|

시장보고서

상품코드

1910484

배향성 스트랜드 보드(OSB) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oriented Strand Board (OSB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

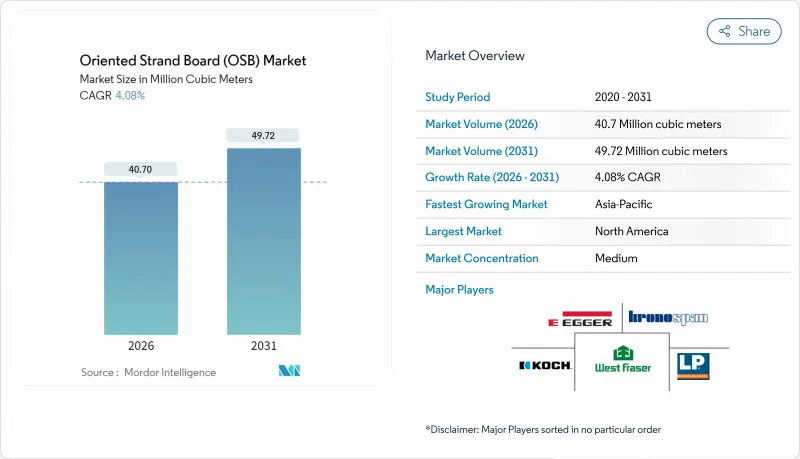

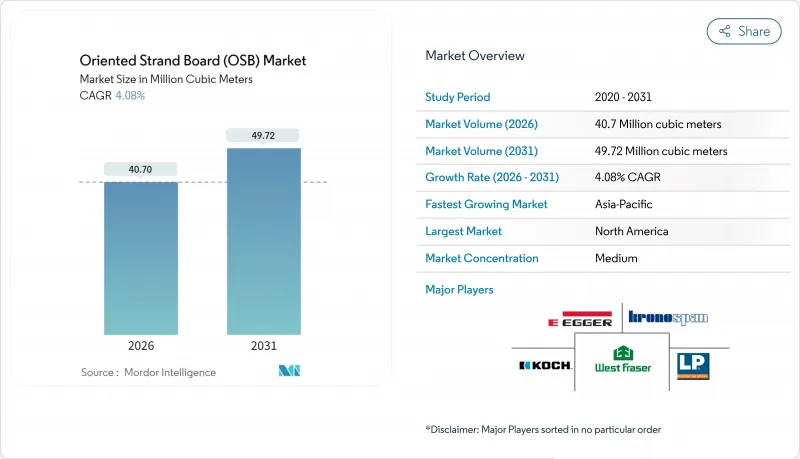

2026년 배향성 스트랜드 보드(OSB) 시장 규모는 4,070만 입방미터로 추정되며, 2025년 3,910만 입방미터에서 성장할 전망입니다.

2031년에는 4,972만입방미터에 달하고, 2026년부터 2031년에 걸쳐 CAGR 4.08%를 나타낼 것으로 예상됩니다.

이 꾸준한 성장 궤적은 합판에 대한 비용 우위성, 저탄소 재료를 뒷받침하는 규제면에서의 추풍, 공정 자동화에 대한 투자가 배향성 스트랜드 보드(OSB) 시장 전체 수요를 강화하고 있다는 것을 부각하고 있습니다. 성숙지역의 건설업체는 운영효율을 추구하고, 신흥경제국 정부는 인프라 자금을 엔지니어드우드에 돌려주고 있으며, 이들이 함께 건전한 수량 성장을 지원하고 있습니다. 경쟁 활동은 공장 자동화와 등급 혁신에 초점을 맞추고 있으며, 웨이어하우저의 AI에 의한 건조기 최적화는 디지털 툴이 생산량과 다운스트림 공정의 패널 품질을 향상시키는 좋은 예입니다.

세계의 배향성 스트랜드 보드(OSB) 시장 동향과 인사이트

합판에 대한 비용 효율적인 대체 재료

제조업체 각사는 스트랜드 배치 소프트웨어와 정밀 수지 투여 기술을 활용해 변동비를 삭감하는 것으로, 침엽수 합판과의 생산 코스트차를 계속적으로 축소하고 있습니다. 루이지애나 퍼시픽사는 2025년 1분기에 OSB 매출액 2억 6,700만 달러를 기록해 스팟 가격이 11% 하락했음에도 불구하고 출하량을 유지했습니다. 이는 합판 생산 능력의 제약으로 인해 수요가 이동한 만큼을 배향성 스트랜드 보드(OSB) 시장이 흡수하고 있는 실태를 뒷받침하고 있습니다. 특히 목재 가격이 입방 미터당 미화 100달러를 초과하는 변동을 보이는 상황에서는 예측 가능한 패널 가격이 주택 건축업자의 예산 확실성을 지원합니다. 그 결과, 배향성 스트랜드 보드(OSB) 시장은 종래 합판이 지배하고 있던 내장 마무리재나 가구용 기재 분야에도 진출하고 있습니다.

세계 건설 활동 확대

아시아태평양의 인프라 정비 추진은 여전히 최대 수요 전환점이며, 이 지역의 CAGR 6.34% 전망에 반영되고 있습니다. 중국의 통나무 비용이 입방 미터당 110달러로 안정되어 있다는 것은 패널 구매자에게 이익률 전망을 뒷받침하는 반면, 인도와 인도네시아의 유틸리티 파이프라인은 장기적인 엔지니어드우드 수요 증가를 뒷받침하고 있습니다. 북미의 단독주택 착공건수는 2024년에 7% 증가하여 건설업체들이 OSB의 균일한 못유지능력을 평가한 결과 외장용 합판 수요 증가로 이어졌습니다. 중동에서는 사우디아라비아와 UAE의 1,800억 달러 규모의 탈탄소화 계획에 의해 목재 수입량이 3배로 증가하고, 수출업체가 새로운 배향성 스트랜드 보드(OSB) 시장 수요층을 개척할 기회가 탄생하고 있습니다. 조립식 공장에서는 OSB의 치수 정밀도를 활용하여 시공 사이클을 단축하고 있으며, 건설 수요의 기세와 패널 소비가 더욱 연동하고 있습니다.

포름알데히드 및 VOC 규제 강화

EU에서는 2026년 8월부터 포름알데히드 농도 0.080mg/m3 미만의 규제가 시행되어 UF 수지에 의존하는 제조업체는 배합 변경이나 쉐어 양도를 강요받습니다. MDI 바인더제 OSB는 면제 대상이 되는 경우가 많은 것, 화학 조성 변경에 의해 변동비가 15-20% 증가해, 코모디티그레이드의 이익률이 압박됩니다. 미국에서는 EPA의 위험 평가 초안이 62개의 이용 사례를 확인하고 직장 노출 기준의 강화를 촉구할 수 있습니다. 이로 인해 환기 설비와 시험 시설의 확충을 향한 자본 지출이 발생합니다. 컴플라이언스 대응은 접착제의 연구 개발 규모를 가진 수직 통합 사업자가 유리하며 배향성 스트랜드 보드(OSB) 시장에서 기술적 민첩성의 전략적 중요성이 더욱 높아지고 있습니다.

부문 분석

OSB/3는 2025년에 배향성 스트랜드 보드(OSB) 시장 점유율의 46.85%를 차지했고, 습윤 환경 대응 패널을 건축 기준이 추천하는 돌풍을 받아, 2031년까지 연평균 복합 성장률(CAGR) 4.58%로 시장 규모를 확대해, 배향성 스트랜드 보드(OSB) 시장에서의 역할을 한층 더 확대될 전망입니다. 제조업체는 페놀·포름알데히드 수지 또는 MDI 수지를 채용해, 나사 유지력을 손상시키지 않고 내수성을 실현. 이것에 의해 집합 주택의 벽체나 지붕 데크용의 사양 설계자에게 지지되고 있습니다. 한편, OSB/4는 틈새 고하중 바닥재 시장을 획득하고 있지만, 고밀도화가 가격감응도가 높은 수요 증가를 억제하고 있습니다. OSB/2는 건조실내용 하지판으로서 비용 효율을 유지하고 있습니다만, 설계자가 재고 관리 효율화를 위해 단일 그레이드로의 일괄 조달을 채용하는 경향으로부터, 개량형 OSB/3에의 쉐어 유출에 직면하고 있습니다.

표면 처리 기술의 혁신으로 OSB/3의 용도는 캐비닛과 장식 시장으로 확대되고 있습니다. 이것들은 종래, 거친 표면 마감 때문에 참가가 곤란했습니다. OSB 코어에 파티클 보드 표면재를 붙인 파인 OSB 제품 라인은 고압 라미네이트의 접착을 가능하게 해 하류 용도를 확대. 이로 인해 가구 산업 집적지에서 배향성 스트랜드 보드(OSB) 시장 침투가 촉진됩니다. 규제면에서는 포름알데히드 규제 강화의 우려에서 OSB/1 수요가 감퇴. 이로 인해 공장 설비 투자는 기존 생산 라인을 고부가가치 구조용 등급으로 전환하는 방향으로 시프트하고 있습니다.

본 배향성 스트랜드 보드(OSB) 보고서는 등급별(OSB/1, OSB/2, OSB/3, OSB/4), 최종 사용자 용도별(건설, 가구, 포장), 지역별(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)으로 분류되어 있습니다. 시장 예측은 수량(입방 미터)으로 제공됩니다.

지역별 분석

북미는 풍부한 기존 공장 기반, 통합된 침엽수 공급망, 건설업자의 제품에 대한 높은 인지도로 2025년에도 배향성 스트랜드 보드(OSB) 시장 점유율의 60.05%를 유지했습니다. 미국은 19억 달러 규모로 세계 최대의 수입국이며 국내 공장이 가동률 향상을 위해 AI 대응 건조기를 도입하여 근대화를 진행하는 중에서도 주로 캐나다 및 브라질 공장에서 조달하고 있습니다. 캐나다는 수출 지향을 유지하고 있지만 급등하는 섬유 원료 비용으로 웨스트 프레이저의 프레이저 레이크 공장 폐쇄에서 볼 수 있듯이 선택적인 생산 조정을 강요하고 있습니다. 이것에 의해 지역 공급이 희박해, 가격을 지지하는 요인이 되고 있습니다.

아시아태평양은 성장의 견인역으로 중국, 인도, ASEAN 국가들이 도시철도, 데이터센터, 중층 주택 프로젝트를 가속화함으로써 2031년까지 연평균 복합 성장률(CAGR) 6.23%를 나타낼 전망입니다. 루리 그룹의 중국 최초의 Fine OSB 라인 가동은 수입 의존에서 국내 일관 생산으로의 전환을 보여주고, 리드 타임 단축과 현지 규제에 맞는 등급의 커스터마이즈를 실현합니다. 인도의 스마트 시티 계획은 엔지니어드 패널의 채용을 촉진하고 있으며 비용과 시공 속도 측면에서 단단한 재료를 능가하고 있습니다. 동남아시아에서는 관광 주도의 숙박시설 건설로 수요가 증가하고 있습니다만, 현지 생산 능력이 따라잡지 않고, 북미나 칠레공급업체에 있어서 수입 루트가 열리고 있습니다.

유럽에서는 엄격한 기후 규제가 목재 우대 정책을 정착시키는 한편, 성숙한 주택 스톡이 수요 증가를 억제하고 안정하면서도 저성장이 계속되고 있습니다. EU 전역에서 2026년에 시행되는 포름알데히드 규제에 의해 비적합 공급업체가 도태되어 이미 MDI 시스템을 도입하고 있는 공장 기회가 증가할 전망입니다. 남유럽의 개수세제 우대조치와 북유럽의 조립식 수출이 추풍이 되고, 배향성 스트랜드 보드(OSB) 시장은 CLT의 진출에 대해서도 방어 가능한 상태를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 합판에 대한 비용 효율적인 대체품

- 세계 건설 활동 확대

- 지속가능성을 중시한 엔지니어드우드에 대한 수요

- 모듈러 및 조립식 주택 붐

- 신흥 저 VOC MDI 접착제 사용 OSB 등급

- 시장 성장 억제요인

- 포름알데히드 및 VOC 규제 강화

- 목재 섬유 가격의 변동성

- CLT의 채용으로 인한 구조재 점유율 감소

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 등급별

- OSB/1

- OSB/2

- OSB/3

- OSB/4

- 최종 사용자 용도별

- 건설

- 바닥 및 지붕

- 벽

- 문

- 기둥 및 보(거푸집)

- 계단

- 기타 건설

- 가구

- 주택

- 상업

- 포장

- 식품 및 음료

- 산업

- 의약품

- 화장품

- 기타 포장

- 건설

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Arbec Forest Products Inc.

- Besgrade Plywood Sdn. Bhd.

- Coillte

- EGGER

- JM Huber Corporation

- Koch IP Holdings, LLC

- Koyuncuoglu Group of Companies

- Kronoplus Limited

- Louisiana-Pacific Corporation

- RoyOMartin

- Sonae Arauco

- STRANDPLYOSB

- Swiss Krono Group

- Tolko Industries Ltd.

- West Fraser

- Weyerhaeuser Company

- Yalong Wood

제7장 시장 기회와 향후 전망

KTH 26.01.22Oriented Strand Board (OSB) market size in 2026 is estimated at 40.7 Million cubic meters, growing from 2025 value of 39.10 Million cubic meters with 2031 projections showing 49.72 Million cubic meters, growing at 4.08% CAGR over 2026-2031.

This steady trajectory highlights how cost advantages over plywood, regulatory tailwinds favoring low-embodied-carbon materials, and process-automation investments are reinforcing demand across the oriented strand board market. Builders in mature regions seek operating efficiencies, while governments in emerging economies channel infrastructure funds toward engineered wood, collectively underpinning healthy volume growth. Competitive activity centers on mill automation and grade innovation; Weyerhaeuser's AI-guided dryer optimization exemplifies how digital tools are lifting throughput and down-line panel quality.

Global Oriented Strand Board (OSB) Market Trends and Insights

Cost-effective Substitution for Plywood

Manufacturers continue to narrow production spreads versus softwood plywood, leveraging strand-alignment software and precision resin dosing to cut variable costs. Louisiana-Pacific booked USD 267 million in OSB revenue in Q1-2025 and maintained shipment volumes despite an 11% spot-price slide, underscoring how the oriented strand board market absorbs demand displaced from constrained plywood capacity. Predictable panel pricing supports budget certainty for residential framers, especially when lumber volatility exceeds USD 100 per m3 swings. Consequently, the oriented strand board market now penetrates interior finish and furniture substrates once dominated by plywood.

Expansion of Global Construction Activity

Asia-Pacific's infrastructure drive remains the single largest demand inflection, reflected in the region's 6.34% CAGR outlook. China's stabilized log cost of USD 110 per m3 supports margin visibility for panel buyers, while public-works pipelines in India and Indonesia lift long-term engineered-wood offtake. North American single-family starts rose 7% in 2024, translating into incremental sheathing volume as builders favor OSB's uniform nail-holding capacity. the Middle East, Saudi and UAE decarbonization plans worth USD 180 billion triple timber imports, positioning exporters to tap fresh oriented strand board market pockets. Prefab factories leverage OSB's dimensional tolerance to shorten install cycles, further linking construction momentum with panel consumption.

Formaldehyde and VOC Regulations Tightening

The EU will enforce sub-0.080 mg/m3 formaldehyde ceilings from August 2026, compelling mills still reliant on UF-based resins to re-formulate or cede share. While OSB produced with MDI binders often qualifies for exemption, switching chemistry inflates variable cost 15-20%, squeezing commodity-grade margins. On the U.S. front, EPA's draft risk assessment flags 62 use-cases that might trigger tougher workplace exposure limits, creating capital spend for enhanced ventilation and test labs. Compliance pathways favor vertically integrated operators with adhesive research and development scale, adding strategic weight to technological agility in the oriented strand board market.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-driven Demand for Engineered Wood

- Modular and Prefab Housing Boom

- Wood-fiber Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OSB/3 generated 46.85% of oriented strand board market share in 2025 and is slated to widen its role as the oriented strand board market size for this grade grows at 4.58% CAGR through 2031, buoyed by building-code preference for panels rated for humid conditions. Manufacturers rely on phenol-formaldehyde or MDI resins to deliver water resistance without sacrificing screw-holding, attracting specifiers in multifamily walls and roof decks. In parallel, OSB/4 captures niche heavy-load floors, but its higher density caps price-sensitive uptake. OSB/2 remains cost-effective in dry-interior sheathing, yet faces share leakage to enhanced OSB/3 as designers adopt one-grade fits-all procurement to streamline inventories.

Surface innovations are expanding OSB/3 utility into cabinetry and decorative markets previously closed due to rough finish. Fine-OSB lines that overlay particleboard faces onto OSB cores permit high-pressure laminate adhesion, enlarging downstream applications and supporting oriented strand board market penetration in furniture clusters. On the regulatory side, OSB/1 demand wanes amid looming formaldehyde scrutiny, steering mill capital toward converting legacy production to higher-value structural grades.

The Oriented Strand Board Report is Segmented by Grade (OSB/1, OSB/2, OSB/3, and OSB/4), End-User Application (Construction, Furniture, and Packaging), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Cubic Meters).

Geography Analysis

North America retained 60.05% oriented strand board market share in 2025 thanks to a deep installed mill base, integrated softwood supply, and builder familiarity with the product. The United States remains the world's largest importer at USD 1.9 billion, primarily sourcing from Canadian and Brazilian plants even while domestic mills modernize with AI-enabled dryers to lift uptime. Canada's export orientation continues, but high fiber costs have forced selective curtailments as illustrated by West Fraser's Fraser Lake shutdown, tightening regional supply, and underpinning pricing.

Asia-Pacific is the growth engine, expanding at a 6.23% CAGR through 2031 as China, India, and ASEAN economies fast-track urban rail, data-center, and mid-rise residential projects. Luli Group's commissioning of China's first Fine-OSB line marks a pivot from reliance on imports toward domestic integrated production that shortens lead times and customizes grades for local codes. India's Smart City program lifts engineered panel adoption, where cost and speed edge out solid timber. Southeast Asian demand rises on tourism-driven hospitality builds, though local capacity lags, opening import lanes for North American and Chilean suppliers.

Europe shows steady but lower growth as stringent climate regulations lock in wood-favoring policies yet mature housing stock tempers volume upside. The EU-wide 2026 formaldehyde limit will likely displace non-compliant suppliers, increasing opportunities for mills already using MDI systems. Southern Europe's renovation credits and Northern Europe's prefab exports provide incremental tailwinds, keeping the oriented strand board market defensible against CLT incursion.

- Arbec Forest Products Inc.

- Besgrade Plywood Sdn. Bhd.

- Coillte

- EGGER

- J.M. Huber Corporation

- Koch IP Holdings, LLC

- Koyuncuoglu Group of Companies

- Kronoplus Limited

- Louisiana-Pacific Corporation

- RoyOMartin

- Sonae Arauco

- STRANDPLYOSB

- Swiss Krono Group

- Tolko Industries Ltd.

- West Fraser

- Weyerhaeuser Company

- Yalong Wood

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective substitution for plywood

- 4.2.2 Expansion of global construction activity

- 4.2.3 Sustainability-driven demand for engineered wood

- 4.2.4 Modular and prefab housing boom

- 4.2.5 Emerging low-VOC MDI-bonded OSB grades

- 4.3 Market Restraints

- 4.3.1 Formaldehyde and VOC regulations tightening

- 4.3.2 Wood-fiber price volatility

- 4.3.3 CLT adoption stealing structural share

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 OSB/1

- 5.1.2 OSB/2

- 5.1.3 OSB/3

- 5.1.4 OSB/4

- 5.2 By End-user Application

- 5.2.1 Construction

- 5.2.1.1 Floor and Roof

- 5.2.1.2 Wall

- 5.2.1.3 Door

- 5.2.1.4 Column and Beam (Shuttering)

- 5.2.1.5 Staircase

- 5.2.1.6 Other Constructions

- 5.2.2 Furniture

- 5.2.2.1 Residential

- 5.2.2.2 Commercial

- 5.2.3 Packaging

- 5.2.3.1 Food and Beverage

- 5.2.3.2 Industrial

- 5.2.3.3 Pharmaceutical

- 5.2.3.4 Cosmetics

- 5.2.3.5 Other Packaging

- 5.2.1 Construction

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arbec Forest Products Inc.

- 6.4.2 Besgrade Plywood Sdn. Bhd.

- 6.4.3 Coillte

- 6.4.4 EGGER

- 6.4.5 J.M. Huber Corporation

- 6.4.6 Koch IP Holdings, LLC

- 6.4.7 Koyuncuoglu Group of Companies

- 6.4.8 Kronoplus Limited

- 6.4.9 Louisiana-Pacific Corporation

- 6.4.10 RoyOMartin

- 6.4.11 Sonae Arauco

- 6.4.12 STRANDPLYOSB

- 6.4.13 Swiss Krono Group

- 6.4.14 Tolko Industries Ltd.

- 6.4.15 West Fraser

- 6.4.16 Weyerhaeuser Company

- 6.4.17 Yalong Wood

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment