|

시장보고서

상품코드

2044196

라이너리스 라벨 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Linerless Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

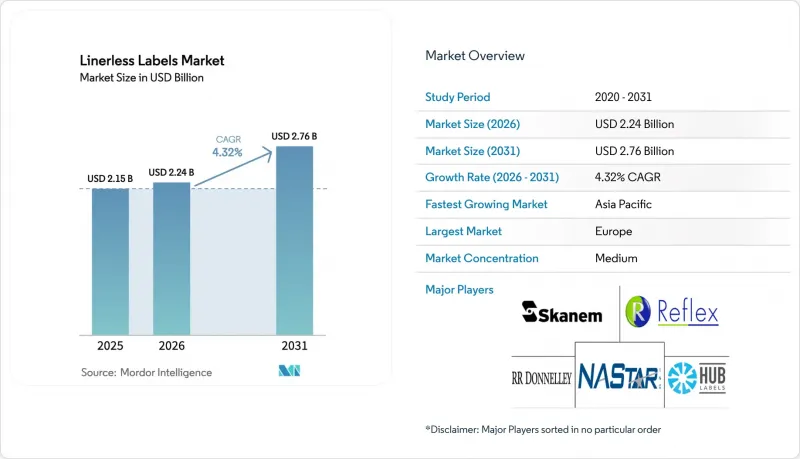

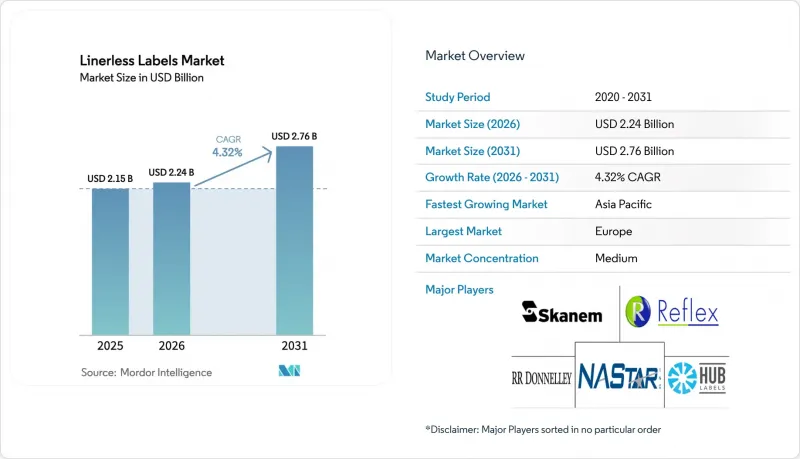

라이너리스 라벨 시장 규모는 2025년 21억 5,000만 달러, 2026년 22억 4,000만 달러에서 2031년까지 27억 6,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.32%를 나타낼 전망입니다.

포장 가공업체들은 라이너 폐기물에 대한 규제 비용이 수익률을 압박하고 있어 라이너리스 구조로의 전환을 추진하고 있습니다. 한편, 자동화된 EC 풀필먼트 라인에서는 스캐너에 이물질이 부착되지 않도록 연속적인 길이의 라벨이 필요합니다. 유럽은 폐기물 없는 형태를 장려하는 확대된 생산자책임재활용(EPR) 벌칙 제도 덕분에 여전히 시장의 중심지이지만, 아시아태평양은 국경 간 소포 운송과 퀵커머스의 다크스토어를 배경으로 가장 빠르게 성장하고 있습니다. 디지털 인쇄, 실리콘 프리 박리 코팅, RFID 임베디드 기판에 대한 투자가 가속화되고 있습니다. 이는 전환 시간을 단축하고 새로운 데이터 서비스를 구현할 수 있기 때문입니다. 수직계열화된 소재 대기업들이 핵심 배합을 지키고 있어 경쟁의 강도는 중간 정도에 머물러 있지만, 고가의 플 렉소 인쇄 자산을 폐기하고 싶지 않은 컨버터 업체들을 RETROFIT 전문 업체들이 적극적으로 끌어들이려고 하고 있습니다.

세계 라이너리스 라벨 시장 동향과 인사이트

식음료 포장에 대한 지속가능성 요구 사항 증가

입법자들은 사용 후 재료에 대해 브랜드 소유자가 금전적 책임을 지도록 하는 방향으로 나아가고 있으며, 라이너리스 라벨은 포장 중량을 30-40% 감소시켜 생산자책임재활용(EPR) 비용을 직접적으로 줄일 수 있습니다. 소매업체들은 2025년까지 라이너 폐기물 지표를 공급업체 평가 기준에 포함시켜 압력을 가하고 있으며, 그 결과 신선식품 및 조리식품 생산업체들이 재고 이익을 보호하기 위해 가장 빠르게 대응하고 있습니다. 이와 함께, 개정된 EU의 포장 및 포장 폐기물 규정은 재활용률 기준치를 부과하고, 위반 시 1kg당 최대 0.80유로(1kg당 0.90달러)의 벌금을 부과하여 조달을 제로 폐기물 형태로 전환하도록 유도하고 있습니다. 'Science Based Targets'에 대한 의지를 표명한 다국적 기업들은 현재 라이너리스화를 Scope 3 배출량 감축 수단으로 인식하고 경영진 차원에서 시급성을 강조하고 있습니다. 소재 업체들은 기존 소매점 분리수거 시스템과 호환성이 입증된 재생지 및 폴리머 기재를 제공함으로써 이에 대응하고 있으며, 도입 주기가 빨라지고 있습니다.

전자상거래 물류의 급격한 성장으로 가변 길이 배송 라벨에 대한 수요가 증가하고 있습니다.

2025년 전 세계 소포 처리량은 전년 대비 22% 증가해, 풀필먼트 업체들은 라이너리스 프린터가 라벨 재료 비용을 최대 25% 절감하고 자동 분류 라인의 병목 현상이었던 박리 공정을 제거할 수 있다는 사실을 발견했습니다. 아마존, 알리바바, 인도의 Blinkit은 현재 배송, 반품, 통관 라벨에 라이너리스(linerless)를 표준으로 채택하여 이전에는 라이너 폐기물 컨테이너를 위해 확보했던 창고 공간의 50%를 확보했습니다. 가변 데이터 필드를 확장하여 통관 코드와 반송 주소를 포함할 수 있기 때문에 과거 국경 간 소포에서 흔히 볼 수 있었던 3겹의 라벨을 1장의 라벨로 대체할 수 있습니다. 소포 운송업체들도 고속 슈트에 미끄러운 라이너가 없다는 점을 높이 평가하고 있으며, 이로 인해 보험료를 절감할 수 있게 되었습니다. 마이크로 풀필먼트 센터의 로봇 기술 보급과 함께 연속 라벨은 자율 인쇄 및 부착 모듈에서 롤 처리를 단순화하기 때문에 라이너리스 라벨 시장은 자동화 로드맵에 밀접하게 통합되어 있습니다.

레거시 라벨링 라인 개조 비용

10색 플 렉소 인쇄기를 라이너리스 웹에 대응하기 위한 업그레이드 비용은 일반적으로 장력 제어, 실리콘 프리 박리 코팅 장치 및 재설계된 언와인더 시스템을 포함하여 미화 150,000-400,000달러가 소요됩니다. EBITDA 마진이 10% 미만인 중소형 컨버터는 투자 회수 기간이 4년을 초과하기 때문에 이사회 승인이 지연되고 있습니다. 인쇄기 제조업체의 리스 플랜은 진입장벽을 낮추기 위한 것이지만, 식료품 라벨 등을 취급하는 가장 큰 규모의 공장이라도 18개월 이내에 손익분기점에 도달하는 것은 어렵습니다. 라이너리스 웹은 닙 압력에 대한 반응이 다르기 때문에 작업자에게 새로운 기술이 필요하며, 직원 재교육이 또 다른 장벽으로 작용합니다. 개조 키트의 가격이 5만 달러 이하로 떨어지거나 재료비 절감 효과가 확대되지 않는 한, 이러한 제약은 단기적으로 도입률을 억제할 것입니다.

부문 분석

2025년, 플렉소 인쇄기는 라이너리스 라벨 시장 점유율의 40.43%를 차지했습니다. 이는 음료 및 가정용 화학제품 분야의 롱로트 프로젝트에서 여전히 판가 경제성이 중요시되고 있기 때문입니다. 그러나 의약품 직렬화, 틈새 SKU, 온디맨드 EC 워크플로우에서는 로트 수보다 가변 데이터가 우선시되기 때문에 디지털 플랫폼은 2031년까지 5.43%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 디지털 헤드의 수명은 2024년 모델보다 30% 더 길어졌고, 손익분기점은 약 8,000리니어미터로 낮아졌습니다. 열전사 장치는 1초 미만의 사이클 타임으로 300dpi의 선명한 바코드를 필요로 하는 배송 라벨에서 아마존과 DHL의 허브에서 열전사 유닛이 주류가 되고 있습니다. 스위스의 식품 접촉 규정을 충족하는 수성 잉크 등 잉크젯 기술의 발전으로 기존 솔벤트 기반 시스템으로는 진입할 수 없었던 델리 및 청과물 라인에 진출할 수 있게 되었습니다.

컨버터 업체들은 플 렉소 인쇄기가 핵심 로트를 처리하고 디지털 스테이션이 최종 단계의 커스터마이징을 담당하는 하이브리드 인쇄실을 구축하여 가동률 평준화와 재고 감소를 꾀하고 있습니다. 25만 달러 미만의 가격대인 리트로핏 키트를 이용하면 기존 언와인드 섹션에 디지털 헤드를 장착할 수 있어, 인쇄기의 전면 교체를 피하고 ROI를 가속화할 수 있습니다. 클라우드 상의 작업 티켓이 라벨의 길이와 그래픽을 자동으로 조정하기 때문에 작업자는 전환 시간을 몇 분으로 단축할 수 있어 계절적 수요가 급증할 때 생산 능력을 확보할 수 있습니다. 이러한 운영상의 이점이 구조적 변화를 촉진하고, 예측 기간 동안 인쇄 기술의 구성 비율이 꾸준히 디지털로 전환될 것으로 예측됩니다.

2025년에는 냉장 운송 중 습기에 강한 폴리프로필렌과 폴리에틸렌에 힘입어 필름 기판이 48.23%의 시장 점유율을 차지했습니다. 브랜드가 재활용 소재의 최소 사용률을 약속하고 규제 당국이 인증된 재활용 소재에 대한 수수료 환급을 제공함에 따라 특수 등급 및 재활용 등급은 현재 CAGR 5.72%로 성장을 지속하고, 있습니다. UPM의 RafCycle 네트워크는 2024년 8,400톤의 폐기물을 회수하여 재생지 라이너 및 PET 필름 코어로 전환함으로써 상업적 규모의 실용성을 입증했습니다. 30-50%의 소비 후 수지를 함유한 재생 PET 페이스 스톡은 음료 멀티팩 선반을 휩쓸고 있으며, 코카콜라, 펩시콜라, 펩시콜라 등이 순환형 아이콘을 내걸고 있습니다. 폴리락산을 기반으로 한 신흥 바이오폴리머 필름은 퇴비화 가능성을 표방하고 있지만, 인장강도의 한계로 인해 저부하의 델리카트슨용 뚜껑 등으로 제한되어 있습니다.

재활용 설계 지침을 채택한 브랜드 소유자는 현재 각 지역에 따라 기재를 지정하고, 장벽 성능 요구 사항과 현지 회수 인프라의 균형을 맞추고 있습니다. 이러한 SKU 증가로 인해 컨버터는 재고를 확대할 수밖에 없었고, 이에 따라 많은 기업들이 3분 이내에 코어를 교체할 수 있는 적시 라미네이팅 라인을 채택하고 있습니다. 폐기된 표면재를 다음 생산 로트의 원료로 재사용하는 폐쇄형 회수 방식은 소매업체 평가 기준에서 조달 점수를 획득하여 재생 필름의 주문량을 늘리고 있습니다. 탄소발자국 대시보드가 공급업체 포털에 도입됨에 따라 수요는 더욱 가속화될 것이며, 재생 및 특수 표면 소재는 가장 빠르게 성장하는 소재 카테고리로 자리 잡을 것으로 예측됩니다.

"라이너리스 라벨 시장 보고서는 인쇄 기술(디지털, 플 렉소, 그라비아 등), 페이스트 스톡 소재(종이, 필름, 특수 및 재생 기판), 접착제 유형(아크릴, 핫멜트, 특수 등), 최종 사용자 산업(식품, 음료, 헬스케어, 화장품, 가정용 화학, 물류 등), 지역별로 분류되어 있습니다. 등) 및 지역별로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

유럽은 2025년 38.82%의 점유율을 차지했으며, 폐기물 감축 의무화, 라이너리스 프린터와 포장 감사가 결합된 슈퍼마켓과의 제휴가 이를 뒷받침하고 있습니다. 독일과 프랑스에서는 플라스틱 저감 목표 달성을 위한 즉각적인 조치로 라이너 폐지를 법제화하여 컨버터는 프리미엄 가격으로 장기 계약을 체결하고 있습니다. 베네룩스 지역에서는 패션 제품 반품을 위해 RFID가 내장된 라이너리스 라벨을 도입하여 국경 간 데이터 추적에 중점을 둔 규제 당국의 기대에 부응하고 있습니다.

아시아태평양은 인도, 인도네시아, 베트남의 소포 취급량이 25% 이상 증가하는 인도, 인도네시아, 베트남에 힘입어 CAGR 6.04%로 가장 강력한 성장세를 보이고 있습니다. Cainiao와 JD Logistics는 도시 쓰레기 처리 비용이 톤당 300위안(42달러)을 초과하는 중국 주요 도시에서 라이너리스 생산라인을 운영하고 있으며, 라이너 폐기 비용이 엄청나게 비싸기 때문입니다. 일본과 한국에서는 일련번호가 부여된 의약품과 소매업의 RFID 셀프 체크아웃과 같은 선진적인 이용 사례를 볼 수 있으며, 성숙한 시장에서도 기술의 축적에 따라 여전히 성장의 여지가 있음을 증명하고 있습니다. 동남아시아의 퀵커머스 창고는 라이너리스 롤을 통해 50%의 저장 공간을 절약할 수 있으며, 이는 임대료가 높은 도심의 허브에서 매우 중요합니다.

북미는 유럽에 비해 점유율에서 뒤쳐져 있지만, 2025년 아마존의 풀필먼트 생태계가 52억 개의 소포를 처리하고, 입출고 라벨에 라이너리스(linerless)를 표준화한 만큼 여전히 중요한 위치를 차지하고 있습니다. 캘리포니아의 SB 54 법에 따라 폐기물 처리 비용이 전국 브랜드의 주요 위험 요소로 떠오르면서 중서부 지역의 컨버터들은 콜드체인 순환을 견딜 수 있는 아크릴 시스템으로 전환해야 하는 상황에 처해 있습니다. 남미에서는 메르카도 리브레가 브라질의 허브에서 라이너리스 라벨을 시범 도입하고 있어 소규모 기반에서 성장이 예상됩니다. 그러나 높은 자본 비용과 제한된 리노베이션 서비스로 인해 더 광범위한 보급을 가로막고 있습니다. 아랍에미리트와 사우디아라비아가 주도하는 중동 및 아프리카에서는 냉장 식품 수입에 대한 투자가 진행되고 있으며, 45℃의 부두 열과 4℃의 물류센터 열을 모두 견딜 수 있는 라벨이 요구되고 있습니다. 이러한 지역적 추세는 라이너리스 라벨 시장의 지속적인 다양화를 보장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The linerless labels market size is projected to expand from USD 2.15 billion in 2025 and USD 2.24 billion in 2026 to USD 2.76 billion by 2031, registering a CAGR of 4.32% between 2026 to 2031. Packaging converters are pivoting to linerless construction because regulatory fees on liner waste are tightening margins, while automated e-commerce fulfillment lines need continuous-length labels that keep scanners clear of debris. Europe remains the commercial anchor thanks to Extended Producer Responsibility penalties that reward waste-free formats, but Asia-Pacific is scaling fastest on the back of cross-border parcel traffic and quick-commerce dark stores. Investments in digital printing, silicone-free release coatings, and RFID-embedded substrates are accelerating because they shrink changeover time and unlock new data services. Competitive intensity is moderate as vertically integrated material giants defend core formulations, even as retrofit specialists court converters unwilling to scrap high-value flexographic assets.

Global Linerless Labels Market Trends and Insights

Rising Sustainability Mandates in Food and Beverage Packaging

Legislators are making brand owners financially responsible for post-use materials, and linerless labels slash packaging mass 30-40%, directly lowering Extended Producer Responsibility fees. Retailers intensified the pressure in 2025 by integrating liner-waste metrics into supplier scorecards, so producers of fresh produce and prepared meals moved quickest to defend shelf margins. In parallel the updated EU Packaging and Packaging Waste Regulation imposes recycling-rate thresholds with penalties up to EUR 0.80 per kg (USD 0.90 per kg) for non-compliance, tilting procurement toward waste-free formats. Multinationals that committed to Science Based Targets now cite linerless conversion as a Scope 3 emission lever, reinforcing board-level urgency. Material vendors are answering with recycled paper and polymer substrates that prove compatibility with existing retail sort streams, so adoption cycles are accelerating.

E-Commerce Logistics Boom Requiring Variable-Length Shipping Labels

Global parcel volumes jumped 22% year over year in 2025, and fulfillment operators discovered that linerless printers cut label material costs by up to 25% and remove a peel-step that bottlenecks automated sortation lines. Amazon, Alibaba and India's Blinkit now treat linerless as default for shipping, returns and customs labels, freeing 50% warehouse space previously reserved for liner waste bins. Because variable-data fields can stretch to cover customs codes and return addresses, one label replaces the three-label stacks once common on cross-border packages. Parcel carriers also value the absence of slip-hazard liners on high-speed chutes, shaving insurance premiums. As robotics proliferate in micro-fulfillment centers, the continuous stock simplifies roll handling for autonomous print-and-apply modules, so the linerless labels market is woven tightly into the automation roadmap.

Retrofit Costs for Legacy Labeling Lines

Upgrading a 10-color flexographic press to handle linerless webs typically costs USD 150,000-400,000 once tension-control, silicone-free release coaters and re-engineered unwind systems are included. Small and mid-sized converters running sub-10% EBITDA margins see payback horizons stretch beyond four years, so board approvals stall. Leasing packages from press makers aim to lower the barrier, yet only the highest-volume plants, such as those serving grocery labels, cross the break-even threshold inside 18 months. Staff retraining compounds the hurdle because linerless webs respond differently to nip pressure, so operators need new skill sets. Until retrofit kits drop below USD 50,000 or material savings widen, this restraint will temper near-term conversion rates.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Waste-Reduction Mandates in Europe and North America

- RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- Raw-Material Price Volatility in Adhesives and Release Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexographic presses secured 40.43% of the linerless labels market share in 2025 because long-run jobs in beverage and household chemicals still favor plate economies. Yet digital platforms are forecast to post a 5.43% CAGR to 2031 as pharmaceutical serialization, boutique SKUs and on-demand e-commerce workflows prioritize variable data over run length. Digital heads now last 30% longer than 2024 models, nudging break-even points down to about 8,000 linear meters. Thermal transfer units dominate Amazon and DHL hubs for shipping labels that need crisp 300-dpi barcodes in sub-second cycle times. Inkjet advances such as water-based formulations that satisfy Swiss food-contact ordinances unlock entry to deli and produce lines previously closed to solvent systems.

Converters are building hybrid pressrooms where flexo engines handle anchor runs while digital stations execute late-stage customization, smoothing utilization and shrinking inventory. Retrofit kits priced below USD 250,000 let plants bolt digital heads onto existing unwind sections, sidestepping a full press replacement and accelerating ROI. As cloud job tickets auto-scale label length and graphics, operators cut changeovers to minutes, freeing capacity during seasonal demand spikes. These operational gains reinforce the structural shift, ensuring the printing-technology mix tilts steadily toward digital over the forecast horizon.

Film substrates delivered 48.23% market share in 2025, driven by polypropylene and polyethylene that resist moisture during chilled transit. Specialty and recycled grades are now clocking a 5.72% CAGR because brands pledge minimum recycled content and regulators grant fee rebates for certified circular materials. UPM's RafCycle network reclaimed 8,400 t of waste in 2024 and channels it into recycled paper liners and PET film cores, proving commercial scale. Recycled PET facestocks with 30-50% post-consumer resin grabbed shelf space on beverage multipacks, where Coca-Cola and PepsiCo showcase circular icons. Emerging biopolymer films based on polylactic acid offer compostability credentials, though tensile limits confine them to low-stress deli lids.

Brand owners adopting design-for-recycling guidelines now specify tailored substrates for each region, balancing barrier needs with local recovery infrastructure. This proliferation of SKUs forces converters to widen inventory, so many turn to just-in-time lamination lines that swap cores in under three minutes. Closed-loop take-back schemes, where waste facestock feeds the next production batch, are winning procurement points in retailer scorecards and lifting order volumes for recycled films. As carbon-footprint dashboards reach supplier portals, demand momentum is set to intensify, cementing recycled and specialty facestocks as the fastest expanding material tier.

The Linerless Labels Market Report is Segmented by Printing Technology (Digital, Flexographic, Gravure, and More), Facestock Material (Paper, Film, and Specialty and Recycled Substrates), Adhesive Type (Acrylic, Hot-Melt, Specialty, and More), End-User Industry (Food, Beverage, Healthcare, Cosmetics, Household Chemicals, Logistics, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Geography Analysis

Europe generated 38.82% of share in 2025, underpinned by mandatory waste-reduction fees and supermarket alliances that bundle linerless printers with packaging audits. Germany and France legislate liner elimination as a quick win in hitting plastics reduction milestones, so converters secure long-term contracts at premium pricing. The Benelux region pioneers RFID-embedded linerless labels for fashion returns, pleasing regulators focused on cross-border data tracking.

Asia-Pacific exhibits the strongest trajectory with a 6.04% CAGR forecast, propelled by India, Indonesia and Vietnam where parcel volumes are compounding above 25%. Cainiao and JD Logistics rolled out linerless lines in Tier 1 Chinese cities where municipal waste fees top CNY 300 t-1 (USD 42 t-1), making liner disposal cost prohibitive. Japan and South Korea showcase advanced use cases in serialized pharma and RFID self-checkout retail, proving that mature markets still generate upside through technology stacking. Southeast Asian quick-commerce warehouses capitalize on the 50% storage-space gain from linerless rolls, vital in high-rent urban hubs.

North America trails Europe on share but remains pivotal because the Amazon fulfilment ecosystem processed 5.2 billion parcels in 2025 and has standardized linerless for inbound and outbound labels. California's SB 54 turns waste fees into headline risks for national brands, nudging Midwest converters toward acrylic systems that survive cold-chain loops. South America grows from a smaller base as Mercado Libre tests linerless in Brazilian hubs; high capital costs and limited retrofit services check broader rollout. The Middle East and Africa, led by the United Arab Emirates and Saudi Arabia, invest in refrigerated food imports, demanding labels that survive both 45 °C quayside heat and 4 °C distribution centers. Collectively, these regional vectors ensure sustained diversification in the linerless labels market.

List of Companies Covered in this Report:

- Avery Dennison Corporation

- CCL Industries Inc. and Innovia Films

- 3M Company

- Beontag

- UPM Raflatac

- Coveris

- Hub Labels Inc.

- Reflex Labels Ltd

- Skanem AS

- NAStar Inc.

- Optimum Group

- SATO Europe GmbH

- ProPrint Group

- Lexit Group AS

- R.R. Donnelley and Sons Company

- Gipako UAB

- Lintec Corporation

- HERMA GmbH

- Zebra Technologies Corporation

- Multi-Color Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Sustainability Mandates in Food and Beverage Packaging

- 4.2.2 E-commerce Logistics Boom Requiring Variable-Length Shipping Labels

- 4.2.3 Regulatory Waste-Reduction Mandates in Europe and North America

- 4.2.4 Quick-Service Restaurant Kitchen Automation Driving On-Demand Linerless Printing

- 4.2.5 RFID-Enabled Connected Packaging and Micro-Fulfillment Adoption

- 4.2.6 Carbon Border Adjustment Mechanisms Elevating Demand for Low-Waste Labeling

- 4.3 Market Restraints

- 4.3.1 Retrofit Costs for Legacy Labeling Lines

- 4.3.2 Raw-Material Price Volatility in Adhesives and Release Coatings

- 4.3.3 Adhesive Build-Up Issues in Cold-Chain Environments

- 4.3.4 Shortage of High-Performance Silicone-Free Adhesives

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Digital (Inkjet and Thermal)

- 5.1.2 Flexographic

- 5.1.3 Gravure

- 5.1.4 Other Printing Technologies

- 5.2 By Facestock Material

- 5.2.1 Paper

- 5.2.2 Film (PP, PET, PE)

- 5.2.3 Specialty and Recycled Substrates

- 5.3 By Adhesive Type

- 5.3.1 Acrylic Adhesives

- 5.3.2 Hot-Melt Adhesives

- 5.3.3 Specialty Adhesives

- 5.3.4 Other Adhesive Types

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Household Chemicals

- 5.4.6 Logistics and E-commerce

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Australia

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc. and Innovia Films

- 6.4.3 3M Company

- 6.4.4 Beontag

- 6.4.5 UPM Raflatac

- 6.4.6 Coveris

- 6.4.7 Hub Labels Inc.

- 6.4.8 Reflex Labels Ltd

- 6.4.9 Skanem AS

- 6.4.10 NAStar Inc.

- 6.4.11 Optimum Group

- 6.4.12 SATO Europe GmbH

- 6.4.13 ProPrint Group

- 6.4.14 Lexit Group AS

- 6.4.15 R.R. Donnelley and Sons Company

- 6.4.16 Gipako UAB

- 6.4.17 Lintec Corporation

- 6.4.18 HERMA GmbH

- 6.4.19 Zebra Technologies Corporation

- 6.4.20 Multi-Color Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment