|

시장보고서

상품코드

2037815

RTU 의약품 포장 시장(제4판) : 동향과 예측(-2035년) - 사전 멸균 유형별/RTU 의약품 포장 시스템 유형별, 용기의 제조 재료별 및 지역별Ready to Use Pharmaceutical Packaging Market (4th Edition): Trends and Forecast Till 2035 - Distribution by Type of Pre-Sterilized / Ready to Use Pharmaceutical Packaging System, Fabrication Material Used for Containers, and Geographical Regions |

||||||

RTU 의약품 포장 시장 - 개요

세계의 RTU(Ready to Use) 의약품 포장 시장은 2035년까지 CAGR 11.5%로 확대하며, 현재 150억 달러에서 2035년에는 399억 달러에 달할 것으로 추정되고 있습니다.

RTU 의약품 포장 시장 - 성장 및 동향

사전 멸균된 RTU 포장 솔루션은 제약사가 무균 충전 및 마무리 공정을 효율화하여 생명을 구하는 치료제의 시장 출시 시간을 단축할 수 있도록 함으로써 무균 의약품 제조의 발전에 중요한 역할을 하고 있습니다. 사전 멸균된 주사기, 바이알, 카트리지 등의 RTU 포맷을 채택하여 세척 및 제열처리와 같은 에너지 집약적인 사내 공정이 불필요합니다. 이를 통해 업무 효율성이 향상되고, 제조업체는 안전한 주사제를 적시에 제공하기 위해 자원을 할당할 수 있습니다.

특히 프리필드 시린지는 정확성과 무공해 투여가 필수적인 바이오의약품 및 GLP-1 치료제 파이프라인의 확대에 따라 고도로 전문화된 솔루션을 제공하고 있으며, 큰 주목을 받고 있습니다. 또한 세포-유전자치료, 항체-약물 접합체(ADC)와 같은 첨단 치료법의 등장은 제약업계의 판도를 바꾸고 있습니다. 이러한 발전과 더불어, 체내 장착형 주사기를 포함한 혁신적인 약물전달 시스템은 RTU(즉시 사용 가능) 포장 솔루션 제공업체에게 큰 성장 기회를 제공하고 있습니다.

이러한 장점에 힘입어 RTU 솔루션은 위탁 충전 및 포장(CFP) 기업 사이에서 특히 소규모의 개별화된 배치 크기 관리와 빈번한 제품 설정에 대한 대응을 위해 채택이 증가하고 있습니다. 이해관계자들이 첨단 소재 코팅과 지속가능한 고분자 용기 개발에 지속적으로 투자함에 따라 RTU 의약품 포장 시장은 향후 수년간 강력한 성장세를 유지할 것으로 예상됩니다.

성장의 원동력 - 시장 확대의 전략적 촉진요인

바이오의약품, 백신 및 첨단 비경구 치료제의 파이프라인이 확장됨에 따라 프리필드 시린지, 바이알, 카트리지 등 오염 위험이 낮은 고품질 포장 솔루션에 대한 수요가 크게 증가하고 있습니다. 미립자, 추출물, 용출물 및 내독소에 대한 민감도가 높기 때문에 제조업체는 엄격한 품질 기준을 충족하는 RTU(Ready To Use) 형식을 점점 더 많이 채택하고 있습니다. 동시에 RTU 패키징은 세척, 제열처리, 멸균과 같은 상류 공정을 생략하여 무균 충전 및 마무리 공정의 업무 효율을 향상시킵니다. 이를 통해 다운타임을 줄이고 라인 운영을 단순화할 수 있습니다. 그 결과, RTU 시스템은 특히 신속한 규제 승인 절차를 거쳐야 하는 제품이나 시간적 제약이 있는 치료제의 출시에 있으며, 보다 빠른 스케일업, 효율적인 기술이전, 시장 출시 기간 단축을 가능하게 합니다.

시장 과제 - 발전을 가로막는 심각한 장애물

사전 멸균 및 RTU 패키징 시장은 기존 패키징에 비해 초기 비용이 높다는 문제에 직면해 있습니다. 이는 사전 멸균, 특수 재료, 고급 핸들링 시스템으로 인해 전체 조달 비용이 증가하기 때문입니다. 이로 인해 특히 중소규모 제조업체의 경우 도입이 제한될 수 있습니다. 또한 전문 공급업체에 대한 의존과 포맷 간 표준화가 미흡한 경우, 공급망 제약과 조달 유연성 저하로 이어질 수 있습니다. 공급업체 네트워크에 어떤 혼란이 발생하면 생산 일정에 직접적인 영향을 미칠 수 있습니다.

또한 RTU 형식은 첨단 충전 및 포장 시스템과의 호환성과 엄격한 취급 절차가 필요하므로 자동화 및 직원 교육에 대한 설비 투자가 필요합니다. 규제 준수 및 검증 요건도 복잡성을 증가시키는 요인이며, 특히 기존 제조 공정에 새로운 RTU 구성요소를 통합할 때 더욱 그러합니다.

RTU 의약품 포장 시장 - 주요 인사이트

이 보고서는 RTU 의약품 포장 시장의 현황을 상세히 분석하고 업계의 잠재적인 성장 기회를 파악합니다. 보고서의 주요 조사 결과는 다음과 같습니다. :

- 현재 무균 충전 및 포장 공정의 효율화와 고가 주사제 치료제의 품질 확보를 위해 105종의 사전 멸균/RTU 1차 포장 용기가 각 사에서 제공되고 있습니다.

- 50% 이상의 기업이 고효능 주사제의 오염 위험을 최소화하고 정확한 약물 투여를 보장하기 위해 자가투여용 멸균/RTU 주사기를 제공하고 있습니다.

- 현재 시장 상황에서는 여러 기업이 개발한 100가지 이상의 멸균/즉시 사용 가능한 캡이 유통되고 있으며, 이들 기업의 대다수(65% 이상)는 대기업/초대형 기업입니다.

- 스토퍼/플런저 스토퍼는 사전 멸균된 네스트 및 튜브 형태로 인해 RTU(즉시 사용 가능) 캡의 가장 일반적인 유형으로 부상했습니다. 특히 80%에 가까운 기업이 감마선 멸균 기술을 사용하여 캡을 멸균하고 있습니다.

- 현재 다양한 이해관계자별로 20종에 가까운 사전 멸균/즉시 사용 가능한 용기 및 캡 시스템이 개발되어 있습니다. 이들 기업의 대다수(40% 이상)는 북미에 본사를 두고 있습니다.

- 대부분의 사전 멸균/RTU 용기는 유리(Type I 붕규산 유리 등)를 사용하여 제조되지만, 사전 멸균/RTU 캡의 약 70%는 고무를 사용하여 제조됩니다.

- 멸균/즉시 사용 가능한 1차 포장 분야 계약의 약 50%가 지난 2년 동안 체결되었습니다. 특히 계약의 과반수(60% 이상)가 유럽에 본사를 둔 기업별로 체결되고 있습니다.

- 2035년까지 수요의 약 40%가 아시아태평양에서 발생할 것으로 예상됩니다. 특히 북미 지역의 사전 멸균/즉시 사용 가능한 1차 포장에 대한 수요는 CAGR 10.4%로 확대될 것으로 예상됩니다.

- RTU(Ready to Use) 형태로의 지속적인 전환은 고부가가치 생물제제를 안전하고 효과적으로 포장하는 데 유용하다는 것이 입증되었으며, 향후 멸균/사용 준비가 완료된 1차 포장 시장을 주도할 것으로 예상됩니다.

- 멸균/즉시 사용 가능한 1차 포장 시장과 관련된 시장 기회는 예측 기간 중 연평균 11.5%의 성장률을 보일 것으로 예상됩니다.

- 북미 시장은 지역내 제조 탄력성 및 지역 밀착형 공급망으로의 빠른 전환으로 인해 비교적 높은 성장률(CAGR 12.4%)을 보일 것으로 예상됩니다.

- 미국 주요 기업별 RTU 1차 포장 시스템의 급속한 기술 발전에 힘입어 미국 RTU 1차 포장 시스템 시장은 연평균 10.4% 성장할 것으로 예상됩니다.

- 신규 바이오의약품의 효율적인 포장 및 공급을 위해 RTU 포장에 대한 수요가 급증하고 있는 점을 감안할 때, 전체 멸균/즉석 사용 1차 포장 시장은 향후 수년간 큰 폭의 성장이 예상됩니다.

멸균/RTU 의약품 포장 시장

시장 규모 및 기회 분석은 다음 매개 변수를 기반으로 세분화됩니다. :

사전 멸균/RTU 의약품 포장 시스템 유형별

- 주사기

- 바이알

- 카트리지

- 캡

- 캡

- 플런저

- 인감

- 스토퍼

- 팁 캡/ 니들 쉴드

용기 제조 재료 유형별

- 유리

- 플라스틱

지역별

- 북미

- 북미

- 아시아태평양

- 라틴아메리카

- 중동 및 북아프리카

RTU 의약품 포장 시장 - 주요 부문

RTU(즉시 사용 가능) 캡이 RTU 의약품 포장 시장의 성장을 주도하고 있습니다.

올해 RTU용 캡은 전체 시장의 약 65%를 차지하고 있습니다. 이러한 압도적인 점유율은 주로 고처리량 무균 충전 및 마감 공정에서 각 충전 용기에 대량으로 필요한 필수 부품인 실, 스토퍼, 캡, 플런저, 팁 캡/니들 쉴드 등 사전 멸균된 캡에 대한 일관된 대량 수요에 기인합니다. 때문입니다.

반면, RTU 바이알 부문은 예측 기간 중 더 높은 CAGR을 보일 것으로 예상됩니다. 이러한 성장은 자본 집약적인 세척 및 멸균 공정을 제거할 수 있는 능력에 기인하며, 이를 통해 제조업체는 운영 비용을 절감하고, 탄소발자국을 줄이며, 중요한 치료제의 시장 출시 기간을 단축할 수 있습니다.

RTU 의약품 포장 시장에서는 유리 재질이 주류를 이루고 있습니다.

시장 예측에 따르면 용기용 RTU 의약품 포장 시장에서 유리계 제조 재료가 가장 큰 점유율(85% 이상)을 차지하고 있습니다. 이러한 장점은 주로 우수한 장벽 특성, 추출물이 적은 특성, 다양한 비경구 제제와의 호환성 등으로 인해 고가 의약품 포장에 유리가 선호되고 있기 때문입니다.

반면, 플라스틱 성형 재료는 예측 기간 중 16.2%의 견고한 CAGR로 성장할 것으로 예상됩니다. 이러한 성장은 고리형 올레핀 폴리머(COP), 고리형 올레핀 코폴리머(COC) 등 첨단 소재의 채택 확대에 힘입은 바 큽니다. 또한 지속가능성 관련 규제의 발전으로 인해 순환형 포장 솔루션으로의 전환이 가속화되고 있습니다. TOPAC(R)과 같은 주요 COC 등급은 단일 소재 또는 폴리올레핀과의 호환성을 고려한 설계를 가능하게 하여 재활용성을 높이고 환경에 미치는 영향을 줄입니다.

스마트 커넥티드 패키징 - RTU 솔루션을 데이터베이스 자산으로 전환하는 RTU 솔루션

스마트 커넥티드 RTU(Ready-to-Use) 포장은 제약업계의 중요한 기술 발전으로, 제품 보호와 공급망 가시성을 모두 향상시킬 수 있습니다. 이 접근 방식은 IoT 센서, RFID/NFC 태그, 고유한 디지털 식별자 등 디지털 기술을 포장 시스템에 통합하여 각 유닛을 데이터 지원 자산으로 효과적으로 변환합니다.

이러한 혁신은 온도에 민감한 바이오의약품 및 백신의 콜드 체인 무결성을 강화하는 데 중요한 역할을 하며, 제조, 유통, 투여의 전 과정에서 제품의 효능을 보장합니다. 또한 센서와 디지털 식별자를 내장하여 추적성을 향상시키고, 엔드투엔드 검증을 통해 위조 방지 대책을 지원하며, 이상 징후를 신속하게 감지하여 규정 준수와 환자 안전을 향상시킵니다.

무균, 무공해 RTU 포장 작업을 실현하는 로봇 자동화 로봇 자동화

로봇 자동화는 특히 무균성, 속도 및 운영상의 유연성이 필수적인 RTU(Ready to Use) 포맷에서 제약 포장 분야를 점점 더 변화시키고 있습니다. Steriline의 'Robotic 3D Control and Picking' 시스템과 같은 첨단 로봇 솔루션은 첨단 비전 기술을 활용하여 중첩된 RTU 용기를 정확하게 식별하고 처리합니다. 이를 통해 사람의 개입을 최소화하고 높은 정확도와 처리량을 유지하면서 오염 위험을 줄일 수 있습니다.

유럽이 세계 RTU 의약품 포장 시장을 주도하다

현재 유럽은 전 세계 RTU 의약품 포장 시장을 독점하고 있으며, 전체 매출 점유율의 50% 이상을 차지하고 있습니다. 이러한 추세는 유럽연합(EU)내 잘 구축된 의약품 인프라와 진보적인 규제 환경에 의해 지원되고 있습니다. Schott Pharma, Gerresheimer, Stevanato 등 주요 기업은 전 세계 공급망에서 RTU 포맷을 표준화하기 위한 'Ready-to-Use Alliance'와 같은 구상을 출범시켜 이 지역의 입지를 더욱 강화하고 있습니다.

아시아태평양 및 북미 신흥 시장 동향

아시아태평양은 중국, 인도 등 각국의 현지화된 충전 및 포장 능력에 대한 대규모 투자에 힘입어 더 높은 CAGR로 성장할 것으로 예상됩니다. 다른 성장 요인으로는 정부 주도의 백신 접종 프로그램과 바이오시밀러 파이프라인의 확대가 있으며, 이는 글로벌 수출 기준을 충족하는 확장 가능한 무균 용기 및 클로저 시스템에 대한 수요를 증가시키고 있습니다.

1차 조사 개요

이 분야의 여러 이해관계자들과의 논의는 본 조사에서 제시된 견해와 인사이트에 영향을 미쳤습니다. 본 시장 보고서에는 다음과 같은 관계자와의 상세한 인터뷰 기록이 포함되어 있습니다. :

- 벨기에,중견기업,사업 개발 및 기술 담당 이사

- 진행자,중견기업,영국,영국

- 미국 중견기업,전 사업개발 프로젝트 매니저

- 인도 대기업 창업자 겸 매니징 디렉터

RTU 의약품 포장 시장의 주요 기업 사례

- Aptar

- Becton, Dickinson and Company

- West Pharmaceutical Services

- DWK Life Sciences

- Datwyler

- Gerresheimer

- Stevanato

- SCHOTT

- Terumo

- Daikyo Seiko

- China Lemon Trading

RTU 의약품 포장 시장 - 조사 범위

- 시장 규모 및 기회 분석: 이 보고서는 [A] 멸균/사용 준비가 완료된 의약품 포장 시스템 유형, [B] 용기 제조 재료 유형, [C] 주요 지역적 지역 등 주요 시장 부문에 초점을 맞춘 글로벌 사용 준비 의약품 포장 시장에 대한 상세한 분석을 제공합니다. 분석합니다.

- 사전 멸균/사용 준비가 완료된 용기 시장 현황: [A] 용기 유형, [B] 제조 재료의 유형, [C] 사용 멸균 기술의 유형, [D] 용기 용량, [E] 충전되는 분자의 유형, [F] 사용 가능한 포장 형태, [G] 설립 연도, [H] 기업 규모, [I] 본사 소재지.

- 사전 멸균/즉시 사용 가능한 캡 시장 현황: [A] 캡의 유형, [B] 사용되는 제조 재료의 유형, [C] 지원되는 용기, [D] 사용되는 멸균 기술의 유형, [E] 충전되는 분자의 유형, [F] 사용 가능한 포장 형태, [G] 설립 연도, [H] 회사, [I] 본사 소재지.

- 사전 멸균/즉시 사용 가능한 컨테이너 클로저 종합 시스템 시장 현황: [A]클로저 유형, [B]사용 재료 유형, [C]컨테이너 유형, [D]사용 멸균 기술 유형, [E]충전되는 분자 유형, [F]사용 가능한 포장 형태, [G]설립 연도, [H] 회사 설립 연도, [H] 본사 소재지. 기업 및 [I] 본사 소재지.

- 기업 경쟁력 분석: 사전 멸균/즉시 사용 가능한 1차 포장 시스템 공급업체에 대한 종합적인 경쟁 분석으로, [A] 기업의 강점, [B] 제품의 강점, [C] 포트폴리오의 다양성 등의 요인을 검증합니다.

- 기업 개요: 사전 멸균/즉시 사용 가능한 용기 및 캡을 제공하는 주요 기업의 상세한 프로필입니다. [A] 기업 개요, [B] 재무 정보(가능한 경우), [C] 제품 포트폴리오, [D] 최근 동향 및 정보에 기반한 미래 전망에 초점을 맞추고 있습니다.

- 제휴 및 협업: [A]제휴 연도, [B]제휴 형태, [C]파트너 유형, [D]중점 분야, [E]포장 시스템 유형, [F]포장 재료 유형, [G]가장 활발한 플레이어, [H]지역 등 여러 매개 변수를 기반으로 RTU 의약품 포장 시장의 이해관계자들이 체결한 거래에 대한 인사이트 분석을 제공합니다.

- 수요 분석: [A] 1차 포장 시스템 유형, [B] 사용되는 제조 재료 등 다양한 관련 매개 변수를 기반으로 멸균/사용 준비가 완료된 용기 및 캡에 대한 현재 및 미래 수요를 상세히 평가합니다.

- 의약품 포장의 미래 동향: 사전 멸균 및 즉시 사용 가능한 의약품 포장 산업 전반의 새로운 동향에 대한 개요입니다.

- 사례 연구: 의약품 포장에서의 로봇: 의약품 제조 및 충진 및 마무리 공정에서 로봇의 역할에 대한 자세한 사례 연구로, 로봇의 장점과 능력에 초점을 맞추고 있습니다. 또한 다양한 제약용 로봇의 리스트과 함께 각 제조사 및 용도에 대한 자세한 정보도 제공합니다.

- 시장 영향 분석: 시장 성장에 영향을 미칠 수 있는 촉진요인, 제약 요인, 기회 및 기존 과제 등 다양한 요인에 대한 철저한 분석입니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 개요

제6장 서론

제7장 멸균/RTU 1차 포장 - 용기 전체상

제8장 멸균/RTU 1차 포장 - 뚜껑 전체상

제9장 멸균/RTU 1차 포장 - 용기-마개 시스템 전체상

제10장 기업의 경쟁력 분석

제11장 기업 개요

제12장 파트너십과 협력 관계

제13장 수요 분석

제14장 의약품 포장에서 향후 동향

제15장 사례 연구 : 의약품 포장에서 로봇의 활용

제16장 시장 영향 분석 : 촉진요인, 저해요인, 기회, 과제

제17장 세계의 RTU 의약품 포장 시장

제18장 RTU 의약품 포장 시장(멸균/RTU 1차 포장 시스템 유형별)

제19장 RTU 의약품 포장 시장(용기의 제조 재료 유형별)

제20장 RTU 의약품 포장 시장(지역별, )

제21장 북미에서 멸균/RTU 1차 포장 시장

제22장 유럽에서 멸균/RTU 1차 포장 시장

제23장 아시아태평양에서 멸균/RTU 1차 포장 시장

제24장 라틴아메리카에서 멸균/RTU 1차 포장 시장

제25장 중동 및 북아프리카에서 멸균/RTU 1차 포장 시장

제26장 결론

제27장 경영 임원의 인사이트

제28장 부록 1 : 표형식 데이터

제29장 부록 2 : 기업 및 조직 리스트

KSA 26.06.01Ready to Use Pharmaceutical Packaging Market: Overview

As per Roots Analysis, the global ready-to-use pharmaceutical packaging market is estimated to grow from USD 15.0 billion in the current year to USD 39.9 billion by 2035, at a CAGR of 11.5% during the forecast period, till 2035.

Ready to Use Pharmaceutical Packaging Market: Growth and Trends

Pre-sterilized, ready-to-use (RTU) packaging solutions are playing a critical role in advancing sterile drug manufacturing by enabling pharmaceutical companies to streamline aseptic fill-finish operations and accelerate time-to-market for life-saving therapies. The adoption of RTU formats such as pre-sterilized syringes, vials, and cartridges eliminates the need for energy-intensive in-house processes, including washing and depyrogenation. This, in turn, enhances operational efficiency and allows manufacturers to allocate resources towards the timely delivery of safe injectable products.

Notably, pre-filled syringes have gained considerable traction, offering a highly specialized solution for the expanding pipeline of biologics and GLP-1 therapies, where precision and contamination-free administration are essential. Further, Further, the emergence of advanced therapeutic modalities such as cell and gene therapies and antibody-drug conjugates is reshaping the pharmaceutical landscape. Alongside these developments, innovative drug delivery systems, including on-body wearable injectors, are creating substantial growth opportunities for RTU packaging solution providers.

Driven by these advantages, RTU solutions are witnessing increased adoption among contract fill-finish organizations, particularly for managing smaller, personalized batch sizes and accommodating frequent product setup. As industry stakeholders continue to invest in the development of advanced material coatings and sustainable polymer-based containers, the ready-to-use pharmaceutical packaging market is expected to maintain a strong growth trajectory in the coming years.

Growth Drivers: Strategic Enablers of Market Expansion

The growing pipeline of biologics, vaccines, and advanced parenteral therapies is significantly increasing the demand for high-quality, low-contamination-risk packaging solutions such as prefilled syringes, vials, and cartridges. Due to their sensitivity to particulates, extractables, leachables, and endotoxins, manufacturers are increasingly adopting ready-to-use (RTU) formats that meet stringent quality standards. At the same time, RTU packaging enhances operational efficiency in aseptic fill-finish processes by eliminating upstream steps such as washing, depyrogenation, and sterilization. This reduces downtime and simplifies line operations. As a result, RTU systems enable faster scale-up, streamlined technology transfer, and accelerated time-to-market, particularly for products under expedited regulatory pathways and time-sensitive therapeutic launches.

Market Challenges: Critical Barriers Impeding Progress

The pre-sterilized, ready-to-use (RTU) packaging market faces challenges related to higher upfront costs compared to conventional packaging, as pre-sterilization, specialized materials, and advanced handling systems increase overall procurement expenses. This can limit adoption, particularly among small and mid-sized manufacturers. In addition, dependence on specialized suppliers and limited standardization across formats may lead to supply chain constraints and reduced flexibility in sourcing. Any disruption in supplier networks can directly impact production timelines.

Further, RTU formats require compatibility with advanced fill-finish systems and strict handling protocols, necessitating capital investment in automation and workforce training. Regulatory compliance and validation requirements also add complexity, particularly when integrating new RTU components into existing manufacturing processes.

Ready to Use Pharmaceutical Packaging Market: Key Insights

The report delves into the current state of the ready-to-use pharmaceutical packaging market and identifies potential growth opportunities within industry. Some key findings from the report include:

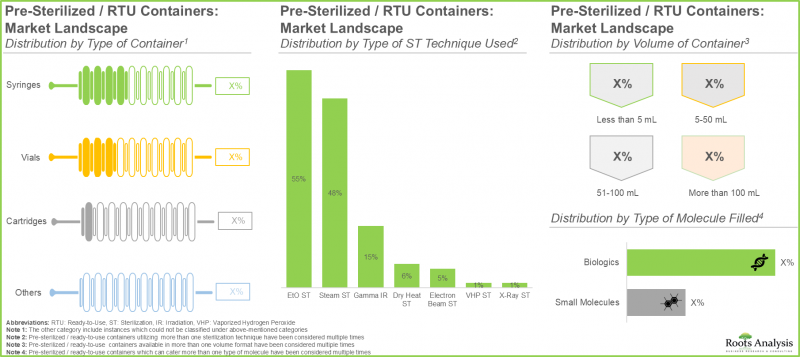

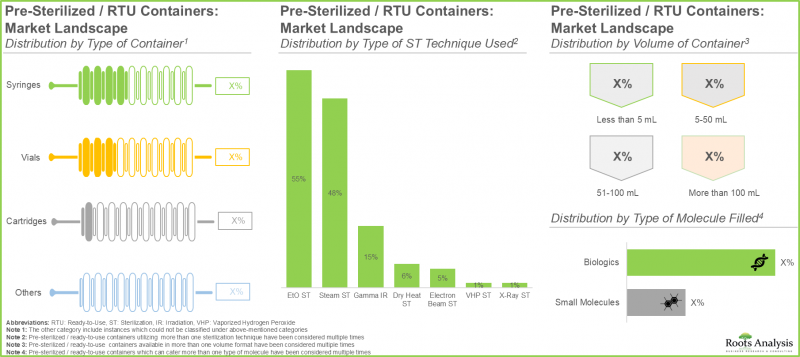

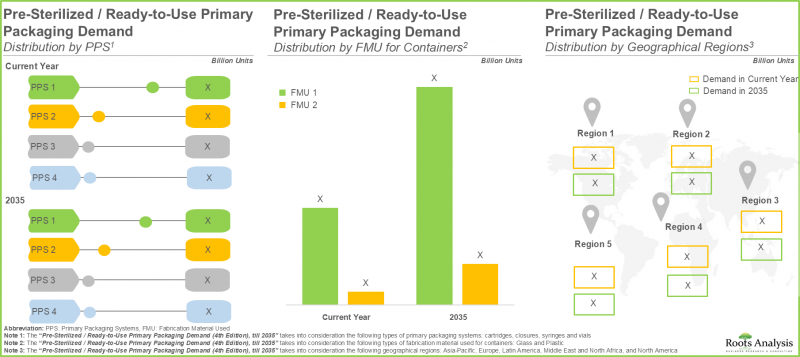

- Currently, 105 pre-sterilized / ready-to-use primary packaging containers are offered by companies for the purpose of streamlining aseptic fill-finish operations and ensuring the integrity of high-value injectable therapies.

- More than 50% of the companies offer self-administering pre-sterilized / ready-to-use syringes for ensuring precise drug delivery by minimizing contamination risk for high-potency injectable therapies.

- The current market landscape features more than 100 pre-sterilized / ready-to-use closures developed by several companies; majority (>65%) of these firms are large / very large players.

- Stoppers / plunger stoppers emerged as the most common types of RTU closure owing to their pre-sterilized nest and tub format; notably, close to 80% of the companies use gamma sterilization techniques for closures.

- Close to 20 pre-sterilized / ready-to-use container-closure systems are being developed by various stakeholders; majority (>40%) of these firms are headquartered in North America.

- Most of the pre-sterilized / ready-to-use containers are fabricated using glass (such as type I borosilicate), while close to 70% of the pre-sterilized / ready-to-use closures are fabricated using rubber.

- Around 50% of the agreements in the pre-sterilized / ready-to-use primary packaging domain were inked in the last two years; notably, majority (>60%) of the deals were inked by the players headquartered in Europe.

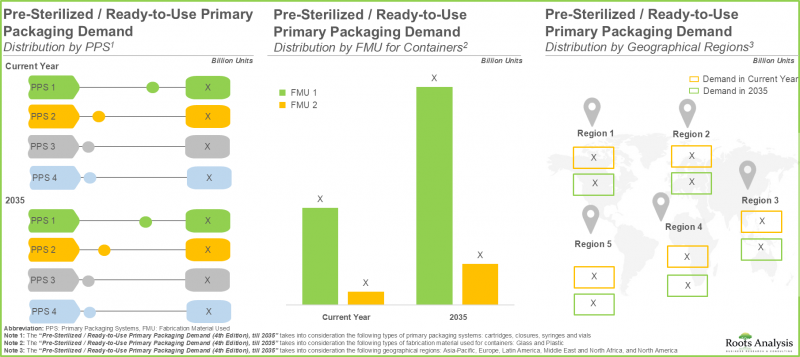

- By 2035, close to 40% of the demand is anticipated to be generated in Asia-Pacific; notably, the demand for pre-sterilized / ready-to-use primary packaging in North America is projected to grow at a CAGR of 10.4%.

- Ongoing shift towards RTU formats have proven useful in the safe and effective packaging of high value biologics; these are anticipated to drive the pre-sterilized / ready-to-use primary packaging market in future.

- The market opportunity associated with pre-sterilized / ready-to-use primary packaging market is expected to witness an annualized growth rate of 11.5% during the forecast period.

- The market in North America is likely to grow at a relatively higher pace (CAGR of 12.4%), owing to a rapid shift towards manufacturing resilience and localized supply chains within this region.

- Driven by the rapid technological advancements within RTU primary packaging systems by prominent players in the US, the market is expected to grow at CAGR of 10.4%.

- Given the surge in demand for RTU packaging in efficient containment and delivery of novel biologics, the overall pre-sterilized / ready-to-use primary packaging market is poised for substantial growth in the coming years.

Pre-Sterilized / Ready to Use Pharmaceutical Packaging Market

The market sizing and opportunity analysis has been segmented across the following parameters:

By Type of Pre-Sterilized / Ready to Use Pharmaceutical Packaging System

- Syringes

- Vials

- Cartridges

- Closures

- Caps

- Plungers

- Seals

- Stoppers

- Tip Caps / Needle Shields

By Type of Fabrication Material Used for Containers

- Glass

- Plastic

By Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Ready to Use Pharmaceutical Packaging Market: Key Segments

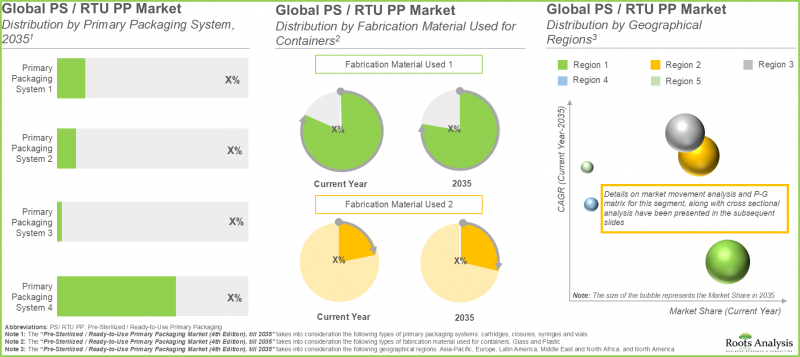

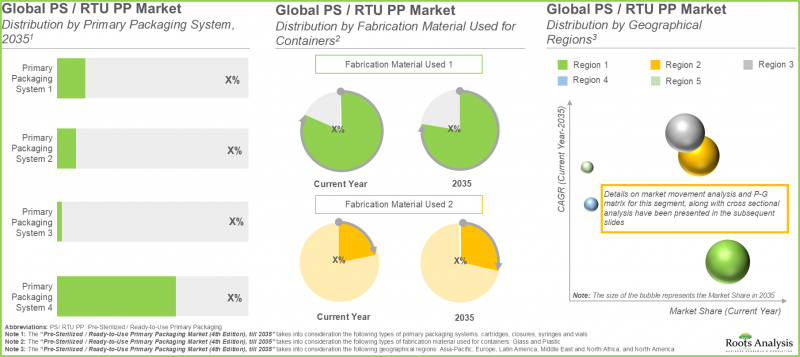

RTU Closures Driving Growth in the Ready-to-Use Pharmaceutical Packaging Market

In the current year, RTU closures account for approximately 65% of the overall market share. This dominance is largely attributed to the consistent, high-volume demand for pre-sterilized closures, including seals, stoppers, caps, plungers, and tip caps / needle shields, which are essential components required in bulk for each filled container within high-throughput aseptic fill-finish operations.

Conversely, the RTU vials segment is projected to witness a higher CAGR over the forecast period. This growth is driven by their ability to eliminate the need for capital-intensive washing and sterilization processes, enabling manufacturers to reduce operational costs, lower their carbon footprint and accelerate time-to-market for critical therapies.

Glass Fabrication Materials Dominate the RTU Pharmaceutical Packaging Market

According to market forecasts, glass-based fabrication materials account for the largest share (>85%) of the RTU pharmaceutical packaging market for containers. This dominance is primarily driven by the increased preference for glass in packaging high-value drugs, owing to its superior barrier properties, minimal extractables profile, and established compatibility with a broad range of parenteral formulations.

In contrast, plastic fabrication materials are projected to grow at a robust CAGR of 16.2% during the forecast period. This growth is supported by the increasing adoption of advanced materials such as cyclic olefin polymers (COP) and cyclic olefin copolymers (COC). Additionally, evolving sustainability regulations are accelerating the transition toward circular packaging solutions, with leading COC grades such as TOPAC(R) enabling mono-material or polyolefin-compatible designs that enhance recyclability and reduce environmental impact.

Smart and Connected Packaging Transforming RTU Solutions into Data-Driven Assets

Smart and connected RTU packaging represents a significant technological advancement within the pharmaceutical industry, enhancing both product protection and supply chain visibility. This approach integrates digital technologies including IoT sensors, RFID / NFC tags, and unique digital identifiers into packaging systems, effectively converting each unit into a data-enabled asset.

These innovations play a critical role in strengthening cold chain integrity for temperature-sensitive biologics and vaccines, ensuring product efficacy throughout manufacturing, distribution, and administration. Furthermore, the incorporation of sensors and digital identifiers enhances traceability, supports anti-counterfeiting measures through end-to-end verification, and enables rapid anomaly detection, thereby improving regulatory compliance and patient safety.

Robotic Automation Enabling Aseptic and Contamination-Free RTU Packaging Operations

Robotic automation is increasingly transforming the pharmaceutical packaging landscape, particularly for RTU formats where sterility, speed, and operational flexibility are critical. Advanced robotic solutions, such as Steriline's Robotic 3D Control and Picking system, utilize sophisticated vision technologies to accurately identify and handle nested RTU containers. This minimizes human intervention, thereby reducing contamination risks while maintaining high precision and throughput.

Europe Leads the Global RTU Pharmaceutical Packaging Market

Europe currently dominates the global RTU pharmaceutical packaging market, accounting for over 50% of total revenue share. This trend is supported by a well-established pharmaceutical infrastructure and a progressive regulatory environment within the European Union. Key industry players, including Schott Pharma, Gerresheimer, and Stevanato, have further strengthened the region's position by forming initiatives such as the "Ready-to-Use Alliance," aimed at standardizing RTU formats across the global supply chain.

Emerging Market Trends in Asia-Pacific and North America

Asia-Pacific is expected to grow at a higher CAGR driven by significant investments in localized fill-finish capabilities across countries such as China and India. Additional growth factors include government-supported vaccination programs and expanding biosimilar pipelines, which are increasing demand for scalable, sterile container-closure systems that meet global export standards.

Primary Research Overview

Discussions with multiple stakeholders in this domain influenced the opinions and insights presented in this study. The market report includes detailed transcripts of interviews conducted with the following individuals:

- Business Development and Technology Director, Mid-sized Company, Belgium

- Facilitator, Mid-sized Company, UK

- Former Project Manager of Business Development, Mid-sized Company, US

- Founder and Managing Director, Large Company, India

Example Players in the Ready to Use Pharmaceutical Packaging Market

- Aptar

- Becton, Dickinson and Company

- West Pharmaceutical Services

- DWK Life Sciences

- Datwyler

- Gerresheimer

- Stevanato

- SCHOTT

- Terumo

- Daikyo Seiko

- China Lemon Trading

Ready to Use Pharmaceutical Packaging Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global ready-to-use pharmaceutical packaging market, focusing on key market segments, including [A] type of pre-sterilized / ready to use pharmaceutical packaging system , [B] type of fabrication material used for containers and [C] key geographical regions.

- Pre-Sterilized / Ready to Use Containers Market Landscape: A comprehensive evaluation of the pre-sterilized / ready to use containers, based on several relevant parameters, such as [A] type of container, [B] type of fabrication material used, [C] type of sterilization technique used, [D] volume of container, [E] type of molecule filled, [F] available packaging format, [G] year of establishment, [H] company size, and [I] location of headquarters.

- Pre-Sterilized / Ready to Use Closures Market Landscape: A comprehensive evaluation of the pre-sterilized / ready to use closures, based on several relevant parameters, such as [A] type of closure, [B] type of fabrication material used, [C] compatible container(s), [D] type of sterilization technique used, [E] type of molecule filled, [F] available packaging format, [G] year of establishment, [H] company and [I] location of headquarters.

- Pre-Sterilized / Ready to Use Container-Closures Overall Systems Market Landscape: A comprehensive evaluation of the pre-sterilized / ready to use container-closure systems, based on several relevant parameters, such as [A] type of closure, [B] type of fabrication material used, [C] type of container(s), [D] type of sterilization technique used, [E] type of molecule filled, [F] available packaging format, [G] year of establishment, [H] company and [I] location of headquarters.

- Company Competitiveness Analysis: A comprehensive competitive analysis of pre-sterilized / ready-to-use primary packaging system providers, examining factors, such as [A] company strength, [B] product strength and [C] portfolio diversity.

- Company Profiles: In-depth profiles of key players that are engaged in offering pre-sterilized / ready-to-use containers and closures, focusing on [A] overview of the company, [B] financial information (if available), [C] product portfolio and [D] recent developments and an informed future outlook.

- Partnerships and Collaborations: An insightful analysis of the deals inked by stakeholders in the ready-to-use pharmaceutical packaging market, based on several parameters, such as [A] year of partnership, [B] type of partnership. [C] type of partner, [D] focus area, [E] type of packaging system, [F] type of packaging material, [G] most active players and [H] geography.

- Demand Analysis: A detailed assessment of the current and future demand for pre-sterilized / ready to use containers and closures, based on various relevant parameters, such as [A] type of primary packaging system and [B] material of fabrication used.

- Upcoming Trends in Pharmaceutical Packaging: A brief description about the emerging trends in the overall pre-sterilized ready-to-use pharmaceutical packaging industry.

- Case Study: Robots in Pharmaceutical Packaging: A detailed case study on the role of robots in the pharmaceutical manufacturing and fill / finish process, highlighting its benefits and capabilities. It provides a list of the various types of pharmaceutical robots, along with details on their respective manufacturers and applications.

- Market Impact Analysis: A thorough analysis of various factors, such as drivers, restraints, opportunities, and existing challenges that are likely to impact market growth.

Key Questions Answered in this Report

- Which are the leading companies in the pre-sterilized / ready-to-use primary packaging system providers market?

- Which region dominates the single use pre-sterilized / ready-to-use primary packaging system providers market?

- What are the key trends observed in the single use pre-sterilized / ready-to-use primary packaging system providers market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by single use pre-sterilized / ready-to-use primary packaging system providers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Marget Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Chapter Overview

- 5.2. Executive Summary: Market Landscape

- 5.3. Executive Summary: Market Trends

- 5.4. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Pharmaceutical Packaging and Filling

- 6.2.1. Necessity of Pharmaceutical Packaging

- 6.2.2. Types of Packaging

- 6.2.3. Limitations of Traditional Primary Packaging

- 6.2.4. Innovation in Pharmaceutical Packaging

- 6.3. Ready-to-Use Primary Packaging

- 6.3.1. Sterilization of Primary Packaging Material

- 6.3.1.1. Sterilization Techniques

- 6.3.2. Advantages of Ready-to-Use Primary Packaging

- 6.3.3. Cost Saving Opportunities in Ready-To-Use Primary Packaging

- 6.3.4. Current Demand for Ready-to-Use Primary Packaging and Key Enablers

- 6.3.1. Sterilization of Primary Packaging Material

- 6.4. Concluding Remarks

7. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING: CONTAINERS OVERALL LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Pre-Sterilized / Ready-to-Use Containers: Overall Market Landscape

- 7.2.1. Analysis by Type of Container

- 7.2.2. Analysis by Type of Fabrication Material Used

- 7.2.3. Analysis by Type of Sterilization Technique Used

- 7.2.4. Analysis by Volume of Container

- 7.2.5. Analysis by Type of Molecule Filled

- 7.2.6. Analysis by Available Packaging Format

- 7.3. Pre-Sterilized / Ready-to-Use Containers Providers: Overall Market Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.3.4. Most Active Players: Analysis by Number of Containers

8. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING: CLOSURES OVERALL LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Pre-Sterilized / Ready-to-Use Closures: Overall Market Landscape

- 8.2.1. Analysis by Type of Closure

- 8.2.2. Analysis by Type of Fabrication Material Used

- 8.2.3. Analysis by Compatible Container

- 8.2.4. Analysis by Type of Sterilization Technique Used

- 8.2.5. Analysis by Type of Molecule Filled

- 8.2.6. Analysis by Available Packaging Format

- 8.3. Pre-Sterilized / Ready-to-Use Closures Providers: Overall Market Landscape

- 8.3.1. Analysis by Year of Establishment

- 8.3.2. Analysis by Company Size

- 8.3.3. Analysis by Location of Headquarters

- 8.3.4. Most Active Players: Analysis by Number of Closures

9. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING: CONTAINER - CLOSURE SYSTEMS OVERALL LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Pre-Sterilized / Ready-to-Use Container - Closure Systems: Overall Market Landscape

- 9.2.1. Analysis by Type of Container

- 9.2.2. Analysis by Type of Closure

- 9.2.3. Analysis by Type of Fabrication Material Used

- 9.2.3.1. Analysis by Type of Fabrication Material Used in Containers

- 9.2.3.2. Analysis by Type of Fabrication Material Used in Closures

- 9.2.4. Analysis by Type of Sterilization Technique Used

- 9.2.5. Analysis by Volume of Container

- 9.2.6. Analysis by Type of Molecule Filled

- 9.3. Pre-Sterilized / Ready-to-Use Container - Closure Systems Providers: Overall Market Landscape

- 9.3.1. Analysis by Year of Establishment

- 9.3.2. Analysis by Company Size

- 9.3.3. Analysis by Location of Headquarters

- 9.3.4. Most Active Players: Analysis by Number of Container - Closure Systems

10. COMPANY COMPETITIVENESS ANALYSIS

- 10.1. Chapter Overview

- 10.2. Assumptions and Key Parameters

- 10.3. Methodology

- 10.4. Overview of Peer Groups

- 10.5. Pre-Sterilized / Ready-to-Use Primary Packaging System Providers: Company Competitiveness Analysis

- 10.5.1. Pre-Sterilized / Ready-to-Use Primary Packaging System Providers Headquartered in North America

- 10.5.2. Pre-Sterilized / Ready-to-Use Primary Packaging System Providers Headquartered in Europe

- 10.5.3. Pre-Sterilized / Ready-to-Use Primary Packaging System Providers Headquartered in Asia-Pacific

11. COMPANY PROFILES

- 11.1. Chapter Overview

- 11.2. Pre-Sterilized / Ready-to-Use Primary Packaging Providers Headquartered in North America

- 11.2.1. Aptar

- 11.2.1.1. Company Overview

- 11.2.1.2. Product Portfolio

- 11.2.1.3. Roots Analysis View

- 11.2.2. Becton, Dickinson and

- 11.2.1. Aptar

Company

- 11.2.2.1. Company Overview

- 11.2.2.2. Product Portfolio

- 11.2.2.3. Roots Analysis View

- 11.2.3. West Pharmaceutical Services

- 11.2.3.1. Company Overview

- 11.2.3.2. Product Portfolio

- 11.2.3.3. Roots Analysis View

- 11.3. Pre-Sterilized / Ready-to-Use Primary Packaging Providers Headquartered in Europe

- 11.3.1. DWK Life Sciences

- 11.3.1.1. Company Overview

- 11.3.1.2. Product Portfolio

- 11.3.1.3. Roots Analysis View

- 11.3.2. Datwyler

- 11.3.2.1. Company Overview

- 11.3.2.2. Product Portfolio

- 11.3.2.3. Roots Analysis View

- 11.3.3. Gerresheimer

- 11.3.3.1. Company Overview

- 11.3.3.2. Product Portfolio

- 11.3.3.3. Roots Analysis View

- 11.3.4. SCHOTT

- 11.3.4.1. Company Overview

- 11.3.4.2. Product Portfolio

- 11.3.4.3. Roots Analysis View

- 11.3.5. Stevanato

- 11.3.5.1. Company Overview

- 11.3.5.2. Product Portfolio

- 11.3.5.3. Roots Analysis View

- 11.3.1. DWK Life Sciences

- 11.4. Pre-Sterilized / Ready-to-Use Primary Packaging Providers Headquartered in Asia-Pacific

- 11.4.1. Terumo

- 11.4.1.1. Company Overview

- 11.4.1.2. Product Portfolio

- 11.4.1.3. Roots Analysis View

- 11.4.2. Daikyo Seiko

- 11.4.2.1. Company Overview

- 11.4.2.2. Product Portfolio

- 11.4.2.3. Roots Analysis View

- 11.4.3. China Lemon Trading

- 11.4.3.1. Company Overview

- 11.4.3.2. Product Portfolio

- 11.4.3.3. Roots Analysis View

- 11.4.1. Terumo

12. PARTNERSHIPS AND COLLABORATIONS

- 12.1. Chapter Overview

- 12.2. Partnership Models

- 12.3. Pre-Sterilized / Ready-to-Use Primary Packaging: Partnerships and Collaborations

- 12.3.1. Analysis by Year of Partnership

- 12.3.2. Analysis by Type of Partnership

- 12.3.3. Analysis by Year and Type of Partnership

- 12.3.4. Analysis by Type of Primary Packaging System

- 12.3.5. Analysis by Type of Fabrication Material Used

- 12.3.6. Most Active Players: Analysis by Number of Partnerships

- 12.3.7. Analysis by Geography

- 12.3.7.1. Intracontinental and Intercontinental Deals

- 12.3.7.2. International and Local Deals

13. DEMAND ANALYSIS

- 13.1. Chapter Overview

- 13.2. Assumptions and Methodology

- 13.3. Global Demand for Pre-Sterilized / Ready-to-Use Primary Packaging System

- 13.3.1. Demand for Pre-Sterilized / Ready-to-Use Primary Packaging System: Analysis by Type of Primary Packaging System

- 13.3.1.1. Demand for Pre-Sterilized / Ready-to-Use Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.1.2. Demand for Pre-Sterilized / Ready-to-Use Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.1.3. Demand for Pre-Sterilized / Ready-to-Use Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.1.4. Demand for Pre-Sterilized / Ready-to-Use Closures, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Container: Analysis by Type of Fabrication Material Used for Containers

- 13.3.2.1. Demand For Pre-Sterilized / Ready-to-Use Glass Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.1.1. Demand For Pre-Sterilized / Ready-to-Use Glass Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.1.2. Demand For Pre-Sterilized / Ready-to-Use Glass Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.1.3. Demand For Pre-Sterilized / Ready-to-Use Glass Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.2. Demand For Pre-Sterilized / Ready-to-Use Plastic Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.2.1. Demand For Pre-Sterilized / Ready-to-Use Plastic Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.2.2. Demand For Pre-Sterilized / Ready-to-Use Plastic Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.2.3. Demand For Pre-Sterilized / Ready-to-Use Plastic Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2.1. Demand For Pre-Sterilized / Ready-to-Use Glass Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging System: Analysis by Geographical Regions

- 13.3.3.1. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.1.1. Demand For Pre-Sterilized / Ready-to-Use Syringes in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.1.2. Demand For Pre-Sterilized / Ready-to-Use Vials in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.1.3. Demand For Pre-Sterilized / Ready-to-Use Cartridges in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.1.4. Demand For Pre-Sterilized / Ready-To-Use Closures in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.2. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.2.1. Demand For Pre-Sterilized / Ready-to-Use Syringes in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.2.2. Demand For Pre-Sterilized / Ready-to-Use Vials in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.2.3. Demand For Pre-Sterilized / Ready-to-Use Cartridges in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.2.4. Demand For Pre-Sterilized / Ready-To-Use Closures in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.3. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.3.1. Demand For Pre-Sterilized / Ready-to-Use Syringes in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.3.2. Demand For Pre-Sterilized / Ready-to-Use Vials in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.3.3. Demand For Pre-Sterilized / Ready-to-Use Cartridges in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.3.4. Demand For Pre-Sterilized / Ready-To-Use Closures in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.4. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.4.1. Demand For Pre-Sterilized / Ready-to-Use Syringes in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.4.2. Demand For Pre-Sterilized / Ready-to-Use Vials in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.4.3. Demand For Pre-Sterilized / Ready-to-Use Cartridges in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.4.4. Demand For Pre-Sterilized / Ready-To-Use Closures in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.5. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.5.1. Demand For Pre-Sterilized / Ready-to-Use Syringes in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.5.2. Demand For Pre-Sterilized / Ready-to-Use Vials in Middle East and North Africa Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.5.3. Demand For Pre-Sterilized / Ready-to-Use Cartridges in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.5.4. Demand For Pre-Sterilized / Ready-To-Use Closures in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.3.1. Demand For Pre-Sterilized / Ready-to-Use Primary Packaging Systems in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.1. Demand for Pre-Sterilized / Ready-to-Use Primary Packaging System: Analysis by Type of Primary Packaging System

14. UPCOMING TRENDS IN PHARMACEUTICAL PACKAGING

- 14.1. Chapter Overview

- 14.2. Preference for Self-Medication of Drugs, Through the Use of Modern Drug Delivery Devices

- 14.2.1. Preference for Self-Medication of Drugs, Through the Use of Modern Drug Delivery Devices

- 14.2.2. Development of Improved Packaging Components and Efforts to Optimize Manufacturing Costs

- 14.2.3. Availability of Modular Facilities

- 14.2.4. Growing Demand and Preference for Personalized Therapies

- 14.2.5. Rise in Provisions for Automating Fill / Finish Operations

- 14.2.6. Surge in Partnership Activity

- 14.2.7. Increase in Initiatives Undertaken by Industry Stakeholders in Developing Regions

- 14.3. Concluding Remarks

15. CASE STUDY: ROBOTS IN PHARMACEUTICAL PACKAGING

- 15.1. Chapter Overview

- 15.2. Role of Robots in Pharmaceutical Industry

- 15.2.1. Key Considerations for Selecting a Robotic System

- 15.2.2. Advantages of Robotic Systems

- 15.2.3. Disadvantages of Robotic Systems

- 15.3. Companies Providing Robots for Use in the Pharmaceutical Industry

- 15.4. Companies Providing Equipment Integrated with Robotic Systems for Pharmaceutical Packaging

- 15.4.1. Aseptic Technologies

- 15.4.1.1. Crystal L1 Robot Line

- 15.4.1.2. Crystal SL1 Robot Line

- 15.4.2. AST

- 15.4.2.1. ASEPTiCell

- 15.4.2.2. GENiSYS R

- 15.4.2.3. GENiSYS C

- 15.4.2.4. GENiSYS Lab

- 15.4.3. Bosch Packaging Technology

- 15.4.3.1. ATO

- 15.4.4. Dara Pharmaceutical Packaging

- 15.4.4.1. SYX-E Cartridge + RABS

- 15.4.5. Fedegari

- 15.4.5.1. Fedegari Isolator

- 15.4.6. IMA

- 15.4.6.1. INJECTA

- 15.4.6.2. STERI LIF3

- 15.4.7. Steriline

- 15.4.7.1. Robotic Nest Filling Machine (RNFM)

- 15.4.7.2. Robotic Vial Filling Machine (RVFM)

- 15.4.7.3. Robotic Nest Capping Machine (RVCM)

- 15.4.8. Vanrx Pharmasystems

- 15.4.8.1. Microcell Vial Filler

- 15.4.8.2. SA25 Aseptic Filling Workcell

- 15.4.1. Aseptic Technologies

16. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 16.1. Chapter Overview

- 16.2. Market Drivers

- 16.3. Market Restraints

- 16.4. Market Opportunities

- 16.5. Market Challenges

- 16.6. Conclusion

17. GLOBAL READY TO USE PHARMACEUTICAL PACKAGING MARKET

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Global Pre-Sterilized / Ready-to-Use Primary Packaging Market, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 17.3.1. Scenario Analysis

- 17.3.1.1. Conservative Scenario

- 17.3.1.2. Optimistic Scenario

- 17.3.1. Scenario Analysis

- 17.4. Key Market Segmentation

18. READY TO USE PHARMACEUTICAL PACKAGING MARKET, BY TYPE OF PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING SYSTEM

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Type of Pre-Sterilized / Ready-to-use Primary Packaging System

- 18.2.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.2.1.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.2.1.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.2.1.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Type of Pre-Sterilized / Ready-to-use Primary Packaging System

- 18.3. Data Triangulation and Validation

19. READY TO USE PHARMACEUTICAL PACKAGING MARKET, BY TYPE OF FABRICATION MATERIAL USED FOR CONTAINERS

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Type of Fabrication Material Used for Containers

- 19.2.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Glass Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Glass Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.1.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Glass Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.1.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Glass Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Plastic Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Plastic Syringes, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.2.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Plastic Vials, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.2.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Plastic Cartridges, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Glass Containers, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Type of Fabrication Material Used for Containers

- 19.3. Data Triangulation and Validation

20. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Geographical Region

- 20.2.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.1.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.1.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.1.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.2.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.2.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.2.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.3.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.3.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures in Asia-Pacific, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.4.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.4.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.4.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.4.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.5. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.5.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Syringes in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.5.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Vials in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.5.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Cartridges in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.5.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Closures in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market for Primary Packaging Systems in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.2.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market: Distribution by Geographical Region

- 20.3. Data Triangulation and Validation

21. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET IN NORTH AMERICA**

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in North America, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 21.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market in the US, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 21.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Canada, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

22. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET IN EUROPE

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Europe, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Germany, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market in France, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in the UK, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Italy, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.5. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Spain, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 22.3.6. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Rest of Europe, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

23. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET IN ASIA-PACIFIC

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Asia-Pacific, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 23.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market in China, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 23.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Australia, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 23.3.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in India, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 23.3.4. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Japan, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 23.3.5. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Rest of Asia-Pacific, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

24. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET IN LATIN AMERICA

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Latin America, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 24.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Brazil, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 24.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Argentina, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

25. PRE-STERILIZED / READY-TO-USE PRIMARY PACKAGING MARKET IN MIDDLE EAST AND NORTH AFRICA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Middle East and North Africa, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 25.3.1. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Israel, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 25.3.2. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Saudi Arabia, Historical Trends (since 2022) and Forecasted Estimates (till 2035)

- 25.3.3. Pre-Sterilized / Ready-to-Use Primary Packaging Market in Iran, Historical Trends (since 2022) and Forecasted Estimates (till 2035)