|

시장보고서

상품코드

1883717

알루미늄 합금 시장 : 합금 유형별, 형상별, 제조 기술별, 프로세스별, 시리즈별, 강도별, 최종 사용자 산업별, 지역별(-2035년)Aluminum Alloys Market, Till 2035- Distribution by Type of Alloy, Type of Form, Type of Production Technique, Type of Process, Type of Series, Type of Strength, End Use Industry, and Geographical Regions: Industry Trends and Global Forecasts |

||||||

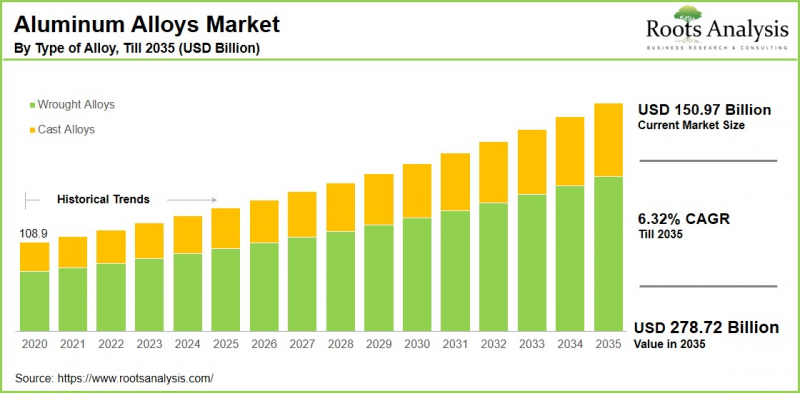

Roots Analysis의 조사에 따르면, 세계의 알루미늄 합금 시장 규모는 현재 1,509억 7,000만 달러로 평가되었고, 2035년까지 2,787억 2,000만 달러로 성장할 전망이며, 예측 기간 동안 CAGR 6.32%로 추정됩니다.

알루미늄 합금 시장 기회 : 분류

합금 유형별

- 주조 합금

- 단조 합금

형상별

- 호일

- 플레이트

- 시트

시리즈별

- 1000 시리즈

- 2000 시리즈

- 3000 시리즈

- 4000 시리즈

- 5000 시리즈

- 6000 시리즈

- 7000 시리즈

- 8000 시리즈

강도별

- 고강도

- 초고강도

제조 기술별

- 고압 다이캐스트

- 저압 다이캐스트

- 로스트 왁스 주조

- 금형 주조(영구형 주조)

- 모래 주조

프로세스별

- 주조

- 압출

- 단조

- 압연

- 기타

최종 사용자 산업별

- 항공우주 및 방위

- 자동차

- 건축 및 건설

- 내구 소비재

- 전기 및 전자 기기

- 포장

- 기타

지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미 국가

- 유럽

- 오스트리아

- 벨기에

- 덴마크

- 프랑스

- 독일

- 아일랜드

- 이탈리아

- 네덜란드

- 노르웨이

- 러시아

- 스페인

- 스웨덴

- 스위스

- 영국

- 기타 유럽 국가

- 아시아

- 중국

- 인도

- 일본

- 싱가포르

- 한국

- 기타 아시아 국가

- 라틴아메리카

- 브라질

- 칠레

- 콜롬비아

- 베네수엘라

- 기타 라틴아메리카 국가

- 중동 및 북아프리카

- 이집트

- 이란

- 이라크

- 이스라엘

- 쿠웨이트

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 북아프리카 국가

- 세계 기타 지역

- 호주

- 뉴질랜드

- 기타 국가들

알루미늄 합금 시장 : 성장 및 동향

알루미늄 합금이란 알루미늄을 주성분으로 하여 구리, 마그네슘, 망간, 규소, 주석, 니켈, 아연 등의 원소를 첨가하여 기계적 및 물리적 특성을 향상시킨 금속 조성물입니다. 알루미늄 합금은 기술 진보 및 지속가능성 요구에 적응하는 탁월한 능력을 특징으로 합니다. 세계 산업이 더 가볍고 강력하고 에너지 효율적인 재료를 추구하면서 알루미늄 합금은 최첨단 엔지니어링에서 우선적으로 선택되는 옵션으로 부상하고 있습니다.

이러한 합금은 강화된 강도, 우수한 내식성, 가공성 향상, 맞춤형 전기 전도성 등 특정 특성을 제공하도록 설계되었으며 항공우주, 자동차, 건설 및 CE 제품에 이르기까지 다양한 용도에 필수적인 존재입니다. 특히 전기자동차 및 재생에너지 인프라 등 내구성과 성능이 중요한 분야에서는 우수한 강도 중량비와 내식성이 높게 평가되고 있습니다.

알루미늄 합금의 또 다른 중요한 측면은 순환 경제의 원칙과 첨단 제조 기술에 대응할 수 있다는 것입니다. 이러한 합금의 재활용 가능성은 세계적인 지속가능성 목표를 뒷받침하며, 부가 제조 및 AI 기반 품질 관리와 같은 가공 방법의 진보가 알루미늄의 가능성의 한계를 밀고 있습니다.

실제로 많은 연구에서 지적한 바와 같이 특성 열화 없이 알루미늄 합금을 재활용할 수 있는 능력은 환경 부하의 경감 및 클로즈드 루프 생산 모델의 채용을 목표로 하는 산업에 있어서 혁신적인 기회가 됩니다. 이 성능, 적응성, 지속가능성의 조합은 알루미늄 합금 시장을 21세기 산업 변혁에서 중요한 추진력으로 자리매김하고 있습니다. 이상의 요인을 고려하면, 알루미늄 합금 시장은 예측 기간 동안 꾸준한 성장이 예상됩니다.

이 보고서는 세계의 알루미늄 합금 시장을 조사했으며, 시장 개요, 배경, 시장 영향요인 분석, 시장 규모 추이 및 예측, 각종 구분, 지역별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

섹션 I : 보고서 개요

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 거시경제지표

섹션 II : 정성적 인사이트

제5장 주요 요약

제6장 서문

제7장 규제 시나리오

섹션 III : 시장 개요

제8장 주요 기업의 종합적 데이터베이스

제9장 경쟁 구도

제10장 화이트 스페이스 분석

제11장 기업의 경쟁력 분석

제12장 스타트업 생태계 분석

섹션 IV : 기업 프로파일

제13장 기업 프로파일

- 장의 개요

- Aleris

- Alcoa

- Aluminium Bahrain

- Aluminium Corporation of China

- AMG ALUMINUM

- Arconic

- Century Aluminum

- China Hestego

- China Hongqiao

- Constellium

- Emirates Global Aluminum

- Extruded Solutions

- Hindalco

- Hydro

- Kaiser Aluminum

- National Aluminum Company

- Novelis

- Norsk Hydro

- Press Metal

- Rio Tinto

- RusAL

- Shandong Nanshan Aluminum

- Shandong Sino Aluminum

- South32

- Southwest Aluminum

- UACJ

- Vedanta Aluminium &Power

섹션 V : 시장 동향

제14장 메가트렌드 분석

제15장 언멧 요구 분석

제16장 특허 분석

제17장 최근 동향

섹션 VI : 시장 기회 분석

제18장 세계의 알루미늄 합금 시장

제19장 합금 유형별 시장 기회

제20장 형상별 시장 기회

제21장 시리즈별 시장 기회

제22장 강도별 시장 기회

제23장 제조 기술별 시장 기회

제24장 프로세스별 시장 기회

제25장 최종 사용자 산업별 시장 기회

제26장 북미의 알루미늄 합금 시장 기회

제27장 유럽의 알루미늄 합금 시장 기회

제28장 아시아의 알루미늄 합금 시장 기회

제29장 중동 및 아프리카의 알루미늄 합금 시장 기회

제30장 라틴아메리카의 알루미늄 합금 시장 기회

제31장 세계 기타 지역의 알루미늄 합금 시장 기회

제32장 시장 집중 분석 : 주요 기업별 분포

제33장 인접 시장 분석

섹션 VII : 전략 도구

제34장 승리의 열쇠가 되는 전략

제35장 Porter's Five Forces 분석

제36장 SWOT 분석

제37장 밸류체인 분석

제38장 ROOTS에 의한 전략 제안

섹션 VIII : 기타 독점적 인사이트

제39장 1차 조사로부터의 인사이트

제40장 보고서의 결론

섹션 IX : 부록

제41장 표 형식 데이터

제42장 기업 및 단체 일람

제43장 커스터마이즈 기회

제44장 ROOTS 구독 서비스

제45장 저자 상세

AJY 25.12.15Aluminum Alloys Market Overview

As per Roots Analysis, the global aluminum alloys market size is estimated to grow from USD 150.97 billion in the current year USD 278.72 billion by 2035, at a CAGR of 6.32% during the forecast period, till 2035.

The opportunity for aluminum alloys market has been distributed across the following segments:

Type of Alloy

- Cast Alloys

- Wrought Alloys

Type of Form

- Foils

- Plates

- Sheets

Type of Series

- 1000 Series

- 2000 Series

- 3000 Series

- 4000 Series

- 5000 Series

- 6000 Series

- 7000 Series

- 8000 Series

Type of Strength

- High Strength

- Ultra-High Strength

Production Technique

- High Pressure Die Casting

- Low Pressure Die Casting

- Investment Casting

- Permanent Mold Casting

- Sand Casting

Type of Process

- Casting

- Extrusion

- Forging

- Rolling

- Others

End Use Industry

- Aerospace & Defense

- Automotive

- Building & Construction

- Consumer Durables

- Electrical & Electronics

- Packaging

- Others

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Aluminum alloys Market: Growth and Trends

Aluminum alloys are metal compositions where aluminum is the main element, mixed with other elements like copper, magnesium, manganese, silicon, tin, nickel, and zinc to improve their mechanical and physical characteristics. The aluminum alloys are distinguished by its exceptional ability to adapt to technological advancements and sustainability requirements. As industries around the globe search for lighter, stronger, and more energy-efficient materials, aluminum alloys have emerged as a preferred choice for cutting-edge engineering.

These alloys are designed to provide specific attributes, including enhanced strength, greater corrosion resistance, improved workability, and customized electrical conductivity, making them essential in various applications ranging from aerospace and automotive to construction and consumer electronics. Their favorable strength-to-weight ratio and resistance to corrosion are especially prized in fields like electric vehicles and renewable energy infrastructure, where durability and performance are critical.

Another key aspect of the aluminum alloys is its ability to respond to the principles of a circular economy and advanced manufacturing techniques. The recyclability of these alloys supports global sustainability objectives, while advancements in processing methods, such as additive manufacturing and AI-based quality control, are pushing the limits of aluminum's potential.

In fact, various researchers point out that the capability to recycle aluminum alloys without degradation of properties represents a transformative opportunity for industries aiming to lessen their environmental impact and adopt closed-loop production models. This combination of performance, adaptability, and sustainability positions the aluminum alloys market as a vital driver of industrial change in the 21st century. As a result, considering the above mentioned factors, the aluminum alloys market is expected to grow at a steady pace during the forecast period.

Aluminum Alloys Market: Key Segments

Market Share by Type of Alloy

Based on type of alloy, the global aluminum alloys market is segmented into cast alloys and wrought alloys. According to our estimates, currently, the wrought alloys segment captures the majority of the market share. This is due to the increasing utilization of wrought alloys in food packaging and consumer goods due to their cost-effectiveness. Additionally, wrought alloys are characterized by a superior strength-to-weight ratio, making them suitable for applications that necessitate both durability and lightweight properties.

On the other hand, the cast aluminum alloys segment is projected to experience a relatively higher CAGR during the forecast period.

Market Share by Type of Form

Based on type of form, the global aluminum alloys market is segmented into foils, plates, and sheets. According to our estimates, currently, the sheets sub-segment captures the majority of the market share. This increase can be attributed to the widespread application of aluminum alloy sheets in the automotive sector, where they play a vital role in reducing the weight of vehicle body panels and structural elements. Additionally, they are utilized in the aerospace industry for fuselage panels and wing skins, and in construction, they serve for roofing, facades, and siding.

On the other hand, the foils segment is anticipated to experience the highest compound annual growth rate (CAGR) throughout the forecast period.

Market Share by Type of Series

Based on type of series, the global aluminum alloys market is segmented into different types. According to our estimates, currently, the 1000 series aluminum alloys capture the majority of the market share. This is due to its high purity along with excellent electrical conductivity and resistance to corrosion. These characteristics support the its extensive application in the chemical and processing sectors.

On the other hand, the foils segment is anticipated to experience the highest compound annual growth rate (CAGR) throughout the forecast period.

Market Share by Type of Strength

Based on type of strength, the global aluminum alloys market is segmented into high strength and ultra-high strength. According to our estimates, currently, the high strength aluminum alloys captures the majority of the market share. This dominance is driven by the increasing need for aluminum alloys across the automotive, aerospace, construction, and marine sectors, where a combination of strength, lightweight properties, and resistance to corrosion is essential for structural integrity and safety features.

Market Share by Production Technique

Based on production technique, the global aluminum alloys market is segmented into high pressure die casting, low pressure die casting, investment casting, permanent mold casting, and sand casting. According to our estimates, currently, the high pressure die casting sub-segment captures the majority of the market share. This growth can be attributed to its capability to efficiently produce complex, high-precision, and high-volume components, particularly within the automotive and electronics industries. Furthermore, the rising implementation of this technique by vehicle manufacturers and producers to satisfy the demand for lightweight, intricate, and cost-efficient parts further propels market expansion.

Market Share by End Use Industry

Based on end use industry, the global aluminum alloys market is segmented into aerospace & defense, automotive, building & construction, consumer durables, electrical & electronics, packaging, and others According to our estimates, currently, the automotive industry sub-segment captures the majority of the market share. This growth can be attributed to automakers' strong emphasis on aluminum alloys to achieve lightweight designs, enhance fuel efficiency, and reduce emissions in their vehicles. Additionally, the essential role of aluminum alloys in constructing vehicle bodies, chassis, and various components further drives market demand.

On the other hand, the packaging sector is anticipated to experience the highest compound annual growth rate (CAGR) during the forecast period.

Market Share by Geographical Regions

Based on geographical regions, the aluminum alloys market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently Asia captures the majority share of the market due to its growing industrialization, urban development, and infrastructure projects. In nations like China and India, the demand for aluminum alloys is primarily driven by their application in construction and manufacturing. Conversely, the market in North America is expected to grow at a higher CAGR during the forecast period.

Example Players in Aluminum Alloys Market

- Aleris

- Alcoa

- Aluminum Bahrain

- Aluminum Corporation of China

- AMG ALUMINUM

- Arconic

- Century Aluminum

- China Hestego

- China Hongqiao

- Constellium

- Emirates Global Aluminum

- Extruded Solutions

- Hindalco

- Hydro

- Kaiser Aluminum

- National Aluminum Company

- Novelis

- Norsk Hydro

- Press Metal

- Rio Tinto

- RusAL

- Shandong Nanshan Aluminum

- Shandong Sino Aluminum

- South32

- Southwest Aluminum

- UACJ

- Vedanta Aluminium & Power

Aluminum Alloys Market: Research Coverage

The report on the aluminum alloys market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the aluminum alloys market, focusing on key market segments, including [A] type of alloy, [B] type of form, [C] type of production technique, [D] type of process, [E] type of series, [F] type of strength, [G] end use industry, and [H] geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the aluminum alloys market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the aluminum alloys market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the aluminum alloys industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the aluminum alloys domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the aluminum alloys market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the aluminum alloys market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the aluminum alloys market.

Key Questions Answered in this Report

- How many companies are currently engaged in aluminum alloys market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Aluminum Alloys Market

- 6.2.1. Types of Aluminum Alloys

- 6.2.2. Alloy Form

- 6.2.3. Advantages of Aluminum Alloys

- 6.2.4. Challenges with Aluminum Alloys

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Aluminum Alloys Market: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Type of Company

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM ANALYSIS

- 12.1. Aluminum Alloys Market: Startup Ecosystem Analysis

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Type of Startup

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Aleris*

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- similar details are presented for other below mentioned companies based on information in the public domain

- 13.3. Alcoa

- 13.4. Aluminium Bahrain

- 13.5. Aluminium Corporation of China

- 13.6. AMG ALUMINUM

- 13.7. Arconic

- 13.8. Century Aluminum

- 13.9. China Hestego

- 13.10. China Hongqiao

- 13.11. Constellium

- 13.12. Emirates Global Aluminum

- 13.13. Extruded Solutions

- 13.14. Hindalco

- 13.15. Hydro

- 13.16. Kaiser Aluminum

- 13.17. National Aluminum Company

- 13.18. Novelis

- 13.19. Norsk Hydro

- 13.20. Press Metal

- 13.21. Rio Tinto

- 13.22. RusAL

- 13.23. Shandong Nanshan Aluminum

- 13.24. Shandong Sino Aluminum

- 13.25. South32

- 13.26. Southwest Aluminum

- 13.27. UACJ

- 13.28. Vedanta Aluminium & Power

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. UNMET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

18. GLOBAL ALUMINUM ALLOYS MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Aluminum Alloys Market, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF ALLOY

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Aluminum Alloys Market for Cast Alloys: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.7. Aluminum Alloys Market for Wrought Alloys: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 19.8. Data Triangulation and Validation

- 19.8.1. Secondary Sources

- 19.8.2. Primary Sources

- 19.8.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF FORM

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Aluminum Alloys Market for Foils: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.7. Aluminum Alloys Market for Plates: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.8. Aluminum Alloys Market for Sheets: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 20.9. Data Triangulation and Validation

- 20.9.1. Secondary Sources

- 20.9.2. Primary Sources

- 20.9.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF SERIES

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Aluminum Alloys Market for 1000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.7. Aluminum Alloys Market for 2000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.8. Aluminum Alloys Market for 3000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.9. Aluminum Alloys Market for 4000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.10. Aluminum Alloys Market for 5000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.11. Aluminum Alloys Market for 6000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.12. Aluminum Alloys Market for 7000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.13. Aluminum Alloys Market for 8000 Series: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 21.14. Data Triangulation and Validation

- 21.14.1. Secondary Sources

- 21.14.2. Primary Sources

- 21.14.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON TYPE OF STRENGTH

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Aluminum Alloys Market for High Strength: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.7. Aluminum Alloys Market for Ultra-High Strength: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 22.8. Data Triangulation and Validation

- 22.8.1. Secondary Sources

- 22.8.2. Primary Sources

- 22.8.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON PRODUCTION TECHNIQUE

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Aluminum Alloys Market for High Pressure Die Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.7. Aluminum Alloys Market for Low Pressure Die Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.8. Aluminum Alloys Market for Investment Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.9. Aluminum Alloys Market for Permanent Mold Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.10. Aluminum Alloys Market for Sand Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 23.11. Data Triangulation and Validation

- 23.11.1. Secondary Sources

- 23.11.2. Primary Sources

- 23.11.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON TYPE OF PROCESS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Aluminum Alloys Market for Casting: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.7. Aluminum Alloys Market for Extrusion: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.8. Aluminum Alloys Market for Forging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.9. Aluminum Alloys Market for Rolling: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.10. Aluminum Alloys Market for Others: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 24.11. Data Triangulation and Validation

- 24.11.1. Secondary Sources

- 24.11.2. Primary Sources

- 24.11.3. Statistical Modeling

25. MARKET OPPORTUNITIES BASED ON END USE INDUSTRY

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Aluminum Alloys Market for Aerospace & Defense: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.7. Aluminum Alloys Market for Automotive: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.8. Aluminum Alloys Market for Building & Construction: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.9. Aluminum Alloys Market for Consumer Durables: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.10. Aluminum Alloys Market for Electrical & Electronics: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.11. Aluminum Alloys Market for Packaging: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.12. Aluminum Alloys Market for Others: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 25.13. Data Triangulation and Validation

- 25.13.1. Secondary Sources

- 25.13.2. Primary Sources

- 25.13.3. Statistical Modeling

26. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN NORTH AMERICA

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Aluminum Alloys Market in North America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.6.1. Aluminum Alloys Market in the US: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.6.2. Aluminum Alloys Market in Canada: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.6.3. Aluminum Alloys Market in Mexico: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.6.4. Aluminum Alloys Market in Other North American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN EUROPE

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Aluminum Alloys Market in Europe: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.1. Aluminum Alloys Market in Austria: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.2. Aluminum Alloys Market in Belgium: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.3. Aluminum Alloys Market in Denmark: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.4. Aluminum Alloys Market in France: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.5. Aluminum Alloys Market in Germany: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.6. Aluminum Alloys Market in Ireland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.7. Aluminum Alloys Market in Italy: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.8. Aluminum Alloys Market in Netherlands: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.9. Aluminum Alloys Market in Norway: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.10. Aluminum Alloys Market in Russia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.11. Aluminum Alloys Market in Spain: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.12. Aluminum Alloys Market in Sweden: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.13. Aluminum Alloys Market in Switzerland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.14. Aluminum Alloys Market in the UK: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.6.15. Aluminum Alloys Market in Other European Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN ASIA

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Aluminum Alloys Market in Asia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.1. Aluminum Alloys Market in China: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.2. Aluminum Alloys Market in India: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.3. Aluminum Alloys Market in Japan: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.4. Aluminum Alloys Market in Singapore: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.5. Aluminum Alloys Market in South Korea: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.6.6. Aluminum Alloys Market in Other Asian Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN THE MIDDLE EAST AND AFRICA (MEA)

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Aluminum Alloys Market in Middle East and Africa (MEA): Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.1. Aluminum Alloys Market in Egypt: Historical Trends (Since 2020) and Forecasted Estimates (Till 205)

- 29.6.2. Aluminum Alloys Market in Iran: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.3. Aluminum Alloys Market in Iraq: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.4. Aluminum Alloys Market in Israel: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.5. Aluminum Alloys Market in Kuwait: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.6. Aluminum Alloys Market in Saudi Arabia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.7. Aluminum Alloys Market in United Arab Emirates (UAE): Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.6.8. Aluminum Alloys Market in Other MENA Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN LATIN AMERICA

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Revenue Shift Analysis

- 30.4. Market Movement Analysis

- 30.5. Penetration-Growth (P-G) Matrix

- 30.6. Aluminum Alloys Market in Latin America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.1. Aluminum Alloys Market in Argentina: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.2. Aluminum Alloys Market in Brazil: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.3. Aluminum Alloys Market in Chile: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.4. Aluminum Alloys Market in Colombia Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.5. Aluminum Alloys Market in Venezuela: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.6.6. Aluminum Alloys Market in Other Latin American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 30.7. Data Triangulation and Validation

31. MARKET OPPORTUNITIES FOR ALUMINUM ALLOYS IN REST OF THE WORLD

- 31.1. Chapter Overview

- 31.2. Key Assumptions and Methodology

- 31.3. Revenue Shift Analysis

- 31.4. Market Movement Analysis

- 31.5. Penetration-Growth (P-G) Matrix

- 31.6. Aluminum Alloys Market in Rest of the World: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.1. Aluminum Alloys Market in Australia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.2. Aluminum Alloys Market in New Zealand: Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

- 31.6.3. Aluminum Alloys Market in Other Countries

- 31.7. Data Triangulation and Validation

32. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

- 32.1. Leading Player 1

- 32.2. Leading Player 2

- 32.3. Leading Player 3

- 32.4. Leading Player 4

- 32.5. Leading Player 5

- 32.6. Leading Player 6

- 32.7. Leading Player 7

- 32.8. Leading Player 8

33. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

34. KEY WINNING STRATEGIES

35. PORTER'S FIVE FORCES ANALYSIS

36. SWOT ANALYSIS

37. VALUE CHAIN ANALYSIS

38. ROOTS STRATEGIC RECOMMENDATIONS

- 38.1. Chapter Overview

- 38.2. Key Business-related Strategies

- 38.2.1. Research & Development

- 38.2.2. Product Manufacturing

- 38.2.3. Commercialization / Go-to-Market

- 38.2.4. Sales and Marketing

- 38.3. Key Operations-related Strategies

- 38.3.1. Risk Management

- 38.3.2. Workforce

- 38.3.3. Finance

- 38.3.4. Others