|

시장보고서

상품코드

2055600

암 생물학적 제제 시장 : 업계 동향과 2035년까지 세계 예측 - 생물제제 유형별, 표적 적응증별, 지역별Cancer Biologics Market: Industry Trends and Global Forecasts Till 2035 - Distribution by Type of Biologic, Target Indication and Geography |

||||||

암 생물학적 제제 시장 : 개요

세계의 암 생물학적 제제 시장 규모는 2035년까지 연평균 복합 성장률(CAGR) 8.9%로 확대되어 현재 1,690억 달러에서 2035년에는 1,890억 달러에 이를 것으로 추정되고 있습니다.

암 생물학적 제제 시장

시장 규모 및 기회 분석은 다음 매개변수를 기준으로 세분화되어 있습니다.

생물학적 제제 유형

- 항체

- 세포 및 유전자 치료

- 종양 용해성 바이러스 요법

- mRNA 치료제 및 백신

- 뉴클레오티드계 약물

- 펩타이드

- 기타

적응증

- 혈액암

- 폐암

- 대장암

- 유방암

- 전립선암

- 피부암

- 신장암

- 자궁경부암 및 위암

- 간암

- 방광암

- 난소암

- 췌장암

- 두경부암

- 뇌암

- 기타 유형 암

지역

- 북미

- 미국

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타 유럽 국가들

- 아시아태평양

- 인도

- 일본

- 한국

- 중국

- 기타 지역

암 생물학적 제제 시장 : 성장 및 동향

세계암회의에 따르면, 암은 심혈관 질환과 감염증에 이어 전 세계에서 세 번째로 많은 사망 원인이 되고 있습니다. 현재 외과 수술, 방사선 치료, 약물 치료 등 다양한 치료법이 이용 가능합니다. 이러한 치료법 중에서도, 특히 조기에 진단된 암의 경우 수술이 주된 치료법이 되고 있습니다. 방사선 치료는 대부분의 경우 수술과 병행되며, 의료 전문가에 의해 국소적으로 시행됩니다. 수년에 걸쳐, 약물 기반 치료법(생물학적 제제 및 저분자 화합물을 모두 포함)의 개발은 다양한 유형의 암에서 현저한 진전을 보이고 있습니다.

단일클론 항체, 이중 특이성 항체, 세포 및 유전자 치료제 등의 생물학적 제제는 특정 생물학적 경로를 표적으로 삼아 그 작용을 조절하는 것을 목적으로 합니다. 생물학적 제제가 암 치료제 시장의 약 70%를 차지하고 있다는 점은 주목할 만합니다. 예를 들어, 머크(Merck)사가 개발한 ‘KEYTRUDA(R)’와 존슨앤드존슨(Johnson & Johnson)사가 개발한 ‘Darzalex(R)’는 암 치료제로 승인받았으며, 최근 매출액은 각각 300억 달러, 120억 달러로 보고되고 있습니다. 이는 이러한 항암제가 임상적 및 상업적으로 매우 중요한 위치를 차지하고 있음을 보여줍니다. 동시에, 저분자 의약품 역시 주로 세포 내로 침투하여 세포 내 신호 전달 경로에 영향을 미칠 수 있는 능력이 있기 때문에 암 치료에서 여전히 기초적인 역할을 수행하고 있습니다.

최근 암 생물학적 제제 시장에서는 차세대 염기서열 분석, CRISPR-Cas9을 이용한 유전자 편집, 단일 세포 분석, 이중 특이성 항체, 항체-약물 복합체(ADC), CAR-T 세포 치료, mRNA 치료/백신 등, 암 세포에 대한 정밀한 표적화 및 맞춤형 치료를 가능하게 하는 기술 분야에서 현저한 진전이 나타나고 있습니다. 이러한 발전과 암 발병률 증가, 그리고 표적 치료에 초점을 맞춘 고효율 맞춤형 치료에 대한 수요 증가가 맞물려 암 생물학적 제제 시장의 성장을 견인하고 있습니다.

성장 요인 - 시장 확대를 전략적으로 촉진하는 요인

세계 암 발병률 증가, 세포 치료 및 유전자 치료 파이프라인의 확대, 맞춤형 의료에 대한 관심 고조, 그리고 제약 기업의 면역 치료 및 병용 요법에 대한 연구개발 투자 증가 등 다양한 요인이 암 바이오의약품 시장의 성장을 견인하고 있습니다. 또한, 맞춤형 암 생물학적 제제 시장에 대한 관심이 높아짐에 따라 많은 제약사가 혁신적인 치료법 개발에 뛰어들고 있습니다. 이러한 치료법은 지속적인 치료 효과를 확보하는 동시에, 다양한 유형의 암에 대한 대체 치료의 선택지를 넓히는 것을 목적으로 합니다. 암 치료 분야의 이러한 급속한 발전에 힘입어, 제약 기업들은 변형 면역 세포, 종양 용해성 바이러스, 유전자 변형 기술에 대한 투자를 확대하고 있으며, 각 환자의 고유한 프로파일에 맞추어 맞춤형으로 설계된, 표적성이 높고 지속 가능한 치료 옵션을 제공합니다. 이러한 발전은 생명공학이 암 생물학적 제제 시장에 막대한 영향을 미치고 있음을 보여줍니다.

시장의 과제 - 진전을 가로막는 중대한 장벽

암 생물학적 제제 분야는 개발 및 제조 비용이 높다는 과제에 직면해 있으며, 이는 중소기업 시장 진입을 가로막고 혁신을 저해하고 있습니다. 세포주 최적화와 같은 복잡한 과정을 거치다 보니, 한 가지 약물당 수십억 달러가 넘는 경우도 드물지 않습니다. 규제상의 장벽으로 인해, 특히 ADC(항체-약물 복합체)와 같은 강력한 치료법의 경우 엄격한 임상시험과 안전성 평가가 요구되어 시장 출시가 수년 지연될 수밖에 없습니다. 수지 및 바이알 부족, 콜드체인 물류의 문제 등 공급망의 취약성은 지정학적 긴장을 배경으로 생산 지연을 더욱 악화시키고 있습니다. 게다가 특허 만료로 인해 바이오시밀러가 가격을 인하하고 오리지널 제품으로부터 시장 점유율을 빼앗으면서 경쟁이 치열해지고 있습니다. 면역원성, 수액 반응, 심각한 부작용과 같은 우려는 환자의 신뢰와 수용을 저해하고 있습니다. 게다가 연간 수만 달러에 달하는 고액의 치료비 또한 개발도상국 시장에서 치료 접근성을 제한하고 있습니다. 이러한 압박에 더해, 저분자 약물 및 화학요법과의 경쟁으로 인해 수요가 증가하고 있음에도 불구하고 지속적인 성장이 저해되고 있습니다.

암 생물학적 제제 시장 - 주요 인사이트

본 보고서는 암 생물학적 제제 시장의 현황을 상세하게 분석하고, 업계 내 잠재적인 성장 기회를 파악하고 있습니다. 보고서의 주요 조사 결과는 다음과 같습니다.

- 신약 도입에 따라 투여 부족이나 과다 투여를 방지하기 위해서는 ‘일률적인’ 방식에서 벗어나 환자 맞춤형 투여 전략으로 전환하는 것이 필수적입니다. 업계에서는 다양한 유형의 항체-약물 복합체(ADC)에 대한 승인이 진행되고 있습니다. 예를 들어, 전이성 요로상피암의 2차 치료제로는 PADVEC(R), CD22 양성 급성 림프구성 백혈병 치료제로는 BESPONSA(R), 미만성 대세포형 B세포 림프종의 3차 치료제로는 ZYNLONTA(R) 등이 있습니다.

- 희귀 림프종 환자의 경우, 완치를 목적으로 하는 기존의 치료법이라 하더라도 아직 완전한 치유에 이르지 못하고 있습니다. 특정 증례에서 재발성 및 난치성 환자의 생존 기간 중앙값은 6개월에서 10개월 사이로 제한되어 있습니다. 그 결과, 현재의 임상시험에서는 실제 임상 현장의 경험을 보다 정확하게 반영하기 위해 환자 보고 결과(PRO)의 중요성이 점점 더 커지고 있습니다. 자기 보고 정보를 연구 설계에 반영함으로써, 임상의는 이 희귀 환자 집단에 대해 개별적으로 최적화된 치료 전략을 수립하는 데 이를 활용할 수 있습니다.

- 요로상피암(이행상피암이라고도 함)은 전 세계 방광암 사례의 80-90%를 차지하며, 근육층 침윤 여부에 따라 더 세분화됩니다.

- 다양한 유형의 치료법이 널리 이용 가능함에도 불구하고, 방광암 분야에서는 내약성이 더 우수하고 무진행 생존 기간(PFS)을 개선하는 약물이 요구되고 있습니다.

- 암 생물학적 제제 시장의 주요 촉진요인과 장벽을 평가하는 것은 이해관계자들에게 귀중한 인사이트를 제공하며, 변화하는 요구에 대응하기 위해 제품 포트폴리오를 강화할 수 있게 해줍니다.

- 현재 암 생물학적 제제 시장은 북미에 집중되어 있지만, 향후 몇 년 동안 아시아태평양 시장이 더 높은 성장률을 보일 것으로 예측됩니다.

- 북미의 암 생물학적 제제 시장은 올해 최대 시장 점유율을 차지할 것으로 예측됩니다. 또한, 적응증별로는 유방암이 예측 기간 동안 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.

- 종양성 질환의 유병률 증가와 표적 치료제 개발에 대한 집중적인 노력에 힘입어, 미국의 암 생물학적 제제 시장은 예측 기간 동안 연평균 성장률(CAGR) 9.1%를 나타낼 것으로 예측됩니다.

암 생물학적 제제 시장 : 주요 부문

mRNA 치료와 백신이 암 치료의 미래가 될 것입니다.

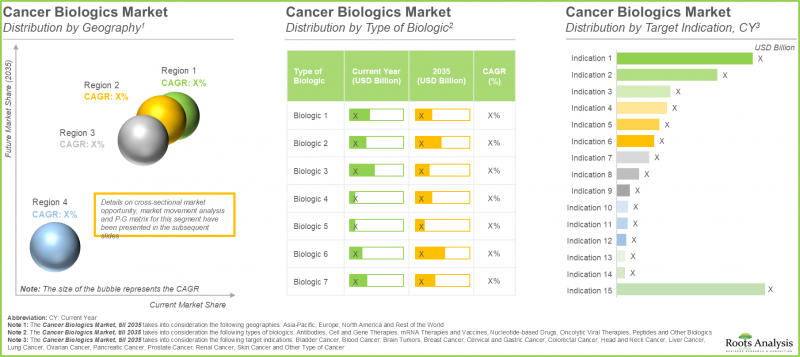

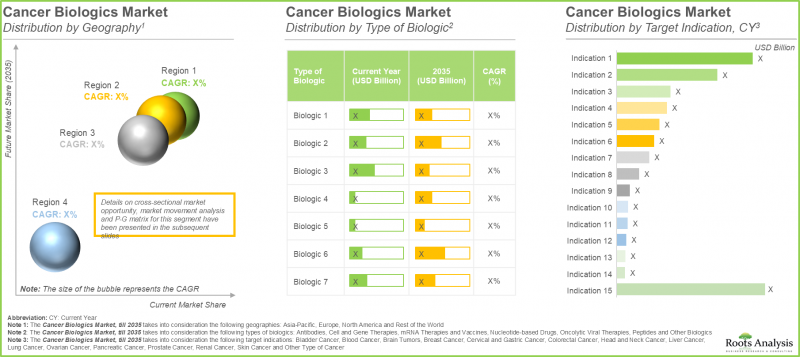

생물학적 제제 유형별로는 시장 세분화에서 항체, 세포 및 유전자 치료, 종양용해성 바이러스 요법, mRNA 치료 및 백신, 뉴클레오티드계 약물, 펩타이드, 기타 생물학적 제제로 분류됩니다. 2035년에는 항체 부문이 전체 시장의 70%를 차지할 것으로 예측됩니다. 이러한 증가는 항체가 높은 특이성을 지니고 있어, 건강한 세포에 대한 손상을 최소화하면서 암세포를 정확하게 표적화할 수 있는 능력에서 기인합니다. mRNA 치료제 및 백신 부문이 더 높은 연평균 성장률(CAGR)을 보일 것으로 예측된다는 점을 강조해 두는 것이 중요합니다. 특히, 각 제약사는 임상시험에서 유망한 결과를 보이고 있는 mRNA 치료제 및 백신(BNT113, mRNA-4157, GRT-C901/GRT-R902 등)이 가까운 시일 내에 블록버스터급 제품이 되어 업계의 대폭적인 성장을 이끌 것으로 전망하고 있습니다.

혈액 질환이 암 생물학적 제제 시장을 주도하고 있습니다.

표적 적응증별로 보면, 시장 세분화에서는 혈액암, 폐암, 대장암, 유방암, 전립선암, 피부암, 신장암, 자궁경부암 및 위암, 간암, 방광암, 난소암, 췌장암, 두경부암, 뇌종양, 기타 암으로 분류됩니다. 암 바이오의약품 시장 전망에 따르면, 혈액암 부문은 총 매출의 약 20%를 차지하고 있습니다. 이러한 압도적인 시장 점유율은 혈액암에 대한 다양한 표적 치료로 인해 생존율이 향상된 결과로 보입니다. 향후 몇 년간, 예측 기간 동안 유방암 분야가 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다. 특히, 미국에서 여성 암 환자의 30%를 유방암이 차지하고 있어, 제약사들은 부작용을 최소화하는 유방암 임상 연구 및 의약품 개발을 추진하고 있습니다.

북미가 큰 수익을 창출하고 있습니다.

지역별로 보면, 시장 세분화 측면에서 시장 전체는 북미, 유럽, 아시아태평양으로 분류됩니다. 당사의 세계 암 생물학적 제제 시장 분석에 따르면, 북미가 총 매출의 45%를 차지하며 시장을 주도하고 있습니다. 이러한 우위는 높은 암 발병률, 지속적인 기술 발전, 그리고 암 생물학적 제제의 발전을 뒷받침하는 유리한 규제 체계에 기인한 것으로 보입니다. 특히 주목할 점은 북미 중에서도 미국이 암 생물학적 제제 분야를 주도하고 있다는 점입니다. 이는 선진적인 의료 시스템, 만성 질환에 대한 철저한 조사, 그리고 맞춤형 암 치료에 대한 수요 증가에 힘입은 것입니다.

1차 조사 개요

본 시장 보고서에서 제시된 견해와 인사이트은 업계 주요 이해관계자들과의 논의에서도 영향을 받았습니다. 본 시장 보고서에는 다음 제3자들과의 논의 내용도 포함되어 있습니다.

- 미국 공립 연구 대학 원장

- 미국 병원 임상부장

- 미국 대기업 부사장

- 스웨덴 공립 연구 대학 교수

- 영국 공립 연구 대학 교수

암 생물학적 제제 시장의 주요 기업 사례

- Abbott

- AbbVie

- Amgen

- AstraZeneca

- BioNTech

- Bristol Myers Squibb

- Eli Lilly and Company

- Gilead Sciences

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Roche

- Sanofi

- Takeda Pharmaceuticals

암 생물학적 제제 시장 : 조사 범위

- 시장 규모 및 기회 분석 : 본 보고서에서는 암 생물학적 제제 시장에 대해(A) 생물학적 제제 유형,(B) 대상 적응증,(C) 지역과 같은 주요 시장 부문에 초점을 맞추어 상세하게 분석했습니다.

- 기업 프로파일:(A) 설립 연도,(B) 본사 소재지,(C) 암 생물학적 제제 포트폴리오,(D) 최근 동향 및(E) 정보에 기반한 미래 전망을 바탕으로, 암 생물학적 제제 개발에 종사하는 북미, 유럽, 아시아태평양의 주요 기업에 대한 상세한 프로파일을 제공합니다.

- 미충족 의료 수요와 치료 지침: 이 모듈에서는 광범위한 적응증에 걸친 치료 지침을 소개하고, 현재의 치료 요법에 대한 종합적인 개요를 제공합니다. 이 지침은 근거에 기반한 치료 권고 사항을 종합하여 안전한 임상 진료를 보장함과 동시에, 특정 적응증에 대한 치료의 미충족 요구를 평가하는 것입니다.

- 시장 영향 분석 : 암 생물학적 제제 산업의 성장에 영향을 미칠 수 있는 요인에 대한 상세한 분석입니다. 또한(A)주요 촉진요인,(B)잠재적 제약 요인,(C)새로운 기회, 그리고(D)기존 과제의 파악 및 분석도 포함되어 있습니다.

목차

제1장 배경

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 주요 요약

제6장 서론

제7장 기업 개요

제8장 미충족 요구와 치료 가이드라인

제9장 시장 영향 분석

제10장 세계의 암 생물학적 제제 시장

제11장 암 생물학적 제제 시장(생물제제 유형별)

제12장 암 생물학적 제제 시장(표적 적응증별)

제13장 암 생물학적 제제 시장(지역별)

제14장 시장 예측 기회 분석 : 북미

제15장 시장 예측 기회 분석 : 유럽

제16장 시장 예측 기회 분석 : 아시아태평양

제17장 시장 예측 기회 분석 : 기타 지역

제18장 결론

제19장 부록 I : 표 형식 데이터

제20장 부록 II : 기업 리스트

LSH 26.06.19Cancer Biologics Market: Overview

As per Roots Analysis, the global cancer biologics market is estimated to grow from USD 169 billion in the current year to USD 189 billion by 2035, at a CAGR of 8.9% during the forecast period, till 2035.

Cancer Biologics Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Type of Biologic

- Antibodies

- Cell and Gene Therapies

- Oncolytic Viral Therapies

- mRNA Therapies and Vaccines

- Nucleotide-based Drugs

- Peptides

- Other Biologics

Target Indication

- Blood Cancer

- Lung Cancer

- Colorectal Cancer

- Breast Cancer

- Prostate Cancer

- Skin Cancer

- Renal Cancer

- Cervical and Gastric Cancer

- Liver Cancer

- Bladder Cancer

- Ovarian Cancer

- Pancreatic Cancer

- Head and Neck Cancer

- Brain Cancer

- Other Type of Cancer

Geography

- North America

- US

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- India

- Japan

- South Korea

- China

- Rest of the World

Cancer Biologics Market: Growth and Trends

According to the World Cancer Congress, cancer ranks as the third most common cause of death worldwide, following cardiovascular diseases and infections. Presently, there are numerous treatment options available, including surgical procedures, radiotherapy, and drug therapies. Among these approaches, surgery is the primary method of treatment, especially for cancers diagnosed at an early stage. Radiotherapy is often used in conjunction with surgery and is administered in a localized manner by medical professionals. Over the years, the development of drug-based treatments (including both biologics and small molecules) has seen significant growth for various cancer types.

Biologic therapies, such as monoclonal antibodies, bispecific antibodies, and cell and gene therapies, aim to target and modify specific biological pathways. It is worth noting that biologics represent nearly 70% of the market for cancer therapeutics. For instance, KEYTRUDA(R) (developed by Merck) and Darzalex(R) (developed by Johnson & Johnson) have received approvals for treating oncological disorders, with reported sales of USD 30 billion and USD 12 billion, respectively, in recent years. This highlights the considerable clinical and commercial significance of these cancer treatments. Simultaneously, small molecule drugs continue to be fundamental in cancer treatment, primarily due to their capability to penetrate cells and influence intracellular signaling pathways.

The cancer biologics market has seen significant advancements in recent years, including next-generation sequencing, CRISPR-Cas9 gene editing, single-cell analysis, bispecific antibodies, antibody-drug conjugates (ADCs), CAR-T cell therapies, and mRNA therapies / vaccines, which enable precise targeting of cancer cells and personalized treatments. Owing to these advancements and the rising incidence of cancer, coupled with the heightened demand for targeted and highly effective personalized treatments, is propelling the growth of the cancer biologics market.

Growth Drivers: Strategic Enablers of Market Expansion

Various drivers are propelling the growth of cancer biologics market including the rising global incidence of cancer, expanding pipelines for cell and gene therapies, growing focus on personalized medicine, and increased R&D investments by pharmaceutical companies in immunotherapy and combination therapies. Further, the heightened attention on the personalized cancer biologics therapy market has attracted numerous pharmaceutical firms to develop innovative treatments, designed to ensure lasting responses while broadening alternative treatments for various cancer types. These rapid advancements in cancer therapies has prompted pharmaceutical firms to invest in modified immune cells, oncolytic viruses, and gene-altered technologies, providing highly targeted, durable treatment options customized to each patient's unique profile. These advancements have demonstrated a considerable influence of biotechnology on the cancer biologics market.

Market Challenges: Critical Barriers Impeding Progress

The cancer biologics sector faces high development and production expenses that discourage smaller companies and hinder innovation, frequently surpassing billions per drug due to complex procedures such as cell line optimization. Regulatory obstacles necessitate stringent clinical trials and safety evaluations, especially for powerful treatments such as ADCs, postponing market introduction by several years. Supply chain weaknesses, such as shortages of resins, vials, and cold chain logistics, worsen production delays in the context of geopolitical tensions. Further, patent expirations allow biosimilars to reduce prices and gain market share from original products, increasing competition. Concerns like immunogenicity, infusion reactions, and serious side effects erode patient confidence and acceptance. Furthermore, expensive therapy expenses, often amounting to tens of thousands each year also restrict access in developing markets. These pressures, along with competition from small molecules and chemotherapy, hinder consistent growth even with increasing demand

Cancer Biologics Market: Key Insights

The report delves into the current state of the cancer biologics market and identifies potential growth opportunities within industry. Some key findings from the report include:

- With the introduction of new medications, it's essential to transition from a "one-size-fits-all" method to tailored dosing strategies to prevent under- or overdosing. The industry has seen the endorsement of antibody drug conjugates for different types; for example, PADVEC(R) for second-line treatment of metastatic urothelial carcinoma, BESPONSA(R) for CD22-positive acute lymphoblastic leukemia, and ZYNLONTA(R) for third-line therapy of diffuse large B-cell lymphoma.

- In individuals with uncommon lymphomas, existing treatments fail to achieve a complete cure, even though they are intended to be curative. In certain instances, the median survival for relapsed / refractory patients ranges from six to ten months. Consequently, current clinical trials are increasingly emphasizing patient-reported outcomes to more accurately reflect real-world experiences. Integrating self-reported information into trial design can assist clinicians in customizing treatment strategies for this uncommon group of patients.

- Urothelial cancer (also known as transitional cell carcinoma) accounts for 80-90% of the bladder cancer cases worldwide and is further segregated based on muscle invasiveness.

- Despite the wide availability of various types of therapies, the bladder cancer segment requires drugs that offer better tolerability and improve progression-free survival (PFS)

- Assessment of the key drivers and barriers in the cancer biologics market provides valuable insights to stakeholders, allowing them to enhance their offerings to adapt to the evolving needs.

- Presently, the cancer biologics market is more concentrated in North America; however, the market in Asia-Pacific is likely to witness higher growth rate in the coming years.

- The cancer biologics market in North America is expected to capture maximum share in the current year; further, in terms of target indication, breast cancer is likely to grow at a higher CAGR during the forecast period.

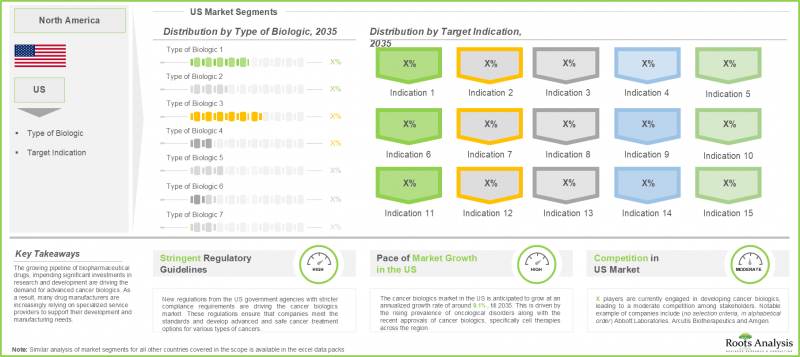

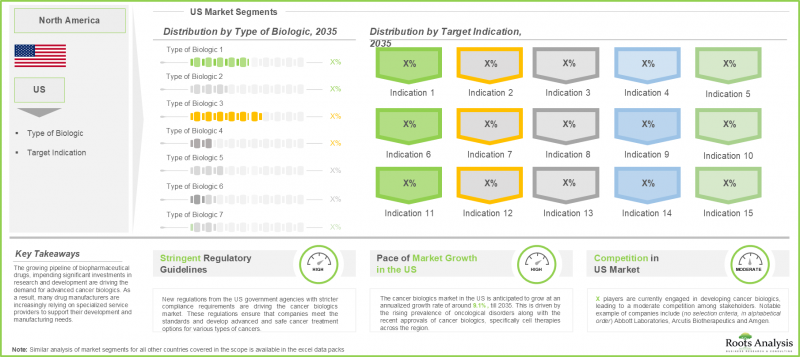

- Driven by the rising prevalence of oncological disorders and focus on targeted therapy development, the cancer biologics market in the US is expected to grow at CAGR of 9.1%, during the forecast period.

Cancer Biologics Market: Key Segments

mRNA Therapies and Vaccines to be the Future of Cancer Treatment

In terms of type of biologic, the market is segmented across antibodies, cell and gene therapies, oncolytic viral therapies, mRNA therapies and vaccines, nucleotide-based drugs, peptides and other biologics. In 2035, the antibodies segment is likely to account for 70% of the total market share. This increase arises from the ability of antibodies to possess high specificity, allowing them to accurately target cancer cells while reducing harm to healthy cells. It is crucial to emphasize that the segment for mRNA therapies and vaccines is expected to experience a greater CAGR. Significantly, the pharmaceutical companies anticipate that the mRNA treatments and vaccines (such as BNT113, mRNA-4157, and GRT-C901 / GRT-R902), which have demonstrated encouraging outcomes in clinical trials, will attain blockbuster status in the near future, signaling substantial industry expansion.

Blood Disorders Dominate the Cancer Biologics Industry

In terms of the target indication, the overall market is segmented across blood cancer, lung cancer, colorectal cancer, breast cancer, prostate cancer, skin cancer, renal cancer, Cervical and Gastric Cancer, liver cancer, bladder cancer, ovarian cancer, pancreatic cancer, head and neck cancer, brain cancer, other types of cancer. As per the forecast for the cancer biologics market, the blood cancer category contributes nearly 20% of total revenue. This largest market share is likely to be a result of improved survival rates attained through different targeted treatments for blood cancer. In the coming years, the breast cancer sector is expected to expand at the highest CAGR throughout the forecast duration. Significantly, breast cancer represents 30% of all cancer cases among women in the US, prompting pharmaceutical firms to push forward with breast oncology studies and drug development that minimize side effects.

North America Generates High Revenue

In terms of geography, the overall market is segmented across North America, Europe and Asia-Pacific. Our analysis of the global cancer biologics market shows that North America leads the market by capturing 45% of the total revenue share. This prevalence is probably due to elevated cancer rates, continuous technological progress, and advantageous regulatory frameworks that aid the advancement of cancer biologics. It is worth highlighting that within North America, The US leads the cancer biologics sector, propelled by advanced healthcare systems, robust research in chronic illnesses, and increasing demand for tailored cancer treatment.

Primary Research Overview

The opinions and insights presented in the market report were also influenced by discussions held with senior stakeholders in the industry. The market report includes transcripts of the following other third-party discussions:

- Director, Public Research University in the US

- Clinical Director, Hospital in the US

- Vice-President, Large Company in the US

- Professor, Public Research University in Sweden

- Professor, Public Research University in the UK

Example Players in Cancer Biologics Market

- Abbott

- AbbVie

- Amgen

- AstraZeneca

- BioNTech

- Bristol Myers Squibb

- Eli Lilly and Company

- Gilead Sciences

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Roche

- Sanofi

- Takeda Pharmaceuticals

Cancer Biologics Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the cancer biologics market, focusing on key market segments, including [A] type of biologic, [B] target indication, and [C] geography.

- Company Profiles: In-depth profiles of prominent players North America, Europe and Asia-Pacific that are engaged in the development of cancer biologics based on [A] year of establishment, [B] location of headquarters, [C] cancer biologics portfolio, [D] recent developments and [E] an informed future outlook.

- Unmet Needs and Treatment Guidelines: The module presents treatment guidelines across a range of indications, providing a comprehensive overview of current treatment regimen. The guidelines synthesize evidence-based recommendations for therapy, ensuring safe clinical care and assessing the unmet needs in the treatment of a particular indication.

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of cancer biologics industry. It also features identification and analysis of [A] key drivers, [B] potential restraints, [C] emerging opportunities, and [D]existing challenges.

Key Questions Answered in this Report

- Which region dominates the cancer biologics market?

- What are the key trends observed in the cancer biologics market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by cancer biologic developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. BACKGROUND

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Concluding Remarks

5. EXECUTIVE SUMMARY

- 5.1. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Overview of Cancer

- 6.2. Pillars of Cancer Therapy

- 6.3. Types of Cancer Treatments

- 6.4. Key Benefits of Cancer Biologics

- 6.5. Future Perspective

7. COMPANY PROFILES

- 7.1. Chapter Overview

- 7.2. Abbott

- 7.2.1. Company Overview

- 7.2.2. Financial Information

- 7.2.3. Cancer Biologics Portfolio

- 7.2.4. Recent Developments and Future Outlook

- 7.3. AbbVie

- 7.4. Amgen

- 7.5. AstraZeneca

- 7.6. BioNTech

- 7.7. Bristol Myers Squibb

- 7.8. Eli Lilly and Company

- 7.9. Gilead Sciences

- 7.10. GlaxoSmithKline

- 7.11. Johnson & Johnson

- 7.12. Merck

- 7.13. Novartis

- 7.14. Pfizer

- 7.15. Roche

- 7.16. Sanofi

- 7.17. Takeda Pharmaceuticals

8. UNMET NEEDS AND TREATMENT GUIDELINES

- 8.1. Bladder Cancer

- 8.1.1. Treatment Guidelines

- 8.1.2. Unmet Need in Bladder Cancer Treatment

- 8.2. Blood Cancer

- 8.3. Brain Cancer

- 8.4. Breast Cancer

- 8.5. Colorectal Cancer

- 8.6. Head and Neck Cancer

- 8.7. Liver Cancer

- 8.8. Lung Cancer

- 8.9. Prostate Cancer

9. MARKET IMPACT ANALYSIS

- 9.1. Market Drivers

- 9.2. Market Restraints

- 9.3. Market Opportunities

- 9.4. Market Challenges

10. GLOBAL CANCER BIOLOGICS MARKET

- 10.1. Key Assumptions

- 10.2. Forecast Methodology

- 10.3. Global Cancer Biologics Market, Till 2035

- 10.3.1. Multivariate Scenario Analysis

- 10.3.1.1. Conservative Scenario

- 10.3.1.2. Optimistic Scenario

- 10.3.1. Multivariate Scenario Analysis

- 10.5. Key Market Segmentations

11. CANCER BIOLOGICS MARKET, BY TYPE OF BIOLOGIC

- 11.1. Cancer Biologics Market: Distribution by Type of Biologic

- 11.1.1. Cancer Biologics Market for Antibodies, Forecasted Estimates (Till 2035)

- 11.1.2. Cancer Biologics Market for Cell and Gene Therapies, Forecasted Estimates (Till 2035)

- 11.1.3. Cancer Biologics Market for Oncolytic Viral Therapies, Forecasted Estimates (Till 2035)

- 11.1.4. Cancer Biologics Market for mRNA Therapies and Vaccines, Forecasted Estimates (Till 2035)

- 11.1.5. Cancer Biologics Market for Nucleotide-based Drugs, Forecasted Estimates (Till 2035)

- 11.1.6. Cancer Biologics Market for Peptides, Forecasted Estimates (Till 2035)

- 11.2. Data Triangulation and Validation

12. CANCER BIOLOGICS MARKET, BY TARGET INDICATION

- 12.1. Cancer Biologics Market: Distribution by Target Indication

- 12.1.1. Cancer Biologics Market for Blood Cancer, Forecasted Estimates (Till 2035)

- 12.1.2. Cancer Biologics Market for Lung Cancer, Forecasted Estimates (Till 2035)

- 12.1.3. Cancer Biologics Market for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 12.1.4. Cancer Biologics Market for Breast Cancer, Forecasted Estimates (Till 2035)

- 12.1.5. Cancer Biologics Market for Prostate Cancer, Forecasted Estimates (Till 2035)

- 12.1.6. Cancer Biologics Market for Skin Cancer, Forecasted Estimates (Till 2035)

- 12.1.7. Cancer Biologics Market for Renal Cancer, Forecasted Estimates (Till 2035)

- 12.1.8. Cancer Biologics Market for Cervical and Gastric Cancer, Forecasted Estimates (Till 2035)

- 12.1.9. Cancer Biologics Market for Liver Cancer, Forecasted Estimates (Till 2035)

- 12.1.10. Cancer Biologics Market for Bladder Cancer, Forecasted Estimates (Till 2035)

- 12.1.11. Cancer Biologics Market for Ovarian Cancer, Forecasted Estimates (Till 2035)

- 12.1.12. Cancer Biologics Market for Pancreatic Cancer, Forecasted Estimates (Till 2035)

- 12.1.13. Cancer Biologics Market for Head and Neck Cancer, Forecasted Estimates (Till 2035)

- 12.1.14. Cancer Biologics Market for Brain Cancer, Forecasted Estimates (Till 2035)

- 12.1.15. Cancer Biologics Market for Other Type of Cancer, Forecasted Estimates (Till 2035)

- 12.2. Data Triangulation and Validation

13. CANCER BIOLOGICS MARKET, BY GEOGRAPHY

- 13.1. Cancer Biologics Market: Distribution by Geography

- 13.1.1. Cancer Biologics Market in North America, Forecasted Estimates (Till 2035)

- 13.1.2. Cancer Biologics Market in the US, Forecasted Estimates (Till 2035)

- 13.1.2. Cancer Biologics Market in Europe, Forecasted Estimates (Till 2035)

- 13.1.2.1. Cancer Biologics Market in Germany, Forecasted Estimates (Till 2035)

- 13.1.2.2. Cancer Biologics Market in France, Forecasted Estimates (Till 2035)

- 13.1.2.3. Cancer Biologics Market in the UK, Forecasted Estimates (Till 2035)

- 13.1.2.4. Cancer Biologics Market in Spain, Forecasted Estimates (Till 2035)

- 13.1.2.5. Cancer Biologics Market in Rest of Europe, Forecasted Estimates (Till 2035)

- 13.1.3. Cancer Biologics Market in Asia-Pacific, Forecasted Estimates (Till 2035)

- 13.1.3.1. Cancer Biologics Market in India, Forecasted Estimates (Till 2035)

- 13.1.3.2. Cancer Biologics Market in Japan, Forecasted Estimates (Till 2035)

- 13.1.3.3. Cancer Biologics Market in South Korea, Forecasted Estimates (Till 2035)

- 13.1.3.4. Cancer Biologics Market in China, Forecasted Estimates (Till 2035)

- 13.1.4. Cancer Biologics Market in Rest of the World, Forecasted Estimates (Till 2035)

- 13.2. Data Triangulation and Validation

14. MARKET FORECAST OPPORTUNITY ANALYSIS: NORTH AMERICA

- 14.1. Cancer Biologics Market in North America: Distribution by Type of Biologic

- 14.1.1. Cancer Biologics Market in North America for Antibodies, Forecasted Estimates (Till 2035)

- 14.1.2. Cancer Biologics Market in North America for Cell and Gene Therapies Forecasted Estimates (Till 2035)

- 14.1.3. Cancer Biologics Market in North America for Oncolytic Viral Therapies, Forecasted Estimates (Till 2035)

- 14.1.4. Cancer Biologics Market in North America for mRNA Therapies and Vaccines, Forecasted Estimates (Till 2035)

- 14.1.5. Cancer Biologics Market in North America for Nucleotide-based Drugs, Forecasted Estimates (Till 2035)

- 14.1.6. Cancer Biologics Market in North America for Peptides, Forecasted Estimates (Till 2035)

- 14.2. Cancer Biologics Market in North America: Distribution by Target Indication

- 14.2.1. Cancer Biologics Market in North America for Blood Cancer, Forecasted Estimates (Till 2035)

- 14.2.2. Cancer Biologics Market in North America for Lung Cancer, Forecasted Estimates (Till 2035)

- 14.2.3. Cancer Biologics Market in North America for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 14.2.4. Cancer Biologics Market in North America for Breast Cancer, Forecasted Estimates (Till 2035)

- 14.2.5. Cancer Biologics Market in North America for Prostate Cancer, Forecasted Estimates (Till 2035)

- 14.2.6. Cancer Biologics Market in North America for Skin Cancer, Forecasted Estimates (Till 2035)

- 14.2.7. Cancer Biologics Market in North America for Renal Cancer, Forecasted Estimates (Till 2035)

- 14.2.8. Cancer Biologics Market in North America for Cervical and Gastric Cancer, Forecasted Estimates (Till 2035)

- 14.2.9. Cancer Biologics Market in North America for Liver Cancer, Forecasted Estimates (Till 2035)

- 14.2.10. Cancer Biologics Market in North America for Bladder Cancer, Forecasted Estimates (Till 2035)

- 14.2.11. Cancer Biologics Market in North America for Ovarian Cancer, Forecasted Estimates (Till 2035)

- 14.2.12. Cancer Biologics Market in North America for Pancreatic Cancer, Forecasted Estimates (Till 2035)

- 14.2.13. Cancer Biologics Market in North America for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 14.2.14. Cancer Biologics Market in North America for Brain Cancer, Forecasted Estimates (Till 2035)

- 14.2.15. Cancer Biologics Market in North America for Other Type of Cancer, Forecasted Estimates (Till 2035)

15. MARKET FORECAST OPPORTUNITY ANALYSIS: EUROPE

- 15.1. Cancer Biologics Market in Europe: Distribution by Type of Biologic

- 15.1.1. Cancer Biologics Market in Europe for Antibodies, Forecasted Estimates (Till 2035)

- 15.1.2. Cancer Biologics Market in Europe for Cell and Gene Therapies Forecasted Estimates (Till 2035)

- 15.1.3. Cancer Biologics Market in Europe for Oncolytic Viral Therapies, Forecasted Estimates (Till 2035)

- 15.1.4. Cancer Biologics Market in Europe for mRNA Therapies and Vaccines, Forecasted Estimates (Till 2035)

- 15.1.5. Cancer Biologics Market in Europe for Nucleotide-based Drugs, Forecasted Estimates (Till 2035)

- 15.1.6. Cancer Biologics Market in Europe for Peptides, Forecasted Estimates (Till 2035)

- 15.2. Cancer Biologics Market in Europe: Distribution by Target Indication

- 15.2.1. Cancer Biologics Market in Europe for Blood Cancer, Forecasted Estimates (Till 2035)

- 15.2.2. Cancer Biologics Market in Europe for Lung Cancer, Forecasted Estimates (Till 2035)

- 15.2.3. Cancer Biologics Market in Europe for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 15.2.4. Cancer Biologics Market in Europe for Breast Cancer, Forecasted Estimates (Till 2035)

- 15.2.5. Cancer Biologics Market in Europe for Prostate Cancer, Forecasted Estimates (Till 2035)

- 15.2.6. Cancer Biologics Market in Europe for Skin Cancer, Forecasted Estimates (Till 2035)

- 15.2.7. Cancer Biologics Market in Europe for Renal Cancer, Forecasted Estimates (Till 2035)

- 15.2.8. Cancer Biologics Market in Europe for Cervical and Gastric Cancer, Forecasted Estimates (Till 2035)

- 15.2.9. Cancer Biologics Market in Europe for Liver Cancer, Forecasted Estimates (Till 2035)

- 15.2.10. Cancer Biologics Market in Europe for Bladder Cancer, Forecasted Estimates (Till 2035)

- 15.2.11. Cancer Biologics Market in Europe for Ovarian Cancer, Forecasted Estimates (Till 2035)

- 15.2.12. Cancer Biologics Market in Europe for Pancreatic Cancer, Forecasted Estimates (Till 2035)

- 15.2.13. Cancer Biologics Market in Europe for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 15.2.14. Cancer Biologics Market in Europe for Brain Cancer, Forecasted Estimates (Till 2035)

- 15.2.15. Cancer Biologics Market in Europe for Other Type of Cancer, Forecasted Estimates (Till 2035)

16. MARKET FORECAST OPPORTUNITY ANALYSIS: ASIA-PACIFIC

- 16.1. Cancer Biologics Market in Asia-Pacific: Distribution by Type of Biologic

- 16.1.1. Cancer Biologics Market in Asia-Pacific for Antibodies, Forecasted Estimates (Till 2035)

- 16.1.2. Cancer Biologics Market in Asia-Pacific for Cell and Gene Therapies, Forecasted Estimates (Till 2035)

- 16.1.3. Cancer Biologics Market in Asia-Pacific for Oncolytic Viral Therapies, Forecasted Estimates (Till 2035)

- 16.1.4. Cancer Biologics Market in Asia-Pacific for mRNA Therapies and Vaccines, Forecasted Estimates (Till 2035)

- 16.1.5. Cancer Biologics Market in Asia-Pacific for Nucleotide-based Drugs, Forecasted Estimates (Till 2035)

- 16.1.6. Cancer Biologics Market in Asia-Pacific for Peptides, Forecasted Estimates (Till 2035)

- 16.2. Cancer Biologics Market in Asia-Pacific: Distribution by Target Indication

- 16.2.1. Cancer Biologics Market in Asia-Pacific for Blood Cancer, Forecasted Estimates (Till 2035)

- 16.2.2. Cancer Biologics Market in Asia-Pacific for Lung Cancer, Forecasted Estimates (Till 2035)

- 16.2.3. Cancer Biologics Market in Asia-Pacific for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 16.2.4. Cancer Biologics Market in Asia-Pacific for Breast Cancer, Forecasted Estimates (Till 2035)

- 16.2.5. Cancer Biologics Market in Asia-Pacific for Prostate Cancer, Forecasted Estimates (Till 2035)

- 16.2.6. Cancer Biologics Market in Asia-Pacific for Skin Cancer, Forecasted Estimates (Till 2035)

- 16.2.7. Cancer Biologics Market in Asia-Pacific for Renal Cancer, Forecasted Estimates (Till 2035)

- 16.2.8. Cancer Biologics Market in Asia-Pacific for Cervical and Gastric Cancer, Forecasted Estimates (Till 2035)

- 16.2.9. Cancer Biologics Market in Asia-Pacific for Liver Cancer, Forecasted Estimates (Till 2035)

- 16.2.10. Cancer Biologics Market in Asia-Pacific for Bladder Cancer, Forecasted Estimates (Till 2035)

- 16.2.11. Cancer Biologics Market in Asia-Pacific for Ovarian Cancer, Forecasted Estimates (Till 2035)

- 16.2.12. Cancer Biologics Market in Asia-Pacific for Pancreatic Cancer, Forecasted Estimates (Till 2035)

- 16.2.13. Cancer Biologics Market in Asia-Pacific for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 16.2.14. Cancer Biologics Market in Asia-Pacific for Brain Cancer, Forecasted Estimates (Till 2035)

- 16.2.15. Cancer Biologics Market in Asia-Pacific for Other Type of Cancer, Forecasted Estimates (Till 2035)

17. MARKET FORECAST OPPORTUNITY ANALYSIS: REST OF THE WORLD

- 17.1. Cancer Biologics Market in Rest of the World: Distribution by Type of Biologic

- 17.1.1. Cancer Biologics Market in Rest of the World for Antibodies, Forecasted Estimates (Till 2035)

- 17.1.2. Cancer Biologics Market in Rest of the World for Cell and Gene Therapies Forecasted Estimates (Till 2035)

- 17.1.3. Cancer Biologics Market in Rest of the World for Oncolytic Viral Therapies, Forecasted Estimates (Till 2035)

- 17.1.4. Cancer Biologics Market in Rest of the World for mRNA Therapies and Vaccines, Forecasted Estimates (Till 2035)

- 17.1.5. Cancer Biologics Market in Rest of the World for Nucleotide-based Drugs, Forecasted Estimates (Till 2035)

- 17.1.6. Cancer Biologics Market in Rest of the World for Peptides, Forecasted Estimates (Till 2035)

- 17.2. Cancer Biologics Market in Rest of the World: Distribution by Target Indication

- 17.2.1. Cancer Biologics Market in Rest of the World for Blood Cancer, Forecasted Estimates (Till 2035)

- 17.2.2. Cancer Biologics Market in Rest of the World for Lung Cancer, Forecasted Estimates (Till 2035)

- 17.2.3. Cancer Biologics Market in Rest of the World for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 17.2.4. Cancer Biologics Market in Rest of the World for Breast Cancer, Forecasted Estimates (Till 2035)

- 17.2.5. Cancer Biologics Market in Rest of the World for Prostate Cancer, Forecasted Estimates (Till 2035)

- 17.2.6. Cancer Biologics Market in Rest of the World for Skin Cancer, Forecasted Estimates (Till 2035)

- 17.2.7. Cancer Biologics Market in Rest of the World for Renal Cancer, Forecasted Estimates (Till 2035)

- 17.2.8. Cancer Biologics Market in Rest of the World for Cervical and Gastric Cancer, Forecasted Estimates (Till 2035)

- 17.2.9. Cancer Biologics Market in Rest of the World for Liver Cancer, Forecasted Estimates (Till 2035)

- 17.2.10. Cancer Biologics Market in Rest of the World for Bladder Cancer, Forecasted Estimates (Till 2035)

- 17.2.11. Cancer Biologics Market in Rest of the World for Ovarian Cancer, Forecasted Estimates (Till 2035)

- 17.2.12. Cancer Biologics Market in Rest of the World for Pancreatic Cancer, Forecasted Estimates (Till 2035)

- 17.2.13. Cancer Biologics Market in Rest of the World for Colorectal Cancer, Forecasted Estimates (Till 2035)

- 17.2.14. Cancer Biologics Market in Rest of the World for Brain Cancer, Forecasted Estimates (Till 2035)

- 17.2.15. Cancer Biologics Market in Rest of the World for Other Type of Cancer, Forecasted Estimates (Till 2035)