|

시장보고서

상품코드

1869575

연속 생산 시장 : 업계 동향과 세계 예측(-2035년) - 약제 분자별, 바이오프로세싱 단계별, 제조되는 제품 유형별, 사업 규모별, 제조 목적별, 기업 규모별, 주요 지역별Continuous Manufacturing Market: Industry Trends and Global Forecasts, Till 2035 - Distribution by Drug Molecule, Stage of Bioprocessing, Product Manufactured, Scale of Operation, Purpose of Manufacturing, Company Size, and Key Geographical Regions |

||||||

연속 생산 시장

연속 생산 시장 규모는 올해 26억 달러에 달할 것으로 추정되며, 2040년까지 42억 달러에 달할 것으로 예측됩니다. 이는 예측 기간 동안 4.9%의 높은 CAGR을 나타낼 것입니다.

시장 기회는 다음과 같은 부문에 분산되어 있습니다.

약제 분자

- 바이오의약품

- 저분자 화합물

바이오프로세싱 단계

- 업스트림 바이오프로세스

- 다운스트림 공정

생산되는 제품 유형

- 원료의약품

- 최종 제형

사업 규모

- 비임상 및 임상

- 상업적 생산

제조 목적

- 자체 제조

- 위탁생산

- 양쪽 다

회사 규모

- 소규모

- 중규모

- 대

주요 지역

- 북미

- 유럽

- 아시아태평양

연속 생산 시장 : 성장과 동향

제약사의 전통적인 의약품 제조는 생산 기간의 장기화, 자원 활용의 비효율성, 비용 증가, 공급망의 복잡성 등 다양한 문제를 안고 있습니다. 이러한 문제를 해결하기 위해 업계 안팎의 기업들은 의약품 제조를 배치 공정에서 연속 공정으로 전환하기 위한 연구개발(R&D)에 대한 투자를 확대하고 있습니다. 이러한 선택지 중 연속 생산은 바이오 의약품 및 저분자 의약품의 대량 생산에 있어 매우 선호되는 방법입니다. 연속 생산는 하나의 생산 사이클 동안 원료와 시약을 지속적으로 첨가하는 연속적인 공정을 통해 원하는 제품을 생산하는 데 도움이 됩니다. 이 연속 공정은 다운타임을 줄이고, 설비 가동률을 최적화하여 효율성과 생산성 향상, 단위 비용 절감(약 40-50%), 그리고 의약품의 신속한 상업화를 실현합니다.

또한, 연속 생산의 도입은 생산성 향상, 운영 효율성 개선, 균일한 제품 품질 등 여러 가지 이점을 가져옵니다. 흥미롭게도, 이해관계자들은 자동화와 실시간 모니터링을 통합하여 이러한 절차를 강화하여 인적 오류를 최소화하고 프로세스의 변동성을 줄이는 것을 목표로 하고 있습니다. 또한, FDA 등 규제 당국은 이 기술로 개발된 의약품의 승인 절차를 가속화할 수 있는 가이드라인을 제시하며, 연속생산을 적극적으로 권장하고 있습니다.

전통적인 제조 공정의 높은 인건비, 상당한 가동 중지 시간, 배치 간 편차가 일관된 제품 품질과 비용 효율성을 보장하는 연속 제약 생산에 대한 수요를 촉진하고 있습니다. 또한, 첨단 실시간 모니터링 기술과 자동화 기술의 도입으로 제약 기업은 다단계 배치 생산 기술에서 신속하고 효율적인 연속 생산으로의 전환을 추진하고 있습니다.

연속 생산 시장 : 주요 인사이트

본 보고서는 연속 생산 시장의 현황을 상세하게 분석하고, 업계 내 잠재적인 성장 기회를 파악합니다. 보고서의 주요 요점은 다음과 같습니다.

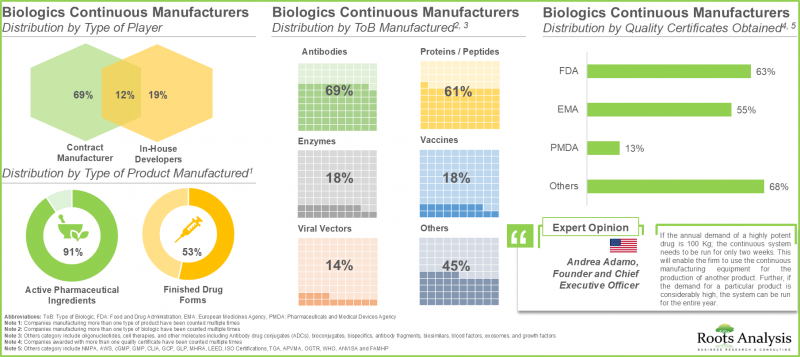

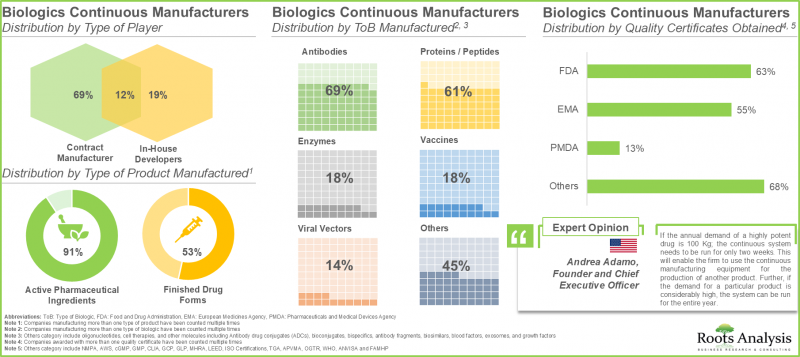

현재 연속형 바이오의약품 제조업체 시장 상황은 신규 진출기업과 기존 기업이 모두 존재하는 매우 세분화된 상태입니다. 이들 기업의 대부분은 미국에 본사를 두고 있습니다.

2. 전 세계 45개 이상의 기업이 연속 생산 기술을 이용한 생물학적 제제 수탁 제조 서비스를 제공합니다. 이 중 80%의 기업이 원료의약품을 생산하고 있습니다.

3. 바이오로직스 수요 증가에 따라 각 업체들은 고품질 제품을 효율적으로 생산하기 위해 연속 생산 기술의 기술 전문성을 강화하고 있습니다.

4. 소분자 의약품의 연속 생산 기술을 보유하고 있다고 주장하는 제조업체는 약 50여 개에 달할 전망입니다. 이들 기업의 80% 이상이 대기업 및 초대형 기업입니다.

5. 연속 생산을 하는 저분자 의약품 제조업체의 80% 이상이 플로우 기술을 활용한 원료의약품 합성에 집중하고 있으며, 이를 통해 제조 공정의 안전성, 효율성, 비용 효율성이 향상되고 있습니다.

6. 연속 생산 분야의 제휴 및 협력의 약 55%가 지난 3년간 체결되었습니다. 그 중 대부분은 제조 계약이었습니다.

7. 기업의 약 35%가 새로운 시설을 설립했으며, 그 중 약 50%는 바이오 의약품과 저분자의 임상 및 상업적 규모의 연속 생산에 초점을 맞추었습니다.

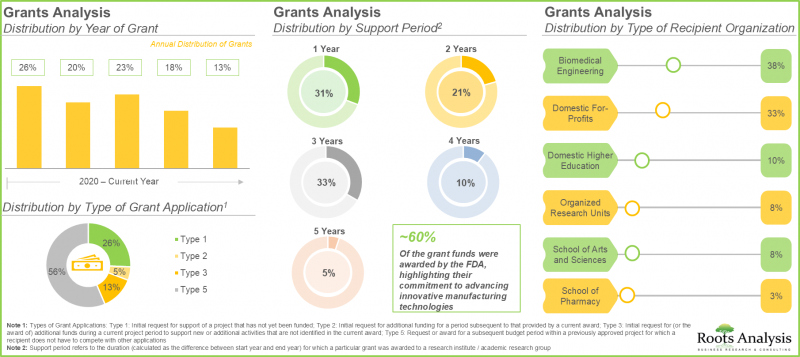

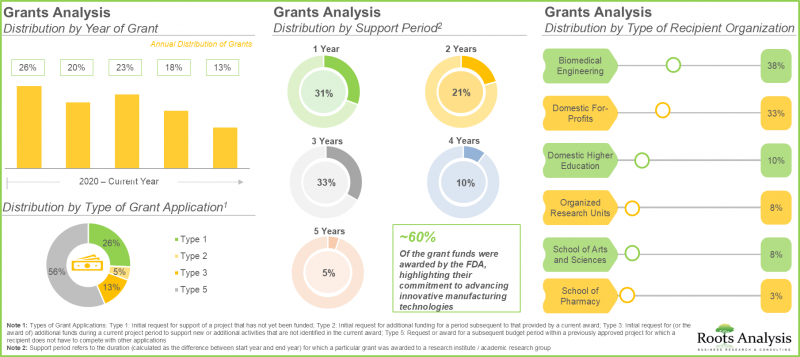

8. 연속 생산 관련 연구에 총 2,500만 달러의 보조금이 지원되고 있으며, 이 중 약 30%는 최대 3년의 지원 기간을 두고 있습니다.

9. 2020년 이후, 연속 생산 관련 특허는 약 80여 건이 승인되었습니다. 또한, 이들 특허의 대부분은 독점권이 만료되기까지 17년이 남았습니다.

10. 현재 전 세계 바이오의약품 연속 생산 설비의 총 용량은 약 22만 5,000리터로 추정됩니다. 이 중 약 40%는 유럽에 기반을 둔 기업 시설에 설치되어 있습니다.

11. 유럽 전역에서 총 시설용량의 약 50%가 임상 및 상업적 규모의 제조를 제공하는 주요 제조업체의 시설에 집중되어 있습니다.

12. 바이오의약품 연속생산 시장은 2035년까지 연평균 4.9%의 성장률을 보일 것으로 예측됩니다. 현재 시장 점유율의 대부분은 업스트림 바이오프로세스가 차지하고 있으며, 그 다음으로 다운스트림 바이오프로세스가 그 뒤를 잇고 있습니다.

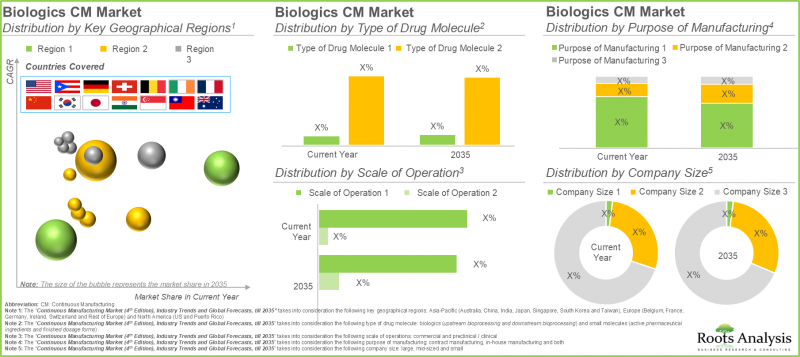

13. 현재 저분자 의약품이 전체 연속 생산 시장의 65% 이상을 차지하고 있습니다. 2035년까지 북미가 90% 이상 시장 점유율을 차지하며 주요 점유율을 차지할 것으로 예측됩니다.

연속 생산 시장 : 주요 부문

연속 생산 시장은 바이오로직스와 저분자 화합물로 구분됩니다. 올해 저분자 화합물 부문이 시장 점유율의 대부분(65% 이상)을 차지했습니다. 이는 생물학적 제제가 살아있는 세포에서 보다 복잡한 추출 절차를 필요로 하는 반면, 저분자 화합물은 화학적 특성으로 인해 제조 공정이 간단하기 때문입니다. 생물학적 제제 부문은 높은 표적 특이성, 낮은 약물 상호작용과 같은 여러 장점에 힘입어 암 및 희귀질환을 포함한 다양한 질환의 치료에 적용될 가능성이 높기 때문에 예측 기간 동안 높은 CAGR로 성장할 가능성이 높다는 점을 강조하는 것이 중요합니다.

연속 생산 공정별 세계 시장은 업스트림 바이오프로세스과 다운스트림 바이오프로세스으로 구분됩니다. 당사의 조사 결과에 따르면, 업스트림 바이오프로세스은 올해 주요 점유율(약 95%)을 차지하고 있습니다. 업스트림 공정은 최종 제품의 정제 및 제형화를 포함한 다운스트림 공정의 기반을 구축하는 것입니다. 따라서 업스트림 공정의 효율성과 품질은 최종 제품의 수율과 품질에 큰 영향을 미칩니다.

제조 제품을 기반으로 한 저분자 연속 생산 시장은 원료의약품과 최종 제형으로 구분됩니다. 최종제형은 올해 가장 큰 점유율(약 65%)을 차지하고 있습니다. 이는 최종 사용자를 위한 최종 제형의 상업화 승인이 증가한 결과입니다. 또한, 원료의약품 부문은 예측 기간 동안 높은 성장 잠재력을 보이고 있습니다.

운영 규모 측면에서 연속 생산 시장은 전임상/임상 단계와 상업 생산 단계로 구분됩니다. 특히 바이오의약품 및 저분자 화합물의 상업적 규모 운영이 현재 연속 생산 시장 점유율의 대부분(약 90%)을 차지하고 있다는 점은 주목할 만합니다. 관류 기반 연속 바이오프로세스 기술의 산업 도입이 증가함에 따라 이러한 기술은 생산 조건에서 불안정한 생물학적 API 제조에 선호되는 선택이 되고 있습니다. 또한, 이러한 프로세스를 현재 워크플로우에 통합하면 열화의 원인이 될 수 있는 제품별로 최종 제품을 주기적으로 분리할 수 있습니다.

제조 목적에 따라 분류하면, 연속 생산 시장은 자체 제조, 수탁 제조, 그리고 이 두 가지 형태로 나뉩니다. 주목할 만한 점은 올해 들어 위탁생산 부문이 생물학적 제제와 저분자 화합물 시장에서 70% 이상의 점유율을 차지하고 있다는 점입니다. 이는 수탁 제조업체가 맞춤형 솔루션을 제공할 수 있는 역량을 강화했기 때문이며, 이를 통해 제조업체는 제조 공정을 위한 자체 제조 시설을 구축하기 위해 자원을 할당하는 대신 자사의 핵심 강점에 집중할 수 있게 되었습니다. 또한, 자체 제조 부문은 예측 기간 동안 높은 CAGR로 성장할 가능성이 높습니다.

기업 규모별로 보면, 연속 생산 시장은 기업 규모에 따라 소규모, 중규모, 대규모로 분류됩니다. 2025년 기준, 대기업 부문이 연속 생산 시장 규모의 대부분(70% 이상의 점유율)을 차지할 것으로 예측됩니다. 이는 대규모 바이오의약품/저분자 의약품 제조업체가 전용 리소스와 역량을 갖추고 있어 중견/중소기업에 비해 제조 워크플로우에서 시장 동향을 빠르게 구현할 수 있기 때문입니다. 또한, 중견기업들은 생산능력 확대와 연속 생산 운영의 효율화를 위한 지속적인 투자를 진행하고 있으며, 그 결과 눈에 띄는 성장률로 확대될 것으로 예측됩니다.

이 부문에서는 북미, 유럽, 아시아태평양 등 다양한 지역 시장 분포를 파악할 수 있습니다. 당사의 조사 결과에 따르면, 유럽은 바이오의약품(약 40%) 및 저분자 의약품(50% 이상) 연속 생산 시장에서 모두 과반수 이상의 점유율을 차지할 것으로 예측됩니다. 이는 연구 개발 활동에서 연구원들의 노력으로 시설 전체에 연속 생산 기술 도입이 빠르게 진행된 결과입니다. 주목할 만한 점은 저분자 연속 생산 시장이 아시아태평양에서 비교적 빠른 속도로 성장할 것으로 예상된다는 점입니다. 이는 연속 생산 기술의 도입을 촉진하고 고품질 의약품 개발을 지원하기 위해 다양한 업계 관계자들이 유연한 생태계의 채택을 확대하고 있기 때문입니다.

연속 생산 시장의 대표적인 진출기업

- AbbVie Contract Manufacturing

- Abzena

- AGC Biologics

- Boehringer Ingelheim

- Corden Pharma

- Glatt

- Kaneka

- Phlow

- Wuxi Biologics

목차

섹션 I : 보고서 개요

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

섹션 II : 정성적 인사이트

제5장 주요 요약

제6장 서론

- 본 장의 개요

- 연속 생산 역사적 진화

- 제약 업계 연속 생산

섹션 III : 시장 개요

제7장 시장 구도 : 생물제제 연속 생산업체

- 본 장의 개요

- 바이오의약품 연속 생산업체 : 시장 구도

제8장 기업 경쟁력 분석 : 지속적 바이오의약품 제조업체

제9장 시장 구도 : 소분자 연속 생산업체

제10장 기업 경쟁력 분석 : 저분자화합물 제조 기업

섹션 IV : 기업 개요

제11장 기업 개요 : 북미에 거점을 둔 연속 생산 서비스 제공업체

- 본 장의 개요

- AbbVie Contract Manufacturing

- Abzena

- AGC Biologics

- Phlow

제12장 기업 개요 : 유럽에 거점을 둔 연속 생산 서비스 제공업체

- 본 장의 개요

- Boehringer Ingelheim

- Corden Pharma

- Glatt

제13장 기업 개요 : 아시아태평양에 거점을 둔 연속 생산 서비스 제공업체

- 본 장의 개요

- Kaneka

- WuXi Biologics

제5장 시장 동향

제14장 파트너십 및 협업

제15장 최근 확장

제16장 보조금 분석

제17장 특허 분석

제18장 연속 바이오프로세스에 관련된 갭

제19장 사내 지속 능력을 가지는 기업 대처

- 본 장의 개요

- 주요 기업별 연속 생산 대처

- Amgen

- Boehringer Ingelheim

- Bristol-Myers Squibb

- GSK

- Merck KGaA

- Novartis

- Pfizer

- Sanofi

제20장 사례 연구 1 : 생물제제 연속 생산 장비

제21장 사례 연구 2 : 연속 생산 공정 도입을 위한 로드맵

제22장 사례 연구 3 : 제약/바이오테크놀러지 산업 모듈러 시설

제23장 캐파시티 분석 : 지속적 바이오의약품 제조업체

제24장 생산능력 분석 : 연속 소분자 제조업체

섹션 VI : 시장 예측과 기회 분석

제25장 세계의 연속 생산 시장

제26장 연속 생산 시장(약제 분자별)

제27장 연속 생산 시장(사업 규모별)

제28장 연속 생산 시장(제조 목적별)

제29장 연속 생산 시장(기업 규모별)

제30장 연속 생산 시장(주요 지역별)

섹션 VII : 지역 시장 기회 분석

제31장 시장 기회 분석 : 북미

제32장 시장 기회 분석 : 유럽

LSH 25.11.24CONTINUOUS MANUFACTURING MARKET

The continuous manufacturing market is estimated to reach USD 2.6 billion in the current year and is likely to reach USD 4.2 billion by 2040, representing a higher CAGR of 4.9% during the forecast period.

The market opportunity has been distributed across the following segments:

Type of Drug Molecule

- Biologics

- Small Molecules

Stage of Bioprocessing

- Upstream Bioprocessing

- Downstream Bioprocessing

Type of Product Manufactured

- Active Pharmaceutical Ingredients

- Finished Dosage Forms

Scale of Operation

- Preclinical / Clinical

- Commercial

Purpose of Manufacturing

- In-House Manufacturing

- Contract Manufacturing

- Both

Company Size

- Small

- Mid-sized

- Large

Key Geographical Regions

- North America

- Europe

- Asia-Pacific

CONTINUOUS MANUFACTURING MARKET: GROWTH AND TRENDS

Conventional drug production by pharmaceutical manufacturers is associated with various challenges, including prolonged production timelines, inefficiencies in resource utilization, higher costs, and supply chain complexities. To circumvent the above-mentioned challenges, industry and non-industry players are increasingly investing in R&D initiatives for transforming pharmaceutical manufacturing from batch processes to continuous methods. Among these options, continuous manufacturing has become a highly favored method for large-scale production of biologics and small molecules. Continuous manufacturing helps in generating the desired product through an ongoing process by consistently adding raw materials and reagents during one production cycle. This ongoing process reduces downtime and optimizes equipment usage, resulting in increased efficiency and productivity, lowered unit costs by (~40-50%), and faster drug commercialization.

Additionally, the implementation of continuous manufacturing provides multiple benefits, including enhanced productivity, improved operational efficiency, and uniform product quality. Interestingly, stakeholders are enhancing these procedures by incorporating automation and real-time monitoring, with an aim to minimize human errors and reduce inconsistencies in the process. Furthermore, regulatory agencies, such as the FDA actively endorses continuous manufacturing by providing guidelines that accelerate the approval process for drugs developed through this technique.

High labor expenses, significant downtime, and variability between batches in traditional manufacturing have driven the demand for continuous pharmaceutical production to guarantee consistent product quality and enhanced cost-effectiveness. Moreover, the implementation advanced real-time monitoring and automation technologies has driven pharmaceutical firms to transition from multi-step batch production techniques to fast and efficient continuous manufacturing

CONTINUOUS MANUFACTURING MARKET: KEY INSIGHTS

The report delves into the current state of the continuous manufacturing market and identifies potential growth opportunities within industry. The key takeaways of the report are:

1. The current market landscape of continuous biologic manufacturers is highly fragmented, featuring the presence of both new entrants and established players; majority of these players are based in the US.

2. More than 45 players offer contract manufacturing services for biologics using continuous manufacturing across the globe; of these, 80% of the players manufacture active pharmaceutical ingredients.

3. Owing to the rising demand for biologics, companies are upgrading their technical expertise in continuous manufacturing techniques to efficiently manufacture high quality products.

4. Close to 50 manufacturers claim to have expertise in continuous manufacturing of small molecules; more than 80% of these players are large and very large firms.

5. Over 80% of the continuous small molecule manufacturers are focused on synthesizing APIs by utilizing flow technology to enhance the safety, efficiency, and cost effectiveness of the production process.

6. Around 55% of the total partnerships and collaborations in the continuous manufacturing domain were inked in past three years; of these, most of the deals were manufacturing agreements.

7. Close to 35% of players have established new facilities; of these, around 50% are focused on both clinical and commercial scale continuous manufacturing of biologics and small molecules.

8. Grants worth USD 25 million have been awarded for research related to continuous manufacturing; ~30% of these grants extend a support period of up to three years.

9. Around 80 patents have been granted related to continuous manufacturing since 2020; further, majority of the patents have 17 years left until they lose their exclusivity.

10. Presently, the global installed biologics continuous manufacturing is estimated to be around 225,000 liters; around 40% of this capacity is installed in the facilities of players based in Europe.

11. Across Europe, nearly 50% of the total capacity is housed in large manufacturers' facilities that offer both clinical and commercial scale manufacturing.

12. The continuous biologics manufacturing market is likely to grow at a CAGR of 4.9%, till 2035; presently, majority of the market share is occupied by upstream bioprocessing followed by downstream bioprocessing

13. In the current year, small molecules account for over 65% of the overall continuous manufacturing market; By 2035, North America is expected to capture the majority share, exceeding 90% of the market.

CONTINUOUS MANUFACTURING MARKET: KEY SEGMENTS

Small Molecule Segment Holds the Largest Share of the Continuous Manufacturing Market

The continuous manufacturing market is segmented across biologics and small molecules. In the current year, small molecules segment captures the majority of the market share (>65%). This can be attributed to the simple production process of small molecules due to its chemical nature, in comparison to biologics, that require more complex extraction procedures from living cells. It is important to highlight that the biologics segment is likely to grow at a higher CAGR during the forecast period, driven by several advantages, such as high target specificity and fewer drug interactions which facilitate their application in treating various disorders, including cancer and rare disorders.

Upstream Bioprocessing is the Most Used Stage of Continuous Manufacturing Market

The global market by stage of continuous manufacturing is segmented across upstream bioprocessing and downstream bioprocessing. Based on our findings, the upstream bioprocessing holds the major share (~95%) in the current year. Upstream processing lays the foundation for downstream processing, which involves purification and formulation of the final product. Thus, efficiency and quality of the upstream processes significantly influence the yield and quality of the final product.

Finished Dosage Forms Dominates the Largest Share of the Continuous Manufacturing Market

The small molecules continuous manufacturing market based on products manufactured is segmented across active pharmaceutical ingredients and finished dosage forms. Finished dosage forms hold the largest share (~65%) in the present year. This is a result of the increase in the approvals for the commercialization of finished doses to end-user. Further, active pharmaceutical ingredients segment shows higher growth potential, during the forecast period.

Commercial Scale Segment Holds the Largest Share of the Continuous Manufacturing Market

In terms of scale of operation, the continuous manufacturing market is segmented across preclinical / clinical and commercial operations. It is worth highlighting that the commercial scale of operation for biologics and small molecules captures majority of the continuous manufacturing market share (~90%), currently. Owing to the increased industrial adoption of perfusion based continuous bioprocessing technologies, these technologies are preferred option for manufacturing of biologic APIs that are unstable under production conditions. Moreover, incorporation of these processes in the current workflow enables regular separation of the final product from by-products that may cause degradation.

Contract Manufacturing Segment Dominates the Continuous Manufacturing Market

In terms of purpose of manufacturing, the continuous manufacturing market is segmented across in-house manufacturing, contract manufacturing and both. It is worth highlighting that the contract manufacturing segment dominates (>70%) the market for both biologics and small molecules in the current year. This is due to the enhanced capability of contract manufacturers in delivering customized solutions, enabling manufacturers to concentrate on their core strengths instead of allocating resources to establish their own manufacturing facilities for the production process Further, in-house manufacturing segment is likely to grow at a higher CAGR during the forecast period.

By Company Size, Large Players Holds the Largest Share of the Continuous Manufacturing Market

In terms of company size, the continuous manufacturing market is based on the company size, such small, mid-sized and large. Large company segments hold majority continuous manufacturing market size (with >70% share) in 2025. This is a result of dedicated resources and capabilities with the large biologics / small molecule manufacturers which allows for rapid implementation of market trends in their manufacturing workflow as compared to mid-sized or small manufacturers. Further, mid-sized companies are undertaking continuous investments to expand their capabilities and streamline continuous manufacturing operations. As a result, they are likely to grow at a notable growth rate.

Asia-Pacific to Propel in the Continuous Manufacturing Sector in the Coming Years

This segment highlights the distribution of market across various geographies, such as North America, Europe, and Asia-Pacific. As per our findings, Europe is likely to capture majority share in both biologics (~40%) and small molecules (>50%) continuous manufacturing market. This is a result of the efforts of researchers in R&D activities to expedite the implementation of continuous manufacturing technologies across their facilities. It is worth highlighting that the small molecule continuous manufacturing market will grow at a relatively faster pace in Asia-Pacific. This is due to increasing adoption of flexible ecosystem by various industry players to facilitate the implementation of continuous manufacturing technologies and support the development of high-quality pharmaceutical products.

Primary Research Overview

Discussions with multiple stakeholders in this domain influenced the opinions and insights presented in this study. The market report includes detailed transcripts of interviews conducted with the following individuals:

- Founder and Chief Executive Officer, Small Organization, US

- Co-Founder and Chief Business Officer, Mid-sized Organization, US

- Chief Executive Officer, Large Organization, India

- Vice President Process Chemistry and Technology, Very Large Organization, US

- General Site Manager, Small Organization, US

- Technical Project Manager, Continuous Manufacturing and Crystallization, Very Large Organization, UK

Example Players in the Continuous Manufacturing Market

- AbbVie Contract Manufacturing

- Abzena

- AGC Biologics

- Boehringer Ingelheim

- Corden Pharma

- Glatt

- Kaneka

- Phlow

- Wuxi Biologics

CONTINUOUS MANUFACTURING MARKET: RESEARCH COVERAGE

The report on continuous manufacturing market features insights into various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of current market opportunity and the future growth potential of continuous manufacturing market, focusing on key market segments, including [A] type of drug molecule, [B] stage of bioprocessing, [C] type of product manufactured, and [D] geographical regions.

- Market Landscape: A comprehensive evaluation of service providers engaged in the continuous manufacturing market based on several relevant parameters, such as [A] type of player, [B] scale of operation, [C] type of dosage form, and [D] type of product manufactured, [E] year of establishment, [F] company size, and [G] location of headquarters.

- Company Competitiveness Analysis: An insightful technology competitiveness and benchmarking analysis, based on various relevant parameters, such as [A] company strength, and [B] portfolio strength.

- Company Profiles: Comprehensive profiles of leading service providers, featuring information on [A] company overview, [B] financial information (if available), [C] continuous manufacturing service portfolio, [D] continuous manufacturing facilities, [E] recent developments, and [E] future outlook statements.

- Partnerships and Collaborations: A detailed analysis of partnerships inked between stakeholders in the continuous manufacturing market, based on several relevant parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D] type of drug molecule, [E] type of product, [F] scale of operation, and [G] geography.

- Recent Expansions: An in-depth analysis of expansions reported in the continuous manufacturing market, based on several relevant parameters, [A] year of expansion, [B] type of expansion, [C] scale of operation, [D] type of drug molecule, [E] type of product, [F] amount invested, and [G] facility area.

- Grant Analysis: A detailed analysis of the various grants reported in the continuous manufacturing domain with relevant information across parameters, such as [A] year of grants award, [B] amount awarded, [C] funding institute center, [D] support period, [E] type of grant application, [F] purpose of grant award, [G] activity code, and [H] study section involved.

- Patent Analysis: A detailed analysis of the various patents filed / granted in the continuous manufacturing domain, based on various mbols, [E] type of applicant, and [F] patent benchmarking analysis. parameters, such as [A] patent publication year, [B] patent application year, [C] patent jurisdiction, [D] CPC Sy

- Gaps Associated with Continuous Bioprocessing: A detailed overview of various technology gaps related to continuous downstream bioprocessing that are currently preventing its implementation, including gaps related to bioburden control, continuous multi-column chromatography, continuous viral inactivation process, continuous viral filtration process, continuous ultrafiltration / diafiltration, continuous buffer supply considerations and continuous monitoring of downstream process.

- Initiatives of Companies with In-House Continuous Capabilities: An overview of various initiatives taken by the leading pharmaceutical companies (in terms of revenues), covering both partnered as well as in-house projects.

- Case Study - Continuous Manufacturing Equipment for Biologics: A case study of the companies offering technologies / equipment that can potentially be used in continuous manufacturing of biologics, providing information on the [A] geographical location of potential stakeholders and [B] the type of technology / equipment provided.

- Case Study - Roadmap for the Adoption of Continuous Manufacturing Processes: A case study on the roadmap for the adoption of continuous manufacturing technique, discussing different strategies that can be followed by the company in order to adopt this technology or transition from batch manufacturing to continuous manufacturing.

- Case Study - Modular Facilities in Pharmaceutical / Biotechnology Industry: A brief description on the concept of modularization, types of modules used in modular buildings and an overview of the modular building construction process

- Capacity Analysis: A detailed analysis on the global installed continuous upstream bioprocessing capacity and global installed continuous small molecule API manufacturing capacity of various small, mid-sized, large, and very large companies engaged in this domain based on parameters such as [A] company size, [B] scale of operation, [C] type of player and [D] key geographical regions.

- Market Impact Analysis: A thorough analysis of various factors, such as [A] drivers, [B] restraints, [C] opportunities, and [D] existing challenges that are likely to impact market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Historical Evolution of Continuous Manufacturing

- 6.3. Continuous Manufacturing in the Pharmaceutical Industry

- 6.3.1. Regulatory Landscape

- 6.3.2. Early Adopters of Continuous Manufacturing

- 6.3.3. Anticipated Shift to Continuous Manufacturing

- 6.3.4. Batch Manufacturing versus Continuous Manufacturing

- 6.3.5. Key Challenges Associated with Continuous Manufacturing

- 6.3.6. Future Perspectives

SECTION III: MARKET OVERVIEW

7. MARKET LANDSCAPE: BIOLOGICS CONTINUOUS MANUFACTURERS

- 7.1. Chapter Overview

- 7.2. Biologics Continuous Manufacturers: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Type of Player

- 7.2.5. Analysis by Scale of Operation

- 7.2.6. Analysis by Type of Biologic Manufactured

- 7.2.7. Analysis by Type of Product Manufactured

- 7.2.8. Analysis by Location of Continuous Manufacturing Facilities

- 7.2.9. Analysis by Type of Continuous Manufacturing Facility

- 7.2.10. Analysis by Stage of Bioprocessing

- 7.2.11. Analysis by Stage of Upstream Bioprocessing

- 7.2.12. Analysis by Stage of Downstream Bioprocessing

- 7.2.13. Analysis by Quality Certificates Obtained

- 7.2.14. Analysis by Range of Installed Capacity

8. COMPANY COMPETITIVENESS ANALYSIS: CONTINUOUS BIOLOGIC MANUFACTURERS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Company Competitiveness Analysis: Continuous Biologics Manufacturers

- 8.4.1. Biologics Continuous Manufacturers based in North America

- 8.4.2. Biologics Continuous Manufacturers based in Europe

- 8.4.3. Biologics Continuous Manufacturers based in Asia-Pacific

9. MARKET LANDSCAPE: SMALL MOLECULES CONTINUOUS MANUFACTURERS

- 9.1. Chapter Overview

- 9.2. Small Molecule Continuous Manufacturers: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Type of Player

- 9.2.5. Analysis by Scale of Operation

- 9.2.6. Analysis by Type of Dosage Form

- 9.2.7. Analysis by Type of Product Manufactured

- 9.2.8. Analysis by Location of Continuous Manufacturing Facilities

- 9.2.9. Analysis by Type of Continuous Manufacturing Process

- 9.2.10. Analysis by Stage of API Manufacturing

- 9.2.11. Analysis by Stage of FDF Manufacturing

- 9.2.12. Analysis by Quality Certificates Obtained

10. COMPANY COMPETITIVENESS ANALYSIS: CONTINUOUS SMALL MOLECULE MANUFACTURERS

- 10.1. Chapter Overview

- 10.2. Assumptions and Key Parameters

- 10.3. Methodology

- 10.4. Company Competitiveness Analysis: Continuous Small Molecule Manufacturers

- 10.4.1. Small Molecules Continuous Manufacturers based in North America

- 10.4.2. Small Molecules Continuous Manufacturers based in Europe

- 10.4.3. Small Molecules Continuous Manufacturers based in Asia-Pacific

SECTION IV: COMPANY PROFILES

11. COMPANY PROFILES: CONTINUOUS MANUFACTURING SERVICE PROVIDERS BASED IN NORTH AMERICA

- 11.1. Chapter Overview

- 11.2. AbbVie Contract Manufacturing

- 11.2.1. Company Overview

- 11.2.2. Financial Information

- 11.2.3. Continuous Manufacturing Service Portfolio

- 11.2.4. Continuous Manufacturing Facilities

- 11.2.5. Recent Developments and Future Outlook

- 11.3. Abzena

- 11.3.1. Company Overview

- 11.3.2. Continuous Manufacturing Service Portfolio

- 11.3.3. Continuous Manufacturing Facilities

- 11.3.4. Recent Developments and Future Outlook

- 11.4. AGC Biologics

- 11.4.1. Company Overview

- 11.4.2. Financial Information

- 11.4.3. Continuous Manufacturing Service Portfolio

- 11.4.4. Continuous Manufacturing Facilities

- 11.4.5. Recent Developments and Future Outlook

- 11.5. Phlow

- 11.5.1. Company Overview

- 11.5.2. Continuous Manufacturing Service Portfolio

- 11.5.3. Continuous Manufacturing Facilities

- 11.5.4. Recent Developments and Future Outlook

12. COMPANY PROFILES: CONTINUOUS MANUFACTURING SERVICE PROVIDERS BASED IN EUROPE

- 12.1. Chapter Overview

- 12.2. Boehringer Ingelheim

- 12.2.1. Company Overview

- 12.2.2. Financial Information

- 12.2.3. Continuous Manufacturing Service Portfolio

- 12.2.4. Continuous Manufacturing Facilities

- 12.2.5. Recent Developments and Future Outlook

- 12.3. Corden Pharma

- 12.3.1. Company Overview

- 12.3.2. Continuous Manufacturing Service Portfolio

- 12.3.3. Continuous Manufacturing Facilities

- 12.3.4. Recent Developments and Future Outlook

- 12.4. Glatt

- 12.4.1. Company Overview

- 12.4.2. Continuous Manufacturing Service Portfolio

- 12.4.3. Continuous Manufacturing Facilities

- 12.4.4. Recent Developments and Future Outlook

13. COMPANY PROFILES: CONTINUOUS MANUFACTURING SERVICE PROVIDERS BASED IN ASIA-PACIFIC

- 13.1. Chapter Overview

- 13.2. Kaneka

- 13.2.1. Company Overview

- 13.2.2. Financial Information

- 13.2.3. Continuous Manufacturing Service Portfolio

- 13.2.4. Continuous Manufacturing Facilities

- 13.2.5. Recent Developments and Future Outlook

- 13.3. WuXi Biologics

- 13.3.1. Company Overview

- 13.3.2. Financial Information

- 13.3.3. Continuous Manufacturing Service Portfolio

- 13.3.4. Continuous Manufacturing Facilities

- 13.3.5. Recent Developments and Future Outlook

SECTION V: MARKET TRENDS

14. PARTNERSHIPS AND COLLABORATIONS

- 14.1. Chapter Overview

- 14.2. Partnership Models

- 14.3. Continuous Manufacturing: Partnerships and Collaborations

- 14.3.1. Analysis by Year of Partnership

- 14.3.2. Analysis by Type of Partnership

- 14.3.3. Analysis by Year and Type of Partnership

- 14.3.4. Analysis by Type of Partner

- 14.3.5. Analysis by Type of Drug Molecule

- 14.3.6. Analysis by Type of Product

- 14.3.7. Analysis by Scale of Operation

- 14.3.8. Most Active Players: Analysis by Number of Partnerships

- 14.3.9. Analysis by Geography

- 14.3.9.1. Analysis by Country

- 14.3.9.2. Analysis by Continent

15. RECENT EXPANSIONS

- 15.1. Chapter Overview

- 15.2. Continuous Manufacturing: Recent Expansions

- 15.2.1. Analysis by Year of Expansion

- 15.2.2. Analysis by Type of Expansion

- 15.2.3. Analysis by Year and Type of Expansion

- 15.2.4. Analysis by Scale of Operation

- 15.2.5. Analysis by Type of Expansion and Scale of Operation

- 15.2.6. Analysis by Type of Drug Molecule

- 15.2.7. Analysis by Type of Expansion and Type of Drug Molecule

- 15.2.8. Analysis by Type of Product

- 15.2.9. Analysis by Amount Invested

- 15.2.10. Analysis by Facility Area

- 15.2.11. Most Active Players: Analysis by Number of Recent Expansions

- 15.2.12. Analysis by Location of Expansion

- 15.2.12.1. Analysis by Country

- 15.2.12.2. Analysis by Continent

- 15.2.13. Analysis by Location of Expansion (Continent) and Type of Expansion

16. GRANT ANALYSIS

- 16.1. Chapter Overview

- 16.2. Scope and Methodology

- 16.3. Continuous Manufacturing: Grants Analysis

- 16.3.1. Analysis by Year of Grants Award

- 16.3.2. Analysis by Amount Awarded

- 16.3.3. Analysis by Funding Institute Center

- 16.3.4. Analysis by Support Period

- 16.3.5. Analysis by Type of Grant Application

- 16.3.6. Analysis by Purpose of Grant Award

- 16.3.7. Analysis by Activity Code

- 16.3.8. Analysis by Study Section Involved

- 16.3.9. Popular NIH Departments: Analysis by Number of Grants

- 16.3.10. Analysis by Type of Recipient Organization

- 16.3.11. Prominent Program Officers: Analysis by Number of Grants

- 16.3.12. Popular Recipient Organizations: Analysis by Number of Grants

- 16.3.13. Popular Recipient Organizations: Analysis by Grant Amount

- 16.3.14. Analysis by Region of Recipient Organization

17. PATENT ANALYSIS

- 17.1. Chapter Overview

- 17.2. Scope and Methodology

- 17.3. Continuous Manufacturing: Patent Analysis

- 17.3.1. Analysis by Patent Publication Year

- 17.3.2. Analysis by Type of Patent and Publication Year

- 17.3.3. Analysis by Patent Application Year

- 17.3.4. Analysis by Patent Jurisdiction

- 17.3.5. Analysis by CPC Symbols

- 17.3.6. Analysis by Type of Applicant

- 17.3.7. Leading Industry Players: Analysis by Number of Patents

- 17.3.8. Leading Non-Industry Players: Analysis by Number of Patents

- 17.4. Patent Benchmarking Analysis

- 17.4.1. Analysis by Patent Characteristics

- 17.5. Patent Valuation

- 17.6. Leading Patents by Number of Citations

18. GAPS ASSOCIATED WITH CONTINUOUS BIOPROCESSING

- 18.1. Chapter Overview

- 18.2. Technological Gaps in Continuous Bioprocessing

- 18.2.1. Gaps related to Bioburden Control

- 18.2.2. Gaps related to Continuous Multi Column Chromatography

- 18.2.2.1. Continuous Chromatography Systems

- 18.2.2.2. Continuous Protein A Chromatography

- 18.2.2.3. Continuous Anion Exchange Chromatography

- 18.2.2.4. Continuous Flow-Through Processing

- 18.2.2.5. Continuous Chromatography Media

- 18.2.3. Gaps related to Continuous Viral Inactivation

- 18.2.3.1. Continuous Viral Inactivation in a Tubular Reactor

- 18.2.3.2. Continuous Viral Inactivation Through Column Chromatography

- 18.2.3.3. Continuous Viral Inactivation using Alternating Hold-Bags

- 18.2.4. Gaps related to Continuous Viral Filtration

- 18.2.5. Gaps related to Continuous Ultrafiltration / Diafiltration

- 18.2.6. Gaps related to Continuous Buffer Supply

- 18.2.7. Gaps related to Continuous On-line Monitoring

- 18.3. Other Gaps Associated with Continuous Bioprocessing

- 18.3.1. Gaps Related to Single-Use Technologies

- 18.3.2. Gaps Related to Process Automation

- 18.3.3. Regulatory Requirements

- 18.4. Concluding Remarks

19. INITIATIVES OF COMPANIES WITH IN-HOUSE CONTINUOUS CAPABILITIES

- 19.1. Chapter Overview

- 19.2. Continuous Manufacturing Initiatives undertaken by Leading Companies

- 19.2.1. Amgen

- 19.2.1.1. In-House Initiatives

- 19.2.2. Boehringer Ingelheim

- 19.2.2.1. In-House Initiatives

- 19.2.3. Bristol-Myers Squibb

- 19.2.3.1. In-House Initiatives

- 19.2.3.2. Partnered Initiatives

- 19.2.4. GSK

- 19.2.4.1. In-House Initiatives

- 19.2.4.2. Partnered Initiatives

- 19.2.5. Merck KGaA

- 19.2.5.1. In-House Initiatives

- 19.2.5.2. Partnered Initiatives

- 19.2.6. Novartis

- 19.2.6.1. In-House Initiatives

- 19.2.6.2. Partnered Initiatives

- 19.2.7. Pfizer

- 19.2.7.1. In-House Initiatives

- 19.2.7.2. Partnered Initiatives

- 19.2.8. Sanofi

- 19.2.8.1. In-House Initiatives

- 19.2.8.2. Partnered Initiatives

- 19.2.1. Amgen

20. CASE STUDY 1: CONTINUOUS MANUFACTURING EQUIPMENT FOR BIOLOGICS

- 20.1. Chapter Overview

- 20.2. Biologics Continuous Manufacturing Equipment: Overall Market Landscape

- 20.2.1. Analysis by Type of Equipment

- 20.2.2. Analysis by Type of Manufacturing Process

- 20.2.3. Analysis by Stage of Bioprocessing

- 20.2.4. Analysis by Scale of Operation

- 20.3. Biologics Continuous Manufacturing Equipment: Developer Landscape

- 20.3.1. Analysis by Year of Establishment

- 20.3.2. Analysis by Company Size

- 20.3.3. Analysis by Location of Headquarters

- 20.3.4. Most Active Players: Analysis by Number of Biologics Continuous Manufacturing Equipment Offered

21. CASE STUDY 2: ROADMAP FOR THE ADOPTION OF CONTINUOUS MANUFACTURING PROCESSES

- 21.1. Chapter Overview

- 21.2. Challenges Associated with the Adoption of Continuous Manufacturing Processes

- 21.3. Key Strategies for the Adoption of Continuous Manufacturing Processes

- 21.3.1. Phase I: Process Development and Implementation

- 21.3.2. Phase II: Equipment / Technology Development and Installation

- 21.3.3. Phase III: Facility / Plant Development and Establishment

- 21.3.4. Phase IV: Product Development and Manufacturing

22. CASE STUDY 3: MODULAR FACILITIES IN PHARMACEUTICAL / BIOTECHNOLOGY INDUSTRY

- 22.1. Chapter Overview

- 22.2. Historical Background

- 22.3. The Concept of Modularization

- 22.3.1. Types of Modular Constructs

- 22.3.2. Modular Construction Process

- 22.4. Modular Construction in the Pharmaceutical Industry

- 22.4.1. Advantages of Modular Construction in the Pharmaceutical Industry

- 22.5. Modular Facility Manufacturers

- 22.5.1. Analysis by Type of Industry Served

- 22.5.2. Analysis by Geographical Coverage

- 22.5.3. Analysis by Type of Modular Construction

- 22.6. Modular Pharmaceutical Cleanrooms

- 22.6.1. Cleanroom Classifications and Current Standards

- 22.6.2. Regulations and Standards Concerning Modular Cleanroom Construction

- 22.6.3. Advantages of Modular Cleanrooms

- 22.7. Modular Cleanroom Providers

- 22.7.1. Analysis by Year of Establishment

- 22.7.2. Analysis by Location of Headquarters

- 22.7.3. Analysis by Type of Modular Cleanroom Offered

- 22.8. Conclusion

23. CAPACITY ANALYSIS: CONTINUOUS BIOLOGIC MANUFACTURERS

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.2.1. Analysis by Range of Installed Capacity

- 23.2.2. Analysis by Company Size

- 23.2.3. Analysis by Scale of Operation

- 23.2.4. Analysis by Type of Player

- 23.2.5. Analysis by Location of Biologics Continuous Manufacturing Facility

- 23.2.5.1. Analysis of Biologics Continuous Manufacturing Capacity Installed in North America

- 23.2.5.2. Analysis of Biologics Continuous Manufacturing Capacity Installed in Europe

- 23.2.5.3. Analysis of Biologics Continuous Manufacturing Capacity Installed in Asia-Pacific

- 23.2.6. Concluding Remarks

24. CAPACITY ANALYSIS: CONTINUOUS SMALL MOLECULES MANUFACTURERS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.2.1. Analysis by Range of Installed Capacity

- 24.2.2. Analysis by Company Size

- 24.2.3. Analysis by Scale of Operation

- 24.2.4. Analysis by Type of Player

- 24.2.5. Analysis by Location of Small Molecules Continuous Manufacturing Facility

- 24.2.5.1. Analysis of Small Molecules Continuous Manufacturing Capacity Installed in North America

- 24.2.5.2. Analysis of Small Molecules Continuous Manufacturing Capacity Installed in Europe

- 24.2.5.3. Analysis of Small Molecules Continuous Manufacturing Capacity Installed in Asia-Pacific

- 24.2.6. Concluding Remarks

SECTION VI: MARKET FORECAST AND OPPORTUNITY ANALYSIS

25. GLOBAL CONTINUOUS MANUFACTURING MARKET

- 25.1. Chapter Overview

- 25.2. Assumptions and Methodology

- 25.3. Global Continuous Manufacturing Market, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 25.3.1. Scenario Analysis

- 25.3.1.1. Conservative Scenario

- 25.3.1.2. Optimistic Scenario

- 25.3.1. Scenario Analysis

- 25.4. Key Market Segmentations

26. CONTINUOUS MANUFACTURING MARKET, BY TYPE OF DRUG MOLECULE

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Continuous Manufacturing Market: Distribution by Type of Drug Molecule

- 26.3.1. Continuous Manufacturing Market for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.1.1. Biologics Continuous Manufacturing Market for Upstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.1.2. Biologics Continuous Manufacturing Market for Downstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.2. Continuous Manufacturing Market for Small Molecules, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.2.1. Small Molecules Continuous Manufacturing Market for Active Pharmaceutical Ingredients, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.2.2. Small Molecules Continuous Manufacturing Market for Finished Dosage Forms, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.3.1. Continuous Manufacturing Market for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 26.4. Data Triangulation and Validation

27. CONTINUOUS MANUFACTURING MARKET, BY SCALE OF OPERATION

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Biologics Continuous Manufacturing Market: Distribution by Scale of Operation

- 27.3.1. Biologics Continuous Manufacturing Market for Preclinical / Clinical Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 27.3.2. Biologics Continuous Manufacturing Market for Commercial Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 27.4. Small Molecules Continuous Manufacturing Market: Distribution by Scale of Operation

- 27.4.1. Small Molecules Continuous Manufacturing Market for Preclinical / Clinical Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 27.4.2. Small Molecules Continuous Manufacturing Market for Commercial Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 27.5. Data Triangulation and Validation

28. CONTINUOUS MANUFACTURING MARKET, BY PURPOSE OF MANUFACTURING

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Biologics Continuous Manufacturing Market: Distribution by Purpose of Manufacturing

- 28.3.1. Biologics Continuous Manufacturing Market for Contract Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.3.2. Biologics Continuous Manufacturing Market for In-house Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.3.3. Biologics Continuous Manufacturing Market for Both, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.4. Small Molecules Continuous Manufacturing Market: Distribution by Purpose of Manufacturing

- 28.4.1. Small Molecules Continuous Manufacturing Market for Contract Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.4.2. Small Molecules Continuous Manufacturing Market In-house Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.4.3. Small Molecules Continuous Manufacturing Market for Both, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 28.5. Data Triangulation and Validation

29. CONTINUOUS MANUFACTURING MARKET, BY COMPANY SIZE

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Biologics Continuous Manufacturing Market: Distribution by Company Size

- 29.3.1. Biologics Continuous Manufacturing Market for Small Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.3.2. Biologics Continuous Manufacturing Market for Mid-sized Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.3.3. Biologics Continuous Manufacturing Market for Large Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.4. Small Molecules Continuous Manufacturing Market: Distribution by Company Size

- 29.4.1. Small Molecules Continuous Manufacturing Market for Small Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.4.2. Small Molecules Continuous Manufacturing Market for Mid-sized Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.4.3. Small Molecules Continuous Manufacturing Market for Large Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 29.5. Data Triangulation and Validation

30. CONTINUOUS MANUFACTURING MARKET, BY KEY GEOGRAPHICAL REGIONS

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Biologics Continuous Manufacturing Market: Distribution by Key Geographical Regions

- 30.3.1. Biologics Continuous Manufacturing Market in North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.1.1. Biologics Continuous Manufacturing Market in the US, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.1.2. Biologics Continuous Manufacturing Market in Puerto Rico, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2. Biologics Continuous Manufacturing Market in Europe, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.1. Biologics Continuous Manufacturing Market in Germany, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.2. Biologics Continuous Manufacturing Market in Switzerland, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.3. Biologics Continuous Manufacturing Market in Belgium, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.4. Biologics Continuous Manufacturing Market in Ireland, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.5. Biologics Continuous Manufacturing Market in France, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.2.6. Biologics Continuous Manufacturing Market in Rest of Europe, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3. Biologics Continuous Manufacturing Market in Asia-Pacific, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.1. Biologics Continuous Manufacturing Market in China, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.2. Biologics Continuous Manufacturing Market in South Korea, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.3. Biologics Continuous Manufacturing Market in Singapore, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.4. Biologics Continuous Manufacturing Market in Taiwan, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.5. Biologics Continuous Manufacturing Market in India, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.6. Biologics Continuous Manufacturing Market in Japan, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.3.7. Biologics Continuous Manufacturing Market in Australia, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.3.1. Biologics Continuous Manufacturing Market in North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4. Small Molecules Continuous Manufacturing Market: Distribution by Key Geographical Regions, 2018, Current Year and 2040

- 30.4.1. Small Molecules Continuous Manufacturing Market in North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.1.1. Small Molecules Continuous Manufacturing Market in the US, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.1.2. Small Molecules Continuous Manufacturing Market in Mexico, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2. Small Molecules Continuous Manufacturing Market in Europe, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.1. Biologics Continuous Manufacturing Market in Germany, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.2. Small Molecules Continuous Manufacturing Market in the UK, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.3. Small Molecules Continuous Manufacturing Market in Italy, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.4. Small Molecules Continuous Manufacturing Market in Switzerland, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.5. Small Molecules Continuous Manufacturing Market in France, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.6. Small Molecules Continuous Manufacturing Market in Belgium, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.2.7. Small Molecules Continuous Manufacturing Market in Rest of Europe, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3. Small Molecules Continuous Manufacturing Market in Asia-Pacific, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3.1. Small Molecules Continuous Manufacturing Market in China, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3.2. Small Molecules Continuous Manufacturing Market in Japan, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3.3. Small Molecules Continuous Manufacturing Market in Singapore, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3.4. Small Molecules Continuous Manufacturing Market in South Korea, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.3.5. Small Molecules Continuous Manufacturing Market in India, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.4.1. Small Molecules Continuous Manufacturing Market in North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 30.5. Data Triangulation and Validation

SECTION VII: MARKET OPPORTUNITY ANALYSIS WITHIN GEOGRAPHICAL REGIONS

31. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

- 31.1. Continuous Manufacturing Market in North America: Distribution by Type of Drug Molecule

- 31.1.1. Continuous Manufacturing Market in North America for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.1.1. Biologics Continuous Manufacturing Market in North America for Upstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.1.2. Biologics Continuous Manufacturing Market in North America for Downstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.2. Continuous Manufacturing Market in North America for Small Molecules, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.2.1. Small Molecules Continuous Manufacturing Market in North America for Active Pharmaceutical Ingredients, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.2.2. Small Molecules Continuous Manufacturing Market in North America for Finished Dosage Forms, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.1.1. Continuous Manufacturing Market in North America for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.2. Continuous Manufacturing Market in North America: Distribution by Scale of Operation

- 31.2.1. Biologics Continuous Manufacturing Market in North America for Preclinical / Clinical Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.2.2. Biologics Continuous Manufacturing Market in North America for Commercial Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.2.3. Small Molecules Continuous Manufacturing Market in North America for Preclinical / Clinical Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.2.4. Small Molecules Continuous Manufacturing Market in North America for Commercial Scale Operations, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3. Continuous Manufacturing Market in North America: Distribution by Purpose of Manufacturing

- 31.3.1. Biologics Continuous Manufacturing Market in North America for Contract Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3.2. Biologics Continuous Manufacturing Market in North America for In-House Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3.3. Biologics Continuous Manufacturing Market in North America for Both, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3.4. Small Molecules Continuous Manufacturing Market in North America for Contract Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3.5. Small Molecules Continuous Manufacturing Market in North America for In-House Manufacturing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.3.6. Small Molecules Continuous Manufacturing Market in North America for Both, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4. Continuous Manufacturing Market in North America: Distribution by Company Size

- 31.4.1. Biologics Continuous Manufacturing Market in North America for Small Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4.2. Biologics Manufacturing Market in North America for Mid-sized Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4.3. Biologics Manufacturing Market in North America for Large Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4.4. Small Molecules Continuous Manufacturing Market in North America for Small Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4.5. Small Molecules Manufacturing Market in North America for Mid-sized Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 31.4.6. Small Molecules Manufacturing Market in North America for Large Companies, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

32. MARKET OPPORTUNITY ANALYSIS: EUROPE

- 32.1. Continuous Manufacturing Market in Europe: Distribution by Type of Drug Molecule

- 32.1.1. Continuous Manufacturing Market in Europe for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 32.1.1.1. Biologics Continuous Manufacturing Market in Europe for Upstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 32.1.1.2. Biologics Continuous Manufacturing Market in Europe for Downstream Bioprocessing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 32.1.2. Continuous Manufacturing Market in Europe for Small Molecules, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 32.1.2.1. Small Molecules Continuous Manufacturing Market in Europe for Active Pharmaceutical Ingredients, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 32.1.1. Continuous Manufacturing Market in Europe for Biologics, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)