|

시장보고서

상품코드

1920860

ADC 세포 독성 페이로드 및 워헤드 시장(제2판) : 동향과 예측(-2035년) - 제품 유형별, 페이로드 유형별, 페이로드 워헤드 하위 카테고리별 및 지역별ADC Cytotoxic Payloads and Warheads Market (2nd Edition): Trends and Forecast Til 2035 - Distribution Type of Product, Type of Payload, Sub-Category of Payload / Warhead and Geographical Regions |

||||||

ADC 세포 독성 페이로드 및 워헤드 시장 - 개요

Roots Analysis에 따르면 ADC 세포 독성 페이로드 및 워헤드 시장 규모는 예측 기간(-2035년)에CAGR 4.9%로 성장할 것으로 보이며, 현재 4억 6,930만 달러에서 2035년까지 7억 2,020만 달러에 이를를 전마입니다.

ADC 세포 독성 페이로드 및 워헤드 시장 - 성장과 동향

항체 약물 복합체(ADC)의 세포독성 제제 및 워헤드는 현대 표적 암 치료의 핵심 요소로, 전반적인 독성을 줄이면서 고효율 화합물을 정확하게 전달하도록 개발되었습니다. 화학적 최적화와 첨단 링커 시스템의 도입을 통해 이러한 페이로드는 ADC의 치료 효능을 향상시켜 제약사가 보다 효율적이고 표적화된 암 치료제를 개발할 수 있게 합니다.

ADC 세포 독성 페이로드 분야는 안전성과 효능 프로필을 향상시키기 위한 페이로드 화학, 접합 기술 및 링커 기술의 발전을 활용하여 빠르게 성장하고 있습니다. ADC 관련 치료제의 혁신과 확장되는 파이프라인에 힘입어 ADC 세포 독성 페이로드 및 워헤드 시장은 상당한 성장을 보이고 있습니다. 세포 독성 페이로드 및 워헤드는 강력한 항암제를 종양 세포에 정확히 전달하고 건강한 조직을 보호함으로써 ADC의 효과에 핵심적 역할을 합니다. ADC가 임상 연구에서 고무적인 결과를 보여주고 종양학 분야 적용에 대한 지속적인 승인을 받으면서 시장 성장이 예상됩니다.

성장 요인 : 시장 확대의 전략적 추진력

링커 안정성, 페이로드 효과성, 표적 전달 시스템의 지속적인 개선은 ADC의 치료 지수를 높이고 있습니다. 이러한 발전으로 연구자들은 건강한 조직에 대한 손상을 줄이면서 종양 제거 효과를 향상시킬 수 있습니다. 이 정밀한 접근법은 혈액암과 고형 종양 모두를 관리하기 위한 종양학 분야의 혁신적인 전략을 주도하고 있습니다.

또한 DNA 손상 화합물 및 미세소관 억제제를 포함한 차세대 페이로드 범주에 대한 수요 증가가 바이오의약품 분야의 상당한 발전을 촉진하고 있습니다. 표적 암 치료에 대한 투자 증가와 접합 기술의 지속적인 발전으로 ADC 세포 독성 페이로드 및 워헤드 시장은 급속한 시장 확장을 경험하고 있습니다. 또한 차세대 다중 탄두 항체-약물 접합체(ADC)의 발전은 기존 ADC 치료법의 단점을 해결함으로써 시장 확장을 크게 촉진할 것으로 예상됩니다.

시장의 과제 : 진전을 막는 심각한 장벽

ADC 세포 독성 페이로드 및 워헤드 개발에는 노출 위험을 완화하기 위한 특수 격리 시설, 엄격한 안전 조치 및 화학 지식이 필요한 극도로 강력하고 위험한 물질의 관리가 요구됩니다. 더욱이 복잡한 접합 방법에서 비롯된 확장성 문제로 인해 이질성, 응집, 안정성 문제 및 대량 생산 시 이상적인 약물-항체 비율(DAR) 달성 장애가 발생합니다. 또한 높은 개발 비용과 원자재 공급망 취약점 역시 시장 확장을 제한합니다.

ADC 세포 독성 페이로드 및 워헤드 시장 - 주요 인사이트

이 보고서는 ADC 세포 독성 페이로드 및 워헤드 시장의 현상을 상세하게 분석하여 업계 내 잠재적 성장 기회를 확인합니다. 주요 조사 결과는 다음과 같습니다.

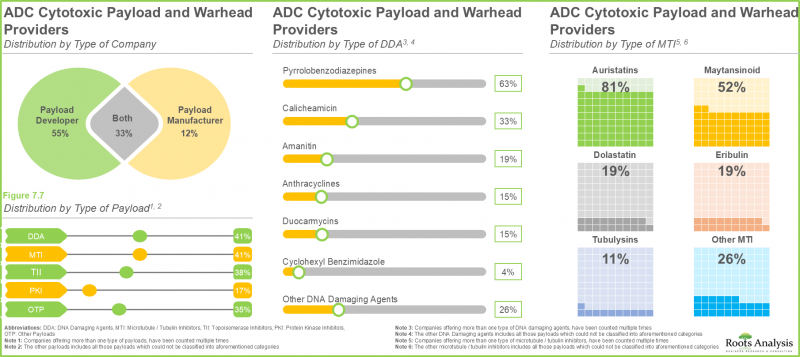

- 현재 시장에는 다양한 치료 분야에서 사용 또는 시험 중인 광범위한 페이로드를 제공한다고 주장하는 약 70개 공급업체가 존재합니다.

- 약 25%의 기업이 피롤로벤조디아제핀(PBZ) 및 아우리스타틴 페이로드를 모두 제공하는데, 이는 이들이 뛰어난 효능을 지니고 분열 중인 세포와 비분열 세포 모두에서 효과적인 세포 사멸을 유도하는 능력이 입증되었기 때문입니다.

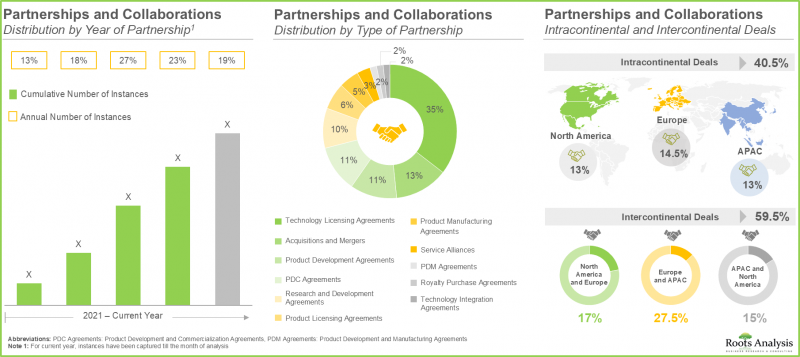

- 최근 다양한 이해관계자들 사이에서 체결된 다수의 파트너십은 이 시장에 대한 관심이 증가하고 있음을 반영합니다. 실제로, 거래의 약 70%가 지난 3년 동안 체결되었습니다.

- 55%의 기업들은 증가하는 수요에 대응하기 위해 서비스 포트폴리오를 강화하기 위한 생산 능력 확장 계획을 추진 중입니다.

- 세계의 ADC 세포 독성 페이로드 제조 설비 용량은 다양한 시설에 고르게 분포되어 있으며, 이 중 대다수(40%)는 유럽에 위치한 시설에 설치되어 있습니다.

- 다수의 임상 후보물질이 전 세계 다양한 지역에서 상용화될 것으로 예상됨에 따라 ADC 세포 독성 페이로드 제조 수요는 크게 증가할 것으로 보입니다.

- 암 유병률 증가와 페이로드 화학 기술 발전에 힘입어 시장은 빠르게 진화하고 있지만, 동시에 엄격한 규제와 안정성 문제에 직면해 있습니다.

- 현재 ADC 세포 독성 페이로드 및 워헤드 시장에서 북미가 가장 큰 점유율을 차지하고 있으며, 이어 유럽, 아시아태평양이 이어지고 있습니다.

- 미국 주요 기업들의 ADC 세포 독성 페이로드 및 워헤드 신속한 성공에 힘입어, ADC 세포 독성 페이로드 및 워헤드 시장은 연평균 복합 성장률(CAGR) 6.7%로 성장할 것으로 전망됩니다.

- 북미의 ADC 세포 독성 페이로드 및 워헤드 시장은 올해 1억 3,800만 달러 규모에 이를 것으로 예상되며, 이 시장에서 토포이소머라제 I 억제제가 대부분 점유율을 차지하며 주도하고 있습니다.

ADC 세포 독성 페이로드 및 워헤드 시장

시장 규모 및 기회 분석은 다음 매개변수에 따라 세분화되었습니다

제품 유형

- 상용화 ADC

- 임상 ADC

페이로드 유형

- 토포이소머라제 억제제

- 튜불린 억제제

- DNA 손상제

- 기타

페이로드 및 워헤드 하위 카테고리

- 토포이소머라제 I 억제제

- 마이탄시노이드

- 오리스타틴

- 기타

지리적 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 스페인

- 아시아태평양

- 중국

- 일본

- 호주

ADC 세포 독성 페이로드 및 워헤드 시장 - 주요 부문

임상용 ADC의 성장이 암 치료를 추진

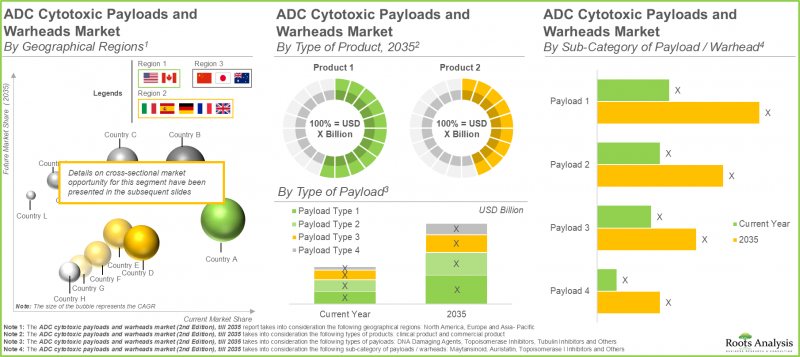

제품 유형별로 ADC 세포 독성 페이로드 및 워헤드 시장은 상용화 ADC와 임상 ADC로 구분됩니다. 상용 ADC 하위 부문이 시장 주도(90%)를 차지하며, 이는 상용화된 ADC의 효과성과 안전성 특성으로 인한 수요 증가에 힘입은 결과입니다. 또한 임상 ADC는 더 높은 연평균 복합 성장률(CAGR)을 기록할 것으로 예상되어 예측 기간 내내 상당한 성장 기회를 시사합니다. 이러한 확장은 ADC의 승인 증가와 다양한 표적 적응증에 대한 지속적인 연구에서 비롯됩니다.

토포이소머라제 억제제는 ADC 세포 독성 페이로드 분야의 확대를 주도

페이로드 유형별로 ADC 세포 독성 페이로드 및 워헤드 시장은 토포이소머라제 억제제, 튜불린 억제제, DNA 손상제 등으로 세분화됩니다. 글로벌 시장은 튜불린 억제제, 토포이소머라제 억제제, DNA 손상제 등 다양한 유형의 페이로드로 세분화됩니다. 토포이소머라제 억제제 하위 부문은 올해 최대 점유율(약 70%)을 차지합니다. 이는 암세포 내 DNA 복제를 방해하는 그들의 핵심 기능과 암 발생률 증가, 정밀 종양학의 진전, 해당 분야 연구 개발에 대한 투자 확대가 결합된 결과입니다.

토포이소머라제 I 억제제가 ADC 세포 독성 페이로드 산업을 주도할 것으로 예상

페이로드 및 워헤드 하위 카테고리별로, ADC 세포 독성 페이로드 및 워헤드 시장은 토포이소머라제 I 억제제, 마이탄시노이드, 오리스타틴 등으로 세분화됩니다. ADC 세포 독성 페이로드 및 워헤드 시장 전망에 따르면, 단일클론 항체, 유전자 치료, 맞춤형 의약품과 같은 혁신적인 치료법의 사용 증가로 인해 토포이소머라제 I 억제제가 올해 시장을 주도할 것으로 예상됩니다(70% 이상). 토포이소메라제 I 억제제 하위 부문의 핵심 요인은 각각 TOP1 억제제인 데룩스테칸(DXd)과 SN-38을 활용하는 엔허투(트라스투주맙 데룩스테칸) 및 트로델비(사시투주맙 고비테칸)와 같은 ADC의 승인입니다. 이러한 페이로드는 DNA 복제 및 수리를 방해함으로써 강력한 항암제로 작용합니다.

시장 지역별 인사이트

유럽, ADC 세포 독성 페이로드 및 워헤드 시장 주도

지역별로 볼 때 ADC 세포 독성 페이로드 및 워헤드 시장은 북미, 유럽, 아시아태평양 지역으로 세분화됩니다. 2035년까지 유럽의 ADC 세포 독성 페이로드 및 워헤드 시장이 약 45%의 점유율로 선두를 달릴 것으로 예상됩니다. 이 지역의 우위를 이끄는 주요 요인으로는 학술 기관과 기업 간의 강력한 협력, 효과적인 화합물을 위한 첨단 제조 능력, 그리고 광범위한 지적 재산 활동 등이 있습니다.

1차 조사 개요

이 시장 보고서에 제시된 견해와 인사이트는 업계의 주요 이해 관계자와의 논의에서도 영향을 받고 있습니다. 시장 보고서에는 다음 이해 관계자와의 인터뷰에 대한 자세한 기록이 포함되어 있습니다.

- 네덜란드 소규모 기업 창립자 겸 최고 과학 책임자

- 프랑스 대형 기업 시장 이사

또한 시장 보고서에는 다음과 같은 제3자 논의 내용도 포함됩니다

- 이탈리아 대형 기관 개발 및 GMP 제조 책임자

- 영국 대형 기관 과학적 비즈니스 개발 매니저 및 ADC 리더

- 미국 초대형 기관 정책 분석가

ADC 세포 독성 페이로드 및 워헤드 시장의 대표적인 진출기업

- Abzena

- Axplora

- CARBOGEN AMCIS

- Cerbios-Pharma

- Eisai

- GeneQuantum

- Levena Biopharma

- MabPlex

- MilliporeSigma(Merck)

- NJ Bio

- Synaffix

- WuXi STA

ADC 세포 독성 페이로드 및 워헤드 시장 - 조사 범위

- 시장 규모 및 기회 분석 : 본 보고서는 ADC 세포 독성 페이로드 및 워헤드 시장에 대해 (A) 제품 유형, (B) 페이로드, (C) 페이로드 및 워헤드 하위 카테고리, (D) 지리적 지역 등 주요 시장 부문에 초점을 맞춘 상세한 분석을 제공합니다.

- 시장 환경 : 설립 연도, 기업 규모, 본사 재료지, 기업 유형, 페이로드 유형, DNA 손상제 유형, 미세소관/튜불린 억제제 유형, 토포이소머라제 억제제 유형, 운영 규모 및 치료 분야 유형 등 여러 관련 매개변수를 기반으로 ADC 세포 독성 페이로드 및 워헤드를 제공하는 기업의 현재 시장 환경에 대한 상세한 개요를 제공합니다.

- 기업 경쟁력 분석 : 공급업체 역량(경력 연수 및 기업 규모 기준), 포트폴리오 역량(DNA 손상제, 미세소관/튜불린 억제제, 토포이소머라제 억제제, 단백질 키나제 억제제, 기타 페이로드 수 및 치료 분야 유형 기준) 및 운영 규모를 기반으로 주요 지리적 지역별 ADC 세포 독성 페이로드 및 워헤드 공급업체에 대한 인사이트 있는 기업 경쟁력 분석합니다.

- 기업 프로파일 : A] 설립 연도, [B] 본사 재료지, [C] ADC 세포 독성 페이로드 및 워헤드 포트폴리오, [D] 최근 동향, [E] 정보 기반의 미래 전망을 기준으로 북미, 유럽 및 아시아태평양 지역의 ADC 세포 독성 페이로드 및 워헤드 시장에 참여하는 주요 기업에 대한 심층 프로파일을 제공합니다.

- 파트너십 및 협력 : [A] 파트너십 체결 연도, [B] 파트너십 유형, [C] 제품 유형, [D] 파트너 유형, [E] 가장 활발한 기업 등 여러 매개변수를 기반으로 해당 산업에 종사하는 이해관계자 간 체결된 파트너십 분석합니다.

- 최근 확장 : ADC 세포 독성 페이로드 및 워헤드와 관련된 각 회사의 능력 강화를 목표로 하는 최근 확장 활동에 대한 분석. 다음의 파라미터에 근거하여 실시 : (A)확장 실시년, (B)확장 유형(신시설 설립, 시설 확장, 생산 능력 확장), (C)확장의 지리적 장소.

- 수요 분석 : 대상 환자 집단, 투여 빈도, 용량 강도 등의 다양한 파라미터에 기초하여, 시판되는 ADC 세포 독성 페이로드 및 워헤드, ADC 세포 독성 페이로드 및 워헤드를 평가하는 임상시험을 고려한 유전자 치료의 세계 연간 수요에 관한 정보에 기초한 추정을 제공합니다.

- 생산 능력 분석 : 공개 정보 및 1차 및 2차 조사에서 얻은 지식을 바탕으로 업계 관계자의 ADC 세포 독성 페이로드 및 워헤드의 총 설치 생산 능력을 추정합니다.

- 시장 영향 분석 : ADC 세포 독성 페이로드 및 워헤드 시장의 성장에 영향을 줄 수 있는 요인에 대한 자세한 분석입니다. 또한 (A) 주요 추진 요인, (B) 잠재적인 억제요인, (C) 새로운 기회, (D) 기존 과제의 식별 및 분석을 특징으로 합니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

- 장의 개요

- 예측 조사 방법

- 시장 평가 프레임워크

- 예측 도구와 기법

- 중요한 고려 사항

- 제한 사항

제4장 거시경제지표

- 장의 개요

- 시장 역학

- 결론

제5장 주요 요약

제6장 소개

- 장의 개요

- 항체 약물 복합체(ADC)의 개요

- ADC의 주요 컴포넌트

- 세포 독성 페이로드

- ADC 제조에서 중요한 단계

- ADC 제조와 관련된 기술적 과제

- ADC 세포 독성 페이로드 및 워헤드 계약 제조의 필요성

- CD 제조에 적합한 파트너를 선택하기 위한 가이드라인

- 세포독성 약물 제조에 관한 규제 고려 사항

- 장래의 전망

제7장 시장 상황 : ADC 세포 독성 페이로드 및 워헤드 공급자

- 장의 개요

- ADC 세포 독성 페이로드 및 워헤드 공급자 : 시장 상황

제8장 기업 경쟁력 분석 : ADC 세포 독성 페이로드 및 워헤드 공급자

- 장의 개요

- 전제 및 주요 파라미터

- 조사 방법

- 기업 경쟁력 분석 : ADC 세포 독성 페이로드 및 워헤드 공급자

제9장 기업 프로파일 : ADC 세포 독성 페이로드 및 워헤드 시장의 주요 기업

- 장의 개요

- CARBOGEN AMCIS

- Cerbios-Pharma

- Levena Biopharma

- MabPlex

- MilliporeSigma

- WuXi STA

제10장 기업 프로파일 : ADC 세포 독성 페이로드 및 워헤드 시장의 기타 주요 기업

- 장의 개요

- Abzena

- Axplora

- Eisai

- GeneQuantum

- NJ Bio

- Synaffix

제11장 파트너십 및 협업

- 장의 개요

- 파트너십 모델

- ADC 세포 독성 페이로드 및 워헤드 : 파트너십과 협력

제12장 최근 확장

- 장의 개요

- ADC 세포 독성 페이로드 및 워헤드 : 최근 확장

제13장 능력 분석 : ADC 세포 독성 페이로드 및 워헤드의 제조

- 장의 개요

- 주요 전제와 조사 방법

제14장 수요 분석 : ADC 세포 독성 페이로드 및 워헤드 공급자

- 장의 개요

- 수요의 주도역

- 주요 전제와 조사 방법

- ADC 세포 독성 페이로드의 세계 연간 수요

제15장 시장 영향 분석

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 시장 기회

- 시장의 과제

제16장 세계의 ADC 세포 독성 페이로드 및 워헤드 시장

제17장 ADC 세포 독성 페이로드 및 워헤드 시장(제품 유형별)

제18장 ADC 세포 독성 페이로드 및 워헤드 시장(페이로드 유형별)

제19장 ADC 세포 독성 페이로드 및 워헤드 시장(페이로드 및 워헤드 하위 카테고리별)

제20장 ADC 세포 독성 페이로드 및 워헤드 시장(지역별)

제21장 시장 기회 분석 : 북미

제22장 시장 기회 분석 : 유럽

제23장 시장 기회 분석 : 아시아태평양

제24장 결론

제25장 주요 인사이트

제26장 부록 1 : 표 형식 데이터

제27장 부록 2 : 기업 및 단체 일람

HBR 26.02.10ADC Cytotoxic Payloads and Warheads Market: Overview

As per Roots Analysis, the ADC cytotoxic payloads and warheads market is estimated to grow from USD 469.3 million in the current year to USD 720.2 million by 2035, at a CAGR of 4.9% during the forecast period, till 2035.

ADC Cytotoxic Payloads and Warheads Market: Growth and Trends

Antibody-drug conjugate (ADC) cytotoxic agents and warheads are essential elements in contemporary targeted cancer treatments, developed to provide highly effective compounds accurately while reducing overall toxicity. Through the incorporation of chemical optimization and advanced linker systems, these payloads improve the therapeutic efficacy of ADCs, allowing pharmaceutical firms to develop more efficient and targeted cancer therapies.

The ADC payloads field is growing swiftly by utilizing advancements in payload chemistry, conjugation techniques, and linker technologies to enhance safety and efficacy profiles. The market for ADC cytotoxic payloads and warheads is seeing substantial growth, fueled by innovations in cancer therapies and an expanding pipeline of ADC-related treatments. Cytotoxic payloads and warheads are crucial for the effectiveness of ADCs, as they guarantee the precise delivery of powerful anti-cancer drugs to tumor cells, protecting healthy tissues. The market is set to grow as ADCs demonstrate encouraging outcomes in clinical studies and receive ongoing approval for application in oncology.

Growth Drivers: Strategic Enablers of Market Expansion

Continuous improvements in linker stability, payload effectiveness, and targeted delivery systems are boosting the therapeutic index of ADCs. These advancements enable researchers to enhance tumor-eradicating effectiveness while reducing harm to healthy tissues. This precision method is driving innovative strategies in oncology for managing both blood cancers and solid tumors.

Moreover, the increasing requirement for next-generation payload categories, including DNA-damaging compounds and microtubule inhibitors, is prompting significant progress within the biopharmaceutical sector. The ADC payloads and warheads market is witnessing rapid market expansion due to increased investment in targeted cancer therapies and the ongoing advancement of conjugation technologies. Additionally, the advancement of next-generation multi-warhead antibody-drug conjugates (ADCs) is likely to greatly enhance market expansion by addressing shortcomings of existing ADC treatments.

Market Challenges: Critical Barriers Impeding Progress

The development of ADC cytotoxic payloads and warheads requires managing extremely potent, dangerous substances that necessitate specialized containment facilities, stringent safety measures, and chemical knowledge to mitigate exposure risks. Further, scalability challenges stem from intricate conjugation methods, resulting in heterogeneity, aggregation, stability concerns, and obstacles in attaining ideal drug-to-antibody ratios (DAR) at high volumes. In addition, elevated development expenses, raw material supply chain weaknesses also limit market expansion.

ADC Cytotoxic Payloads and Warheads Market: Key Insights

The report delves into the current state of the ADC cytotoxic payloads and warheads market and identifies potential growth opportunities within industry. Some key findings from the report include:

- The current market landscape features a presence of close to 70 providers that claim to offer broad range of payloads, which are being used or tested across various therapeutic areas.

- Around 25% companies offer both pyrrolobenzodiazepine and auristatin payloads, owing to their exceptional potency and demonstrated ability to induce effective cell death in both dividing and non-dividing cells.

- The rising interest in this market is reflected from the diverse partnerships established among various stakeholders in the recent past; in fact, close to 70% of deals were inked in the last three years.

- 55% of the companies have undertaken capacity expansion initiatives to strengthen their service portfolio in order to keep pace with the growing demand.

- The global installed ADC payload manufacturing capacity is well distributed across different facilities worldwide; majority (40%) of this capacity is installed in facilities located in Europe.

- The demand for ADC payload manufacturing is likely to increase significantly as several clinical candidates are expected to be commercialized across various regions of the globe.

- Fueled by rising cancer prevalence and advancements in payload chemistry, the market is rapidly evolving while also contending with stringent regulations and stability challenges.

- Currently, North America captures the largest share within the ADC cytotoxic payloads and warheads market, followed by Europe and Asia-Pacific.

- Driven by the rapid success of ADC payloads and warheads by prominent players in the US, the ADC cytotoxic payloads and warheads market is expected to grow at CAGR of 6.7%.

- The ADC cytotoxic payloads and warheads market in North America is expected to be worth USD 138 million in the current year; further, within this market, topoisomerase I inhibitors dominates by capturing the majority share.

ADC Cytotoxic Payloads and Warheads Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Type of Product

- Commercialized ADCs

- Clinical ADCs

Type of Payload

- Topoisomerase Inhibitors

- Tubulin Inhibitors

- DNA Damaging Agents

- Others

Sub-Category of Payload / Warhead

- Topoisomerase I inhibitors

- Maytansinoid

- Auristatin

- Others

Geographical Regions

- North America

- US

- Canada

- Europe

- Germany

- France

- Italy

- UK

- Spain

- Asia-Pacific

- China

- Japan

- Australia

ADC Cytotoxic Payloads and Warheads Market: Key Segments

Growth of Clinical ADCs is Propelling Cancer Treatment

In terms of type of product, the ADC cytotoxic payloads and warheads market is segmented across commercialized and clinical ADCs. The commercial ADCs sub-segment leads the market (90%), fueled by rising demand for marketed ADCs due to their effectiveness and safety characteristics. Additionally, clinical ADCs are expected to experience a greater CAGR, indicating significant growth opportunities throughout the forecast timeframe. This expansion results from the rising approval of ADCs and their continuous investigation across various target indications.

Topoisomerase Inhibitors Propel Expansion in ADC Cytotoxic Payload Sector

In terms of type of payload, the ADC cytotoxic payloads and warheads market is segmented across topoisomerase inhibitors, tubulin inhibitors, DNA damaging agents and others. The global market is segmented across different types of payloads, such as tubulin inhibitors, topoisomerase inhibitors, DNA damaging agents, and others. The topoisomerase inhibitors sub-segment holds the largest share (~70%) this year. This their crucial function in interfering with DNA replication in cancer cells, combined with the increasing incidence of cancer, progress in precision oncology, and heightened investments in research and development in this field.

Topoisomerase I Inhibitors Set to Lead ADC Payload Industry

In terms of sub-category of payload / warhead, the ADC cytotoxic payloads and warheads market is segmented across topoisomerase I inhibitors, maytansinoid, auristatin and others. As per the ADC cytotoxic payloads and warheads market forecast, the growing use of innovative treatments, such as monoclonal antibodies, gene therapies, and personalized medicine, is expected to enable topoisomerase I inhibitors to lead (>70%) the market in the current year. A key factor in the topoisomerase I inhibitor sub-segment is the approval of ADCs like Enhertu (trastuzumab deruxtecan) and Trodelvy (sacituzumab govitecan), which utilize TOP1 inhibitors deruxtecan (DXd) and SN-38, respectively. These payloads serve as powerful anti-cancer agents by disrupting DNA replication and repair.

Market Regional Insights

Europe Dominates the ADC Cytotoxic Payloads and Warheads Market

In terms of geography, the ADC cytotoxic payloads and warheads market is segmented across North America, Europe and Asia-Pacific. By 2035, the market for ADC cytotoxic payloads / warheads in Europe is expected to lead, holding approximately 45% of the market share. Crucial factors that contribute to the dominance of the region include strong collaborations between academic institutions and businesses, advanced manufacturing abilities for effective compounds, and extensive activity in intellectual property.

Primary Research Overview

The opinions and insights presented in the market report were also influenced by discussions held with senior stakeholders in the industry. The market report includes detailed transcripts of interviews conducted with the following individuals:

- Founder and Chief Scientific Officer, Small Organization, Netherlands

- Market Director, Large Organization, France

In addition, the market report includes transcripts of the following other third-party discussions:

- Head of Development and GMP Manufacturing, Large Organization, Italy

- Scientific business development manager and ADC lead, Large Organization, United Kingdom

- Policy Analyst, Very Large Organization, United States

Example Players in ADC Cytotoxic Payloads and Warheads Market

- Abzena

- Axplora

- CARBOGEN AMCIS

- Cerbios-Pharma

- Eisai

- GeneQuantum

- Levena Biopharma

- MabPlex

- MilliporeSigma (Merck)

- NJ Bio

- Synaffix

- WuXi STA

ADC Cytotoxic Payloads and Warheads Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the ADC cytotoxic payloads and warheads market, focusing on key market segments, including [A] type of product, [B] payload, [C] sub-category of payload / warhead, and [D] geographical regions.

- Market Landscape: A detailed overview of the current market landscape of companies offering ADC cytotoxic payloads and warheads, based on several relevant parameters, including year of establishment, company size, location of the headquarters, type of company, type of payload, type of DNA damaging agents, type of microtubule / tubulin inhibitors, type of topoisomerase inhibitors, scale of operation and type of therapeutic area.

- Company Competitiveness Analysis: An insightful company competitiveness analysis of ADC cytotoxic payloads and warheads providers (across key geographical regions), based on supplier strength (in terms of years of experience and company size), and portfolio strength (in terms of number of DNA damaging agents, microtubule / tubulin inhibitors, topoisomerase inhibitors, protein kinase inhibitors, other payloads, and type of therapeutic area) and scale of operation.

- Company Profiles: In-depth profiles of prominent players North America, Europe and Asia-Pacific that are engaged in the ADC cytotoxic payloads and warheads market based on [A] year of establishment, [B] location of headquarters, [C] ADC cytotoxic payloads and warheads portfolio, [D] recent developments and [E] an informed future outlook.

- Partnerships and Collaborations: An analysis of the partnerships inked between stakeholders engaged in this industry, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of product, [D] type of partner and [E] most active players.

- Recent Expansions: An analysis of the recent expansions undertaken by various companies in order to augment their respective capabilities related to ADC cytotoxic payloads and warheads, based on several parameters, such as [A] year of expansion, [B] type of expansion (new facility establishment, facility expansion, and capacity expansion), and [C] geographical location of the expansion.

- Demand Analysis: An informed estimate of the global annual demand for gene therapies, taking into account the marketed ADC cytotoxic payloads and warheads and clinical trials evaluating ADC cytotoxic payloads and warheads, based on various parameters, such as target patient population, dosing frequency and dose strength.

- Capacity Analysis: An estimate of the overall installed ADC cytotoxic payloads and warheads manufacturing capacity of industry players based on the information available in the public domain, and insights generated from both secondary and primary research.

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of ADC cytotoxic payloads and warheads market. It also features identification and analysis of [A] key drivers, [B] potential restraints, [C] emerging opportunities, and [D] existing challenges.

Key Questions Answered in this Report

- Which are the leading companies in the ADC cytotoxic payloads and warheads market?

- Which region dominates the ADC cytotoxic payloads and warheads market?

- What are the key trends observed in the ADC cytotoxic payloads and warheads market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by ADC cytotoxic payloads and warheads developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Executive Summary: Market Landscape

- 5.2. Executive Summary: Market Trends

- 5.3. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Antibody Drug Conjugate (ADC)

- 6.3. Key Components of ADCs

- 6.4. Cytotoxin Payloads

- 6.5. Key Steps in ADC Manufacturing

- 6.6. Technical Challenges Associated with ADC Manufacturing

- 6.7. Need for Contract Manufacturing of ADC Payloads / Warheads

- 6.8. Guidelines for Selecting a Suitable Partner for Manufacturing CD

- 6.9. Regulatory Considerations for Cytotoxic Drugs Manufacturing

- 6.10. Future Outlook

7. MARKET LANDSCAPE: ADC CYTOTOXIC PAYLOAD AND WARHEAD PROVIDERS

- 7.1. Chapter Overview

- 7.2. ADC Cytotoxic Payload and Warhead Providers: Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters (Region)

- 7.2.4. Analysis by Location of Headquarters (Country)

- 7.2.5. Analysis by Location of Facilities

- 7.2.6. Analysis by Type of Company

- 7.2.7. Analysis by Type of DNA Damaging Agent

- 7.2.8. Analysis by Type of Microtubule / Tubulin Inhibitors

- 7.2.9. Analysis by Type of Topoisomerase Inhibitors

- 7.2.10. Analysis by Scale of Operation

- 7.2.11. Analysis by Type of Therapeutic Area

8. COMPANY COMPETITIVENESS ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS PROVIDERS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers

- 8.4.1. ADC Cytotoxic Payloads and Warheads Providers based in North America

- 8.4.2. ADC Cytotoxic Payloads and Warheads Providers based in Europe

- 8.4.3. ADC Cytotoxic Payloads and Warheads Providers based in Asia-Pacific

9. COMPANY PROFILES: LEADING PLAYERS IN THE ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 9.1. Chapter Overview

- 9.2. CARBOGEN AMCIS

- 9.2.1. Company Overview

- 9.2.2. Financial Information

- 9.2.3. Recent Developments and Future Outlook

- 9.3. Cerbios-Pharma

- 9.3.1. Company Overview

- 9.3.2. Recent Developments and Future Outlook

- 9.4. Levena Biopharma

- 9.4.1. Company Overview

- 9.4.2. Recent Developments and Future Outlook

- 9.5. MabPlex

- 9.5.1. Company Overview

- 9.5.2. Recent Developments and Future Outlook

- 9.6. MilliporeSigma

- 9.6.1. Company Overview

- 9.6.2. Financial Information

- 9.6.3. Recent Developments and Future Outlook

- 9.7. WuXi STA

- 9.7.1. Company Overview

- 9.7.2. Financial Information

- 9.7.3. Recent Developments and Future Outlook

10. COMPANY PROFILES: OTHER LEADING PLAYERS IN THE ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 10.1. Chapter Overview

- 10.2. Abzena

- 10.2.1. Company Overview

- 10.3. Axplora

- 10.3.1. Company Overview

- 10.4. Eisai

- 10.4.1. Company Overview

- 10.5. GeneQuantum

- 10.5.1. Company Overview

- 10.6. NJ Bio

- 10.6.1. Company Overview

- 10.7. Synaffix

- 10.7.1. Company Overview

11. PARTNERSHIPS AND COLLABORATIONS

- 11.1. Chapter Overview

- 11.2. Partnership Models

- 11.3. ADC Cytotoxic Payloads and Warheads: Partnerships and Collaborations

- 11.3.1. Analysis by Year of Partnership

- 11.3.2. Analysis by Type of Partnership

- 11.3.3. Analysis by Year and Type of Partnership

- 11.3.4. Analysis by Type of Partner

- 11.3.5. Most Active Players: Analysis by Number of Partnerships

- 11.3.6. Analysis by Geography

- 11.3.6.1. Analysis by Country

- 11.3.6.2. Analysis by Continent

12. RECENT EXPANSIONS

- 12.1. Chapter Overview

- 12.2. ADC Cytotoxic Payloads and Warheads: Recent Expansions

- 12.2.1. Analysis by Year of Expansion

- 12.2.2. Analysis by Type of Expansion

- 12.2.3. Analysis by Year and Type of Expansion

- 12.2.4. Most Active Players: Analysis by Number of Recent Expansions

- 12.2.5. Analysis by Location of Expansion

- 12.2.5.1. Analysis by Country

- 12.2.5.2. Analysis by Continent

13. CAPACITY ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS MANUFACTURING

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.2.1. Analysis by Range of Installed Capacity

- 13.2.2. Analysis by Scale of Operation

- 13.2.3. Analysis by Location of ADC Cytotoxic Payloads and Warheads Facility

14. DEMAND ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS PROVIDERS

- 14.1. Chapter Overview

- 14.2. Demand Drivers

- 14.3. Key Assumptions and Methodology

- 14.4. Global Annual Demand for ADC Payloads

- 14.4.1. Global Clinical Demand for ADC Payloads

- 14.4.1.1. Analysis by Type of Payload

- 14.4.1.2. Analysis by Phase of Development

- 14.4.2. Global Commercial Demand for ADC Payloads

- 14.4.1.1. Analysis by Payload

- 14.4.1.2. Analysis by Type of Payload

- 14.4.1.2. Analysis by Therapeutic Area

- 14.4.1.3. Analysis by Geographical Regions

- 14.4.1. Global Clinical Demand for ADC Payloads

15. MARKET IMPACT ANALYSIS

- 15.1. Market Drivers

- 15.2. Market Restraints

- 15.3. Market Opportunities

- 15.4. Market Challenges

16. GLOBAL ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.3. Global ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.1. Scenario Analysis

- 16.3.1.1. Conservative Scenario

- 16.3.1.2. Optimistic Scenario

- 16.3.1. Scenario Analysis

- 16.4. Key Market Segmentations

17. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY TYPE OF PRODUCT

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Product

- 17.3.1. Commercialized ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 17.3.2. Clinical ADC Cytotoxic Payloads and Warheads Market ADCs, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

18. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY TYPE OF PAYLOAD

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload

- 18.3.1. ADC Cytotoxic Payloads and Warheads Market for Tubulin inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.2. ADC Cytotoxic Payloads and Warheads Market for Topoisomerase Inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.3. ADC Cytotoxic Payloads and Warheads Market for DNA Damaging Agents, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.4. ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

19. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY SUB-CATEGORY OF PAYLOAD / WARHEAD

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Sub-Categories of Payload / Warhead

- 19.3.1. ADC Cytotoxic Payloads and Warheads Market for Topoisomerase I inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.2. ADC Cytotoxic Payloads and Warheads Market for Maytansinoid, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.3. ADC Cytotoxic Payloads and Warheads Market for Auristatin, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.4. ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

20. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Geographical Regions

- 20.3.1. ADC Cytotoxic Payloads and Warheads Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1.1. ADC Cytotoxic Payloads and Warheads Market in the US, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1.2. ADC Cytotoxic Payloads and Warheads Market in Canada, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2. ADC Cytotoxic Payloads and Warheads Market in Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.1. ADC Cytotoxic Payloads and Warheads Market in Germany, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.2. ADC Cytotoxic Payloads and Warheads Market in the UK, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.3. ADC Cytotoxic Payloads and Warheads Market in France, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.4. ADC Cytotoxic Payloads and Warheads Market in Italy, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.5. ADC Cytotoxic Payloads and Warheads Market in Spain, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.1. ADC Cytotoxic Payloads and Warheads Market in China, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.2. ADC Cytotoxic Payloads and Warheads Market in Japan, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.4. ADC Cytotoxic Payloads and Warheads Market in Australia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1. ADC Cytotoxic Payloads and Warheads Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

21. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

- 21.1. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Product

- 21.1.1. ADC Cytotoxic Payloads and Warheads Market in North America for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.1.2. ADC Cytotoxic Payloads and Warheads Market in North America for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Payload

- 21.2.1. ADC Cytotoxic Payloads and Warheads Market in North America for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.2. ADC Cytotoxic Payloads and Warheads Market in North America for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.3. ADC Cytotoxic Payloads and Warheads Market in North America for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.4. ADC Cytotoxic Payloads and Warheads Market in North America for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Payload / Warhead

- 21.3.1. ADC Cytotoxic Payloads and Warheads Market in North America for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.2. ADC Cytotoxic Payloads and Warheads Market in North America for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.3. ADC Cytotoxic Payloads and Warheads Market in North America for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.4. ADC Cytotoxic Payloads and Warheads Market in North America for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

22. MARKET OPPORTUNITY ANALYSIS: EUROPE

- 22.1. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Product

- 22.1.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.1.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Payload

- 22.2.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.3. ADC Cytotoxic Payloads and Warheads Market in Europe for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.4. ADC Cytotoxic Payloads and Warheads Market in Europe for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Payload / Warhead

- 22.3.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.3. ADC Cytotoxic Payloads and Warheads Market in Europe for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.4. ADC Cytotoxic Payloads and Warheads Market in Europe for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

23. MARKET OPPORTUNITY ANALYSIS: ASIA-PACIFIC

- 23.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Product

- 23.1.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.1.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Payload

- 23.2.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.4. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Payload / Warhead

- 23.3.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.4. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- *Detailed information on Chapter 21 to 23 is available in the Excel Data Packs shared along with the report**

24. CONCLUDING REMARKS

25. EXECUTIVE INSIGHTS

- 25.1 Chapter Overview

- 25.2. Company A (Mid-sized company, Netherlands)

- 25.2.1. Company Snapshot

- 25.2.2. Interview Transcript: Founder and Chief Scientific Officer

- 25.3. Company B (Small Company, US)

- 25.3.1. Company Snapshot

- 25.3.2. Interview Transcript: Founder and Chief Executive Officer

- 25.4. Company C (Small Company, France)

- 25.4.1. Company Snapshot

- 25.4.2. Interview Transcript: Co-founder and Chief Executive Officer

- 25.5. Company D (Large Company, Italy)

- 25.5.1. Company Snapshot

- 25.5.2. Interview Transcript: Chief Executive Officer and Technical Business Development Manager

- 25.6. Company E (Large Company, South Korea)

- 25.6.1. Company Snapshot

- 25.6.2. Interview Transcript: Chief Business Officer