|

시장보고서

상품코드

2015363

광 AI 액셀러레이터 시장(-2040년) : 업계 동향과 세계 예측Optical AI Accelerator Market, Till 2040: Industry Trends and Global Forecasts |

||||||

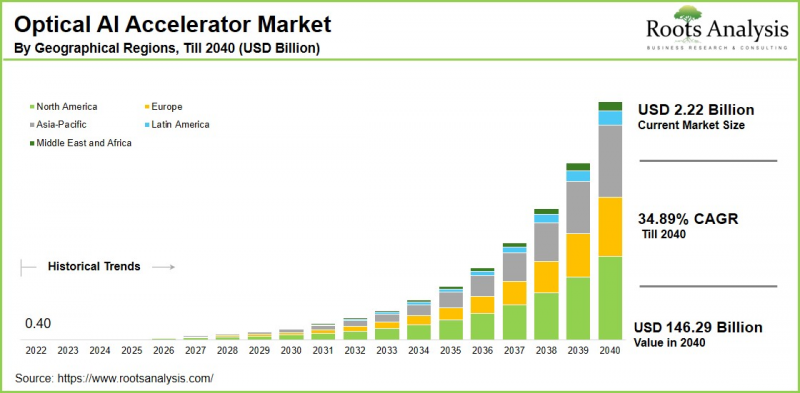

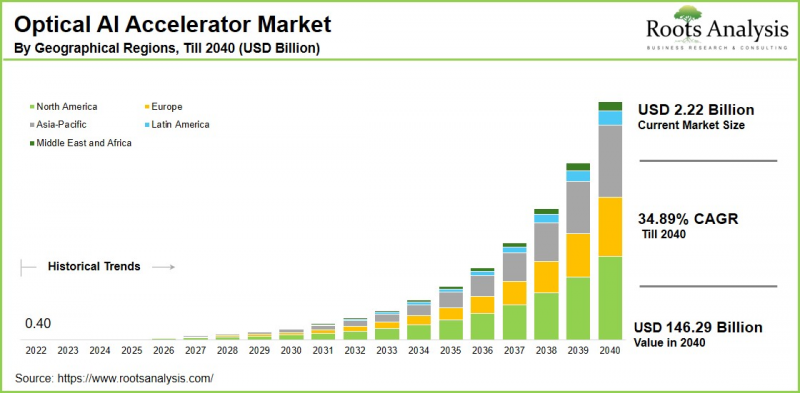

광 AI 가속기 시장 전망

세계의 광 AI 액셀러레이터 시장 규모는 현재 22억 2,000만 달러에서 2040년까지 1,462억 9,000만 달러에 달할 것으로 추정되며, 2040년까지 CAGR로 34.89%의 확대가 전망되고 있습니다.

광 AI 가속기는 실리콘 포토닉스 칩과 같은 포토닉스 기술을 활용하여 전자가 아닌 빛을 이용하여 AI 연산을 수행하는 첨단 하드웨어와 통합 시스템으로 구성되어 있습니다. 이러한 가속기는 행렬 곱셈 속도를 크게 향상시키는 동시에 에너지 소비를 크게 줄일 수 있습니다. 그 결과, 데이터센터, 엣지 컴퓨팅 환경, HPC 인프라 전반에 걸쳐 획기적인 성능상 이점을 제공합니다.

광 AI 가속기에 대한 수요 확대는 주로 현대 AI 모델의 계산 부하 증가, 클라우드 플랫폼을 통해 생성되는 데이터 양의 기하급수적 증가, 실시간 분석에 대한 수요 증가에 의해 촉진되고 있습니다. 주요 응용 분야로는 거대 언어 모델 훈련, 이미지 인식, 자율 시스템 등이 있습니다. 이러한 수요에 대응하기 위해 각 업체들은 대역폭을 최적화하고 열적 제약을 줄이기 위해 설계된 하이브리드 전기-광학 아키텍처, 확장 가능한 포토닉 패브릭 등 혁신적인 솔루션을 개발하고 있습니다. 업계 리더들은 또한 그린 컴퓨팅을 촉진하는 규제 요건을 충족하기 위해 에너지 절약형 설계를 우선시하고 있으며, 차세대 AI 클러스터를 지원하는 코패키지드 옵틱을 개발하고 있습니다. 이러한 기술 발전과 지속적인 시장 투자는 광 AI 가속기 시장의 꾸준한 구조적 진화를 촉진할 것으로 전망됩니다.

경영진을 위한 전략적 인사이트

광 AI 가속기 시장의 주요 성장 촉진요인

광 AI 가속기 시장의 성장은 주로 워크플로우 최적화 및 실시간 의사결정을 가능하게 하는 AI 기술의 보급에 따른 데이터 처리 요구가 증가함에 의해 촉진되고 있습니다. AI 워크로드의 규모와 복잡성이 증가함에 따라 열적 제약 없이 방대한 양의 데이터를 초고속으로 처리할 수 있는 고성능 가속기에 대한 요구가 증가하고 있습니다.

또한 지속적인 AI 작업을 운영하는 데이터센터는 막대한 전력 소비와 발열이라는 과제에 직면해 있으며, 이에 사업자들은 기존 전자 시스템보다 높은 에너지 효율과 비용 절감을 위해 광 AI 가속기를 도입하고 있습니다. 고속 통신 네트워크의 급속한 확장, 특히 5G의 발전과 새로운 5G 인프라의 개발은 실시간 신호 분석을 지원하는 에지 기반 광 AI 처리에 대한 수요를 더욱 가속화하고 있습니다. 또한 실리콘 포토닉스 기술의 지속적인 발전과 광칩 집적화의 비용 효율성이 향상됨에 따라 광 AI 가속기의 상업적 타당성이 높아져 시장에서의 채택이 확대되고 있습니다.

광 AI 가속기 시장: 업계내 기업 간 경쟁 상황

광 AI 가속기 시장은 전통 있는 다국적 기업과 신생 전문 기술 기업 모두가 진입해 치열한 경쟁이 벌어지고 있는 것이 특징입니다. Broadcom, IBM, Marvell Technology, Microsoft, Huawei Technologies, NVIDIA와 같은 기존 주요 기업은 자사의 첨단 설계 생태계와 기존 네트워크를 활용하여 광기술 기능을 광범위한 AI 가속 제품군에 통합하고 있습니다. 가속 제품군에 광기술 기능을 통합하고 있습니다.

동시에 Ayar Labs, LightOn, Luminous Computing, Q.ANT, Salience Labs, Xanadu Quantum Technologies, Arago Semiconductor 등의 전문적인 이노베이터는 혁신적인 혁신적인 신경망 아키텍처와 참신한 도파관 설계를 추진하고 있습니다. 또한 양사는 전략적 제휴를 체결하기 위해 노력하고 있습니다. 예를 들어 최근 OpenAI와 브로드컴은 OpenAI가 설계한 10기가와트 분량의 AI 가속기를 브로드컴의 이더넷 기반 네트워크 시스템과 통합하여 공동 개발 및 배포하는 획기적인 제휴를 발표하여 차세대 대규모 AI 인프라의 기반을 강화했습니다. 강화했습니다. 이러한 제휴와 혁신 주도 전략은 시장 전반의 경쟁을 심화시키고 제품 포트폴리오를 강화하는 데 기여하고 있습니다.

세계의 광학 AI 가속기(Optical AI Accelerator) 시장에 대해 조사했으며, 시장 규모 추정과 기회 분석, 경쟁 상황, 기업 개요 등의 정보를 전해드립니다.

목차

제1장 프로젝트의 개요

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 개요

제6장 서론

제7장 규제 시나리오

제8장 주요 기업의 종합적 데이터베이스

제9장 경쟁 구도

제10장 화이트 스페이스 분석

제11장 기업 경쟁력 분석

제12장 스타트업 에코시스템 분석

제13장 기업 개요

제14장 메가트렌드 분석

제15장 미충족 요구 분석

제16장 특허 분석

제17장 최근 발전

제18장 세계의 광 AI 액셀러레이터 시장

제19장 시장 기회 : 컴포넌트 유형별

제20장 시장 기회 : 기술 유형별

제21장 시장 기회 : 배포 방식별

제22장 시장 기회 : 기능 유형별

제23장 시장 기회 : 에너지 효율 Tier 유형별

제24장 시장 기회 : 광컴퓨팅 패러다임 유형별

제25장 시장 기회 : 응용 분야별

제26장 시장 기회 : 최종 용도 산업별

제27장 북미의 광 AI 액셀러레이터의 시장 기회

제28장 유럽의 광 AI 액셀러레이터의 시장 기회

제29장 아시아태평양의 광 AI 액셀러레이터의 시장 기회

제30장 라틴아메리카의 광 AI 액셀러레이터의 시장 기회

제31장 중동 및 아프리카의 광 AI 액셀러레이터의 시장 기회

제32장 시장 집중도 분석 : 주요 기업별

제33장 인접 시장 분석

제34장 주요 성공 전략

제35장 Porter's Five Forces 분석

제36장 SWOT 분석

제37장 밸류체인 분석

제38장 Roots의 전략적 제안

제39장 1차 조사로부터의 인사이트

제40장 리포트 결론

제41장 표형식 데이터

제42장 기업과 조직 리스트

KSA 26.05.06Optical AI Accelerator Market Outlook

As per Roots Analysis, the global optical AI accelerator market size is estimated to grow from USD 2.22 billion in current year to USD 146.29 billion by 2040, at a CAGR of 34.89% during the forecast period, till 2040.

An optical AI accelerator comprises advanced hardware and integrated systems that utilize photonic technologies (such as silicon photonics chips), to perform artificial intelligence computations using light rather than electrons. These accelerators significantly enhance matrix multiplication speeds while substantially reducing energy consumption. As a result, they deliver transformative performance benefits across data centers, edge computing environments, and high-performance computing (HPC) infrastructures.

Growing demand for optical AI accelerators is primarily driven by the increasing computational intensity of modern AI models, coupled with the exponential rise in data volumes generated through cloud platforms and the expanding need for real-time analytics. Key application areas include large language model training, image recognition, and autonomous systems. In response to this demand, companies are advancing innovative solutions, including hybrid electro-optic architectures and scalable photonic fabrics designed to optimize bandwidth and mitigate thermal constraints. Industry leaders are also prioritizing energy-efficient designs to align with regulatory mandates promoting green computing, while exploring co-packaged optics to support next-generation AI clusters. Collectively, these technological advancements and sustained market investments are expected to drive the steady structural evolution of the optical AI accelerator market.

Strategic Insights for Senior Leaders

Key Drivers Propelling Growth of Optical AI Accelerator Market

The growth of the optical AI accelerator market is primarily driven by escalating data processing requirements resulting from the widespread adoption of AI technologies to optimize workflows and enable real-time decision-making. As AI workloads expand in scale and complexity, there is an increasing need for high-performance accelerators capable of processing massive data volumes at ultra-fast speeds without thermal limitations.

Additionally, data centers operating continuous AI tasks face substantial power consumption and heat generation challenges, prompting operators to adopt optical AI accelerators to achieve greater energy efficiency and cost savings compared to conventional electronic systems. The rapid expansion of high-speed telecommunications networks, particularly with the advancement of 5G and emerging 6G infrastructure, is further accelerating demand for edge-based optical AI processing to support real-time signal analysis. Moreover, ongoing advancements in silicon photonics technologies and improved cost-efficiency of photonic chip integration are enhancing the commercial viability of optical AI accelerators, thereby supporting broader market adoption.

Optical AI Accelerator Market: Competitive Landscape of Companies in this Industry

The optical AI accelerator market is characterized by intense competition, marked by the presence of both established multinational corporations and emerging specialized technology firms. Established players such as Broadcom, IBM, Marvell Technology, Microsoft, Huawei Technologies, and NVIDIA are leveraging their advanced design ecosystems, and established networks to integrate photonic capabilities into broader AI acceleration portfolios.

Concurrently, specialized innovators, including Ayar Labs, LightOn, Luminous Computing, Q.ANT, Salience Labs, Xanadu Quantum Technologies, and Arago Semiconductor, are advancing disruptive neural network architectures and novel waveguide designs. Further, companies are engaged in signing strategic partnerships; for instance, recently, OpenAI and Broadcom announced a landmark collaboration to co-develop and deploy 10 gigawatts of OpenAI-designed AI accelerators integrated with Broadcom's Ethernet-based networking systems, reinforcing the foundation for next-generation large-scale AI infrastructure. Collectively, such alliances and innovation-led strategies are intensifying competition and strengthening product portfolios across the market.

Key Technological Advancements and Emerging Trends in the Industry

The optical AI accelerator market is witnessing several transformative trends driven by expanding edge AI deployment, advancements in automation, and evolving data center infrastructure. Increasing emphasis on compact optical chips is expected to enable on-device AI processing in smartphones and IoT systems, reducing reliance on cloud connectivity and minimizing latency. Simultaneously, the rapid advancement of automation and robotics (including real-time vision applications in autonomous vehicles), is driving the demand for low-latency, energy-efficient optical inference hardware. Further, companies are also exploring quantum-optical hybrid architectures, integrating optical AI accelerators with quantum technologies to unlock next-generation computational capabilities within research and advanced innovation environments.

Regional Analysis of Optical AI Accelerator Market

According to our estimates, North America holds a significant market share. This is driven by the strong presence of technology companies such as Google, Amazon, Meta, Microsoft, and OpenAI, along with substantial venture capital investment supporting optical technology startups. Emerging players, including Lightmatter and Ayar Labs, are actively developing advanced hardware platforms that are rapidly piloted by major technology firms for next-generation data center deployments.

Meanwhile, the Asia-Pacific region is projected to witness robust expansion, with an anticipated CAGR of approximately 32%, supported by policy-driven initiatives (such as China's "New Infrastructure" program) promoting optical computing for machine learning and edge data center development. Additionally, Taiwan's well-established silicon photonics manufacturing ecosystem positions it as a critical hub for co-packaged optics production, while India's smart city initiatives integrating edge AI acceleration further contribute to regional market growth.

Key Challenges in Optical AI Accelerator Market

The optical AI accelerator market faces several structural and technological challenges that may constrain its growth trajectory. High development costs associated with co-packaged optics (CPO) and advanced photonic chip fabrication, requiring capital-intensive manufacturing facilities, pose significant barriers to entry, particularly for smaller firms. Additionally, immature supply chains and a limited supplier base for specialized optical and neuromorphic photonic components contribute to procurement bottlenecks and price volatility. Further, technical integration complexities, particularly involving materials such as Indium Phosphide (InP) and Silicon Nitride (SiN), necessitate new design architectures and manufacturing platforms, potentially delaying product commercialization.

Scalability also remains a concern, as current photonic AI prototypes struggle to match the transistor density and integration levels of conventional electronic chips for highly complex AI models. Furthermore, a shortage of specialized talent in neural network optical computing and photonic engineering limits the pace of innovation and large-scale production expansion.

Optical AI Accelerator Market: Key Market Segmentation

Market Share by Type of Component

- Hardware

- Lasers / Light Sources (On-chip vs. External)

- Modulators and Detectors

- Optical Interconnects

- Optical Switching Modules

- Optical Waveguides

- Photonic Integrated Circuits (PICs)

- Software

- AI Optimization & Compiler Tools

- Deployment & Runtime Software (SDKs)

- Photonic Simulation & Modeling

- Services

- Design & Integration

- Maintenance & Support

Market Share by Type of Technology

- Hybrid Photonic-Electronic Integration

- Optical Neural Networks (ONN)

- Silicon Photonics (SiPh)

- Silicon Nitride (SiN)

- Thin-Film Lithium Niobate (TFLN)

Market Share by Deployment Mode

- Cloud-Based

- On-Premises

Market Share by Type of Function

- Inference-Optimized Accelerators

- Training-Optimized

Market Share by Type of Energy Efficiency Tier

- High-Throughput (<1 pJ / MAC)

- Ultra-Low Power (<100 aJ / MAC)

Market Share by Type of Optical Compute Paradigm

- Analog Optical Computing

- Digital Optical Computing

Market Share by Application Area

- Autonomous Vehicles

- Data Centers

- Edge Computing

- High-Performance Computing

- Healthcare

- Telecommunications

- Other Applications

Market Share by End Use Industry

- Aerospace & Defense

- Automotive

- Banking

- Consumer Electronics

- Financial Services

- Insurance (BFSI)

- Healthcare & Life Sciences

- IT & Telecommunications

Market Share by Geographical Regions

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Rest of Europe

- Asia-Pacific

- Australia

- China

- India

- Japan

- New-Zealand

- Singapore

- South Korea

- Rest of Asia-Pacific

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Rest of Latin America

- Middle East and Africa (MEA)

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Rest of MEA

Example Players in Optical AI Accelerator Market

- Ayar Labs

- Broadcom

- Cisco Systems

- Huawei Technologies

- IBM

- Intel

- Lightelligence

- Lightmatter

- LightOn

- Lumai

- Luminate Accelerator

- Luminous Computing

- Marvell Technology

- Microsoft

- Neurophos

- NIVIDIA

- OpenAI

- Q.ANT

- STMicroelectronics

- Synopsys

- Salience Labs

- Xanadu Quantum Technologies

Optical AI Accelerator Market: Report Coverage

The report on the optical AI accelerator market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the optical AI accelerator market, focusing on key market segments, including [A] type of component, [B] type of technology, [C] deployment mode, [D] type of function, [E] type of energy efficiency tier, [F] type of optical compute paradigm, [G] application area, [H] end use industry, [I] geographical regions, and [J] leading players.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the optical AI accelerator market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the optical AI accelerator market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] product / technology portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the optical AI accelerator industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the optical AI accelerator domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the optical AI accelerator market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the optical AI accelerator market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2040?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

1. PROJECT OVERVIEW

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Concluding Remarks

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Optical AI Accelerator

- 6.2.1. Type of Component

- 6.2.2. Type of Technology

- 6.2.3. Type of Deployment Mode

- 6.2.4. Type of Function

- 6.2.5. Type of Energy Efficiency Tier

- 6.2.6. Type of Optical Compute Paradigm

- 6.2.7. Application Area

- 6.2.8. End Use Industry

- 6.3. Future Perspective

7. REGULATORY SCENARIO

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Optical AI Accelerator Market: Overall Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Type of Company

- 9.3. Key Findings

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM ANALYSIS

- 12.1. Optical AI Accelerator Market: Startup Ecosystem Analysis

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Location of Headquarters

- 12.1.4. Analysis by Ownership Type

- 12.2. Key Findings

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Ayar Labs

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- Similar details are presented for other below mentioned companies (based on information in the public domain)

- 13.3. Ayar Labs

- 13.4. Broadcom

- 13.5. Cisco Systems

- 13.6. Huawei Technologies

- 13.7. IBM

- 13.8. Intel

- 13.9. Lightelligence

- 13.10. Lightmatter

- 13.11. LightOn

- 13.12. Lumai

- 13.13. Luminate Accelerator

- 13.14. Luminous Computing

- 13.15. Marvell Technology

- 13.16. Microsoft

- 13.17. Neurophos

- 13.18. NIVIDIA

- 13.19. OpenAI

- 13.20. Q.ANT

- 13.21. STMicroelectronics

- 13.22. Synopsys

- 13.23. Salience Labs

- 13.24. Xanadu Quantum Technologies

14. MEGA TRENDS ANALYSIS

15. UNMET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

18. GLOBAL OPTICAL AI ACCELERATOR MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Optical AI Accelerator Market: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF COMPONENT

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Optical AI Accelerator Market for Hardware: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.1. Optical AI Accelerator Hardware Market for Lasers / Light Sources (On-chip vs. External): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.2. Optical AI Accelerator Hardware Market for Modulators and Detectors: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.3. Optical AI Accelerator Hardware Market for Optical Interconnects: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.4. Optical AI Accelerator Hardware Market for Optical Switching Modules: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.5. Optical AI Accelerator Hardware Market for Optical Waveguides: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.6.6. Optical AI Accelerator Hardware Market for Photonic Integrated Circuits (PICs): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7. Optical AI Accelerator Market for Software: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7.1. Optical AI Accelerator Software Market for AI Optimization & Compiler Tools: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7.2. Optical AI Accelerator Software Market for Deployment & Runtime Software (SDKs): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7.3. Optical AI Accelerator Software Market for Photonic Simulation & Modeling: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.8. Optical AI Accelerator Market for Services: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.8.1. Optical AI Accelerator Services Market for Design & Integration: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.8.2. Optical AI Accelerator Services Market for Maintenance & Support: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.9. Data Triangulation and Validation

- 19.9.1. Secondary Sources

- 19.9.2. Primary Sources

- 19.9.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF TECHNOLOGY

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Optical AI Accelerator Market for Hybrid Photonic-Electronic Integration: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.7. Optical AI Accelerator Market for Silicon Photonics (SiPh): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.8. Optical AI Accelerator Market for Silicon Nitride (SiN): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.9. Optical AI Accelerator Market for Thin-Film Lithium Niobate (TFLN): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.10. Data Triangulation and Validation

- 20.10.1. Secondary Sources

- 20.10.2. Primary Sources

- 20.10.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON DEPLOYMENT MODE

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Optical AI Accelerator Market for Cloud-Based: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.7. Optical AI Accelerator Market for On-Premises: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.8. Data Triangulation and Validation

- 21.8.1. Secondary Sources

- 21.8.2. Primary Sources

- 21.8.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON TYPE OF FUNCTION

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Optical AI Accelerator Market for Thin-Film Lithium Niobate (TFLN): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.7. Optical AI Accelerator Market for Training-Optimized: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.8. Data Triangulation and Validation

- 22.8.1. Secondary Sources

- 22.8.2. Primary Sources

- 22.8.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON TYPE OF ENERGY EFFICIENCY TIER

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Optical AI Accelerator Market for High-Throughput (<1 pJ / MAC): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.7. Optical AI Accelerator Market for Ultra-Low Power (<100 aJ / MAC): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.8. Data Triangulation and Validation

- 23.8.1. Secondary Sources

- 23.8.2. Primary Sources

- 23.8.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON TYPE OF OPTICAL COMPUTE PARADIGM

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Optical AI Accelerator Market for Analog Optical Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.7. Optical AI Accelerator Market for Digital Optical Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.8. Data Triangulation and Validation

- 24.8.1. Secondary Sources

- 24.8.2. Primary Sources

- 24.8.3. Statistical Modeling

25. MARKET OPPORTUNITIES BASED ON APPLICATION AREA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Optical AI Accelerator Market for Autonomous Vehicles: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.7. Optical AI Accelerator Market for Data Centers: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.8. Optical AI Accelerator Market for Edge Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.9. Optical AI Accelerator Market for High-Performance Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.10. Optical AI Accelerator Market for Healthcare: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.11. Optical AI Accelerator Market for Telecommunications: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.12. Optical AI Accelerator Market for Other Applications: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.13. Data Triangulation and Validation

- 25.13.1. Secondary Sources

- 25.13.2. Primary Sources

- 25.13.3. Statistical Modeling

26. MARKET OPPORTUNITIES BASED ON END USE INDUSTRY

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Optical AI Accelerator Market for Aerospace & Defense: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.7. Optical AI Accelerator Market for Automotive: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.8. Optical AI Accelerator Market for Banking: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.9. Optical AI Accelerator Market for Consumer Electronics: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.9. Optical AI Accelerator Market for Financial Services: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.10. Optical AI Accelerator Market for Insurance (BFSI): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.11. Optical AI Accelerator Market for Healthcare & Life Sciences: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.12. Optical AI Accelerator Market for IT & Telecommunications: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.13. Data Triangulation and Validation

- 26.13.1. Secondary Sources

- 26.13.2. Primary Sources

- 26.13.3. Statistical Modeling

27. MARKET OPPORTUNITIES FOR OPTICAL AI ACCELERATOR IN NORTH AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Optical AI Accelerator Market in North America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.1. Optical AI Accelerator Market in the US: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.2. Optical AI Accelerator Market in Canada: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.3. Optical AI Accelerator Market in Mexico: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.4. Optical AI Accelerator Market in Other North American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR OPTICAL AI ACCELERATOR IN EUROPE

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Optical AI Accelerator Market in Europe: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.1. Optical AI Accelerator Market in Austria: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.2. Optical AI Accelerator Market in Belgium: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.3. Optical AI Accelerator Market in Denmark: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.4. Optical AI Accelerator Market in France: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.5. Optical AI Accelerator Market in Germany: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.6. Optical AI Accelerator Market in Ireland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.7. Optical AI Accelerator Market in Italy: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.8. Optical AI Accelerator Market in the Netherlands: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.9. Optical AI Accelerator Market in Norway: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.10. Optical AI Accelerator Market in Russia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.11. Optical AI Accelerator Market in Spain: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.12. Optical AI Accelerator Market in Sweden: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.13. Optical AI Accelerator Market in Switzerland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.14. Optical AI Accelerator Market in the UK: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.15. Optical AI Accelerator Market in Other European Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR OPTICAL AI ACCELERATOR IN ASIA-PACIFIC

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Optical AI Accelerator Market in Asia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.1. Optical AI Accelerator Market in China: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.2. Optical AI Accelerator Market in India: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.3. Optical AI Accelerator Market in Japan: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.4. Optical AI Accelerator Market in Singapore: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.5. Optical AI Accelerator Market in South Korea: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.6. Optical AI Accelerator Market in Other Asian Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR OPTICAL AI ACCELERATOR IN LATIN AMERICA

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Revenue Shift Analysis

- 30.4. Market Movement Analysis

- 30.5. Penetration-Growth (P-G) Matrix

- 30.6. Optical AI Accelerator Market in Latin America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.1. Optical AI Accelerator Market in Argentina: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.2. Optical AI Accelerator Market in Brazil: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.3. Optical AI Accelerator Market in Chile: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.4. Optical AI Accelerator Market in Colombia Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.5. Optical AI Accelerator Market in Venezuela: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.6. Optical AI Accelerator Market in Other Latin American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.7. Data Triangulation and Validation

31. MARKET OPPORTUNITIES FOR OPTICAL AI ACCELERATOR IN MIDDLE EAST AND AFRICA (MEA)

- 31.1. Chapter Overview

- 31.2. Key Assumptions and Methodology

- 31.3. Revenue Shift Analysis

- 31.4. Market Movement Analysis

- 31.5. Penetration-Growth (P-G) Matrix

- 31.6. Optical AI Accelerator Market in Middle East and Africa (MEA): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.1. Optical AI Accelerator Market in Egypt: Historical Trends (Since 2022) and Forecasted Estimates (Till 205)

- 31.6.2. Optical AI Accelerator Market in Iran: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.3. Optical AI Accelerator Market in Iraq: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.4. Optical AI Accelerator Market in Israel: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.5. Optical AI Accelerator Market in Kuwait: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.6. Optical AI Accelerator Market in Saudi Arabia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.7. Optical AI Accelerator Market in United Arab Emirates (UAE): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.6.8. Optical AI Accelerator Market in Other MEA Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 31.7. Data Triangulation and Validation

32. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

33. ADJACENT MARKET ANALYSIS

34. KEY WINNING STRATEGIES

35. PORTER'S FIVE FORCES ANALYSIS

36. SWOT ANALYSIS

37. VALUE CHAIN ANALYSIS

38. ROOTS STRATEGIC RECOMMENDATIONS

- 38.1. Chapter Overview

- 38.2. Key Business-related Strategies

- 38.2.1. Research & Development

- 38.2.2. Product Manufacturing

- 38.2.3. Commercialization / Go-to-Market

- 38.2.4. Sales and Marketing

- 38.3. Key Operations-related Strategies

- 38.3.1. Risk Management

- 38.3.2. Workforce

- 38.3.3. Finance

- 38.3.4. Others