|

시장보고서

상품코드

1950748

LED 조명 시장 : 데이터베이스 및 주요 기업 전략(2026년 동향)2026 Global LED Lighting Market Trend- Database and Player Strategies |

||||||

최신 TrendForce 보고서 '세계의 LED 조명 시장(2026년 동향) : 데이터베이스 및 주요 기업의 전략(2026년 상반기)'에 따르면, 세계 LED 조명 시장은 거시 경제의 변동과 수요 조정을 거쳐 2026년 수축에서 안정화로 이행하는 중요한 전환기를 맞이할 전망입니다. 유통 채널의 재고가 건전한 수준으로 되돌아가고 있기 때문에 연간 감소폭은 대폭 축소되고, 수요 전체는 서서히 기본적인 교환 수요 주도의 성장 궤도로 회귀할 것으로 예측됩니다. 더욱 중요한 점에서 경쟁 구도는 구조적 변화를 겪고 있으며 가격 경쟁에서 용도 주도의 가치 창출 및 시스템 통합 능력으로 전환하고 있습니다.

2026년 세계의 LED 조명 시장에 대한 5가지 전략적 고려사항은 다음과 같습니다.

1. 일반 조명 시장 : 산업용 및 실외 부문이 주요 촉진요인

2026년에도 일반 조명 시장은 조정 단계에 있지만 특정 하위 부문에서는 견조한 성장 가능성이 나타났습니다.

산업용 조명은 방위, 항공우주, 원자력, 액화천연가스(LNG), 전략적 자원 분야에 대한 투자에 힘입어 2026년에는 핵심적인 성장 엔진이 될 전망입니다. 동시에 AI 데이터센터의 건설 가속화로 액체 냉각 시스템과 서버 랙용으로 설계된 인프라 조명에 대한 수요가 증가하고 있습니다. 옥외 부문에서는 노후화된 인프라 업데이트 및 터널 조명 기준의 업그레이드가 수리 수요를 지속적으로 견인하고 있습니다. 또한 스포츠, 엔터테인먼트 시설을 위한 조명, 스마트 및 에너지 절약 솔루션이 시장에 큰 성장을 가져왔습니다.

지역별로는 유럽이 여전히 시장을 선도하고 북미, 아시아태평양이 계속되고 있습니다. 유럽의 LED 조명 시장은 2025-2030년까지 연평균 복합 성장률(CAGR) 2.3%로 확대될 것으로 예측됩니다. 이 성장은 주로 급등하는 에너지 비용을 억제하기 위해 에너지 절약 조명 개조 솔루션의 도입 가속을 지원합니다. 아시아태평양 시장은 성장세를 유지하고 있으며, 특히 동남아시아 시장에서는 같은 예측 기간을 통해 3.6%의 연평균 복합 성장률(CAGR)이 예상됩니다.

2. 스마트 조명 시장 : 기술 사양 경쟁에서 시나리오 기반 및 인간 중심의 가치로 전환

TrendForce의 분석에 따르면 2025년 세계 조명 산업은 '이모셔널 라이팅'과 '인간 중심 조명(HCL)'을 핵심으로 하는 새로운 단계로 이행했습니다. 경쟁의 초점은 발광 효율 및 통신 프로토콜과 같은 전통적인 성능 지표에서 일일 리듬 조절 및 체험형 시나리오에 중점을 둔 가치 제안으로 전환하고 있습니다.

AI 기반 디밍, 풀 스펙트럼 제어 및 소프트웨어 정의 조명(SDL)을 통해 조명 제품은 정적 하드웨어 장치에서 지각 및 적응 학습이 가능한 지능형 시스템 노드로 진화하고 있습니다. TrendForce의 데이터에 따르면 스마트 조명 시장은 2030년까지 217억 8,500만 달러에 이를 것으로 예측되며, 2025-2030년 CAGR은 13.6%로 성장이 전망됩니다. 성장의 대부분은 주택 조명, 야외 조명, 산업 조명의 세 가지 주요 용도 시나리오에서 AI 활용과 시스템 업그레이드로 인한 가치 향상으로 인한 것입니다.

인공지능, SDL 및 IoT 기술의 융합으로 조명은 기본 조명 장비에서 스마트 생활 환경, 도시 거버넌스 시스템 및 산업 디지털화 프레임워크에서 중요한 감지 상호 작용 노드로 전환하고 있습니다. 소프트웨어 및 하드웨어의 통합 능력, 생태계 연계, 시나리오 인식 인사이트를 갖춘 공급업체는 향후 스마트 조명 시장에서 경쟁 우위를 얻는 좋은 위치에 설 것입니다.

3. 농업용 조명 : 지역별 차별화가 심화, 유럽에서는 성장 여지 있음

특수 작물의 갱신 사이클은 예상대로 진행되지 않았으며, 예산 제약으로 최종 제품 가격에 하락 압력이 계속되고 있습니다. 한편, 2025년에는 세계적으로 신규 온실 및 수직 농장 건설 프로젝트가 연기되었습니다.

그러나 유럽은 에너지 효율 규제 및 고광합성 광자 효율(PPF/W, PPE) 솔루션의 도입으로 비교적 견조를 유지하고 있으며, 북미 및 기타 지역의 약점을 효과적으로 상쇄하고 있습니다. 2025년 세계 LED 원예 조명 시장은 13억 6,500만 달러(전년 대비 4%)에 달했습니다.

2026년을 감안할 때, 특히 온실 용도 분야에 초점을 맞추면 유럽에서 고압 나트륨 램프(HPS) 시스템으로부터 LED로의 가속 교체가 수요를 계속 견인합니다. 한편, 북미, 아시아, 중동에서는 식량 안보 정책 및 수출 지향형 농업 투자를 배경으로 새로운 확대 사이클에 들어갑니다. 높은 PPE, 스펙트럼 조정 가능, 지능형 LED 조명 시스템에 대한 수요 증가가 예상됩니다. TrendForce는 2030년까지 시장 규모가 10억 4,100만 달러에 이르렀으며, 2025-2030년 연평균 성장률(CAGR)은 4%로 예측했습니다.

LED 패키징 분야에서는 2026년 멀티 채널 분광 기술의 채용이 가속될 것으로 전망됩니다. 신규 등록 제품의 대부분은 동적 디밍 기능과 고정밀 제어 요구 사항을 갖추고 있으며, 고품질 솔루션 수요 증가 및 LED 출하량 증가를 견인합니다. 과거 재고 조정 및 산업 재편을 통해 농업용 조명 LED의 평균 판매 가격은 2026년 안정화될 것으로 예측됩니다.

4. 제조업체 수익 : 스마트 조명 및 부문별 용도 시장 점유율 확대

TrendForce의 최신 통계에 따르면 전 세계 주요 조명 제조업체 20개 회사의 총 매출은 2025년 전년 대비 2% 감소한 233억 5,500만 달러로 예측됩니다. 상위 5개사는 변함없이 Signify, Acuity Brands, Panasonic, LEDVANCE, Zumtobel이 이름을 잇습니다.

특정 부문에서 전문가용 부문 조명은 규모의 경제성에서 우위를 나타냅니다. 한편, Signify나 LEDVANCE 등 세계의 일반 조명 리더 기업은 부동산 시장의 침체와 기존 주택 및 상업용 일반 조명 시장에 있어서 가격 경쟁의 영향으로 2025년에 수익이 축소되었습니다. 이에 비해 하이테크 니치 분야에 특화된 기업은 견조한 실적을 유지하고 있습니다.

방폭 및 산업 조명을 전문으로 하는 왈롬사는 세계 에너지 채굴 활동 회복과 산업 안전 수요 증가로 2025년 5.8%의 수익 성장이 전망되고 있습니다. 마찬가지로 선박 및 해양 에너지 조명을 전문으로 하는 그라목스·그룹은 EU의 해양 탄소 배출 정책의 영향으로 선박 조명의 업그레이드 수요에 견인되어 3.2%의 안정된 성장률을 유지할 것으로 예측되고 있습니다.

TrendForce는 일반 조명 시장에서 규모의 경제적 효과가 감소하는 동안 하이테크 틈새 분야가 제조업체의 수익성과 성장을 유지하는 열쇠가 될 것이라고 생각합니다.

5. LED 포장 시장 : 가격 경쟁에서 안정화 및 품질 향상

TrendForce의 분석에 따르면 2025년 조명용 LED 시장은 유럽과 미국의 국제 브랜드에 의한 적극적인 비용 최적화 전략과 고비용 성능 솔루션의 집중적인 채택으로 가격 하락 격화와 판매 오더 전망이 낮습니다.

장기간의 이익률 압축을 거쳐 LED 패키징 시장은 2026년 하강 사이클에서 벗어날 것으로 예측됩니다. 업스트림 재료 비용이 증가함에 따라 LED 패키징 가격은 안정화될 가능성이 높아 지속적인 가격 하락에서 수량 감소와 가격 안정화가 공존하는 환경으로의 전환을 나타낼 것입니다.

지속가능성 정책, 탄소 삭감 목표, 강화된 그린 빌딩 기준을 뒷받침하고, 산업 구조는 질적 변화를 이루고 있습니다. LED 조명 업계는 2026년 경기 순환 밑바닥을 완료하고 2027년 회복을 시작할 것으로 전망됩니다. TrendForce는 신중하면서도 낙관적인 전망을 유지하고 있으며, 전 세계 조명용 LED 시장 규모는 2030년까지 37억 3,400만 달러에 달했으며, 2025-2030년 연평균 성장률(CAGR)은 2.5%로 예측했습니다.

TrendForce는 일반 조명, 스마트 조명 및 원예 조명의 각 부문에 대한 시장 규모, 가격 동향, 지역별 분포 외에도 LED 패키징 분야의 동향 분석을 통해 세계 LED 조명 산업 동향에 대한 깊은 인사이트를 제공합니다. 본 보고서는 상위 20개 업체의 수익과 전략을 추적하고 Signify, Acuity, Panasonic, LEDVANCE 및 Opple 등 주요 기업의 경쟁적 포지셔닝을 검증함과 동시에 월별 부문별 시장 분석에 근거하여 7개의 주요 조명 기구 카테고리에서의 동향과 가격 동향을 개설하고 있습니다.

목차

파트 1 서문

- 시장 조사 방법

- 세계 경제(GDP)

- 환율

파트 2 일반 조명 시장 예측(2026-2030년)

- 일반 LED 조명 시장 규모 : 수요, 시장 가치, 수량 및 평균 판매 가격-제품별

- 일반 LED 조명 시장 규모 : 수요, 시장 가치, 카테고리별, 램프 및 조명기구

- 일반 LED 조명 시장 규모 : 수요, 시장 가치, 지역별

- 일반 LED 조명 시장 규모 : 수요, 시장 가치, 수량-제품별, 지역별

- 일반 LED 조명 시장 규모 : 수요, 시장 가치, 용도별

- 일반 LED 조명 보급률(설치량 기준)

- 일반 조명용 LED 시장 : 가치, 수량- 용도별

- 일반 조명용 LED 시장 : 가치, 수량, 평균 판매 가격-전력별

- 일반 조명용 LED 시장 : 가치, 수량, 평균 판매 가격-패키지 유형별

- 일반 조명용 LED 시장 : 가치-CCT

- 일반 조명용 LED 시장 : 가치 및 수량-CRI

- 일반 조명용 LED 가격

파트 3 스마트 조명 시장 예측(2026-2030년)

- 스마트 LED 조명 시장 규모, 수요, 시장 가치 및 용도별

- 스마트 LED 조명 시장 규모, 수요, 시장 가치 및 지역별

파트 4 농업용 조명 시장 예측(2026-2030년)

- 원예용 LED 조명 시장 규모, 수요, 시장 가치 및 용도별

- 원예용 LED 조명 시장 규모, 수요, 시장 가치 및 지역별

- 농업용 조명 LED 시장 : 칩 유형별 가치 및 수량

- 농업용 조명 LED 시장 : 전력별 가치 및 수량

- 농업용 조명 LED 가격

- 원예 조명 LED 참가 기업의 수익 랭킹 예측(2023-2025년)

파트 5 조명 산업의 수익 순위 및 추정

- 조명기기 제조업체 상위 20사 수익 예측(2023-2025년)

- 조명기기 제조업체 수익 랭킹 주요 10개사, 응용별 예측(2023-2025년)

- 조명 LED 참가 기업의 수익 예측(2023-2025년)

6부 LED 조명 제품 사양 및 가격

- 제품 및 가격 : 필라멘트 램프-지역별

- 제품 및 가격 : 가로등-지역별

- 제품 및 가격 : 패널 라이트-지역별

- 제품 및 가격 : 트로퍼-지역별

- 제품 및 가격 : 고/저베이-지역별

- 제품 및 가격 : 방폭 라이트-지역별

- 제품 및 가격 : 원예용 조명-용도별

(PDF) 1. 세계의 LED 조명 시장 동향 : 진출 기업 전략(2025년)

제1장 세계의 스마트 LED 조명 시장 동향

- 세계의 스마트 LED 조명 시장 규모 분석(2026-2030년)

- 세계의 스마트 LED 조명 시장 규모 분석 : 주택(2026-2030년)

- 스마트 주택 조명 제품(2025-2026년)

- 세계의 스마트 LED 조명 시장 규모 분석 : 옥외(2026-2030년)

- 세계의 스마트 LED 조명 시장 규모 분석 : 산업용(2026-2030년)

- 세계의 스마트 LED 조명 시장 규모 분석 : 지역별(2026-2030년)

- 스마트 조명 제어 프로토콜-Bluetooth

- 스마트 조명 제어 프로토콜-Zhaga

제2장 조명 업계의 수익 및 시장 전략 분석

- 조명 제조업체 수익 랭킹 상위 20사 : 토탈라이팅(2023-2025년)

- 조명 제조업체 수익 랭킹 상위 20사 : LED 조명(2023-2025년)

- 조명 산업의 수익 및 제품 전략

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- 중국 조명 제조업체의 수익 및 제품 전략

- LEDVANCE/MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF) 2. LED 조명 시장 월별 보고서 : 부문별 용도 및 제품 분석

- 서문

- 트렌드포스의 시점

- 시장 개요 및 특징 분석

- 제품 유형 및 용도 시나리오 분석

- 주류 제품 사양 및 LED 요건 분석

- 제조업체의 동향 및 경쟁 구도 분석

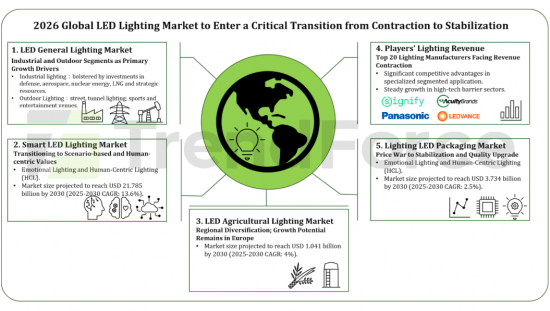

According to the latest TrendForce report, 2026 Global LED Lighting Market Trend- Database and Player Strategies (1H26), the global LED lighting market, after undergoing macroeconomic volatility and demand corrections, is expected to enter a critical transition phase in 2026, shifting from contraction to stabilization. As channel inventories return to healthier levels, the annual decline is projected to narrow significantly, with overall demand gradually reverting to fundamental replacement-driven growth. More importantly, the competitive landscape is undergoing a structural transformation - from price-based competition toward application-driven value creation and system integration capabilities.

Below are 5 strategic observations for the global LED lighting market in 2026:

1. General Lighting Market: Industrial and Outdoor Segments as Primary Growth Drivers

Although general lighting remains in an adjustment phase in 2026, selected subsegments demonstrate resilient growth potential.

Industrial lighting is set to become the core growth engine in 2026, bolstered by investments in defense, aerospace, nuclear energy, liquefied natural gas (LNG), and strategic resources. Simultaneously, the accelerated construction of AI data centers is driving demand for infrastructure lighting tailored for liquid cooling systems and server racks. In the outdoor segment, the renewal of aging infrastructure and upgrades to tunnel lighting standards continue to fuel retrofit demand. Furthermore, lighting for sports and entertainment venues, alongside smart and energy-saving solutions, are providing significant incremental growth to the market.

By region, Europe still dominates the market, followed by the North America and Asia-Pacific regions. The European LED lighting market is projected to expand at a CAGR of 2.3% from 2025 to 2030. This growth is mainly supported by the accelerating enforced adoption of energy-saving lighting retrofit solutions to rein in the rising energy costs. The Asian-Pacific market keeps up its momentum on growth, especially in the Southeastern market, with a CAGR of 3.6% throughout the same forecast period.

2. Smart Lighting Market: Transitioning from Technical Spec Wars to Scenario-based and Human-centric Values

TrendForce indicates that in 2025, the global lighting industry entered a new phase centered on Emotional Lighting and Human-Centric Lighting (HCL). Competitive dynamics are shifting away from traditional performance metrics such as luminous efficacy and communication protocols toward value propositions focused on circadian rhythm regulation and experiential scenarios.

Enabled by AI-based dimming, full-spectrum control, and Software-Defined Lighting (SDL), lighting products evolve from static hardware devices into intelligent system nodes capable of perception and adaptive learning. According to TrendForce data, the smart lighting market is projected to reach USD 21.785 billion by 2030, representing a CAGR of 13.6% from 2025 to 2030. Growth will mostly come from value enhancement through AI enablement and system upgrades in three major application scenarios: residential, outdoor, and industrial lighting.

As AI, SDL, and IoT technologies converge, lighting is transitioning from basic illumination equipment to a critical sensing and interaction node within smart living environments, urban governance systems, and industrial digitalization frameworks. Suppliers with software-hardware integration capabilities, ecosystem collaboration and scenario-aware insights will be well-positioned to gain a competitive edge in the future smart lighting market.

3. Agricultural Lighting: Deepening Regional Differentiation with Upside Potential in Europe

Replacement cycles for specialty crops have not materialized as expected, while budget constraints have led to continued downward pressure on end-product pricing. Meanwhile, new greenhouse and vertical farm construction projects have been postponed globally in 2025.

However, Europe remains comparatively resilient, supported by energy-efficiency regulations and the adoption of high photosynthetic photon efficacy (PPF/W, PPE) solutions, effectively offsetting weakness in North America and other regions. In 2025, the global LED horticultural lighting market reached USD 1.365 billion (+4% YoY).

Looking ahead to 2026, with a specific focus on greenhouse applications, accelerated LED replacement of high-pressure sodium (HPS) systems in Europe will continue to drive demand. Meanwhile, North America, Asia, and the Middle East are entering a new expansion cycle, supported by food security policies and export-oriented agricultural investments. Demand for high-PPE, spectrum-tunable, and intelligent LED lighting systems is expected to increase. TrendForce projects the market to reach USD 1.041 billion by 2030, with a CAGR of 4% from 2025 to 2030.

In the LED packaging segment, 2026 is expected to mark accelerated adoption of multi-channel spectral technologies. Most newly registered products will feature dynamic dimming functionality and higher precision control requirements, driving demand for higher-quality solutions and increased LED shipment volumes. Following previous inventory adjustments and industry consolidation, agricultural lighting LED ASPs are expected to stabilize in 2026.

4. Manufacturer Revenue: Rising Share of Smart Lighting and Segmented Application Markets

According to TrendForce's latest statistics, total revenue of the global top 20 lighting companies is projected to decline 2% YoY to USD 23.355 billion in 2025. The top five players remain unchanged: Signify, Acuity Brands, Panasonic, LEDVANCE, and Zumtobel.

TrendForce observes that at specific segments, professional segmented lighting shows advantages in terms of economies of scale. While global general lighting leaders such as Signify and LEDVANCE face revenue contraction in 2025 due to sluggish real estate markets and price competition in the traditional residential and commercial general lighting markets. Conversely, companies focusing on high-tech niche areas show steady performance.

Warom, specializing in explosion-proof and industrial lighting, is expected to achieve a 5.8% revenue growth for 2025, as it has benefited from the recovery of global energy extraction activities and the rise in industrial safety demands. Similarly, Glamox Group, which focuses on marine and offshore energy lighting, is projected to maintain a steady growth rate of 3.2%, driven by the demand for ship lighting upgrades influenced by the EU's maritime carbon emission policies.

TrendForce believes that as the effect of economies of scale is diminishing in the general lighting market, high-tech niche segments have become the key for manufacturers to maintain profitability and growth.

5. LED Packaging Market: From Price War to Stabilization and Quality Upgrade

TrendForce analysis indicates that in 2025, the lighting LED market faced intensified price erosion and low order visibility due to aggressive cost optimization strategies by international brands from Europe and the USA and concentrated adoption of high cost-performance solutions.

After prolonged margin compression, the LED packaging market is expected to exit its downward cycle in 2026. With rising upstream material costs, LED packaging prices are likely to stabilize, marking a transition from continuous price decline to a volume contraction with price stabilization environment.

Supported by sustainability policies, carbon reduction targets, and strengthened green building standards, the industry structure is undergoing qualitative transformation. The LED lighting industry is expected to complete its cyclical bottoming phase in 2026 and begin recovery in 2027. TrendForce maintains a cautiously optimistic outlook, forecasting the global lighting LED market to reach USD 3.734 billion by 2030, representing a 2025-2030 CAGR of 2.5%.

TrendForce provides in-depth insights into global LED lighting industry trends, covering market size, pricing, and regional distribution across general, smart, and horticultural lighting segments, along with analysis of developments in the LED packaging sector. The report tracks revenue and strategies of the top 20 manufacturers, examines the competitive positioning of leading players such as Signify, Acuity, Panasonic, LEDVANCE, and Opple, and outlines trends and price movements in seven major luminaire categories, supported by monthly segmented markets analysis.

TABLE OF CONTENTS

PART 1 Introduction

- 1.1 Market Research Methodology

- 1.2 Global Economics (GDP)

- 1.3 Exchange Rates

PART 2 General Lighting Market Forecast (2026-2030)

- 2.1 General LED Lighting Market Scale-Demand Market Value & Volume & ASP-by Product

- 2.2 General LED Lighting Market Scale-Demand Market Value-by Category-Lamps & Luminaries

- 2.3 General LED Lighting Market Scale-Demand Market Value-by Region

- 2.4 General LED Lighting Market Scale-Demand Market Value & Volume-by Product & by Region

- 2.5 General LED Lighting Market Scale-Demand Market Value-by Application

- 2.6 General LED Lighting Penetration Rate (Installed Based Volume)

- 2.7 General Lighting LED Market-Value & Volume-by Application

- 2.8 General Lighting LED Market-Value & Volume & ASP-by Power

- 2.9 General Lighting LED Market-Value & Volume & ASP-by Package Type

- 2.10 General Lighting LED Market-Value-by CCT

- 2.11 General Lighting LED Market-Value & Volume-by CRI

- 2.12 General Lighting LED Price

PART 3 Smart Lighting Market Forecast (2026-2030)

- 3.1 Smart LED Lighting Market Scale-Demand Market Value-by Application

- 3.2 Smart LED Lighting Market Scale-Demand Market Value-by Region

PART 4 Agricultural Lighting Market Forecast (2026-2030)

- 4.1 Horticultural LED Lighting Market Scale-Demand Market Value-by Application

- 4.2 Horticultural LED Lighting Market Scale-Demand Market Value-by Region

- 4.3 Agricultural Lighting LED Market-Value & Volume-by Chip Type

- 4.4 Agricultural Lighting LED Market-Value & Volume-by Power

- 4.5 Agricultural Lighting LED Price

- 4.6 Horticultural Lighting LED Player Revenue Ranking (2023-2025E)

PART 5 Lighting Player Revenue Ranking and Estimated

- 5.1 Top 20 Lighting Player Revenue (2023-2025E)

- 5.2 Top 10 Lighting Player Revenue Ranking by Application (2023-2025E)

- 5.3 Lighting LED Player Revenue (2023-2025E)

PART 6 LED Lighting Product Specification and Price

- 6.1 Product & Price- Filament Lamp-by Region

- 6.2 Product & Price- Street Light-by Region

- 6.3 Product & Price- Panel Light-by Region

- 6.4 Product & Price- Troffer-by Region

- 6.5 Product & Price- High/Low Bay-by Region

- 6.6 Product & Price- Explosion Proof Light-by Region

- 6.7 Product & Price- Horticultural Light- by Application

(PDF)1. 2025 Global LED Lighting Market Trend- Player Strategies

Chapter 1 Global Smart LED Lighting Market Trend

- 2026-2030 Global Smart LED Lighting Market Size Analysis

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Residential

- 2025-2026 Smart Residential Lighting Products

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Outdoor

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Industrial

- 2026-2030 Global Smart LED Lighting Market Size Analysis: by Region

- Smart Lighting Control Protocol- Bluetooth

- Smart Lighting Control Protocol- Zhaga

Chapter 2 Lighting Player Revenue and Market Strategies Analysis

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: Total Lighting

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: LED Lighting

- Lighting Player Revenue and Product Strategies

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- Chinese Lighting Player Revenue and Product Strategies

- LEDVANCE / MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF)2. LED Lighting Market Monthly Report-Segment Application and Product Analysis

- Foreword

- TrendForce's Perspective

- Market Overview and Feature Analysis

- Product Types and Application Scenario Analysis

- Mainstream Product Specifications and LED Requirement Analysis

- Manufacturer Dynamics and Competitive Landscape Analysis