|

시장보고서

상품코드

1637897

정부기관용 클라우드 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Government Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

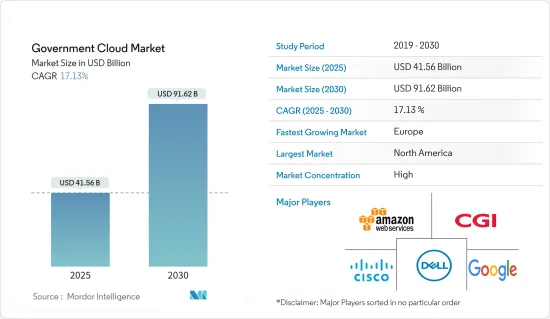

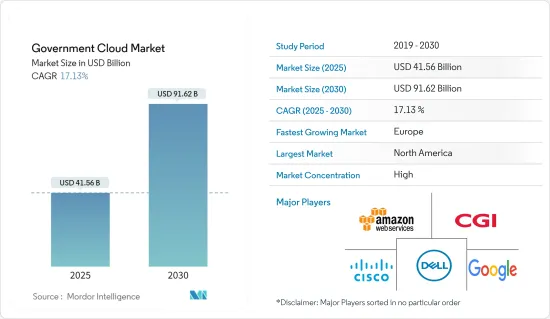

정부기관용 클라우드 시장 규모는 2025년에 415억 6,000만 달러로 추정되고, 예측기간 2025년부터 2030년까지의 CAGR은 17.13%로 전망되며, 2030년에는 916억 2,000만 달러에 달할 것으로 예측됩니다.

정부기관용 클라우드란 정부기관용으로 명확하게 구축된 가상화와 클라우드 컴퓨팅 시스템을 말합니다. 이 세계 프로그램은 전 세계 연방 정부의 운영, 재무, 전략 및 IT 목표를 지원하는 클라우드 솔루션을 식별하고 개발하기 위한 것입니다.

주요 하이라이트

- 인구조사 데이터 증가(인구의 끊임없는 증가), 새로운 시책이나 이니셔티브, 다른 지역과의 협력, 신규 사업의 급증에 의한 GDP 증가 등에 의해 정부의 데이터 생성량은 증가하고 있습니다. 물리적 하드웨어 기반 레거시 시스템은 비효율적이며 공간이 부족할 수 있습니다. 따라서 정부기관용 클라우드가 필요합니다.

- 또한 정부는 클라우드 기능을 활용하여 보다 신속하고 확장 가능한 시민용 애플리케이션 및 서비스를 생성할 수 있습니다. 행정기관은 클라우드 네이티브 보안 서비스를 이용하여 보안 향상, 전개의 근대화와 안전성 확보, 클라우드 네이티브의 자동 스케일링 기능으로 높은 내결함성을 실현할 수 있습니다.

- 국가와 지역의 법률, 시책 및 전술을 바탕으로 많은 국가에서 정부 클라우드가 상승하고 있습니다. 예를 들어, 미국의 GovCloud 이니셔티브는 특히 보안에 중점을 두고 확립된 표준에 따라 클라우드 컴퓨팅 시스템을 채택하도록 지원합니다. 이 프로그램은 연방 클라우드 컴퓨팅 전략과 NIST 클라우드 컴퓨팅 기술 로드맵 등 몇 가지 지침을 작성합니다.

- 각 지역의 정부 시책이 시장의 큰 억제요인이 되고 있습니다. EU, 미국, 싱가포르, 인도 정부는 정부 기관의 데이터를 현지 데이터센터에 저장할 의무가 있습니다. 이러한 규제는 현지 진출기업에게는 혜택이 있지만, 세계 기업에게는 추가적인 재정적 부담을 강하게 하고 있습니다.

- COVID-19의 발생으로 정부 기관이 원격 워크 액세스를 도입하거나 다양한 국가에서 봉쇄를 시행하는 중 보안 문제에 대한 의식이 높아지고 있기 때문에 클라우드 기반 서비스 및 툴의 용도가 진행되고 있으며, 정부기관용 클라우드 시장은 큰 성장이 예상되고 있습니다.

정부기관용 클라우드 시장 동향

더 큰 클라우드 스토리지 기능에 대한 요구가 성장에 기여

- 모든 유형의 디지털 데이터는 세계적으로 항상 극적으로 증가하고 있습니다. 이러한 데이터를 효과적으로 관리하는 것이 세계 각국의 정부에 요구되고 있으며, 혁신을 촉진하고 국민의 복지와 행복을 위한 규정을 정비하는 정부의 능력이 과제가 되고 있습니다. Global Datasphere에 따르면 2025년까지 175제타바이트의 디지털 데이터가 존재한다고 합니다. 정부기관은 대량의 데이터를 작성하고 있어 클라우드 기반의 스토리지에 대한 수요가 높아지고 있다

- 클라우드 스토리지의 요구와 채용률은 모든 정부 부서에서 저비용 데이터 백업, 스토리지, 보호 요구 증가 및 모바일 기술 활용 증가로 인해 생성되는 데이터를 관리하는 요구 사항이 증가함에 따라 유리합니다.

- 또한 은행산업에서는 데이터 유출 건수가 증가하고 있기 때문에 정부계 은행은 클라우드 스토리지를 채택하고 있습니다. 클라우드 스토리지는 은행 자체 또는 타사가 관리하고 소유하는 위치에 데이터를 저장할 수 있으므로 최종 사용자의 보안을 향상시킵니다. 예상되는 기간 동안 클라우드 스토리지 채택이 진행될 것으로 예상됩니다.

- 클라우드 솔루션 시장 진출 기업은 현재 대량의 데이터가 생성되므로 데이터를 저장하고 처리하는 저렴한 방법을 개발할 필요가 있습니다. 예를 들어 Tata Communications는 지난 7월 인도 당국이 요구하는 은행, 기업, 산업 부문의 데이터 프라이버시, 보호 규정 준수, 보안 기준을 충족하기 위해 커스터마이즈된 커뮤니티 클라우드 플랫폼인 IZOTM Financial Cloud를 발표했습니다.

유럽이 가장 큰 성장을 이룰 전망입니다.

- 유럽 위원회는 2012년 최초의 클라우드 컴퓨팅 전략을 발표했습니다. 그 목적은 경제의 모든 영역에서 클라우드 컴퓨팅의 사용을 가속화하고 확대하는 것이 었습니다. 현재 유럽 대륙 기업의 36%가 클라우드 서비스를 이용하고 있으며 2020년 클라우드 직접 투자액은 추정 540억 유로(5조 6,360억 달러)로 내년에는 두배로 될 것으로 예상되고 있습니다.

- 유럽 전역에서 혁신적이고 주권적인 엣지와 클라우드 기술의 채용을 유지하기 위해서는 에지와 클라우드 설비의 밀도를 높여야 하기 때문에 유럽 시장은 클라우드 네이티브 5G를 채용하고 산업 로컬 5G 네트워크를 실현할 계획입니다. 이는 네트워크 장비 제공업체의 국제 경쟁과 IT 및 통신 사업자의 세계 실적를 활용하여 모바일 네트워크를 널리 분산된 클라우드 에지 노드의 세계 네트워크로 전환하기 때문입니다.

- 또한 유럽 연합(EU)은 향후 7년간 100억 유로(104억 4,000만 달러)를 투자해 Amazon, Google, Alibaba 등 다국적 기업에 대항할 수 있는 국내 클라우드 컴퓨팅 시장의 창설을 계획하고 있다 합니다. 이러한 요인은 예측 기간 동안 정부기관용 클라우드 시장을 밀어 올릴 것으로 예상됩니다.

- 원격지의 엔드포인트에서 사용자 로그, 시책 및 시스템에 대한 방대한 시민 데이터에 액세스하기 위해 다양한 산업 부문에서 정부기관용 클라우드를 널리 채택하는 것은 이 지역 전체 시장 성장을 가속하는 주요 요인 중 하나입니다.

정부기관용 클라우드 산업 개요

정부기관용 클라우드 시장은 마이크로소프트, Oracle NEC, IBM, 구글 등의 대기업이 정부기관용 클라우드 솔루션과 서비스를 제공하고 있으며 시장이 집중되고 있습니다. 기존 벤더가 견고한 골격을 구축하고 있기 때문에 이 시장에 대한 진입 장벽은 높습니다.

테랑가나 주 정부는 정보 기술(IT) 워크로드를 클라우드로 전환하여 전자 통치 계획을 가속화하고, 33개 부국과 289개 조직을 통해 보다 신속하고 신뢰할 수 있는 시민 서비스를 제공하며, 높은 운영 효율성 그리고 IT 비용 절감을 실현하기로 결정했습니다.

2022년 1월, Dell 기술은 애플리케이션 및 데이터가 존재하는 위치에 관계없이 일관된 경험을 제공하는 멀티클라우드 기능을 도입하여 포트폴리오가 확대됨에 따라 멀티클라우드로의 여행을 가속화했습니다. 또한 Dell 인프라 보안, 지원 및 예측 가능한 비용과 결합된 적절한 클라우드 환경 선택을 지원하는 새로운 오퍼와 리소스를 제공하고 개발자 운영(DevOps) 지원도 확대했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 연구의 정의 및 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력-Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

제6장 시장 성장 촉진요인

- 대용량 스토리지에 대한 요구가 시장 수요 견인

- 데이터의 투명성에 대한 요구가 시장 확대

제7장 시장 성장 억제요인

- 클라우드 컴퓨팅의 스킬 갭이 시장 성장 방해

제8장 시장 세분화

- 도입 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 딜리버리 모드별

- 인프라 어 서비스

- 프라폼 아즈 아 서비스

- 서비스형 소프트웨어

- 용도별

- 서버 및 스토리지

- 재해 복구 및 데이터 백업

- 보안 및 컴플라이언스

- 분석

- 컨텐츠 관리

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제9장 경쟁 구도

- 기업 프로파일

- Amazon Web Services Inc.

- CGI Inc.

- Cisco Systems Inc.

- Dell Inc.

- Google Inc.

- IBM Corporation

- Microsoft Corporation

- NetApp Inc.

- Oracle Corporation

- Rackspace Inc.

- Salesforce.com Inc.

- VMWare Inc.

제10장 투자 분석

제11장 시장 기회 및 향후 동향

AJY 25.02.07The Government Cloud Market size is estimated at USD 41.56 billion in 2025, and is expected to reach USD 91.62 billion by 2030, at a CAGR of 17.13% during the forecast period (2025-2030).

Government cloud refers to virtualization and cloud computing systems explicitly created for governmental entities. This global program aims to identify and develop cloud solutions supporting global federal governments' operational, financial, strategic, and IT goals.

Key Highlights

- Government data generation is increasing due to growing census data (constant population growth), new policies and initiatives, cooperation with other regions, and increased GDP due to the mushrooming of new businesses. Physical hardware-based legacy systems are inefficient and may run out of room. Government cloud is therefore required.

- Moreover, governments may create more swiftly and scalable applications and services for citizens by utilizing cloud capabilities. Agencies can use cloud-native security services to improve security, modernize and secure their deployment, and achieve higher resilience through cloud-native auto-scaling capabilities.

- Based on their national and local laws, policies, and tactics, government clouds are emerging in numerous nations. For instance, the GovCloud initiative in the US supports the adoption of cloud computing systems following established standards, with a particular emphasis on security. This program has produced several guidelines, including the Federal Cloud Computing Strategy and the NIST Cloud Computing Technology Roadmap.

- Government policies across different regions have been a major restraining factor for the market. The governments in the EU, US, Singapore, and India have mandated that the data from government agencies be saved in local data centers. These regulations have benefitted the local players but have exerted additional financial strain on global companies.

- With the outbreak of COVID-19, the government cloud market is expected to witness significant growth as cloud-based services and tools are increasingly adapted due to government organizations deploying remote work access and rising awareness of security issues amid lockdowns in various countries.

Government Cloud Market Trends

Need for Greater Cloud Storage Capabilities to witness growth

- Digital data of all kinds are constantly growing dramatically on a global scale. The requirement for governments worldwide to manage such data effectively is posing challenges to their capacity to foster innovation and make provisions for the welfare and happiness of their citizens. According to Global Datasphere, 175 zettabytes of digital data will exist by 2025. Government agencies are producing large amounts of data, increasing the demand for cloud-based storage.

- The need for and adoption rate of cloud storage are favored by the rise in the need for low-cost data backup, storage, and protection across all government sectors, as well as the requirement to manage the data produced by the increased use of mobile technologies.

- Additionally, due to the growing number of data breaches in the banking industry, government banks are adopting cloud storage, which enables them to save data in a location that is either maintained and owned by the bank itself or by a third party, improving end-user security. Over the projected period, this is anticipated to enhance the adoption of cloud storage.

- Players in the cloud solutions market are currently compelled to develop inexpensive ways to store and handle the data due to the volume of data produced. The government cloud market will grow due to these factors in the future; for instance, In July last year, Tata Communications launched 'IZOTM Financial Cloud,' a community cloud platform tailored to fulfill Indian authorities' demanding data privacy, protection compliance, and security criteria for the banking, enterprises, and industries sectors.

Europea to Witness the Highest Growth

- The European Commission unveiled its first cloud computing strategy in 2012. The goal of the process was to accelerate and broaden the usage of cloud computing in all spheres of the economy. Currently, 36% of the continent's companies use cloud services2, for an estimated €54 billion (USD 5636 Billion) of direct cloud spending in 2020, which is expected to double by next year.

- As the Increased density of edge and cloud facilities is needed to sustain the adoption of innovative and sovereign edge and cloud technologies across the continent, the European market is planning to adopt cloud native 5G and enable industrial local 5G networks, leveraging the global competitiveness of its network equipment providers and the worldwide footprint of its telecommunication operators to transform the mobile network into a global network of widely distributed cloud-edge nodes.

- Moreover, the European Union plans to invest EUR 10 billion(USD 10.44 Billion) over the next seven years to create a domestic cloud computing market that could compete with multinational companies like Amazon, Google, and Alibaba. These factors will boost the government cloud market during the forecast period.

- The widespread adoption of government cloud across various industrial verticals for accessing the excessive amount of citizen data regarding user logs, policies, and systems from remote endpoints is one of the key factors driving the market growth across the region.

Government Cloud Industry Overview

The market for government cloud is concentrated with major giants, such as Microsoft, Oracle NEC, IBM, and Google, providing cloud solutions and services for the government. This market's entry barrier is high since the existing vendors have a strong foothold.

In September 2022 - Amazon Web Services Inc announced that it has joined the government of Telangana for the project to transform its citizen service delivery by advancing its cloud adoption framework as the Telangana state government has decided to migrate its information technology (IT) workloads to the cloud to accelerate its eGovernance plans, and deliver faster and more reliable citizen services through its 33 departments and 289 organizations while achieving high-operational efficiency and reduced IT costs.

In January 2022 - Dell technologies sped Journey to Multi-Cloud with Portfolio Expansion with introduced multi-cloud capabilities that offer a consistent experience wherever applications and data reside, along with also expanding support for developer operations (DevOps) with new offers and resources to help choose the right cloud environment combined with the security, support and predictable cost of Dell infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Definitions and Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

6 Market Drivers

- 6.1 Need for Greater Storage Capabilities is Driving the Market Demand

- 6.2 Need for Data Transparency are Expanding the Market

7 Market Restraints

- 7.1 Cloud Computing Skills Gap is Hindering the Market Growth

8 MARKET SEGMENTATION

- 8.1 By Deployment model

- 8.1.1 Public Cloud

- 8.1.2 Private Cloud

- 8.1.3 Hybrid Cloud

- 8.2 By Delivery Mode

- 8.2.1 Infrastructure-as-a-Service

- 8.2.2 Pltaform-as-a-Service

- 8.2.3 Software-as-a-Service

- 8.3 By Application

- 8.3.1 Server and Storage

- 8.3.2 Disaster Recovery/Data Backup

- 8.3.3 Security and Compliance

- 8.3.4 Analytics

- 8.3.5 Content Management

- 8.4 By Geography

- 8.4.1 North America

- 8.4.2 Europe

- 8.4.3 Asia Pacific

- 8.4.4 Latin America

- 8.4.5 Middle East and Africa

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Amazon Web Services Inc.

- 9.1.2 CGI Inc.

- 9.1.3 Cisco Systems Inc.

- 9.1.4 Dell Inc.

- 9.1.5 Google Inc.

- 9.1.6 IBM Corporation

- 9.1.7 Microsoft Corporation

- 9.1.8 NetApp Inc.

- 9.1.9 Oracle Corporation

- 9.1.10 Rackspace Inc.

- 9.1.11 Salesforce.com Inc.

- 9.1.12 VMWare Inc.