft Corporation

- 6.4.7 Broadcom Inc. (Symantec)

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Trend Micro Inc.

- 6.4.11 Palo Alto Networks Inc.

- 6.4.12 Check Point Software Technologies Ltd.

- 6.4.13 CrowdStrike Holdings Inc.

- 6.4.14 Fortinet Inc.

- 6.4.15 McAfee Corp.

- 6.4.16 Tripwire Inc. (Belden)

- 6.4.17 Ivanti

- 6.4.18 ServiceNow Inc.

- 6.4.19 ATandT Cybersecurity (AlienVault)

- 6.4.20 Skybox Security Inc.

- 6.4.21 F-Secure Corporation

- 6.4.22 Flexera Software LLC (Secunia Research)

- 6.4.23 Netskope Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment