|

시장보고서

상품코드

1906943

공공안전 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Public Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

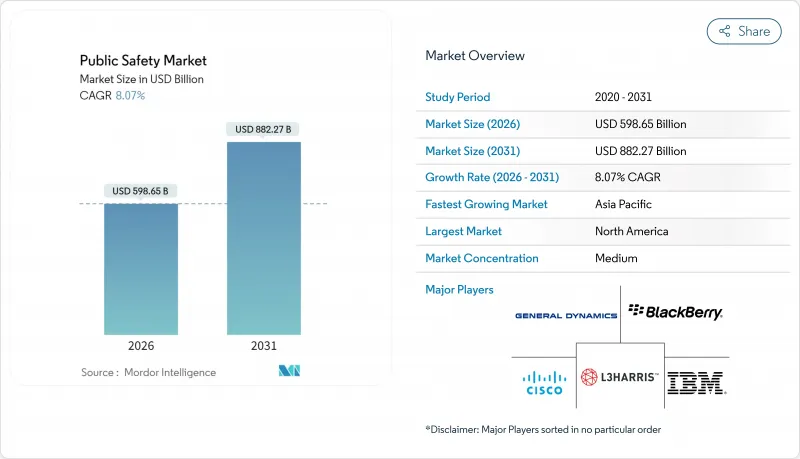

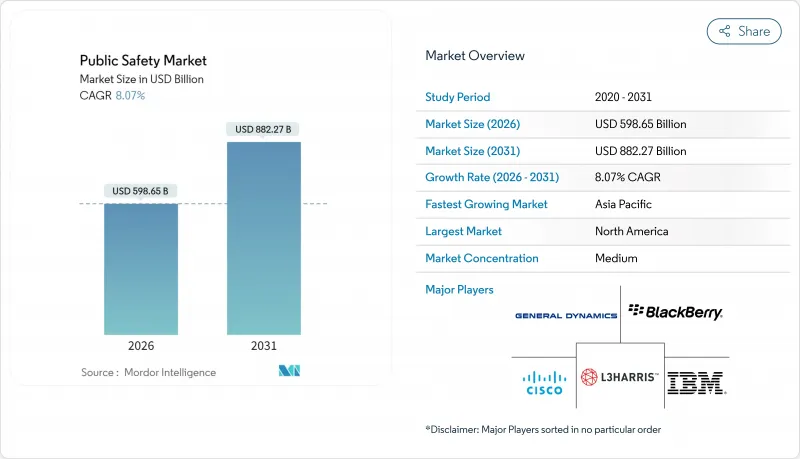

공공안전 시장은 2025년 5,539억 5,000만 달러로 평가되었고, 2026년 5,986억 5,000만 달러로 성장할 것으로 추정되며, 2026-2031년 CAGR 8.07%로 성장을 지속하여 2031년까지 8,822억 7,000만 달러에 달할 것으로 예측됩니다.

재해 구호 예산 증가, 방위 지출 확대, 노후화된 육상 이동 무선(LMR) 자산을 미션 크리티컬한 5G 네트워크로 대체하는 세계의 요청이 이 상승세를 공동으로 지원하고 있습니다. 연방 정부의 주도 노력으로 FirstNet의 63억 달러 규모의 5G 업그레이드가 플랫폼 현대화를 가속화하고 있습니다. 한편 FEMA(연방긴급사태관리청)가 2025 회계 연도에 요구한 289억 6,900만 달러의 예산은 기후 변화 관련 대응 자금의 규모를 부각시키고 있습니다. 동시에 10억 달러 규모의 스마트 시티 조성 프로그램이 제안되고 있어 실시간 감시 및 분석 기능의 도입 확대가 기대됩니다. 기업 자본의 흐름도 이러한 매크로 신호를 반영합니다. Microsoft의 UAE 거점 G42에 대한 15억 달러 출자와 두바이 경찰의 종합적인 AI 로드맵은 지정학적 야망이 지역의 공공안전 지출에 어떻게 반영되는지를 보여주는 좋은 예입니다.

세계의 공공안전 시장 동향 및 인사이트

기후 관련 재해의 빈도 및 심각화가 긴급 대응 지출 증가 초래

기후 변화로 인한 재해는 정부기관의 조달 우선순위를 재정의하고 있습니다. 허리케인 헬렌의 10년간 2,000억 달러에 이르는 부흥 비용은 재해 대응의 재정적 규모를 부각시켰습니다. 2025년 로스앤젤레스 산불 위기에서는 12,000동 이상의 건물이 소실되어 캘리포니아 주가 25억 달러의 긴급 예산을 계상했습니다. 통합 인시던트 명령 시스템 계약이 가속되었습니다. FEMA(연방 긴급 사태 관리청)의 2025년도 재해 구제 기금은 289억 6,900만 달러를 요청하였고, 그 중 10억 달러는 '강인한 인프라 및 커뮤니티 구축'에 충당되는 것이 결정되었습니다. 기술 중심의 강인화에 대한 노력이 더욱 명확해졌습니다. 카네기 재해 달러 데이터베이스에서 알 수 있듯이 각 기관은 다중 소스 데이터를 통합하는 상호 운용 가능한 플랫폼을 점점 더 강조하고 있습니다. 일본의 Spectee Pro는 AI 구동의 상황 인식 정보에 대한 수요를 실증하고 있으며, 1,100건 이상의 지자체 계약을 획득하여 거의 완벽한 연속율을 유지하고 있습니다.

높아지는 지정학적 긴장이 통합 지휘 통제 센터용 방위 및 국토 안보 예산 촉진

세계의 불안정화는 견고한 통신 시스템 및 사이버 방어로의 자본 유입을 촉진하고 있습니다. 미국 2024 회계연도 국방수권법은 대 UAS(무인항공기 시스템) 대책과 제로 트러스트 게이트웨이를 우선사항으로 삼아 민간기관에 대한 파급 효과를 시사하고 있습니다. 국내 방재 대책에서는 국가 수준의 사이버 리스크가 시민 영역에 파급되고 있음을 지적하고, 긴급 사태 관리자가 양자 내성 암호화를 요구하는 움직임을 촉구하고 있습니다. L3Harris의 차세대 보안 프로세서 판매 오더는 공급업체가 이러한 요구에 부응하고 있음을 뒷받침합니다.

분할된 전파 스펙트럼 관리는 기관 간 네트워크의 상호 운용성 억제

다양한 대역 계획 및 레거시 프로토콜이 여전히 완고한 장벽이 되고 있습니다. CISA의 '국가 상호 운용성 현장 운영 가이드'는 호환되지 않는 주파수를 주요 운영 위험으로 나열합니다. 거버넌스 부족은 문제를 악화시키고 있으며, 왜 통신할 수 없는가? 연방 수준에서는 프로젝트 25와 AES-256으로의 전환이 권장되고 있으며, 지역 수준에서의 도입 불일치가 사일로화를 지속하고 있습니다.

부문 분석

이 솔루션은 2025년 수익의 67.60%를 차지했으며, 이점은 통합 통신 네트워크, AI 기반 영상 분석 및 긴급 관리 플랫폼에 의해 지원됩니다. 이러한 솔루션은 기관이 단일 상호 운용 가능한 제품군으로 조달하는 경향이 커지고 있습니다. 중요 통신 서브시스템은 FirstNet에 의한 전국적인 5G 구축이 가져온 공공안전시장 규모 확대로부터 직접적인 혜택을 받았습니다. 서비스 분야에서는 기관이 스펙트럼 최적화, 사이버 보안 강화, AI 모델 조정을 외부 위탁하는 움직임에 따라 운영 관리 서비스와 전문 컨설팅이 CAGR 8.94%로 성장하고 있습니다.

전문 서비스의 수익 확대는 상호 운용성 감사 및 스펙트럼 관리 로드맵과 같은 내부적으로 유지되는 적은 기술 세트에 대한 수요 증가도 반영합니다. 관리 서비스 계약은 총 소유 비용을 줄이면서 가동 시간 보증을 강화하기 때문에 인원 제한에 직면하는 지자체에게 매력적입니다. 생체 인증 보안의 도입은 프라이버시 문제에 직면하고 있지만, 교통 거점 및 교정 시설에서는 여전히 진전을 볼 수 있습니다. FEMA에 의한 289억 6,900만 달러의 재해 기금 기여 요청은 인시던트 명령 대시보드에 대한 지출을 촉진하고 통합 지원 플랫폼과 관련된 공공안전 시장 규모 확대에 기여합니다.

연방기관이 기밀 데이터의 물리적 관리를 견지하고 있는 가운데, 2025년의 도입 형태에서는 온프레미스가 여전히 71.20%를 차지하고 있습니다. 그러나 종량 과금제의 경제성 및 리프레시 사이클 단축을 원동력으로 클라우드는 CAGR 9.41%로 진전하고 있습니다. 타일러 테크놀로지스사가 SaaS가 신규 계약 가치의 90%를 차지함을 밝힌 것은 구독 모델로의 결정적인 전환을 시사하고 있습니다.

하이브리드 아키텍처는 거버넌스와 위험에 대한 최적의 절충안으로 부상하고 있습니다. 엣지 노드가 위치 정보 기반 데이터를 유지하는 반면 분석 워크로드는 클라우드에서 처리되므로 AI 구동 비디오 피드 지연이 줄어듭니다. 미국 정부 인력 긴급 신고 시스템이 BlackBerry AtHoc의 클라우드 플랫폼을 명시적으로 요구하는 것은 비기밀 용도에서 오프프레미스 소프트웨어에 대한 연방 정부의 수용도가 증가하고 있음을 나타냅니다. 컴플라이언스 프레임 워크가 성숙함에 따라 공급업체는 FedRAMP 지원 스택을 번들로 제공하고 데이터 주권에 대한 우려를 줄이면서 대응 가능한 점유율을 확대하고 있습니다.

공공안전 시장 시장 세분화는 컴포넌트별(솔루션-중요 통신 네트워크, 모니터링 및 분석 시스템 등), 전개 모드별(온프레미스, 클라우드), 최종 사용자 산업별(법 집행 기관 등), 기술별(인공지능 및 예측 분석 등), 기관 유형별(연방 및 국가 기관 등) 및 지역별로 실시됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

지역별 분석

북미는 2025년 33.90%의 수익 점유율을 유지했습니다. 이는 확립된 조성 프로그램 및 FirstNet의 전국적인 전개에 연동된 성숙한 공공안전 시장 규모에 뒷받침됩니다. 유럽에서는 영국 내무성과 IBM이 공동으로 구축하는 긴급 서비스 네트워크(30만 명의 대응 요원을 대상)를 배경으로 꾸준한 도입이 진행되고 있습니다. 한편 중동은 2031년까지 8.73%라는 지역 최고 CAGR을 기록할 전망입니다. 이는 UAE, 사우디아라비아, 이스라엘이 공공안전 기술을 경제 다각화 전략에 통합하기 때문입니다.

대규모 정부계 투자 기관이 AI 인큐베이션을 가속시키고 있습니다. Microsoft의 G42에 대한 15억 달러 투자는 하이퍼스케일 컴퓨팅 및 클라우드 모범 사례를 지역 기관에 제공합니다. 두바이 경찰의 AI 전략은 예측 분석, 무인 순찰 차량, 시민 서비스 키오스크를 망라하고 종합적인 디지털 경찰 구상을 보여줍니다. 아시아태평양에서는 성숙도에 편차가 있습니다. 싱가포르 홈팀 과학기술청(HTX)은 고급 사건 분석을 위해 Google, Microsoft, Thales와 공동으로 생성된 AI 모델 '피닉스'를 개발하고 있습니다. 라틴아메리카에서는 아메리카 개발 은행의 지침을 활용하여 AI를 책임지고 통합했습니다. 우선 주 관할 구역 간 범죄 데이터 조화에 중점을 두고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 기후 관련 재해의 빈도 및 심각도 증가에 의한 긴급 대응 지출 확대

- 높아지는 지정학적 긴장이 통합 지휘 통제 센터용 방위 및 국토 안보 예산 촉진

- 공공안전 기관 전체에서 레거시 LMR에서 4G/5G 미션 크리티컬 광대역 네트워크로의 전환 의무화

- 스마트 시티 프로그램에 의한 실시간 영상 감시 및 상황 인식 플랫폼 확대

- 연방 정부의 경제 대책 패키지가 클라우드 기반의 공공안전 소프트웨어 조달 가속

- AI를 활용한 예측형 경찰 분석 기술의 융합에 의해 대응 시간 단축

- 시장 성장 억제요인

- 분단된 전파 스펙트럼 관리가 기관 네트워크 간 상호 운용성 저해

- 고액의 초기 설비 투자 및 긴 조달 사이클이 자금 부족의 지자체에서 도입 제한

- 증가하는 사회적 모니터링 및 데이터 프라이버시 규제(GDPR(EU 개인정보보호규정), CCPA)가 얼굴 인식 감시 시스템의 도입 지연 초래

- IoT 센서의 사이버 보안 취약성이 본격적인 도입에 망설임

- 밸류체인 및 공급망 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 솔루션

- 중요 통신 네트워크

- 모니터링 및 분석 시스템

- 생체인증 보안 및 인증 시스템

- 긴급 사태 및 재해 관리 플랫폼

- 인시던트 및 증거 관리 소프트웨어

- 서비스

- 전문 서비스

- 매니지드 서비스

- 솔루션

- 전개 모드별

- 온프레미스

- 클라우드

- 최종 사용자 업계별

- 법 집행 기관

- 소방서

- 응급 의료 서비스

- 운송 및 중요 인프라 사업자

- 재해 및 구조 관리 당국

- 기타 공공안전 기관

- 기술별

- 인공지능 및 예측 분석

- 사물인터넷(IoT) 센서 및 게이트웨이

- 클라우드 및 엣지 컴퓨팅

- 빅데이터 및 GIS 분석

- 5G 및 미션 크리티컬 LTE 네트워크

- 대리점 유형별

- 연방 및 국가

- 주 및 성

- 지자체 및 지역

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 이스라엘

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Motorola Solutions Inc.

- Cisco Systems Inc.

- L3Harris Technologies Inc.

- Hexagon AB

- IBM Corporation

- General Dynamics Corporation

- BlackBerry Ltd.

- Thales Group

- NICE Ltd

- Verint Systems Inc.

- Atos SE

- CentralSquare Technologies

- Semtech Corporation

- Huawei Technologies Co. Ltd.

- Everbridge Inc.

- Tyler Technologies Inc.

- Axon Enterprise Inc.

- Bosch Security Systems

- Digital Barriers plc

- Cape Analytics Inc.

- NEC Corporation

- Leonardo SpA

- Intrado Corporation

제7장 시장 기회 및 장래 전망

AJY 26.01.26The public safety market is expected to grow from USD 553.95 billion in 2025 to USD 598.65 billion in 2026 and is forecast to reach USD 882.27 billion by 2031 at 8.07% CAGR over 2026-2031.

Rising disaster-relief appropriations, heightened defense outlays, and a global mandate to replace aging land-mobile-radio (LMR) assets with mission-critical 5G networks jointly underpin this upward trajectory. Federal initiatives such as FirstNet's USD 6.3 billion 5G upgrade are accelerating platform modernization, while FEMA's FY 2025 request of USD 28.969 billion underscores the scale of climate-related response funding. At the same time, a proposed USD 1 billion smart-city grant program promises to widen adoption of real-time surveillance and analytics capabilities. Corporate capital flows mirror these macro signals: Microsoft's USD 1.5 billion stake in UAE-based G42 and Dubai Police's all-encompassing AI roadmap exemplify how geopolitical ambitions translate into local public-safety spend.

Global Public Safety Market Trends and Insights

Heightened Frequency and Severity of Climate-related Disasters Increasing Emergency-Response Spending

Climate-induced hazards are redefining agency procurement priorities. Hurricane Helene's USD 200 billion, 10-year recovery bill spotlighted the fiscal magnitude of disaster response. The 2025 Los Angeles wildfire crisis razed >12,000 structures and triggered California's USD 2.5 billion emergency allocation, accelerating contracts for integrated incident-command systems. FEMA's FY 2025 Disaster Relief Fund call for USD 28.969 billion, including a USD 1 billion Building Resilient Infrastructure and Communities carve-out, further evidences commitment to technology-centric resilience. Agencies increasingly favor interoperable platforms that aggregate multi-source data, as documented in the Carnegie Disaster Dollar Database. Japan's Spectee Pro illustrates demand for AI-driven situational intelligence, having secured 1,100+ local-government contracts with near-perfect retention.

Rising Geopolitical Tensions Pushing Defense and Homeland-Security Budgets for Integrated Command-and-Control Centres

Global insecurity is funneling capital into hardened communications and cyber-defense. The U.S. FY 2024 National Defense Authorization Act prioritizes counter-UAS and zero-trust gateways, signaling cross-over benefits for civil agencies. Domestic Preparedness notes the spill-over of nation-state cyber risk into civic domains, prompting emergency managers to seek quantum-resilient encryption. L3Harris' next-generation security-processor award underlines vendor response to these requirements.

Fragmented Radio-Spectrum Governance Hindering Interoperability Between Agency Networks

Diverse band plans and legacy protocols remain stubborn barriers. CISA's National Interoperability Field Operations Guide lists incompatible frequencies as a primary operational risk. Governance gaps exacerbate the issue; the "Why Can't We Talk?" report cites duplicated funding streams and absent coordination as root causes. Though Project 25 and AES-256 transitions are endorsed at federal level, inconsistent local adoption perpetuates silos.

Other drivers and restraints analyzed in the detailed report include:

- Mandated Transition from Legacy LMR to 4G/5G Mission-Critical Broadband Networks Across Public-Safety Agencies

- Smart-City Programs Scaling Real-time Video Surveillance and Situational-Awareness Platforms

- High Up-front CAPEX and Long Procurement Cycles Limiting Adoption in Cash-Strapped Municipalities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions contributed 67.60% of 2025 revenue, a dominance underpinned by bundled communication networks, AI-enabled video analytics, and emergency-management platforms that agencies increasingly procure as single, interoperable suites. Critical-communication sub-systems benefited directly from the public safety market size uplift generated by FirstNet's nationwide 5G build-out. Within services, managed operations and professional consulting are growing at 8.94% CAGR as agencies outsource spectrum optimization, cybersecurity hardening, and AI model tuning.

Professional-services revenue momentum also mirrors growing demand for interoperability audits and spectrum-management road-maps-skill sets rarely retained in-house. Managed-service contracts reduce total cost of ownership yet bolster uptime guarantees, appealing to municipalities constrained by head-count caps. Biometric-security rollouts face privacy headwinds but still post gains in transportation hubs and correctional facilities. FEMA's USD 28.969 billion disaster-fund call fuels spend on incident-command dashboards, expanding the public safety market size attached to integrated response platforms.

On-premise still holds 71.20% of 2025 deployments as federal entities insist on physical control over sensitive data. Cloud, however, advances at 9.41% CAGR, driven by pay-as-you-go economics and reduced refresh cycles. Tyler Technologies' revelation that SaaS now represents 90% of new contract value signals a decisive pivot toward subscription models.

Hybrid architectures are emerging as the preferred governance-risk compromise: edge nodes retain location-based data while analytical workloads float in the cloud, trimming latency for AI-driven video feeds. The U.S. government's Personnel Emergency Notification System, explicitly requiring BlackBerry AtHoc's cloud platform, signals increasing federal comfort with off-premise software for non-classified uses. As compliance frameworks mature, vendors bundle FedRAMP-ready stacks, expanding addressable share while mitigating data-sovereignty concerns.

Public Safety Market is Segmented by Component (Solution - Critical Communication Network, Surveillance and Analytics Systems, and More), Deployment Type (On-Premise, Cloud), End-User Vertical (Law Enforcement Agencies, and More), Technology (Artificial Intelligence and Predictive Analytics, and More), Agency Type (Federal/National, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 33.90% revenue share in 2025, underpinned by entrenched grant programs and the mature public safety market size tied to FirstNet's nationwide footprint. Europe continues steady adoption, bolstered by the UK's Home Office-IBM Emergency Services Network that will serve 300,000 responders. Yet the Middle East commands the highest regional CAGR at 8.73% through 2031 as UAE, Saudi Arabia, and Israel embed public-safety tech within broader economic-diversification blueprints.

Large sovereign investment vehicles accelerate AI incubation; Microsoft's USD 1.5 billion equity in G42 brings hyperscale compute and cloud best practices to regional agencies. Dubai Police's AI strategy spans predictive analytics, unmanned patrol vehicles, and citizen-service kiosks, illustrating a holistic digital-policing vision. Asia-Pacific displays mixed maturity: Singapore's Home Team Science and Technology Agency (HTX) co-develops the Phoenix generative-AI model with Google, Microsoft, and Thales for advanced incident-analytics. Latin America leverages Inter-American Development Bank guidance to integrate AI responsibly, focusing first on crime-data harmonization across provincial jurisdictions.

- Motorola Solutions Inc.

- Cisco Systems Inc.

- L3Harris Technologies Inc.

- Hexagon AB

- IBM Corporation

- General Dynamics Corporation

- BlackBerry Ltd.

- Thales Group

- NICE Ltd

- Verint Systems Inc.

- Atos SE

- CentralSquare Technologies

- Semtech Corporation

- Huawei Technologies Co. Ltd.

- Everbridge Inc.

- Tyler Technologies Inc.

- Axon Enterprise Inc.

- Bosch Security Systems

- Digital Barriers plc

- Cape Analytics Inc.

- NEC Corporation

- Leonardo S.p.A.

- Intrado Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Frequency and Severity of Climate-related Disasters Increasing Emergency Response Spending

- 4.2.2 Rising Geopolitical Tensions Pushing Defense and Homeland Security Budgets for Integrated Command-and-Control Centres

- 4.2.3 Mandated Transition from Legacy LMR to 4G/5G Mission-Critical Broadband Networks Across Public Safety Agencies

- 4.2.4 Smart City Programs Scaling Real-time Video Surveillance and Situational Awareness Platforms

- 4.2.5 Federal Stimulus Packages Accelerating Cloud-based Public Safety Software Procurement

- 4.2.6 Convergence of AI-Powered Predictive Policing Analytics Reducing Response Time

- 4.3 Market Restraints

- 4.3.1 Fragmented Radio Spectrum Governance Hindering Interoperability Between Agency Networks

- 4.3.2 High Up-front CAPEX and Long Procurement Cycles Limiting Adoption in Cash-Strapped Municipalities

- 4.3.3 Rising Public Scrutiny and Data-Privacy Regulations (GDPR, CCPA) Slowing Deployment of Facial-Recognition Surveillance

- 4.3.4 Cyber-security Vulnerabilities in IoT Sensors Creating Reluctance for Full-scale Roll-outs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Critical Communication Network

- 5.1.1.2 Surveillance and Analytics Systems

- 5.1.1.3 Biometric Security and Authentication Systems

- 5.1.1.4 Emergency and Disaster Management Platforms

- 5.1.1.5 Incident and Evidence Management Software

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solution

- 5.2 By Deployment Type

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Vertical

- 5.3.1 Law Enforcement Agencies

- 5.3.2 Firefighting Departments

- 5.3.3 Emergency Medical Services

- 5.3.4 Transportation and Critical Infrastructure Operators

- 5.3.5 Disaster and Rescue Management Authorities

- 5.3.6 Other Public Safety Bodies

- 5.4 By Technology

- 5.4.1 Artificial Intelligence and Predictive Analytics

- 5.4.2 Internet of Things Sensors and Gateways

- 5.4.3 Cloud and Edge Computing

- 5.4.4 Big-Data and GIS Analytics

- 5.4.5 5G and Mission-Critical LTE Networks

- 5.5 By Agency Type

- 5.5.1 Federal / National

- 5.5.2 State and Provincial

- 5.5.3 Municipal / Local

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia

- 5.6.4.7 New Zealand

- 5.6.4.8 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Israel

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Motorola Solutions Inc.

- 6.4.2 Cisco Systems Inc.

- 6.4.3 L3Harris Technologies Inc.

- 6.4.4 Hexagon AB

- 6.4.5 IBM Corporation

- 6.4.6 General Dynamics Corporation

- 6.4.7 BlackBerry Ltd.

- 6.4.8 Thales Group

- 6.4.9 NICE Ltd

- 6.4.10 Verint Systems Inc.

- 6.4.11 Atos SE

- 6.4.12 CentralSquare Technologies

- 6.4.13 Semtech Corporation

- 6.4.14 Huawei Technologies Co. Ltd.

- 6.4.15 Everbridge Inc.

- 6.4.16 Tyler Technologies Inc.

- 6.4.17 Axon Enterprise Inc.

- 6.4.18 Bosch Security Systems

- 6.4.19 Digital Barriers plc

- 6.4.20 Cape Analytics Inc.

- 6.4.21 NEC Corporation

- 6.4.22 Leonardo S.p.A.

- 6.4.23 Intrado Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment