|

시장보고서

상품코드

1940707

표면 실장 기술 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Surface Mount Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

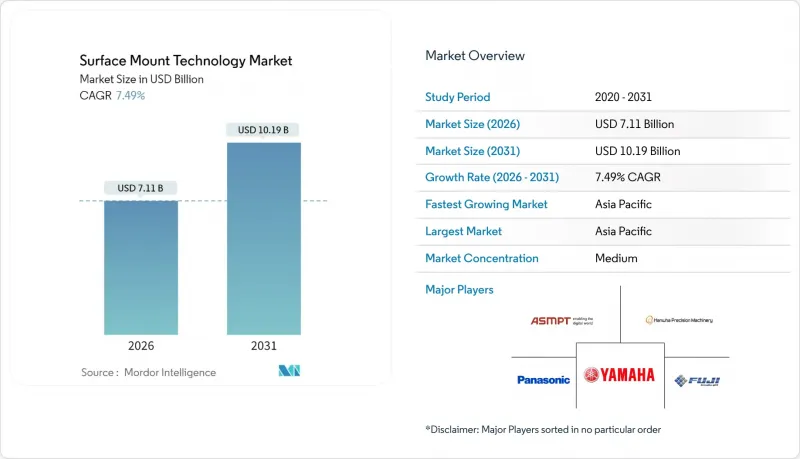

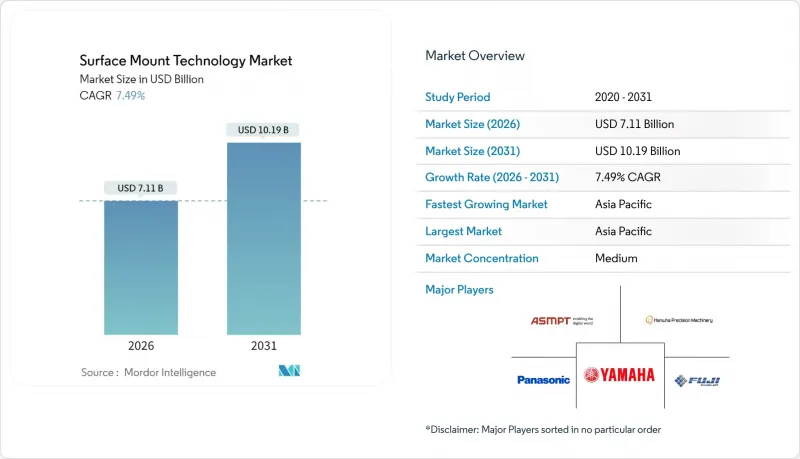

표면 실장 기술(SMT) 시장은 2025년에 66억 1,000만 달러로 평가되었으며, 2026년 71억 1,000만 달러에서 2031년까지 101억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 7.49%로 예상됩니다.

이러한 성장 궤도를 뒷받침하는 것은 민생기기, 전기자동차, 산업 자동화에서 소형화, 고밀도화되는 전자기기에 대한 수요입니다. 5G 인프라의 빠른 확산, 인공지능 서버의 성장, 엣지 및 IoT 제품의 보급으로 아시아, 북미, 유럽 전역의 생산 라인은 거의 풀가동 상태를 유지하고 있습니다. 자동차 제조업체들은 현재 -40℃에서 150℃의 온도 변화를 견딜 수 있는 자동차 등급 SMT 솔루션을 요구하고 있으며, 이로 인해 장비 요구사항이 더욱 엄격해지고 있습니다. 한편, 마이크로 LED와 시스템 인 패키지(SiP)의 혁신으로 인해 실장 정밀도에 대한 요구는 ±25μm에서 10μm 미만의 영역으로 이동하고 있습니다. 반도체와 고정밀 세라믹을 중심으로 한 공급망의 불안정성은 최종 시장의 건전한 기반에도 불구하고 단기적인 생산량의 주요 제약요인으로 작용하고 있습니다.

세계 표면 실장 기술(SMT) 시장 동향 및 인사이트

IoT 및 웨어러블 기기, 초 고밀도 PCB 채택을 촉진하다

현재 디바이스 제조업체들은 단일 스마트워치에 1만 개 이상의 적층 세라믹 커패시터를 탑재하고 있으며, 이는 5년 전의 3배에 달하는 수치입니다. 50µ&m 미만의 전도성 트레이스와 75µm 미만의 마이크로 비아를 인쇄하기 위해 어셈블리에서는 01005 패키지를 ±25µ&m의 정확도로 안정적으로 처리할 수 있는 배치 도구에 의존하고 있습니다. FCC의 방사능 제한 및 IEC의 안전 요건 준수에 따라 전자기 간섭(EMI) 차폐 대책이 더욱 강화되어 정밀 솔더 페이스트 검사 및 자동 광학 검사 시스템(AOI)에 대한 수요가 증가하고 있습니다.

자동차 ADAS 전자장치 채택으로 신뢰성 요건 재구축

전기자동차의 레퍼런스 디자인에는 대당 1만개 이상의 MLCC와 200개 이상의 전자제어유닛(ECU)이 사용되며, 수명주기 인증이 3년 이상에 달하고, SMT 수량이 증가하고 있습니다. ISO 26262 기능 안전 표준의 의무화와 -40°C에서 150°C까지의 작동 온도 범위로 인해 공급업체는 자동차 PPAP 및 AEC-Q200 스트레스 테스트에 기반한 프로세스 인증을 요구받고 있습니다. 솔더 조인트의 장기적인 신뢰성을 검증할 수 있는 장비 제조업체는 유럽과 일본에서 다년간의 공급 계약을 체결하고 있습니다.

높은 초기 설비투자비용이 중소기업의 장벽으로 작용하다

차세대 실장 플랫폼은 인라인 SPI, AOI, X-Ray 검사 장비를 합치면 라인당 300만 달러 이상입니다. 예지보전 분석은 총소유비용을 절감할 수 있지만, 많은 중소 EMS 제공업체들은 3년 이내에 투자 회수를 정당화하는 데 어려움을 겪고 있습니다. 장비 렌탈이나 성과 연동형 서비스 계약이 등장하고 있지만, Tier 1 OEM을 제외하고는 아직 일반적이지 않습니다.

부문 분석

액티브 부품은 2025년 표면 실장 기술(SMT) 시장 점유율의 65.74%를 차지했습니다. 이는 AI 서버 및 전기자동차용 MCU, ASIC, 전원 관리 부품에 대한 수요가 가속화되었기 때문입니다. 이종 SoC 설계와 고전압 트랜지스터의 채택 확대에 힘입어 이 부문은 2031년까지 CAGR 8.62%로 성장할 것으로 예상됩니다. 수동 부품은 5G 단말기와 차량용 트랙션 인버터의 부품 수 증가에 따른 수혜를 계속 누리고 있지만, 세라믹과 탄탈륨 소재의 부족으로 공급망의 회복력을 시험하는 상황이 계속되고 있습니다.

고객의 기대는 부품 비용 관리에서 기판 레벨의 집적도 및 장기 신뢰성으로 진화하고 있습니다. OEM 업체들은 10ppm 미만의 불량률과 15년의 필드 수명을 요구하고 있으며, 기판 벤더, 부품업체, 실장 장비 공급업체 간의 긴밀한 협력을 촉진하고 있습니다. 능동 및 수동 부품의 공동 설계 라이브러리와 완전한 조립 설계(DFA) 검토를 제공하는 공급업체는 신제품의 대량 생산을 가속화하고, 첨단 웨어러블 기기 및 산업용 IoT 게이트웨이의 우선 공급업체로 자리매김하고 있습니다.

2025년에도 실장 장비는 표면 실장 기술(SMT) 시장 규모의 42.62%를 차지했으며, 검사 장비가 CAGR 8.83%로 가장 빠르게 성장할 것으로 예상됩니다. 고속 픽앤플레이스 장치는 머신러닝 비전 시스템에 의한 헤드 압력 자동 조정으로 ±10㎛의 정밀도로 시간당 10만 개 처리를 실현했습니다. 납땜 장비는 무연 합금이 요구하는 엄격한 온도 구배로 인해 공정 창이 좁아지는 반면, 스크린 인쇄 플랫폼은 폐쇄 루프 SPI 피드백을 채택하여 초기 수율을 향상시킵니다.

투자 동향은 딥러닝을 활용하여 오판정률을 90% 감소시키고 검사 속도를 4배 향상시키는 AOI 및 X-Ray 시스템에 유리합니다. ViTrox와 Koh Young은 IPC-CFX 연결성을 통합하여 실시간 분석을 통해 수율을 떨어뜨리는 추세를 몇 분 안에 감지할 수 있습니다. 분석 구독을 번들로 제공하는 설비 금융 패키지는 높은 초기 비용 부담을 줄이고, 동유럽과 동남아시아의 Tier-2 EMS 기업들이 라인 업그레이드를 할 수 있도록 유도하고 있습니다.

지역별 분석

아시아태평양은 2025년 기준 표면 실장 기술(SMT) 시장의 48.05%를 차지하며 2031년까지 연평균 8.12%의 CAGR을 기록할 것으로 예상됩니다. 중국, 대만, 한국은 2027년까지 신규 300mm 팹에 총 840억 달러 이상을 투자하여 업스트림 공정의 기판 및 부품 생산능력을 확보할 것으로 예상됩니다. 일본 구마모토 클러스터는 TSMC JASM의 200억 달러 규모의 확장 계획을 중심으로월 10만장 이상의 12인치 웨이퍼 생산능력을 추가하는 동시에 3,400개의 첨단 기술 일자리를 창출할 예정입니다.

북미는 뒤쳐져 있지만, CHIPS 법에 따라 가속화되고 있으며, 이미 발표된 프로젝트를 통해 2024년 120억 달러에서 2027년까지 이 지역의 설비투자액이 2배로 증가할 것으로 예상됩니다. 애리조나 주와 뉴욕주의 첨단 패키징 시범 프로젝트는 AI 가속기를 위한 10μm 이하의 배치를 목표로 하고 있으며, 태평양 횡단 운송 경로에 대한 의존도를 낮추기 위해 노력하고 있습니다. 사이버 보안 대책이 강조되는 생산 흐름에 대한 규제가 강화됨에 따라, 공장은 CMMC 및 IPC-1791 인증의 신뢰할 수 있는 제조업체 인증을 획득하기 위해 노력하고 있습니다.

유럽에서는 자동차용 전력 반도체와 와이드밴드갭 디바이스에 집중하고 있으며, 인피니언과 ST마이크로일렉트로닉스가 800V EV 인버터 지원을 위한 설비투자를 추진하고 있습니다. 이 지역의 RoHS 확대 및 도입 예정인 에코 디자인 규정은 수리 가능한 PCB를 권장하고, 선택적 납땜 및 재작업 플랫폼에 대한 수요를 자극하고 있습니다. 유럽의 '기술 협약'에 기반한 인력 기술 향상 프로그램은 IPC 인증 상호연결 설계자 커리큘럼과 연계하여 2029년까지 14만 6,000명의 인력 부족 해소를 목표로 하고 있습니다.

중동 및 아프리카에서는 사우디아라비아와 아랍에미레이트가 EMS 특혜와 공공요금 할인을 결합한 기술단지에 주권기금 자본을 투입하여 점진적인 진전을 보이고 있습니다. 남아프리카공화국 하우텡 주에 위치한 이 공장은 단납기 및 다품종 수리 주문에 대응할 수 있는 모듈식 SMT 라인을 필요로 하는 통신장비 재생업체를 유치하고 있습니다. 그러나 인프라 부족과 전문 인력 부족으로 인해 사하라 이남 대부분의 시장에서 첨단 장비의 도입이 제한되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The Surface Mount Technology market was valued at USD 6.61 billion in 2025 and estimated to grow from USD 7.11 billion in 2026 to reach USD 10.19 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

Demand for miniaturized, high-density electronics in consumer devices, electric vehicles, and industrial automation is underpinning this trajectory. Accelerated deployment of 5 G infrastructure, growth in artificial-intelligence servers, and the spread of edge and IoT products are keeping production lines close to full capacity across Asia, North America, and Europe. Automotive original-equipment manufacturers now specify automotive-grade SMT solutions able to tolerate -40 °C to 150 °C thermal swings, further tightening equipment requirements. Meanwhile, micro-LED and System-in-Package (SiP) innovations are shifting placement accuracy expectations from +-25 µm toward the sub-10 µm realm. Supply-chain volatility, especially for semiconductors and high-precision ceramics, remains the primary brake on near-term throughput despite healthy end-market fundamentals.

Global Surface Mount Technology Market Trends and Insights

IoT and Wearables Fuel Ultra-Dense PCB Adoption

Device makers now pack more than 10,000 multilayer ceramic capacitors into a single smartwatch, tripling the count seen five years ago. To print conductive traces below 50 µm and microvias under 75 µm, assemblies rely on placement tools that consistently handle 01005 packages at +-25 µm accuracy. Compliance with FCC emissions limits and IEC safety requirements is pushing additional electromagnetic-interference shielding steps, elevating demand for precision solder-paste inspection and automated optical inspection systems.

Automotive ADAS Electronics Adoption Reshapes Reliability Needs

Electric-vehicle reference designs use upward of 10,000 MLCCs and more than 200 electronic control units each, lifting SMT volumes even as lifecycle qualification stretches beyond three years. ISO 26262 functional-safety mandates and -40 °C to 150 °C operating windows compel suppliers to certify processes under automotive PPAP and AEC-Q200 stress tests. Equipment makers that can validate long-term solder-joint reliability are winning multiyear supply agreements across Europe and Japan.

High Upfront Capex Constrains Smaller Firms

Next-generation placement platforms cost upward of USD 3 million per line when bundled with in-line SPI, AOI, and x-ray testers. Although predictive-maintenance analytics lower total cost of ownership, many small and medium EMS providers struggle to justify payback within three years. Equipment rental and outcome-based service contracts are emerging but remain uncommon outside Tier-1 OEMs.

Other drivers and restraints analyzed in the detailed report include:

- 5G Infrastructure and High-Frequency Boards

- System-in-Package Integration in Smartphones

- Lead-Free Solder Thermal Constraints Lower Yield

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active Components accounted for 65.74% of the Surface Mount Technology market share in 2025 as MCU, ASIC, and power-management demand accelerated in AI servers and electric vehicles. The segment is forecast to grow at an 8.62% CAGR to 2031 on the back of increased adoption of heterogenous SoC designs and high-voltage transistors. Passive Components still benefit from rising unit counts in 5G handsets and automotive traction inverters, but ceramic and tantalum material shortages continue to test supply-chain resiliency.

Customer expectations are evolving from component cost control to board-level integration density and long-tail reliability. OEMs request sub-10 ppm failure rates and 15-year field lifetimes, driving closer collaboration between substrate vendors, component makers, and placement-equipment suppliers. Suppliers that deliver active-passive co-design libraries and full Design-for-Assembly review accelerate new-product ramps, securing supplier-of-choice status for advanced wearables and industrial IoT gateways.

Placement Equipment still commands 42.62% of the Surface Mount Technology market size in 2025, but Inspection Equipment is rising fastest with a 8.83% CAGR. High-speed pick-and-place machines now hit 100 k cph with +-10 µm accuracy, aided by machine-learning vision systems that auto-tune head pressure. Soldering Equipment faces process-window squeezes as lead-free alloys demand tighter thermal gradients, while Screen-Printing platforms adopt closed-loop SPI feedback to boost first-pass yield.

Investment momentum favors AOI and x-ray systems that harness deep learning to cut false-call rates by 90 % and raise inspection speed four-fold. ViTrox and Koh Young incorporate IPC-CFX connectivity for real-time analytics that flag yield-eroding trends within minutes. Equipment finance packages bundling analytics subscriptions help offset sticker shock, enticing Tier-2 EMS firms in Eastern Europe and Southeast Asia to upgrade lines.

The Surface Mount Technology Market Report is Segmented by Component (Passive Components [Resistors, Capacitors], and More), Equipment Type (Placement Equipment [High-Speed Pick-And-Place Machines], and More), Assembly Line Type (High-Mix/Low-Volume, and More), End-User Industry (Consumer Electronics, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 48.05% Surface Mount Technology market share in 2025 and is forecast to post an 8.12% CAGR through 2031. China, Taiwan, and South Korea together are slated to invest more than USD 84 billion in new 300 mm fabs by 2027, securing upstream substrate and component capacity. Japan's Kumamoto cluster, anchored by TSMC JASM's USD 20 billion expansion, adds over 100,000 12-inch wafers per month while creating 3,400 high-tech roles.

North America trails but is accelerating under the CHIPS Act, with announced projects doubling regional capacity investment from USD 12 billion in 2024 to USD 24.7 billion by 2027. Advanced packaging pilots in Arizona and New York target sub-10 µm placement for AI accelerators, reducing dependence on trans-Pacific shipping lanes. Regulatory emphasis on cyber-secure production flows nudges factories toward CMMC and IPC-1791 trusted builder accreditation.

Europe focuses on automotive power semiconductors and wide-band-gap devices, with Infineon and STMicroelectronics driving capital expenditure to support 800 V EV inverters. The region's RoHS expansion and incoming Ecodesign rules favor repairable PCBs, stimulating demand for selective soldering and rework platforms. Workforce upskilling programs under Europe's Pact for Skills align with IPC's certified interconnect designer curriculum, aiming to close a 146,000-worker gap by 2029.

Middle East and Africa makes incremental gains as Saudi Arabia and the UAE funnel sovereign-fund capital into tech parks that bundle EMS incentives with reduced utility tariffs. South Africa's Gauteng hub attracts telecom-equipment refurbishers that rely on modular SMT lines to process short-run, high-mix repair orders. Still, infrastructure gaps and limited specialist labor temper adoption of cutting-edge equipment in most sub-Saharan markets.

- ASMPT Limited

- Fuji Corporation

- Yamaha Motor Co., Ltd. (SMT Division)

- Panasonic Holdings Corporation (Panasonic Smart Factory Solutions)

- Hanwha Precision Machinery Co., Ltd.

- Mycronic AB

- Juki Corporation

- Nordson Corporation

- Koh Young Technology Inc.

- Saki Corporation

- Test Research, Inc. (TRI)

- Viscom SE

- Europlacer Holdings Ltd.

- Shenzhen JT Automation Equipment Co., Ltd.

- Rehm Thermal Systems GmbH

- Heller Industries, Inc.

- MIRTEC Co., Ltd.

- Shenzhen NEODEN Technology Co., Ltd.

- Shenzhen JAGUAR Automation Equipment Co., Ltd.

- Hanwa Precision Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT and wearables driving high-density PCB demand

- 4.2.2 Automotive ADAS electronics adoption

- 4.2.3 Expansion of 5G infrastructure and high-frequency boards

- 4.2.4 System-in-Package (SiP) integration in smartphones

- 4.2.5 MicroLED display manufacturing requirements

- 4.2.6 OEM outsourcing to EMS firms in emerging economies

- 4.3 Market Restraints

- 4.3.1 High upfront capex for high-speed placement lines

- 4.3.2 Lead-free solder thermal constraints lowering yield

- 4.3.3 Semiconductor supply-chain volatility causing under-utilisation

- 4.3.4 Skilled labour shortage for AI-driven inspection systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Trends Impact Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Passive Components

- 5.1.1.1 Resistors

- 5.1.1.2 Capacitors

- 5.1.2 Active Components

- 5.1.2.1 Transistors

- 5.1.2.2 Integrated Circuits

- 5.1.1 Passive Components

- 5.2 By Equipment Type

- 5.2.1 Placement Equipment

- 5.2.1.1 High-speed Pick-and-Place Machines

- 5.2.2 Soldering Equipment

- 5.2.2.1 Reflow Ovens

- 5.2.2.2 Wave Solder Systems

- 5.2.3 Inspection Equipment

- 5.2.3.1 Automated Optical Inspection (AOI)

- 5.2.3.2 Solder Paste Inspection (SPI)

- 5.2.3.3 X-ray Inspection

- 5.2.4 Screen Printing Equipment

- 5.2.1 Placement Equipment

- 5.3 By Assembly Line Type

- 5.3.1 High-Mix / Low-Volume (HMLV)

- 5.3.2 High-Volume / High-Mix (HVHM)

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Industrial Electronics

- 5.4.4 Aerospace and Defense

- 5.4.5 Healthcare

- 5.4.6 Telecom and IT Infrastructure

- 5.4.7 Other End-users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ASMPT Limited

- 6.4.2 Fuji Corporation

- 6.4.3 Yamaha Motor Co., Ltd. (SMT Division)

- 6.4.4 Panasonic Holdings Corporation (Panasonic Smart Factory Solutions)

- 6.4.5 Hanwha Precision Machinery Co., Ltd.

- 6.4.6 Mycronic AB

- 6.4.7 Juki Corporation

- 6.4.8 Nordson Corporation

- 6.4.9 Koh Young Technology Inc.

- 6.4.10 Saki Corporation

- 6.4.11 Test Research, Inc. (TRI)

- 6.4.12 Viscom SE

- 6.4.13 Europlacer Holdings Ltd.

- 6.4.14 Shenzhen JT Automation Equipment Co., Ltd.

- 6.4.15 Rehm Thermal Systems GmbH

- 6.4.16 Heller Industries, Inc.

- 6.4.17 MIRTEC Co., Ltd.

- 6.4.18 Shenzhen NEODEN Technology Co., Ltd.

- 6.4.19 Shenzhen JAGUAR Automation Equipment Co., Ltd.

- 6.4.20 Hanwa Precision Machinery Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment