|

시장보고서

상품코드

1848187

세계 및 중국의 AI 데이터센터 시장(2025년) : 전개와 전망2025 Global and China AI Data Centers: Deployment and Outlook |

||||||

가격

※ 부가세 별도

한글목차

영문목차

※ 본 상품은 영문 자료로 한글과 영문 목차에 불일치하는 내용이 있을 경우 영문을 우선합니다. 정확한 검토를 위해 영문 목차를 참고해주시기 바랍니다.

본 보고서는 미국과 중국 CSP의 AI 데이터센터 확장에 초점을 맞추고 있습니다. 미국 기업은 세계로 규모를 확대하고 국내 투자를 확대하는 반면, 중국 기업은 자체 개발 칩으로 확대하지만, 모두 향후 에너지 안정성을 우선시합니다.

주요 하이라이트:

- 미국 CSP는 컴퓨팅과 에너지의 통합을 목표로 세계 AI 데이터센터 구축에 박차를 가하고 있는 반면, 중국 CSP는 BBAT와 3대 통신사가 주도하는 듀얼 트랙 모델을 추구하고 있습니다.

- 에너지의 가용성, 송전망의 안정성, 정책 환경, 전력 비용 및 규제와의 연계에 따라 투자 속도와 전개가 좌우되는 가운데, 입지 선정에 있어 에너지의 가용성, 송전망의 안정성, 정책적 환경이 매우 중요해지고 있습니다.

- 미국의 CSP들은 AI와 HPC 수요를 지원하기 위해 수백억 달러에서 1,000억 달러에 이르는 단일 프로젝트 투자를 통해 기가 와트급 용량으로 확장하고 있습니다.

- 중국 CSP는 국가 정책에 힘입어 자체 개발 칩과 소버린 클라우드 전략을 추진하고, 해외 진출을 추진하면서 국내 핵심 빌드를 유지하고 있습니다.

- 고전압 직류(HVDC) 전원 아키텍처는 점차 전통적인 모델을 대체하고 있으며, 기가 와트 규모의 계산을 지원하고 에너지 소비를 줄이기 위해 필수적인 요소로 자리 잡고 있습니다.

샘플

목차

제1장 소개

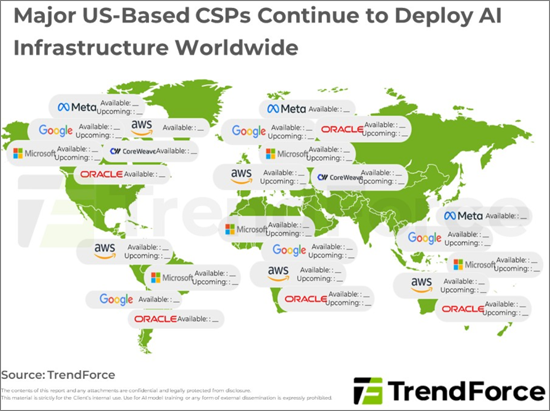

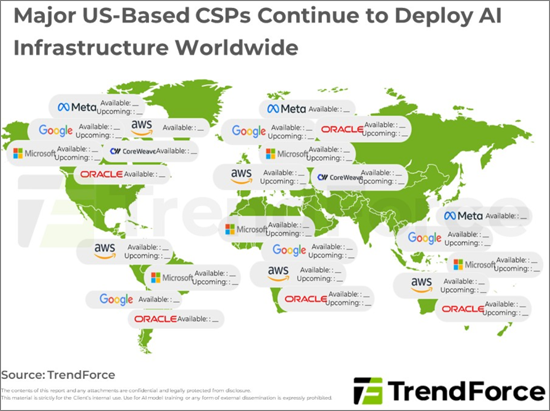

- 미국에 본사를 둔 주요 클라우드 서비스 제공업체(CSP)는 컴퓨팅 역량에서의 경쟁 우위 확보를 목표로 전 세계적으로 AI 인프라 구축을 지속하고 있습니다.

제2장 북미 주요 클라우드 서비스 제공업체(CSP)들은 기가와트(GW) 규모의 AI 데이터센터로의 전환을 적극적으로 추진하고 있으며, 향후 거점 선정 시 에너지 관련 고려 사항이 중요해지고 있습니다.

- Google의 북미 전략은 주로 전미 각지에 다수의 거점을 설립하는 것이지만, 독일의 미텐발트 계획은 에너지 공급 문제로 중단되었습니다.

- 미국 정부의 요구에 부응하여, 메타의 하이페리온 슈퍼컴퓨팅 프로젝트의 투자 목표가 500억 달러로 대폭 상향 조정되었습니다.

제3장 Oracle은 미국 최초의 주권 AI 프로젝트를 추진하며 인프라 구축에 NVIDIA GPU를 적극 활용하고 있습니다.

- 향후 3년간 Starget는 7GW의 발전 능력 달성을 목표로 하고 있으며, Oracle은 5.5GW 이상의 용량을 제공할 예정

제4장 NVIDIA는 클라우드 AI 시장에서 GPU 서버의 영향력을 강화하기 위해 OpenAI에 대한 투자를 발표했습니다.

제5장 중국의 CSP는 지정학과 국가 정책의 지침 아래 신흥 시장에서 동시에 데이터센터를 확장

- 중국 CSP에 의한 국내외 데이터센터의 적극적인 건설 BBAT

제6장 중국 주요 통신사 3곳이 주권 클라우드와 공공 건설 수요에 힘입어 국가 정책의 핵심 추진자로서 현지화된 서버와 데이터센터를 가동합니다.

- 중국 통신 사업자 중국 서버·AI 시장의 주역으로서 국가 프로젝트 출범을 담당

제7장 미국과 중국의 CSP별 AI 데이터센터에 대한 지속적인 참여를 통한 전력 인프라(HVDC 등) 개발 기회 창출

KSM 25.10.31The report highlights AI data center expansion by U.S. and Chinese CSPs. U.S. firms scale globally and invest more at home, while Chinese firms expand with self-developed chips, but both prioritize energy stability going forward.

Key Highlights:

- U.S. CSPs are accelerating global AI data center deployments with a trend toward integrated compute and energy, while Chinese CSPs pursue a dual-track model led by BBAT and the three major telecoms.

- Energy availability, grid stability, and policy environments have become critical in site selection, with power costs and regulatory collaboration shaping investment pace and deployment.

- U.S. CSPs commit single-project investments ranging from tens to hundreds of billions of dollars, scaling to gigawatt-level capacity to support AI and HPC demand.

- Chinese CSPs, backed by national policies, are advancing self-developed chips and sovereign cloud strategies, maintaining core domestic builds while expanding overseas.

- High-voltage direct current (HVDC) power architectures are gradually replacing traditional models, becoming essential to support gigawatt-scale compute and reduce energy consumption.

SAMPLE VIEW

Table of Contents

1. Introduction

- Major US-Based CSPs Continue to Deploy AI Infrastructure Worldwide, Aiming to Gain a Competitive Edge in Computing Power

2. Leading North American CSPs Are Actively Transitioning to GW-Scale AI Data Centers, with Energy-Related Considerations Becoming Critical for Future Site Selection

- Google's Strategy for North America Primarily Involves Establishing Numerous Sites Across the Country, While Its Mittenwald Project in Germany Is Canceled Due to Energy Supply Issues

- Investment Target of Meta's Hyperion Supercomputing Project Has Been Raised Significantly to US$50 Billion in Response to US Government's Needs

3. Oracle Pushes Forward with the First Sovereign AI Project in the US and Relies Heavily on NVIDIA's GPUs for Infrastructure Build-Out

- In Next Three Years, Starget Is Targeted to Reach 7GW, with Oracle Providing Over 5.5GW of Capacity

4. NVIDIA Has Announced Investment in OpenAI to Strengthen Its GPU Server Influence in the Cloud AI Market

5. Chinese CSPs Expand Data Centers in Emerging Markets Simultaneously under Geopolitics and Guidance of National Policies

- Aggressive Construction of Domestic and Overseas Data Centers by Chinese CSPs BBAT

6. Three Major Chinese Telecom Operators Actuate Localized Servers and Data Centers as Key Advocators for National Policies under Demand for Sovereign Cloud and Public Construction

- Chinese Telecom Operators Responsible for Establishment of National Projects as Key Actuators of China's Server and AI Market