|

시장보고서

상품코드

1687365

세계의 니들 코크스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Needle Coke - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

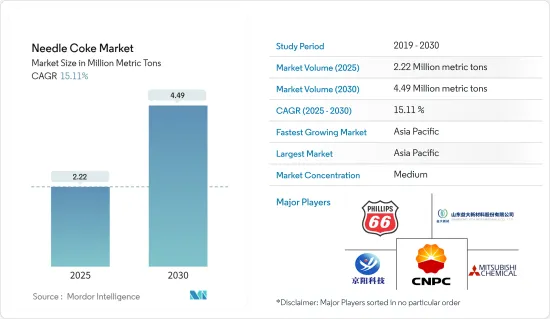

세계의 니들코크스 시장 규모는 2025년 222만 톤으로 추정되며, 예측기간 중(2025-2030년) CAGR 15.11%를 나타낼 전망이며, 2030년에는 449만 톤에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 니들 코크스 시장에 부정적인 영향을 주었습니다. 팬데믹 동안 제철소에서의 수요가 감소했기 때문에 흑연 전극의 제조가 큰 영향을 받아 니들 코크스의 소비가 감소했습니다.

중기적으로는 EAF 철강 제조에 대한 투자 증가와 스크랩 철강 소비를 증가시키는 정부의 유리한 정책이 시장 성장을 가속하는 중요한 요인입니다.

그러나 석유 코크스와 관련된 건강 피해는 조사 시장의 성장을 방해할 가능성이 높습니다.

세계의 리튬 이온 배터리 생산 증가는 예측 기간 동안 시장에 호기심이 될 것입니다.

아시아태평양은 지배적인 시장에 부상했습니다. 또한 인도, 중국, 일본 등의 국가들로부터의 높은 수요에 의해 2024-2029년까지 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

니들 코크스 시장 동향

흑연 전극 부문이 시장을 독점

니들 코크스는 전기로에 사용되는 흑연 전극의 주요 원료입니다. 이것은 열팽창 계수(CTE)가 매우 낮은 흑연 전극을 제조하는 데 사용되는 고급 및 고가 석유 코크스입니다.

철강 및 기타 금속 산업에서 사용되는 전기로에서의 흑연 전극의 광범위한 적용을 위해, 흑연 전극용 니들 코크스의 용도는 니들 코크스의 가장 큰 용도를 차지합니다.

그라파이트는 열전도율이 높고, 열이나 충격에 강합니다. 또, 철을 녹이는데 필요한 큰 전류를 흘리는데 필요한 전기 저항도 낮습니다. 그 때문에 EAF(전기로)에서 발생하는 지극히 높은 열량에 견딜 수 있습니다.

흑연 전극은 RP 흑연 전극, HP 흑연 전극, SHP 흑연 전극, UHP 흑연 전극의 4유형로 나뉩니다.

흑연 전극은 주로 전로강, 합금강, 각종 합금, 비금속의 제조에 사용됩니다. 이 전극은 고열을 발생시킬 수 있으며, 강철의 정련이나 유사한 제련 공정에도 사용됩니다.

Sanergy Group Limited의 데이터에 따르면 2023년 세계 흑연 전극 생산량은 878만 5,000톤으로, 2024년에는 79만 5,400톤에 이를 것으로 예측됐습니다.

2023년 12월, Graphite India Limited(GIL)는 Godi India Private Ltd의 강제 전환 우선 주식에 50캐롤 루피(약 600만 달러)를 투자했습니다. Godi India는 전기자동차(EV)를 위한 지속가능한 배터리와 슈퍼커패시터를 기반으로 하는 에너지 저장시스템의 생산을 지원하는 첨단 연구개발을 추진하고 있습니다. 이 투자는 첨단 배터리와 에너지 저장 기술로 다각화하는 GIL의 전략에 부합합니다.

2023년 11월, HEG Limited는 인도의 매디아 프라데시 주에 있는 흑연 전극의 생산 능력을 연산 80킬로톤에서 100킬로톤으로 확대하는 데 성공했습니다.

상기 요인은 예측 기간 동안 흑연 전극 용도의 바늘 코크스 수요에 영향을 미칠 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 중국(니들 코크스의 최대 생산국이자 소비국이기도 함)과 일본 등의 국가를 포함하기 때문에 니들 코크스 시장을 독점할 것으로 예상됩니다.

중국은 흑연 전극의 소비량과 생산 능력으로 세계 최대의 점유율을 차지하고 있습니다. 중국에는 40개 이상의 공식 흑연 전극 제조업체가 있습니다.

이와 더불어 중국 정부는 친환경 철강 생산 수단의 개발에도 힘을 쏟고 있습니다. EAF 기술은 주로 철 스크랩을 원료로 하며, 그 용해에 전력을 사용합니다.

일본은 석유, 석탄, 타르계 피치 니들 코크스의 주요 생산국 및 수출국 중 하나입니다. 일본 기업은 세계 최대의 흑연 전극 생산국 중 하나입니다.

인도의 철강 업계는 탈탄소화에 대한 대처를 강화하고 탄소 배출량의 삭감에 적극적으로 임하고 있습니다.

EAF의 채택이 진행됨에 따라 흑연 전극 수요 급증이 예상됩니다.

일본 제2위의 철강 제조업체인 JFE Steel은 2023년 11월에 대규모 전기로(EAF)의 건설 계획을 발표했습니다. 후변화 이니셔티브에 따른 탄소 배출의 억제에 대한 동사의 헌신을 강조하는 것입니다.새로운 전기로는 주로 자동차 및 기타 분야에 공급되어 연간 260만 톤의 배출 감축이 전망됩니다.

흑연 전극은 철강 생산의 주요 방법인 전기로(EAF) 공정에서 중요한 역할을 하고 있습니다. 한국철강협회의 보고에 따르면 철강업은 한국의 GDP의 1.5%, 제조업의 4.9%를 차지하고 있습니다.

따라서 아시아태평양은 위의 측면에서 세계 니들 코크스 시장을 독점 할 가능성이 높습니다.

니들 코크스 산업 개요

니들 코크스 시장은 부분적으로 통합되어 있습니다. 시장의 주요 기업(특별한 순서 없음)에는 Phillips 66 Company, China National Petroleum Corporation(CNPC), Shandong Yida Rongtong Trading Co., Shandong Jing Yang Technology, Mitsubishi Chemical Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- EAF 철강 제조에 대한 투자 증가

- 철스크랩 소비 확대를 위한 정부 정책

- 억제요인

- 석유 코크스에 따른 건강 피해

- 업계의 밸류체인 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 개요

제5장 시장 세분화

- 제품 유형별

- 석유계

- 콜타르 피치계

- 용도별

- 흑연 전극

- 리튬 이온 배터리

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 분석

- 주요 기업의 전략

- 기업 프로파일

- Baosteel Group

- China National Petroleum Corporation(CNPC)

- China Petroleum & Chemical Corporation(Sinopec)

- Indian Oil Corporation

- Liaoning Baolai Bioenergy Co., Ltd.

- Mitsubishi Chemical Corporation

- Nippon Steel Corporation

- Phillips 66

- Posco Mc Materials

- Seadrift Coke LP(Graftech International)

- Shandong Dongyang Technology Co. Ltd

- Shandong Yida New Materials Co. Ltd

- Shanxi Hongte Coal Chemical Co. Ltd

제7장 시장 기회와 앞으로의 동향

- 리튬 이온 전지가 니들 코크스 수요를 끌어 올린다

The Needle Coke Market size is estimated at 2.22 million metric tons in 2025, and is expected to reach 4.49 million metric tons by 2030, at a CAGR of 15.11% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the needle coke market. During the pandemic, the manufacturing of graphite electrodes was heavily affected due to less demand from the steel manufacturing plants, which reduced the consumption of needle coke. However, the market registered a significant growth rate after the restrictions were lifted due to the recovering demand for lithium-ion batteries and graphite electrodes.

Over the medium term, increasing investments in EAF steel manufacturing and favorable government policies to increase scrap steel consumption are significant factors driving the growth of the studied market.

However, health hazards associated with petroleum coke are likely to hinder the growth of the studied market.

The increase in lithium-ion battery production globally is likely to act as an opportunity for the market studied during the forecast period.

Asia-Pacific emerged as the dominant market. It is also expected to register the highest CAGR from 2024 to 2029 due to the high demand from countries such as India, China, Japan, and others.

Needle Coke Market Trends

Graphite Electrodes Segment to Dominate the Market

Needle coke is a primary raw material for graphite electrodes in electric furnaces. It is a premium-grade, high-value petroleum coke used to manufacture graphite electrodes with a very low coefficient of thermal expansion (CTE).

Owing to the wide application of graphite electrodes in electric arc furnaces, which are used in steel and other metal industries, the application of needle coke for graphite electrodes accounts for the largest application of needle coke.

Graphite has high thermal conductivity and is resistant to heat and any impact. Also, it has low electrical resistance, which is needed to conduct large electrical currents necessary to melt iron. Thus, it can sustain extremely high heat levels generated by EAF (electric arc furnace). Making the electrodes requires processing coke, including baking and rebaking, to convert it into graphite, which can take up to six months.

Graphite electrodes are divided into four types: RP graphite electrodes, HP graphite electrodes, SHP graphite electrodes, and UHP graphite electrodes.

Graphite electrodes are primarily used to manufacture electric arc furnace steel, alloy steel, various alloys, and nonmetals. These electrodes can generate high levels of heat and are also used in refining steel and similar smelting processes. They can melt iron scrap in an electric arc furnace at about 1,600°C.

According to data from Sanergy Group Limited, the production volume of graphite electrodes worldwide was 8785 thousand metric tons in 2023 and is projected to reach 795.4 thousand metric tons in 2024.

In December 2023, Graphite India Limited (GIL) invested INR 50 crore (approximately USD 6 million) in compulsorily convertible preference shares of Godi India Private Ltd. This investment provides GIL with a 31% equity shareholding in Godi India. Godi India is engaged in advanced Research and development to support the production of sustainable batteries for electric vehicles (EVs) and supercapacitor-based energy storage systems. Godi India's environment-friendly and carbon-neutral processes include Aqueous Electrode ProcessingTM, Active Dry CoatingTM, and Pranic BinderTM. This investment aligns with GIL's strategy to diversify into advanced battery and energy storage technologies.

In November 2023, HEG Limited successfully expanded its graphite electrode capacity in Madhya Pradesh, India, from 80 kilotons per annum to 100 kilotons per annum. The company made a substantial investment of INR 1,200 crore (USD 143.741 million) for this capacity expansion. As a result, HEG is the third-largest graphite electrode company in the Western world.

The factors mentioned above are expected to affect the demand for needle coke for graphite electrode application during the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific is expected to dominate the needle coke market, as it includes countries such as China (the biggest producer and consumer of needle coke) and Japan.

China holds the largest share of graphite electrode consumption and production capacity in the global scenario. There are over 40 official graphite electrode manufacturers in China. The Chinese market's demand for graphite electrodes and further diversification into lithium-ion battery anodes, fueled by the EV industry's growth, are both driving a comeback in the demand for needle coke. For the foreseeable future, this demand is expected to continue to increase steadily, with corresponding pricing support.

In addition to this, the Chinese government is also focusing on developing eco-friendly means of producing steel. Hence, Chinese authorities are actively promoting Electric Arc Furnace (EAF) technology as a means to curb carbon emissions and foster sustainability in the steel industry. EAF technology relies primarily on steel scrap as its raw material, with electricity used to melt it. Driven by supportive national policies, the adoption of EAF technology is poised to become a prevailing trend in China, consequently bolstering the demand for graphite electrodes.

Japan is one of the leading producers and exporters of petroleum, coal, and tar-based pitch needle coke. Japanese companies are one of the largest producers of graphite electrodes in the world. The market giants of graphite electrodes include Showa Denko, Nippon Carbon, SEC Carbon, and Tokai Carbon.

The Indian steel industry is actively working to reduce carbon emissions through intensified efforts to decarbonize. As part of this push, there is a rising trend in adopting electric arc furnace (EAF) technology for steel production. EAFs rely on electricity and steel scrap, making them a more sustainable choice than traditional methods.

With the growing adoption of EAFs, there is a significant expected surge in demand for graphite electrodes. The Indian government's move to eliminate customs duty on scrap imports directly benefits EAF steel manufacturers. Coupled with favorable national policies, these further fuel the shift toward EAFs and drive the demand for graphite electrodes.

JFE Steel, Japan's second-largest steelmaker, announced in November 2023 its plans to construct a large-scale electric arc furnace (EAF). The EAF is slated to replace an existing blast furnace at its Kurashiki plant by around 2027. This strategic move underscored the company's commitment to curbing carbon emissions, which is in line with global climate change initiatives. The new EAF will primarily cater to automotive and other sectors, with an anticipated annual emissions reduction of 2.6 million tons.

Graphite electrodes play an important role in the electric arc furnace (EAF) process, a key method for steel production. The steel sector in South Korea is significant, driving the nation's economic growth by catering to industries like automotive, construction, and shipbuilding. The steel industry accounts for 1.5% of the nation's GDP and 4.9% of its manufacturing sector, as reported by the Korean Iron & Steel Association. Notably, South Korea ranks as the sixth-largest steel producer globally.

Hence, Asia-Pacific is likely to dominate the global needle-coke market based on the aspects mentioned above.

Needle Coke Industry Overview

The needle coke market is partially consolidated. Some of the major players in the market (not in any particular order) include Phillips 66 Company, China National Petroleum Corporation (CNPC), Shandong Yida Rongtong Trading Co., Shandong Jing Yang Technology Co. Ltd, and Mitsubishi Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Investments in EAF Steel Manufacturing

- 4.1.2 Government Policies to Increase Scrap Steel Consumption

- 4.2 Restraints

- 4.2.1 Health Hazards Associated with Petroleum Coke

- 4.3 Industry Value-Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Overview

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Petroleum Based

- 5.1.2 Coal-tar Pitch Based

- 5.2 Application

- 5.2.1 Graphite Electrodes

- 5.2.2 Lithium-ion Batteries

- 5.2.3 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Baosteel Group

- 6.4.2 China National Petroleum Corporation (CNPC)

- 6.4.3 China Petroleum & Chemical Corporation (Sinopec)

- 6.4.4 Indian Oil Corporation

- 6.4.5 Liaoning Baolai Bioenergy Co., Ltd.

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 Nippon Steel Corporation

- 6.4.8 Phillips 66

- 6.4.9 Posco Mc Materials

- 6.4.10 Seadrift Coke LP (Graftech International)

- 6.4.11 Shandong Dongyang Technology Co. Ltd

- 6.4.12 Shandong Yida New Materials Co. Ltd

- 6.4.13 Shanxi Hongte Coal Chemical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Lithium-ion Batteries to Boost the Demand for Needle Coke